|

市场调查报告书

商品编码

1939571

气雾剂涂料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Aerosol Paints - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

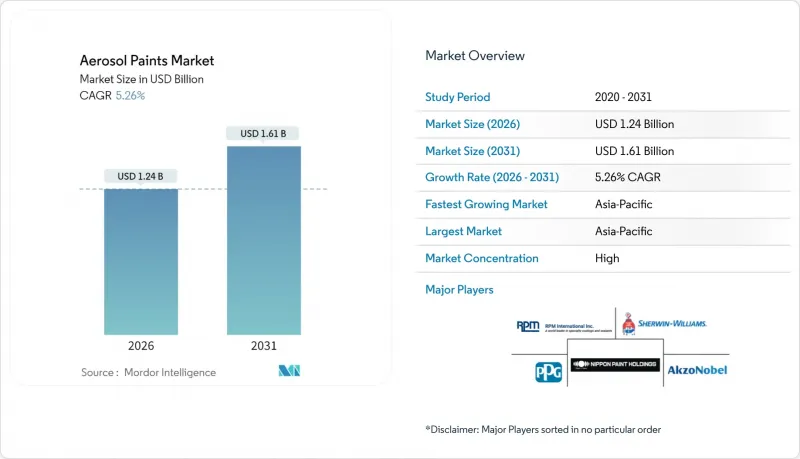

2025年气雾剂涂料市场价值为11.8亿美元,预计到2031年将达到16.1亿美元,高于2026年的12.4亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.26%。

建设业的復苏、汽车客製化需求的成长以及蓬勃发展的DIY文化正在推动销售成长,而树脂技术和自动化点胶系统的持续创新则支撑了高端定价。製造商正在加速向水性涂料转型,以满足日益严格的VOC法规要求,同时又不影响涂料质量,其中无需喷涂室的特种双组分聚氨酯体係正日益受到青睐。日益激烈的竞争主要围绕着技术整合、永续性以及旨在扩大地域覆盖范围和加强在高利润细分市场准入的定向併购展开。

全球气雾剂涂料市场趋势与洞察

住宅和商业建设活动增加

随着新建住宅和维修计划中对精准修补涂料的需求不断增长,气雾涂料市场正迅速渗透到新建和维护阶段。承包商倾向于使用气雾剂来匹配运作中区域的颜色,从而减少停工时间和过喷现象。製造商也积极回应,推出针对不同基材的专用涂料,兼具快速固化和耐磨性,确保在包括石材、复合材料和金属设备在内的各种材料上都能保持稳定的性能。区域监管协调简化了产品核可,并推广统一的标籤标准,使跨国计划实施更加便利。

汽车改装与重新喷漆文化的兴起

对第1151号规则的修订暂时放宽了挥发性有机化合物(VOC)的限制,从而允许高性能气雾剂修补漆的持续供应。科思创的透明涂层对比测试表明,奈米改性双组分聚氨酯在耐刮擦性方面具有优越性。即使汽车销售趋于平稳,气雾剂的需求依然强劲,这主要得益于北美和欧洲车迷对轮毂、卡钳和装饰件的个人化改装。在新兴市场,个人化是身份的象征,催生了区域色彩搭配和针对热带气候量身定制的抗紫外线配方。汽车製造商正与涂料供应商合作,提供经经销商认可的气雾剂补漆套装,既保障了保固范围,又获得了售后市场的收入。

严格的挥发性有机化合物(VOC)含量规定

加州2023-2031年的法规降低了挥发性有机化合物(VOC)的允许含量并禁止使用芳香族溶剂,这需要耗费大量成本进行配方调整。美国环保署(EPA)已将合规期限延长至2027年1月,但产业测试週期仍很短。加拿大2024年的法规适用于130种产品,并要求每个司法管辖区使用不同的产品编号(SKU)。配方调整会增加原料的复杂性,并可能降低光泽度和覆盖率,尤其是在冷喷涂环境下。然而,采用先进水性化学技术的领先企业预计,一旦性能统一,就能简化全球部署流程。

细分市场分析

至2025年,丙烯酸配方将占气雾涂料市场32.47%的份额,预计到2031年将维持5.22%的复合年增长率。其兼具附着力、紫外线稳定性和低VOC相容性等优点,使其在建筑和DIY领域广泛应用。聚氨酯系统在汽车和工业领域占据高端地位,双组分气雾剂套装可提供工厂级的耐久性。环氧树脂体系儘管成长放缓,但仍是重型防腐蚀涂料的必备之选,而醇酸树脂体系则在偏好传统涂饰製程的工匠中拥有一定的市场份额。 「其他」类别中的混合奈米增强树脂具有红外线反射率和加速固化等特殊性能,促使供应商采用模组化配方平台,从而实现高效的客製化。

为了应对监管审查,丙烯酸树脂供应商正加大对自交联乳化的研发投入。这款乳液既能保持溶剂型涂料的硬度,又能实现水洗,从而缩小了其环境足迹。通用单体骨架使得气雾剂和散装喷涂剂型之间的快速转换成为可能,提高了规模经济效益。适用于塑胶、金属和石材等多种基材的压克力颜料正日益受到青睐,因为DIY用户对全表面应用的需求不断增长。同时,聚氨酯开发商正致力于控制反应延迟并延长活化后的适用期,这使其对在偏远地区工作的车辆维修人员更具吸引力。

气雾剂涂料市场报告按树脂类型(丙烯酸树脂、环氧树脂、聚氨酯树脂、醇酸树脂及其他树脂)、技术类型(溶剂型、水性)、终端用户行业(汽车、建筑、木材及包装、运输、DIY及其他终端用户行业)和地区(亚太地区、北美地区、欧洲及其他地区)进行细分。市场预测以美元以金额为准。

区域分析

到2025年,亚太地区将占全球市场份额的45.10%,复合年增长率达5.62%。中国的大型计划将支撑建筑需求,而印度的中产阶级家庭则推动了DIY计画对金属色和粉红彩色係涂料的需求。立邦涂料以23亿美元收购AOC,以及在印度的扩张,标誌着该公司在该地区拥有战略布局。政府基础建设支出即使在消费週期性低迷时期也能提供稳定的需求基础。

北美浓厚的DIY文化为品牌商和自有品牌都提供了稳定的现金流。虽然大规模翻新会受到通货膨胀的影响,但对小规模装饰性修缮的需求仍然强劲。

在欧洲市场,旨在标准化测试方法和共用水性涂料转型最佳实践的联盟正在推动技术领先地位的形成。公共资金正在推动使用低全球暖化潜值推进剂的先导计画,而消费者的环保标籤正在影响他们的购买选择。为加强地缘政治动盪后的供应链韧性,製造商正转向近岸采购关键原料,这正在潜移默化地调整成本结构和区域产能分配。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 住宅和商业建设活动增加

- DIY维修和装饰计划的兴起

- 汽车改装与重新喷漆文化的兴起

- 一种新型双组分聚氨酯气雾剂系统可实现无需喷漆房的维修

- 用于老化基础设施的奈米陶瓷喷涂(直接金属涂层)

- 市场限制

- 严格的挥发性有机化合物(VOC)含量规定

- 根据《基加利修正案》逐步淘汰氢氟碳化合物推进剂

- 压力涂料储存的防火规定

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 通过树脂

- 丙烯酸纤维

- 环氧树脂

- 聚氨酯

- 醇酸

- 其他树脂

- 透过技术

- 溶剂型

- 水溶液

- 按最终用户行业划分

- 车

- 建筑学

- 木材/包装

- 运输

- DIY

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Aeroaids Corporation

- Akzo Nobel NV

- BASF

- Kobra Paint

- Masco Corporation

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- RPM International Inc.

- RusTA

- The Sherwin-Williams Company

第七章 市场机会与未来展望

The Aerosol Paints Market was valued at USD 1.18 billion in 2025 and estimated to grow from USD 1.24 billion in 2026 to reach USD 1.61 billion by 2031, at a CAGR of 5.26% during the forecast period (2026-2031).

Construction recovery, automotive personalization, and a flourishing DIY culture fuel volume growth, while continuous resin innovation and automated dispensing systems support premium pricing. Manufacturers accelerate water-borne transitions to meet stricter VOC rules without sacrificing finish quality, and specialty 2-K polyurethane systems gain traction for booth-free repairs. Competitive intensity pivots around technology integration, sustainability credentials, and targeted mergers and acquisitions that broaden geographic footprints and boost access to high-margin niches.

Global Aerosol Paints Market Trends and Insights

Rising Residential and Commercial Construction Activities

Demand accelerates as new housing and renovation projects specify precision touch-up coatings, allowing the aerosol paints market to penetrate both initial build and maintenance phases. Contractors favor aerosols for color-matching occupied spaces, reducing downtime and overspray. Manufacturers respond with substrate-specific blends that combine rapid cure with abrasion resistance, ensuring consistent performance across masonry, composites, and metal fixtures. Regulatory alignment across regions is streamlining product approvals and driving uniform label standards that further ease cross-border project execution.

Growing Automotive Customisation and Refinishing Culture

Rule 1151 amendments grant temporary VOC leniency, enabling continued supply of high-performance refinishing aerosols. Covestro's clearcoat benchmarking validates nano-modified 2-K polyurethane dominance in scratch resistance. Enthusiasts in North America and Europe customize wheels, calipers, and trim, driving steady aerosol volumes despite plateauing vehicle sales. In emerging markets, personalization indicates social status, fostering localized color palettes and UV-stable formulations tailored to tropical climates. OEMs collaborate with paint suppliers to launch dealer-approved aerosol touch-up kits that protect warranty coverage and capture aftermarket revenue.

Stringent VOC-Content Regulations

California's 2023-2031 rules cut allowable VOC levels and ban aromatic solvents, compelling costly reformulations. The U.S. EPA deferred compliance to January 2027, yet industry testing cycles remain compressed. Canada's 2024 limits span 130 products, requiring distinct SKUs per jurisdiction. Reformulation increases raw-material complexity and may reduce gloss or coverage, particularly in cold-spray environments. However, early movers leveraging advanced water-borne chemistries anticipate global rollout efficiencies once performance parity is achieved.

Other drivers and restraints analyzed in the detailed report include:

- Emerging 2-K Polyurethane Aerosol Systems Enabling Booth-Free Repairs

- Nano-Ceramic Direct-to-Metal Sprays for Ageing Infrastructure

- Phase-Down of HFC Propellants Under Kigali Amendment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic formulations held the leading 32.47% share of the aerosol paints market in 2025, with a parallel 5.22% CAGR to 2031. Their balance of adhesion, UV stability, and low-VOC adaptability underpins widespread acceptance across architectural and DIY channels. Polyurethane earns premium positioning in automotive and industrial sectors, where two-component aerosol kits deliver factory-grade durability. Epoxy systems remain essential for heavy-duty anticorrosion protection despite slower growth, while alkyd retains niche loyalty among craftsmen who favor traditional finishes. Hybrid nano-enhanced resins in the "other" category promise targeted gains such as infrared reflectivity and accelerated cure, nudging suppliers toward modular formulation platforms that streamline custom orders.

In response to regulatory scrutiny, acrylic suppliers invest in self-crosslinking emulsions that deliver solvent-borne hardness with water clean-up, shrinking the environmental gap. Shared monomer backbones allow rapid pivoting between aerosol and bulk-spray formats, improving economies of scale. As DIY users demand all-surface products, multi-substrate acrylics compatible with plastics, metals, and masonry gain prominence. Concurrently, polyurethane developers tackle latency management to extend post-activation pot life, broadening appeal to fleet maintenance crews operating in remote locations.

The Aerosol Paints Report is Segmented by Resin (Acrylic, Epoxy, Polyurethane, Alkyd, and Other Resins), Technology (Solvent-Borne, Water-Borne), End-User Industry (Automotive, Architectural, Wood and Packaging, Transportation, Do-It-Yourself (DIY), and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 45.10% global share in 2025 and advances at 5.62% CAGR. China's mega-projects sustain architectural demand, while India's middle-class households spur growth in DIY metallic and pastel shades. Nippon Paint's USD 2.3 billion AOC acquisition and Indian expansions illustrate strategic anchoring in the region. Government infrastructure outlays infuse stable volume pipelines even during cyclical consumer dips.

North America benefits from an entrenched DIY culture, generating steady cash flow for branded lines and private labels alike. Although inflation weighs on big-ticket remodeling, smaller decor touch-ups remain resilient.

Europe's market fosters technology leadership through collaborative compliance consortia that standardize test methods and share best practices on water-borne conversion. Public funding incentivizes pilot projects employing low-GWP propellants, while consumer eco-labels sway purchase choices. Supply-chain resilience exercises following geopolitical disruptions push manufacturers to near-shore key raw materials, subtly reshaping cost structures and regional capacity allocation.

- Aeroaids Corporation

- Akzo Nobel N.V.

- BASF

- Kobra Paint

- Masco Corporation

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- RPM International Inc.

- RusTA

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Residential and Commercial Construction Activities

- 4.2.2 Increasing DIY Refurbishment and Decor Projects

- 4.2.3 Growing Automotive Customisation and Refinishing Culture

- 4.2.4 Emerging 2-K Polyurethane Aerosol Systems Enabling Booth-Free Repairs

- 4.2.5 Nano-Ceramic Direct-to-Metal Sprays for Ageing Infrastructure

- 4.3 Market Restraints

- 4.3.1 Stringent VOC-Content Regulations

- 4.3.2 Phase-Down of HFC Propellants Under Kigali Amendment

- 4.3.3 Fire-Code Restrictions on Pressurised Paint Storage

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Alkyd

- 5.1.5 Other Resins

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Architectural

- 5.3.3 Wood and Packaging

- 5.3.4 Transportation

- 5.3.5 Do-It-Yourself (DIY)

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aeroaids Corporation

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 BASF

- 6.4.4 Kobra Paint

- 6.4.5 Masco Corporation

- 6.4.6 Nippon Paint Holdings Co., Ltd.

- 6.4.7 PPG Industries Inc.

- 6.4.8 RPM International Inc.

- 6.4.9 RusTA

- 6.4.10 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

气雾剂涂料市场:2026-2032年全球市场预测(依应用、销售管道、推进剂类型、配方类型及价格范围划分)

气雾剂涂料市场:2026-2032年全球市场预测(依应用、销售管道、推进剂类型、配方类型及价格范围划分) 气雾剂涂料市场规模、份额及成长分析(按产品、应用和地区划分):产业预测(2026-2033 年)

气雾剂涂料市场规模、份额及成长分析(按产品、应用和地区划分):产业预测(2026-2033 年) 全球气溶胶涂料市场

全球气溶胶涂料市场