|

市场调查报告书

商品编码

1939141

业务流程管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Business Process Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

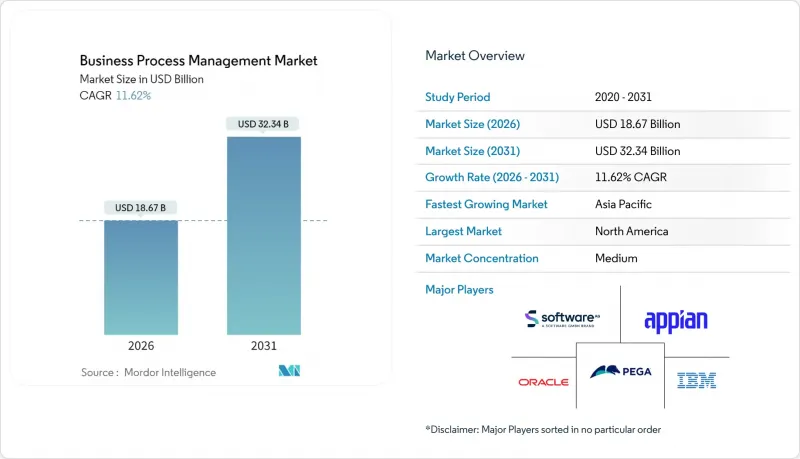

2025年业务流程管理市场价值为167.3亿美元,预计到2031年将达到323.4亿美元,高于2026年的186.7亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 11.62%。

数位化优先营运模式的扩展、人工智慧引擎与工作流程套件的整合以及监管审查的日益严格,都支撑着对端到端流程协作平台的稳定需求。云端原生交付、低程式码开发以及由流程挖掘驱动的数位双胞胎正在融合,加速大中型企业等采用者实现价值。亚太地区积极的自动化计划,以及银行、金融服务和保险(BFSI)和医疗保健行业合规计划范围的扩大,进一步推动了成长潜力。这市场领导领导者加快建立生态系统策略,以建立整合分析、规则引擎和机器人助理的超自动化堆迭。

全球业务流程管理市场趋势与洞察

加速采用低程式码/无程式码 BPM 套件推动流程自动化的普及。

到 2025 年,四分之三的 BPM 平台将整合低程式码工具,使业务团队无需深厚的编码知识即可配置工作流程。这将使计划交付时间从数月缩短至数週,并在初始采用阶段将流程效率提高 30%。公民开发人员的加入将有助于中小企业绕过有限的 IT 资源,同时透过模板和视觉化版本控制来维持管治。像 Bizagi 这样的供应商将扩展 AI 代理,使其能够根据自然语言提示自动生成模型,从而在不影响合规性的前提下扩大存取权限。

云端原生流程自动化平台提供弹性可扩充性

像 Camunda Zeebe 这样的横向扩展引擎能够随着丛集节点的增加而线性提升吞吐量,这使得一家公共部门计费处理领域的早期采用者实现了自动化覆盖率 65% 的提升。云端交付降低了资本支出,并确保了混合环境的弹性, Oracle最新季度 62 亿美元的云端收入也印证了这一点。快速连接器库加速了集成,这与云端 BPM 服务消费量年增 27% 的成长相吻合。

异质IT环境中日益增长的整合复杂性

一项针对ERP的长期研究表明,由传统ERP、云端SaaS和细分业务线应用构成的多层生态系统会增加BPM整合的范围,并使初始预算估算翻倍。 BPM协会警告称,忽视API深度、事件流和资料映射要求会增加计划失败的机率和总体拥有成本。

细分市场分析

预计到 2031 年,混合部署将占业务流程管理市场规模的 17.80%,复合年增长率最高,而云端将在 2025 年保持 61.35% 的市场份额。金融监管机构基于位置的数据规则使得混合部署成为需要本地审核追踪但又能受益于弹性分析沙箱的工作负载的最佳选择。

各组织指出,混合云的风险平衡特性是实现现代化转型的关键,无需耗费巨资大规模迁移高容量事务核心系统。例如,欧洲的 GDPR 法规要求政府机构在利用云端 AI 引擎进行文件分类的同时,将个人资料保留在本地伺服器上。美国退伍军人事务部利用 Camunda 的灵活分区技术,实现了自动化率 65% 的提升,便是一个很好的例证。随着整合平台的日趋成熟,预计到 2031 年,混合云环境在业务流程管理市场的份额将不断增长,但纯公共云端仍将是新部署的主流选择。

虽然流程自动化以 39.20% 的份额领先收入,但流程挖掘和分析预计将以 22.10% 的复合年增长率增长,成为业务流程管理市场中最具活力的细分市场,因为早期采用者转向主动异常检测和预测性工作流程调整,而这是传统任务自动化无法实现的。

此平台蓝图整合了资料探勘模组和即时推荐功能,旨在降低转换成本并缩短价值实现时间。 Celonis 在 2024 年福布斯云端 100 强榜单中的排名表明了市场对流程智慧的需求,而对 Symbio 等公司的收购则标誌着其业务拓展至设计管治和持续改进领域。儘管内容管理、案例管理和规则引擎仍将保持其重要性,但成长的主要驱动力正转向以分析为中心的编配套件。

区域分析

到2025年,北美将占据全球业务流程管理市场41.10%的份额,这主要得益于成熟的云端技术应用、先进的整合技能以及密集的AI赋能服务供应商生态系统。金融服务、公共部门和科技业占据了该地区的大部分需求,超自动化先导计画正稳步过渡到大规模计画。供应商之间的竞争十分激烈,推动功能不断更新、订阅定价模式的创新。

预计到2031年,亚太地区的复合年增长率将达到14.20%。这反映了印度、印尼和越南等国政府主导的数位转型政策,这些政策正将自动化预算导向业务流程管理(BPM)平台。 IBM的研究表明,71%的亚太企业难以实现数位投资的完全回报,因此BPM被视为端到端优化的结构框架。电信、电子商务和公共部门数位身分识别方案是早期采用BPM的重点领域。低程式码的普及进一步降低了快速成长的中小型企业的实施风险。

欧洲正经历稳定成长,GDPR、ESG报告以及新的人工智慧监管要求迫使企业将资料沿袭和同意管理纳入协调流程。在拉丁美洲,金融科技的快速发展,例如巴西拥有1.3亿用户的即时支付系统PIX,正在催生对后勤部门协调和风险分析模组的大量需求。中东和非洲则呈现选择性加速发展,各国政府的数位政府宪章为税务、海关和公民服务等职能部门的工作流程现代化提供了财政支持。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加速采用低程式码/无程式码 BPM 套件

- 云端原生流程自动化平台的需求日益增长

- 扩展整合RPA和AI的超自动化计划

- 合规主导的银行、金融服务和医疗保健产业数位转型

- 流程挖掘驱动的数位双胞胎技术在优化的应用

- 嵌入BPM解决方案的ESG报告工作流程

- 市场限制

- 异质IT环境中日益增长的整合复杂性

- 企业级部署的前期成本高昂,且投资收益(ROI) 不确定。

- 公民开发者 BPM倡议的管理技能短缺

- 由于独家流程模型标准而导致的供应商锁定风险

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素的影响

第五章 市场规模与成长预测

- 透过部署

- 云

- 本地部署

- 杂交种

- 透过解决方案

- 流程改善

- 流程自动化

- 内容和文件管理

- 个案管理

- 业务规则管理

- 整合与优化

- 流程挖掘与分析

- 按组织规模

- 大公司

- 小型企业

- 按最终用户行业划分

- 银行、金融服务和保险(BFSI)

- 政府和公共部门

- 医疗保健和生命科学

- 资讯科技/通讯

- 零售和消费品

- 製造业和工业

- 其他产业(能源、教育等)

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- OpenText Corporation

- Oracle Corporation

- Software AG

- TIBCO Software Inc.

- Fujitsu Limited

- Ultimus Inc.

- BP Logix Inc.

- Pegasystems Inc.

- Appian Corporation

- SAP Signavio(SAP SE)

- ASG Technologies Group, LLC

- Kissflow Inc.

- Nintex Global Ltd

- Comindware(CMW Lab)

- Microsoft Corporation

- Celonis SE

- UiPath Inc.

- Camunda Services GmbH

- Bizagi Group Ltd

第七章 市场机会与未来展望

The business process management market was valued at USD 16.73 billion in 2025 and estimated to grow from USD 18.67 billion in 2026 to reach USD 32.34 billion by 2031, at a CAGR of 11.62% during the forecast period (2026-2031).

Expanding digital-first operating models, the integration of AI engines into workflow suites, and heightened regulatory oversight are reinforcing steady demand for end-to-end process orchestration platforms. Cloud-native delivery, low-code development, and process-mining-enabled digital twins are converging to reduce time-to-value for both enterprise and mid-market adopters. Asia-Pacific's aggressive automation agenda, combined with the widening scope of compliance programs across BFSI and healthcare, further amplifies growth potential. Market leaders are therefore accelerating ecosystem plays that blend analytics, rules engines, and robotic assistants into unified hyper-automation stacks.

Global Business Process Management Market Trends and Insights

Accelerated adoption of low-code / no-code BPM suites democratizes process automation

Three out of four BPM platforms embed low-code tooling in 2025, allowing business teams to configure workflows without deep coding knowledge, which trims project delivery cycles from months to weeks and lifts process efficiency by 30% in early programs .Citizen-developer rollouts help SMEs bypass scarce IT resources while preserving governance through templates and visual version control . Vendors such as Bizagi extend AI agents that auto-generate models from natural-language prompts, broadening access without jeopardizing compliance.

Cloud-native process automation platforms enable elastic scalability

Horizontal scale-out engines like Camunda Zeebe maintain linear throughput growth as cluster nodes are added, which delivers 65% gains in automation coverage for early adopters in public-sector claims processing. Cloud delivery mitigates capex and ensures fault tolerance across hybrid footprints, an attribute underscored by USD 6.2 billion in Oracle's latest quarterly cloud revenue . Rapid connector libraries accelerate integration, aligning with the 27% YoY surge in cloud BPM services consumption.

Rising integration complexity in heterogeneous IT landscapes

Multi-layered ecosystems blending legacy ERPs, cloud SaaS, and niche line-of-business apps inflate BPM integration scopes and can double original budget estimates, as documented in longitudinal ERP studies. The BPM Institute warns that overlooking API depth, event streams, and data-mapping demands elevates project-failure odds and total cost of ownership.

Other drivers and restraints analyzed in the detailed report include:

- Hyper-automation initiatives integrate RPA and AI for end-to-end process intelligence

- Compliance-driven digital transformation accelerates across BFSI and healthcare

- High upfront costs and uncertain ROI for enterprise-wide roll-outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployment accounted for 17.80% of the business process management market size and is forecast to post the fastest CAGR through 2031, whereas cloud retained 61.35% share in 2025. Financial regulators' location-based data rules make hybrid the preferred pathway for workloads requiring on-premise audit trails yet benefiting from elastic analytics sandboxes.

Organizations cite hybrid's risk-balanced profile as critical to sustain modernization while avoiding expensive wholesale migration of high-volume transactional cores. Europe's GDPR mandates, for instance, push government agencies to retain personal data in local servers while tapping cloud AI engines for document classification, exemplified by the U.S. Veterans Affairs' 65% automation rate leap using Camunda's flexible partitioning. As integration fabrics mature, hybrid footprints are expected to capture a larger slice of the business process management market by 2031 without displacing pure public-cloud exemplars in greenfield contexts.

Process automation dominated revenue with 39.20% share, yet process mining and analytics is set to expand at 22.10% CAGR, making it the most dynamic segment within the business process management market. Early adopters pivot toward proactive anomaly detection and predictive workflow tuning, capabilities that conventional task automation lacks.

Platform roadmaps now bundle mining modules with real-time recommendations, thereby raising switching costs and shrinking time to savings. Celonis' ranking in the 2024 Forbes Cloud 100 underlines market appetite for process intelligence, while acquisitions such as Symbio extend reach into design governance and continuous improvement. Content management, case management, and rule engines retain specialist relevance but cede headline growth to analytics-centric orchestration suites.

The Business Process Management Market Report Segments the Industry Into by Deployment (Cloud, On-Premise), by Solution (Process Improvement, Process Automation, Content and Document Management, and More), by End-User Industry (Banking, Financial Services, and Insurance (BFSI), Government and Defense, Healthcare, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 41.10% of the business process management market size in 2025 thanks to mature cloud adoption, deep integration skill sets, and a dense ecosystem of AI-enabled service providers. Financial services, public sector, and technology verticals represent the bulk of regional demand, with hyper-automation pilots shifting steadily into scaled programs. Vendor competition is pronounced, spurring continuous feature refresh and driving subscription-pricing innovations.

Asia-Pacific is on track for a 14.20% CAGR to 2031, reflecting government-backed digital-transformation mandates across India, Indonesia, and Vietnam that funnel automation budgets into BPM platforms. IBM's survey shows 71% of Asia-Pacific enterprises struggle to unlock full digital investment returns, positioning BPM as the structural framework for end-to-end optimization. Telecommunications, e-commerce, and public-sector digital-identity schemes are early adoption hotspots; low-code access further de-risks adoption for burgeoning SMEs.

Europe maintains steady growth buoyed by GDPR, ESG reporting, and emerging AI-act requirements that force enterprises to codify data lineage and consent management into orchestrated processes. Latin America's fintech surge, exemplified by Brazil's PIX real-time payment rails serving 130 million users, creates a demand cascade for back-office orchestration and risk analysis modules. Middle East and Africa see selective acceleration where national digital-government charters bankroll workflow modernization for tax, customs, and citizen-service functions.

- IBM Corporation

- OpenText Corporation

- Oracle Corporation

- Software AG

- TIBCO Software Inc.

- Fujitsu Limited

- Ultimus Inc.

- BP Logix Inc.

- Pegasystems Inc.

- Appian Corporation

- SAP Signavio (SAP SE)

- ASG Technologies Group, LLC

- Kissflow Inc.

- Nintex Global Ltd

- Comindware (CMW Lab)

- Microsoft Corporation

- Celonis SE

- UiPath Inc.

- Camunda Services GmbH

- Bizagi Group Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated adoption of low-code / no-code BPM suites

- 4.2.2 Growing demand for cloud-native process automation platforms

- 4.2.3 Expansion of hyper-automation initiatives integrating RPA and AI

- 4.2.4 Compliance-driven digital transformation across BFSI and healthcare

- 4.2.5 Emergence of process-mining-driven digital twins for optimisation

- 4.2.6 Embedded ESG reporting workflows within BPM solutions

- 4.3 Market Restraints

- 4.3.1 Rising integration complexity in heterogeneous IT landscapes

- 4.3.2 High upfront costs and uncertain ROI for enterprise-wide roll-outs

- 4.3.3 Skills shortage to govern citizen-developer BPM initiatives

- 4.3.4 Vendor lock-in risks from proprietary process-model standards

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Solution

- 5.2.1 Process Improvement

- 5.2.2 Process Automation

- 5.2.3 Content and Document Management

- 5.2.4 Case Management

- 5.2.5 Business Rules Management

- 5.2.6 Integration and Optimisation

- 5.2.7 Process Mining and Analytics

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-User Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Government and Public Sector

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 IT and Telecommunication

- 5.4.5 Retail and Consumer Goods

- 5.4.6 Manufacturing and Industrial

- 5.4.7 Other Industries (Energy, Education, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Israel

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 United Arab Emirates

- 5.5.5.1.4 Turkey

- 5.5.5.1.5 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 IBM Corporation

- 6.4.2 OpenText Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 Software AG

- 6.4.5 TIBCO Software Inc.

- 6.4.6 Fujitsu Limited

- 6.4.7 Ultimus Inc.

- 6.4.8 BP Logix Inc.

- 6.4.9 Pegasystems Inc.

- 6.4.10 Appian Corporation

- 6.4.11 SAP Signavio (SAP SE)

- 6.4.12 ASG Technologies Group, LLC

- 6.4.13 Kissflow Inc.

- 6.4.14 Nintex Global Ltd

- 6.4.15 Comindware (CMW Lab)

- 6.4.16 Microsoft Corporation

- 6.4.17 Celonis SE

- 6.4.18 UiPath Inc.

- 6.4.19 Camunda Services GmbH

- 6.4.20 Bizagi Group Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球资料集文件工具市场报告

2026年全球资料集文件工具市场报告 房地产业务流程管理市场:按组件、应用、最终用户和部署类型划分-2026-2032年全球市场预测2026年全球业务流程文件工具市场报告2026年全球业务流程管理市场报告业务流程监控与最佳化市场:依组件、产业、部署类型与组织规模划分-2026-2032年全球预测

房地产业务流程管理市场:按组件、应用、最终用户和部署类型划分-2026-2032年全球市场预测2026年全球业务流程文件工具市场报告2026年全球业务流程管理市场报告业务流程监控与最佳化市场:依组件、产业、部署类型与组织规模划分-2026-2032年全球预测 业务流程管理 (BPM) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分

业务流程管理 (BPM) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分 全球业务流程管理市场规模、份额、趋势和成长分析报告(2026-2034年)

全球业务流程管理市场规模、份额、趋势和成长分析报告(2026-2034年) 业务流程管理 (BPM) 市场规模、份额、趋势和预测(按实施类型、组件、业务功能、组织规模、行业垂直领域和地区划分),2026-2034 年

业务流程管理 (BPM) 市场规模、份额、趋势和预测(按实施类型、组件、业务功能、组织规模、行业垂直领域和地区划分),2026-2034 年 商业活动监控软体市场规模、份额和成长分析(按部署类型、组织规模、垂直产业、功能、供应商类型和地区划分)-2026-2033年产业预测业务流程管理市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034)

商业活动监控软体市场规模、份额和成长分析(按部署类型、组织规模、垂直产业、功能、供应商类型和地区划分)-2026-2033年产业预测业务流程管理市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034)