|

市场调查报告书

商品编码

1939142

发泡聚丙烯(EPP)泡沫:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Expanded Polypropylene (EPP) Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

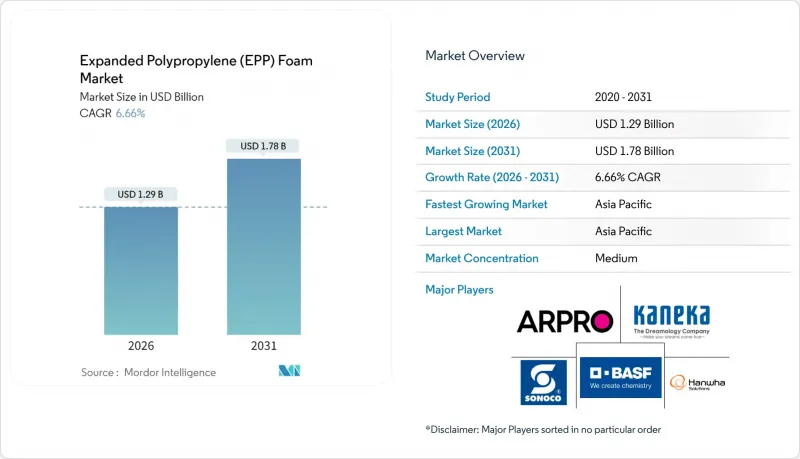

预计到 2026 年,发泡聚丙烯 (EPP) 泡沫市值将达到 12.9 亿美元,高于 2025 年的 12.1 亿美元。

预计到 2031 年,该市场规模将达到 17.8 亿美元,2026 年至 2031 年的复合年增长率为 6.66%。

更严格的车辆重量法规、物流行业的企业净零排放目标以及节能建筑维修,透过奖励轻量化设计、形状可恢復性和闭合迴路可回收性,扩大了EPP(环保塑胶)的应用范围。美国对2027年及以后车型的平均车辆二氧化碳排放量设定了更严格的限制,加速了保险桿系统中从钢和铝向吸能泡沫材料的过渡。同时,欧盟的永续产品生态设计(ESPR)法规要求使用可重复使用且经证实可回收的包装。电子商务的成长推动了对能够承受高速物流网路衝击的多层抗衝击容器的需求。此外,欧洲区域供热网路的扩张正在利用EPP绝缘的相变模组来经济高效地储存能量。垂直整合供应商之间的整合,例如Knauf收购BASF位于尼奥波伦的工厂,显示市场趋势是规模、IATF 16949认证和再生材料含量组合正成为赢得合约的决定性因素。

全球发泡聚丙烯(EPP)泡沫市场趋势与洞察

无毒且可回收的材料特性

EPP符合FDA CFR第21章和欧盟法规10/2011的要求,无需额外迁移测试即可直接接触食品,从而可在食品和药品供应链中使用可重复使用的容器。德勒斯登工业大学2024年的GePart计划证明,模塑零件的再生材料含量可超过70%,且不会影响机械强度。德国通用工业公司于2025年启动了EPP Loop项目,目标是到2030年回收德国75%的EPP废弃物。这将建立国内原料供应,降低模塑商的树脂成本。 JSP的ARPRO RE、RC和REvolution系列产品已证明其可实际应用近100%的消费后聚丙烯,满足汽车OEM厂商的范围3要求。这些措施正在将可回收性从单纯的声誉优势转变为采购的先决条件。

对轻便安全汽车的需求

美国环保署 (EPA) 针对 2027 年及以后车型製定的法规要求大幅减少二氧化碳排放,迫使汽车製造商在保险桿芯材、座椅衬垫和后备箱衬垫中用聚合物泡沫替代金属。 EPP 即使在多次衝击后仍能保持其能量吸收性能,CPSC 16 CFR Part 1203 测试证明,其峰值加速度可达 300g。 JSP 占据全球汽车 EPP 市场约 50% 的份额,并在浦那(预计 2024 年运作)和拉莫斯阿里斯佩(预计 2025 年运作)新建工厂,为现代、大众、通用和丰田等汽车品牌供应产品。韩华先进材料利用其 112 万吨的内部聚丙烯产能,即使在波动较大的周期内也能确保树脂的稳定供应,从而巩固其在车顶内衬和后备箱装饰材料领域的地位。德国 VDA 4560 标准现已限制使用一次性 EPP,除非有已记录的回收循环。这使得配备 RFID 标籤的可重复使用运输箱的需求更大。

聚丙烯价格波动

2024年至2025年间,丙烯价格波动幅度达15%至20%。这主要是由于中东地区裂解装置因不可抗力因素停产以及中国出口趋势的变化,导致原料成本上涨,而原料成本约占EPP零件价值的70%。特种轮胎边缘级丙烯价格更高,且仅由少数几家树脂生产商供应,包括BASF、LG化学、韩华和布拉斯科,这使得新车上市导致需求激增时,采购出现瓶颈。合约价格反映现货市场波动,但存在长达60天的滞后,迫使模塑商持有高成本库存,或与拒绝支付额外费用的OEM厂商重新谈判中期合约。虽然像韩华这样的垂直整合集团可以透过使用自有树脂来降低风险,但独立製造商则面临利润率压缩和产能扩张放缓的困境。

细分市场分析

至2025年,合成级聚丙烯将占发泡聚丙烯(EPP)市场的91.74%。由于原料短缺以及价格是化石基聚丙烯的三倍,生物基聚丙烯在全球生质塑胶产量中所占比例较小。这限制了其应用范围,使其仅限于仪錶板和家电机壳等高利润应用领域。因此,儘管随着回收率的提高,这种依赖性正在缓解,但发泡聚丙烯(EPP)市场仍然依赖原油基丙烯的经济状况。

JSP 和德勒斯登工业大学已证实,使用 70%工业废弃物后回收聚丙烯 (PP) 製成的零件具有可行性,表明原始设备製造商 (OEM) 无需支付生物溢价即可实现其脱碳目标。 EPP Loop 的自愿回收计画预计在 2030 年前将多达 55 千吨的废弃物转化为其他原生材料。如果该计划取得成功,再生合成聚丙烯有望取代生物基聚丙烯,成为低碳环保的首选替代品,尤其是在 ESPR 的数位化产品护照使品牌所有者能够清晰了解产品中的回收成分之后。

区域分析

预计到2025年,亚太地区将占总营收的41.65%,并在2031年之前维持7.15%的年均成长率,这主要得益于中国、印度和泰国汽车产量的成长。 JSP位于浦那的工厂新增了1.4万吨珠粒产能,缩短了现代和塔塔汽车组装的前置作业时间;其墨西哥工厂则为北美地区的本田和通用汽车供货。 KANEKA的Eperan PP生产线已在马来西亚和中国投入使用,均通过了IATF认证,进一步巩固了其对福特、大众和日产的区域供应基础。

北美正受惠于製造业回流计画和美墨加协定(USMCA)的规定,模製成型的EPP零件正被运往阿拉巴马州、田纳西州和安大略省的组装厂。韩华位于维吉尼亚和墨西哥的工厂正在将树脂整合到成品中,从而降低价格波动并减少物流排放。 Zote Forms计划在2025年第二季前在肯塔基州增设第二个低压容器,以扩大高性能等级产品的生产,满足航太客户对密度范围的严格要求。

欧洲的需求受欧洲永续包装法规 (ESPR) 和德国 VDA 4560 标准的共同影响,这两项法规共同规范了逐步淘汰一次性包装和强制回收汽车塑胶容器。克瑙夫于 2024 年收购BASF位于尼奥波伦的工厂,确保了其在欧洲 35 个地点的自有树脂珠供应,这标誌着在树脂运输成本不断上涨的情况下,企业正朝着本地自给自足的方向发展。 EPP Loop 在德国、法国和比荷卢经济联盟国家设立的回收点网路进一步支持了循环经济的实现。

南美洲虽然面积不大,但对巴西的汽车工厂而言却有着重要的战略意义。中东和非洲地区在药品低温运输配送方面也取得了新的进展,例如南非的疫苗接种宣传活动就使用了经世卫组织预先认证的可重复使用EPP(增强型人用包装)冷藏箱。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 无毒且可回收的材料特性

- 对轻便安全汽车的需求

- 电子商务对防护包装的需求激增

- 热能储存利用范例

- 可重复使用的低温运输医疗包装

- 市场限制

- 聚丙烯价格波动

- 与价格较低的EPS和其他发泡体竞争

- 生物基聚丙烯原料短缺

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 定价分析

第五章 市场规模与成长预测

- 按原料

- 合成聚丙烯

- 生物基聚丙烯

- 依表单类型

- 加工发泡聚丙烯(EPP)

- 模压EPP

- 其他发泡体

- 透过使用

- 车

- 垫材/工业包装

- 家具

- 食品包装

- HVAC

- 运动与休閒

- 其他用途

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- ALPLA

- Armacell

- BASF

- BEWi(IZOBLOK)

- Clark Foam Products Corporation

- Foampartner

- Furukawa Electric Co., Ltd.

- Hanwha Solutions

- JSP

- KK Nag Pvt. Ltd

- Kaneka Corporation

- Knauf Industries

- Polyfoam Australia Pty Ltd

- Sekisui Plastics Co.

- Signode Industrial Group Llc

- Sonoco Products Company

- SSW PearlFoam GmbH

- Woodbridge

- Zotefoams Plc

第七章 市场机会与未来展望

The expanded polypropylene foam market size in 2026 is estimated at USD 1.29 billion, growing from 2025 value of USD 1.21 billion with 2031 projections showing USD 1.78 billion, growing at 6.66% CAGR over 2026-2031.

Heightened regulatory pressure on vehicle mass, corporate net-zero agendas in logistics, and building efficiency retrofits are expanding the addressable scope for EPP by rewarding lightweight design, shape recovery, and closed-loop recyclability. U.S. fleet-average CO2 limits that tighten from Model Year 2027 onward are accelerating the shift from steel and aluminum to energy-absorbing foams in bumper systems, while the EU's Ecodesign for Sustainable Products Regulation (ESPR) requires reusable packaging with proven recyclability. E-commerce growth is amplifying the need for multi-impact protective containers that can withstand high-velocity fulfillment networks. Meanwhile, district-heating build-outs in Europe are utilizing EPP-insulated phase-change modules to store energy cost-effectively. Consolidation among vertically integrated suppliers-exemplified by Knauf's acquisition of BASF's Neopolen facility-signals a market where scale, IATF 16949 certification, and recycled-content portfolios are key factors in determining contract wins.

Global Expanded Polypropylene (EPP) Foam Market Trends and Insights

Non-Toxic and Recyclable Material Properties

EPP's compliance with FDA CFR Title 21 and EU Regulation 10/2011 permits direct food contact without additional migration tests, enabling the use of repeated-use containers in grocery and pharmaceutical supply chains. TU Dresden's 2024 GePart project demonstrated that molded parts can incorporate more than 70% recycled content without compromising their mechanical integrity. General Industries Deutschland launched the EPP Loop program in 2025 with a target to recycle 75% of German EPP waste by 2030, providing a domestic feedstock that reduces resin costs for molders. JSP's ARPRO RE, RC, and REvolution grades demonstrate the viable use of nearly 100% post-consumer polypropylene, meeting automotive OEM Scope 3 mandates. Collectively, these initiatives turn recyclability from a reputational perk into a procurement prerequisite.

Automotive Lightweighting and Safety Demand

The EPA's Model Year 2027-plus rules enforce steep CO2 reductions, pushing automakers to replace metal with polymer foams in bumper cores, seat pads, and trunk liners. EPP maintains energy absorption after multiple impacts, validated under CPSC 16 CFR Part 1203 tests that cap peak acceleration at 300 g. JSP holds about 50% global share of automotive-grade EPP and is commissioning plants in Pune (2024) and Ramos Arizpe (2025) to supply Hyundai, Volkswagen, GM, and Toyota programs locally. Hanwha Advanced Materials leverages 1.12 million t of captive polypropylene capacity to secure resin in volatile cycles, reinforcing its position on headliners and trunk trims. Germany's VDA 4560 now restricts single-use EPP unless a documented return loop exists, deepening demand for reusable transport boxes fitted with RFID tags.

Polypropylene Price Volatility

The propylene monomer price fluctuated by 15-20% during 2024-2025, following force-majeure outages at Middle East crackers and shifting Chinese export flows, which increased raw material costs that account for nearly 70% of the EPP part value. Specialty bead grades face extra premiums and are supplied by a handful of resin makers-BASF, LG Chem, Hanwha, and Braskem-creating procurement bottlenecks when auto launches spike demand. Contract prices lag behind spot market movements by up to 60 days, forcing molders to either hold costly inventory or renegotiate mid-term with OEMs that resist surcharges. Vertically integrated groups, such as Hanwha, mitigate exposure by utilizing in-house resin, whereas independents endure margin compression that slows capacity additions.

Other drivers and restraints analyzed in the detailed report include:

- Boom in E-Commerce Protective Packaging

- Thermal-Energy-Storage Use-Cases

- Competition from Cheaper EPS and Other Foams

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic grades accounted for 91.74% of the 2025 demand in the expanded polypropylene foam market size. Bio-based polypropylene accounted for a smaller portion of global bioplastics output, held back by feedstock scarcity and a price that can triple that of fossil-based polypropylene, limiting take-up to high-margin applications such as dashboards and consumer electronics housings. The expanded polypropylene foam market, therefore, remains tied to crude-derived propylene economics, although developments in recycled content are tempering that dependence.

JSP and TU Dresden have validated parts with 70% post-industrial PP, allowing OEMs to meet decarbonization goals without paying a bio-premium. EPP Loop's voluntary take-back scheme could redirect up to 55 kilotons of waste into virgin-replacement streams by 2030. If successful, recycled synthetic PP may outpace bio-PP as the preferred low-carbon lever, especially once ESPR's digital product passport makes recycled content transparent to brand owners.

The Epp Foam Market Report Segments the Industry Into Raw Material (Synthetic Polypropylene, Bio-Based Polypropylene), Foam (Fabricated EPP, Molded EPP, Other Foams), Application (Automotive, Dunnage, Furniture, Food Packaging, HVAC, Sports and Leisure, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa).

Geography Analysis

Asia-Pacific delivered 41.65% of 2025 revenue and will grow 7.15% annually to 2031 on the back of rising vehicle output in China, India, and Thailand. JSP's Pune plant adds 14 kilotons of bead capacity, cutting lead times to Hyundai and Tata assembly lines, while its Mexican site supplies Honda and GM in North America. Kaneka's Eperan PP lines across Malaysia and China, all IATF-certified, further anchor regional supply for Ford, VW, and Nissan.

North America benefits from reshoring initiatives and USMCA rules, with molded EPP parts shipped in sequence to assembly plants in Alabama, Tennessee, and Ontario. Hanwha's sites in Virginia and Mexico integrate resin into finished parts, buffering price swings and trimming logistics emissions. Zotefoams will add a second low-pressure vessel in Kentucky by Q2 2025 to scale high-performance grades for aerospace customers demanding tight density windows.

Europe's demand is shaped by ESPR and Germany's VDA 4560, which collectively phase out single-use packaging and impose take-back on automotive containers. Knauf's 2024 pickup of BASF's Neopolen plant secures captive bead supply for 35 sites across the continent, signaling a pivot to regional self-sufficiency as resin freight costs rise. EPP Loop's network of collection depots in Germany, France, and Benelux further supports closed-loop ambitions.

South America remains small but strategically important for Brazilian auto plants. The Middle East and Africa are showing nascent traction in cold-chain pharmaceutical distribution, with South African vaccine campaigns adopting reusable EPP coolers approved under the WHO prequalification.

- ALPLA

- Armacell

- BASF

- BEWi (IZOBLOK)

- Clark Foam Products Corporation

- Foampartner

- Furukawa Electric Co., Ltd.

- Hanwha Solutions

- JSP

- K K Nag Pvt. Ltd

- Kaneka Corporation

- Knauf Industries

- Polyfoam Australia Pty Ltd

- Sekisui Plastics Co.

- Signode Industrial Group Llc

- Sonoco Products Company

- SSW PearlFoam GmbH

- Woodbridge

- Zotefoams Plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Non-toxic and recyclable material properties

- 4.2.2 Automotive lightweighting and safety demand

- 4.2.3 Boom in e-commerce protective packaging

- 4.2.4 Thermal-energy-storage use-cases

- 4.2.5 Reusable cold-chain medical packaging

- 4.3 Market Restraints

- 4.3.1 Polypropylene price volatility

- 4.3.2 Competition from cheaper EPS and other foams

- 4.3.3 Scarce bio-PP feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Price Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Synthetic Polypropylene

- 5.1.2 Bio-based Polypropylene

- 5.2 By Foam Type

- 5.2.1 Fabricated EPP

- 5.2.2 Molded EPP

- 5.2.3 Other Foams

- 5.3 By Application

- 5.3.1 Automotive

- 5.3.2 Dunnage/Industrial Packaging

- 5.3.3 Furniture

- 5.3.4 Food Packaging

- 5.3.5 HVAC

- 5.3.6 Sports and Leisure

- 5.3.7 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 ASEAN Countries

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi-Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 ALPLA

- 6.4.2 Armacell

- 6.4.3 BASF

- 6.4.4 BEWi (IZOBLOK)

- 6.4.5 Clark Foam Products Corporation

- 6.4.6 Foampartner

- 6.4.7 Furukawa Electric Co., Ltd.

- 6.4.8 Hanwha Solutions

- 6.4.9 JSP

- 6.4.10 K K Nag Pvt. Ltd

- 6.4.11 Kaneka Corporation

- 6.4.12 Knauf Industries

- 6.4.13 Polyfoam Australia Pty Ltd

- 6.4.14 Sekisui Plastics Co.

- 6.4.15 Signode Industrial Group Llc

- 6.4.16 Sonoco Products Company

- 6.4.17 SSW PearlFoam GmbH

- 6.4.18 Woodbridge

- 6.4.19 Zotefoams Plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

发泡聚丙烯市场:按产品类型、製造流程、密度和应用分類的全球市场预测 – 2026–2032

发泡聚丙烯市场:按产品类型、製造流程、密度和应用分類的全球市场预测 – 2026–2032 全球发泡聚丙烯市场规模、份额、趋势和成长分析报告(2026-2034)聚丙烯硬质泡棉市场按产品类型、製造流程、密度、终端用途产业和应用划分-全球预测,2026-2032年

全球发泡聚丙烯市场规模、份额、趋势和成长分析报告(2026-2034)聚丙烯硬质泡棉市场按产品类型、製造流程、密度、终端用途产业和应用划分-全球预测,2026-2032年 2026年全球闭孔泡棉市场报告2026-2034年全球闭孔聚氨酯泡棉市场规模、份额、趋势与成长分析报告

2026年全球闭孔泡棉市场报告2026-2034年全球闭孔聚氨酯泡棉市场规模、份额、趋势与成长分析报告 发泡聚丙烯市场规模、份额及成长分析(按产品、应用及地区划分)-2026-2033年产业预测

发泡聚丙烯市场规模、份额及成长分析(按产品、应用及地区划分)-2026-2033年产业预测 发泡聚丙烯(EPP)市场规模、份额和成长分析(按类型、最终用途产业、应用和地区划分)-2026-2033年产业预测

发泡聚丙烯(EPP)市场规模、份额和成长分析(按类型、最终用途产业、应用和地区划分)-2026-2033年产业预测 全球EPP泡沫市场、市场规模及预测分析(2018-2034)

全球EPP泡沫市场、市场规模及预测分析(2018-2034) 全球 EPP 泡棉市场(按类型、应用和地区)预测(至 2030 年)

全球 EPP 泡棉市场(按类型、应用和地区)预测(至 2030 年) 发泡聚丙烯市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争细分,2020-2030 年)

发泡聚丙烯市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争细分,2020-2030 年)