|

市场调查报告书

商品编码

1939156

生质乙醇:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Bioethanol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

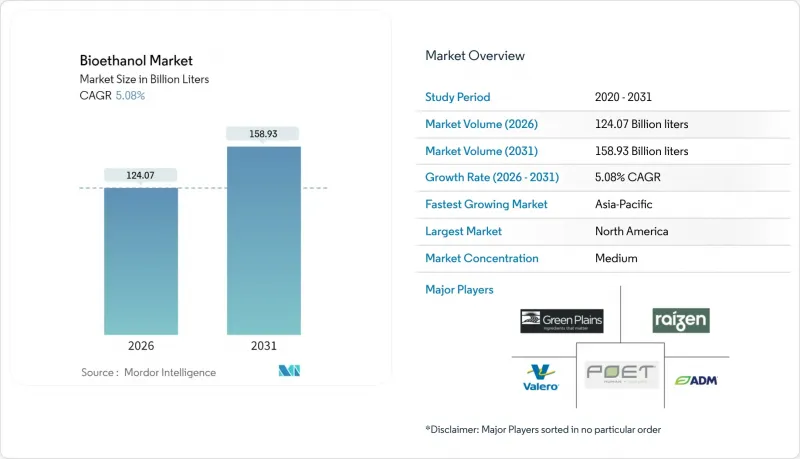

2025年生质乙醇市场价值为1,180.7亿公升,预计到2031年将达到1,589.3亿公升,而2026年为1,240.7亿升。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.08%。

对E10-E20混合燃料的持续政策支持、对乙醇喷射机燃料日益增长的兴趣以及具有成本优势的原料供应,都支撑着这一增长轨迹,即便轻型车辆电气化进程仍在继续。北美玉米基生产能力、巴西甘蔗的柔软性以及来自中东投资者的新资本流入,都在增强供应安全。同时,亚太地区各国政府正迅速推动积极的混合燃料目标,以扩大区域需求基础,炼油商也正在采用低碳乙醇以满足日益严格的ESG指标。这些因素共同确保了生质乙醇市场能够抵御其他交通运输脱碳路径的竞争。

全球生质乙醇市场趋势与洞察

全球强制混合使用E10和E20燃料

更严格的掺混规定创造了可预测的基本负载需求,使生质乙醇市场免受原油价格波动的影响,同时确保产能扩张。日本全国范围内的E10推广和E20试点项目、巴西27%的掺混比例上限柔软性以及印度加速推进的30%目标,共同促进了年度采购量的增长,并鼓励了新的工厂投资。监管机构透过燃料品质标准、国内采购规则和进口限制来支持合规,确保掺混目标转化为实际供应,而不是纸面上的积分。这些政策正在将生质乙醇市场转变为国家能源安全战略的重要组成部分,即便电气化进程不断推进。

炼油厂面临的碳减排和ESG压力

面对投资者的密切关注和日益严格的碳排放标准,炼油商开始将低碳强度生质乙醇视为策略差异化优势,而不仅仅是合规因素。加州修订后的2024年低碳燃料标准强化了碳排放标准,并鼓励基于ISCC等认证体系的供应。欧盟修订后的可再生能源指令也同样鼓励使用来源可追溯且永续的乙醇。为此,BP等公司斥资14亿美元收购了邦吉生物能源公司,实现了上游工程的垂直整合,并一举实现了原料安全和全生命週期排放管理。在可再生燃料含量低于强制性标准的市场,会产生溢价需求,从而维持有利于低碳生产商的价格差异。

轻型车辆的快速电气化

电动车的日益普及正在降低主要市场对汽油的需求上限。在挪威,2024年新车销量中将有94%是电动车,而在中国,这一比例已超过35%。国际能源总署(IEA)预测,到2030年,电动车在全球轻型车市场的份额将达到30%。因此,炼油商面临调合原料来源日益减少的困境,生质乙醇生产商被迫转向航空燃料、重型运输和出口主导策略。由于新兴国家电动车普及速度缓慢,区域需求差异依然存在,这为生质乙醇市场的地理多元化提供了机会。

细分市场分析

到2025年,玉米基生物乙醇产量将占生质乙醇市场规模的58.12%,这主要得益于美国中西部地区和巴西马托格罗索州的扩张,以及成熟的铁路和沿海运输网络。生产商正利用酵素技术的进步和产品特定的增值措施(特别是将酒糟用作牲畜饲料和将碳捕获技术应用于饮料生产)来降低单位成本并提高碳排放评分。中西部地区对碳捕获和地下储存丛集的持续投资进一步提升了生物乙醇全生命週期性能的可靠性。

预计到2031年,小麦乙醇的复合年增长率将达到5.45%,成为成长最快的主要原料。欧洲企业正利用奖励诱因促进国内粮食多样化,而澳洲的丰收季则提供了出口机会。蛋白质溢价的上涨使小麦酒糟成为极具吸引力的牲畜饲料,抵消了淀粉成本上涨的影响。高浓度发酵和分馏等技术创新提高了工厂运转率,增强了小麦在生质乙醇市场的竞争力。

其他原料,如甘蔗、木薯和新兴的木质纤维素原料,可提供策略性的利基供应,并对冲天气相关的作物产量波动。巴西的甘蔗透过甘蔗渣汽电共生保持结构性的成本优势,而印尼的尼帕棕榈和墨西哥的龙舌兰试点计画旨在将未充分利用的土地投入生产。这种多元化有助于缓解价格波动,并响应政策制定者减少粮食作物替代方案的呼吁。

生质乙醇市场报告按原料类型(甘蔗、玉米、小麦及其他原料)、应用领域(汽车及交通运输、食品饮料、製药、化妆品及个人护理、其他应用领域)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行细分。市场预测以公升为单位。

区域分析

2025年,北美将维持全球55.10%的玉米乙醇产量份额,这得益于其完善的玉米基础设施、稳定的可再生燃料标准(RFS)目标以及各州层面的低碳燃料倡议。生产商正在整合碳捕获、直接空气捕获和管道网络,以降低玉米乙醇的碳排放强度,使其符合高价值碳信用市场的准入标准。加拿大正充分利用其小麦和玉米原料产业丛集的优势,而墨西哥不断增长的需求正在吸收来自美国的出口,从而加强洲际贸易流量,并稳定区域平衡。

预计到2031年,亚太地区将以5.74%的复合年增长率实现最高的生物乙醇市场成长,主要得益于印度30%的掺混目标以及中国的进口需求将推动消费。亚太地区各国政府正将生质乙醇的推广视为提高农村收入和节约外汇的途径,并鼓励当地投资建造多种原料的生物炼製设施。泰国、菲律宾和越南正根据其农业现代化计画推行掺混比例政策,而印尼则正在试行以尼帕棕榈为原料的乙醇生产路线,以规避粮食作物供应的限制。

欧洲优先考虑永续性认证,并优先考虑符合严格温室气体减排标准的残余乙醇。德国和法国的配额制度支撑了需求,而英国的可再生运输燃料义务(RTFO)则优先考虑永续航空燃料(SAF),间接促进了从乙醇向喷射机燃料的过渡。在巴西的主导,南美洲正迎来外资流入,特别用于扩大甘蔗、玉米和汽电共生综合资产,其中包括阿联酋135亿美元的投资。非洲市场仍处于小众阶段,但由于联合国粮农组织的清洁烹饪解决方案计划,该计划将乙醇定位为家庭能源替代方案,非洲市场正在成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球有益的E10-E20混合燃料强制令

- 炼油厂面临的碳减排和ESG压力

- 美国玉米和巴西甘蔗的成本优势

- 辛烷值需求推动了乙醇作为芳烃替代品的发展。

- 航空业对乙醇衍生永永续航空燃料(SAF)的需求趋势

- 市场限制

- 轻型车辆的快速电气化

- 粮食与燃料、土地利用之争

- 基于间接土地利用变化的碳强度评估方法的收紧

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依原料类型

- 甘蔗

- 玉米

- 小麦

- 其他成分

- 透过使用

- 汽车和运输设备

- 食品/饮料

- 製药

- 化妆品和个人护理

- 其他用途(燃料电池、发电)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Abengoa

- ADM

- Alto Ingredients Inc.

- Blue Biofuels Inc.

- BP plc

- Cenovus Energy

- Cristalco

- CropEnergies AG

- Ethanol Technologies

- GranBio Investimentos SA

- Green Plains Inc.

- Henan Tianguan Group Co. Ltd

- Jilin Fuel Ethanol Co. Ltd

- KWST

- Lantmannen

- POET LLC

- Raizen

- SEKAB

- SUNCOR Energy Inc.

- Tereos

- Valero

- VERBIO Vereinigte Bioenergie AG

第七章 市场机会与未来展望

The Bioethanol Market was valued at 118.07 billion litres in 2025 and estimated to grow from 124.07 billion litres in 2026 to reach 158.93 billion litres by 2031, at a CAGR of 5.08% during the forecast period (2026-2031).

Continued policy backing for E10-E20 blends, growing interest in ethanol-to-jet fuel, and cost-advantaged feedstock supply underpin this trajectory even as light-duty vehicle electrification advances. North American corn-based capacity, Brazilian sugarcane flexibility, and fresh capital inflows from Middle Eastern investors reinforce supply security. Meanwhile, Asia-Pacific governments fast-track aggressive blending targets that deepen regional demand pools, and refiners pursue low-carbon ethanol to satisfy tightening ESG metrics. Together, these factors sustain the bioethanol market's resilience against competing transport decarbonization pathways.

Global Bioethanol Market Trends and Insights

Favourable Global E10-E20 Blending Mandates

Strengthened blending requirements are creating predictable baseload demand that insulates the bioethanol market from crude price swings while locking in capacity expansion. Japan's nationwide E10 roll-out and pilot E20 zones, Brazil's 27% ceiling flexibility, and India's accelerated 30% target together lift annual offtake volumes and encourage new plant investment. Regulatory agencies back compliance through fuel-quality standards, domestic content rules, and import controls, ensuring blend targets translate into physical deliveries rather than paper credits. These policies turn the bioethanol market into a structural element of national energy security strategies even as electrification gains momentum.

Carbon-Reduction and ESG Pressure on Refiners

Refiners facing investor scrutiny and stringent carbon standards now view low-intensity bioethanol as a strategic differentiator instead of a mere compliance component. California's 2024 Low Carbon Fuel Standard update tightened carbon benchmarks, rewarding supplies certified under schemes such as ISCC. The EU's revised Renewable Energy Directive likewise privileges traceable, sustainably sourced ethanol. In response, companies like BP vertically integrated upstream via the USD 1.4 billion acquisition of Bunge Bioenergia, securing feedstock and lifecycle emission control in one step. Premium demand emerges in markets where renewable-content uptake exceeds mandate floors, sustaining price spreads favorable to lower-carbon producers.

Rapid Electrification of Light-Duty Vehicles

Soaring EV adoption trims gasoline demand ceilings in core markets. Norway hit 94% EV penetration for 2024 new car sales, China surpassed 35%, and the IEA forecasts a 30% global light-vehicle share by 2030. As a result, refiners face shrinking blend pools, compelling bioethanol producers to pivot toward aviation, heavy-duty transport, and export-led strategies. Regional demand divergence persists because emerging economies lag in vehicle electrification, creating opportunities for geographic diversification within the bioethanol market.

Other drivers and restraints analyzed in the detailed report include:

- Feedstock Cost Advantage in U.S. Corn and Brazil Sugarcane

- Octane Demand Spurring Ethanol as Aromatic Substitute

- Food-vs-Fuel and Land-Use Controversy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corn-based output contributed 58.12% of the bioethanol market size in 2025, anchored by the U.S. Midwest, Brazil's Mato Grosso expansion, and well-established rail and barge logistics. Producers leverage enzyme advances and co-product valorization, notably distillers' grains for livestock feed and captured CO2 for beverages, to compress unit costs and improve carbon scores. Continuing investments in carbon capture and underground storage clusters across the Midcontinent further enhance lifecycle performance credentials.

Wheat ethanol is projected to record a 5.45% CAGR through 2031, the fastest growth among mainstream feedstocks. European players harness policy incentives for domestic grain diversification, while Australia's bumper wheat cycles offer export opportunities. Rising protein premiums make wheat distillers' grains attractive to livestock feeders, offsetting higher starch costs. Technology breakthroughs enabling high-gravity fermentation and fractional distillation improve plant utilization rates, strengthening wheat's competitiveness within the bioethanol market.

Other feedstocks, such as sugarcane, cassava, and emerging lignocellulosic sources, supply niche but strategic volumes that hedge against weather-induced crop swings. Brazilian sugarcane retains a structural cost edge via bagasse-fired cogeneration, while Indonesia's nipa palm and Mexico's agave pilots aim to unlock marginal-land production. Such diversification dampens price volatility and aligns with policymakers' pressure to minimize food-crop displacement.

The Bioethanol Market Report is Segmented by Feedstock Type (Sugarcane, Corn, Wheat, and Other Feedstock), Application (Automotive and Transportation, Food and Beverages, Pharmaceutical, Cosmetics and Personal Care, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Liters).

Geography Analysis

North America maintained 55.10% of global volume in 2025 thanks to entrenched corn infrastructure, stable Renewable Fuel Standard targets, and supportive state-level Low Carbon Fuel initiatives. Producers integrate carbon capture, direct air capture, and pipeline networks that compress the carbon intensity of corn ethanol, qualifying it for high-value credit markets. Canada leverages wheat and corn feedstock clusters, whereas Mexico's demand uptick absorbs U.S. exports, reinforcing continental trade flows that stabilize regional balance.

Asia-Pacific records the highest forecast CAGR at 5.74% through 2031 as India's 30% blend target and China's import appetite amplify consumption. Regional governments frame bioethanol expansion as rural income support and foreign-exchange savings, encouraging local investment in multi-feedstock biorefineries. Thailand, the Philippines, and Vietnam advance blend mandates aligned with agricultural modernization plans, while Indonesia pilots nipa-to-ethanol routes to sidestep food-crop constraints.

Europe emphasizes sustainability certification and favors residue-based ethanol that fulfills stringent greenhouse-gas savings thresholds. Quota systems in Germany and France anchor demand, and the United Kingdom's Renewable Transport Fuel Obligation prioritizes SAF, indirectly boosting ethanol-to-jet pathways. South America, dominated by Brazil, attracts foreign capital, notably the UAE's USD 13.5 billion commitment, to expand integrated assets that marry sugarcane, corn, and cogeneration. Middle East and Africa remain niche but rising, catalyzed by FAO programs for clean cooking solutions that position ethanol as a household energy alternative.

- Abengoa

- ADM

- Alto Ingredients Inc.

- Blue Biofuels Inc.

- BP p.l.c.

- Cenovus Energy

- Cristalco

- CropEnergies AG

- Ethanol Technologies

- GranBio Investimentos SA

- Green Plains Inc.

- Henan Tianguan Group Co. Ltd

- Jilin Fuel Ethanol Co. Ltd

- KWST

- Lantmannen

- POET LLC

- Raizen

- SEKAB

- SUNCOR Energy Inc.

- Tereos

- Valero

- VERBIO Vereinigte Bioenergie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Favourable global E10-E20 blending mandates

- 4.2.2 Carbon-reduction and ESG pressure on refiners

- 4.2.3 Feedstock cost advantage in U.S. corn and Brazil sugarcane

- 4.2.4 Octane demand spurring ethanol as aromatic substitute

- 4.2.5 Airline demand for ethanol-to-jet SAF pathways

- 4.3 Market Restraints

- 4.3.1 Rapid electrification of light-duty vehicles

- 4.3.2 Food-vs-fuel and land-use controversy

- 4.3.3 Stricter ILUC-based carbon-intensity scoring

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Feedstock Type

- 5.1.1 Sugarcane

- 5.1.2 Corn

- 5.1.3 Wheat

- 5.1.4 Other Feedstock

- 5.2 By Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Food and Beverages

- 5.2.3 Pharmaceutical

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Other Applications (Fuel Cells, Power Generation)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Abengoa

- 6.4.2 ADM

- 6.4.3 Alto Ingredients Inc.

- 6.4.4 Blue Biofuels Inc.

- 6.4.5 BP p.l.c.

- 6.4.6 Cenovus Energy

- 6.4.7 Cristalco

- 6.4.8 CropEnergies AG

- 6.4.9 Ethanol Technologies

- 6.4.10 GranBio Investimentos SA

- 6.4.11 Green Plains Inc.

- 6.4.12 Henan Tianguan Group Co. Ltd

- 6.4.13 Jilin Fuel Ethanol Co. Ltd

- 6.4.14 KWST

- 6.4.15 Lantmannen

- 6.4.16 POET LLC

- 6.4.17 Raizen

- 6.4.18 SEKAB

- 6.4.19 SUNCOR Energy Inc.

- 6.4.20 Tereos

- 6.4.21 Valero

- 6.4.22 VERBIO Vereinigte Bioenergie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

生物液体热电发电市场:依技术、容量范围、原料、应用和最终用途划分-2026-2032年全球市场预测生质乙醇市场:依原料、製造技术、混合类型、等级、通路和最终用途划分-2026-2032年全球市场预测生物丁醇市场:2026-2032年全球市场预测(依产品类型、原料、生产流程、应用、终端用户产业及通路划分)

生物液体热电发电市场:依技术、容量范围、原料、应用和最终用途划分-2026-2032年全球市场预测生质乙醇市场:依原料、製造技术、混合类型、等级、通路和最终用途划分-2026-2032年全球市场预测生物丁醇市场:2026-2032年全球市场预测(依产品类型、原料、生产流程、应用、终端用户产业及通路划分) 生物丁醇市场报告:按原料、应用、终端用户产业和地区划分(2026-2034 年)生质乙醇市场规模、份额、趋势和预测:按类型、燃料混合物、生产方法、最终用途行业和地区划分,2026-2034年生质乙醇酵母市场:2026-2032年全球市场预测(按产品类型、配方类型、技术、应用和最终用户产业划分)

生物丁醇市场报告:按原料、应用、终端用户产业和地区划分(2026-2034 年)生质乙醇市场规模、份额、趋势和预测:按类型、燃料混合物、生产方法、最终用途行业和地区划分,2026-2034年生质乙醇酵母市场:2026-2032年全球市场预测(按产品类型、配方类型、技术、应用和最终用户产业划分) 2026年全球生质乙醇酵母市场报告2026年全球生质乙醇市场报告生质乙醇交通运输市场:依原料、纯度、製造技术、应用及通路划分-2026-2032年全球市场预测

2026年全球生质乙醇酵母市场报告2026年全球生质乙醇市场报告生质乙醇交通运输市场:依原料、纯度、製造技术、应用及通路划分-2026-2032年全球市场预测 生质乙醇产能、产量、市场规模、平均价格及预测(2018-2034 年)

生质乙醇产能、产量、市场规模、平均价格及预测(2018-2034 年)