|

市场调查报告书

商品编码

1939596

亚太地区软质包装:市占率分析、产业趋势与统计、成长预测(2026-2031)Asia-Pacific Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

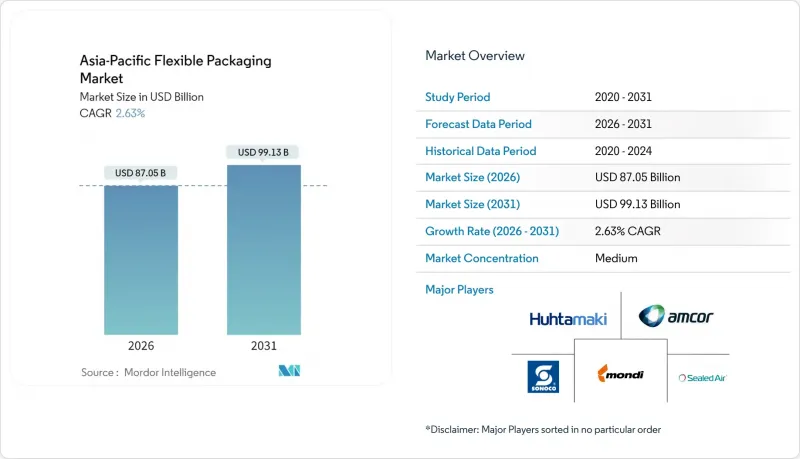

预计到 2026 年,亚太地区的软质包装市场规模将达到 870.5 亿美元。

这意味着从 2025 年的 848.2 亿美元成长到 2031 年的 991.3 亿美元,2026 年至 2031 年的复合年增长率为 2.63%。

随着日本、澳洲以及中国和印度试点城市的监管机构强制推行单一材料包装规格,资金正从原物料吨位转向高阻隔阻隔性和可回收设计。儘管中国仍保持规模优势,但印度4.89%的复合年增长率表明,随着加工商寻求更低的劳动力成本以及对零食和个人保健产品日益增长的需求,市场格局正在发生地域性转移。预计到2024年,塑胶将占据68.12%的市场份额,但生质塑胶和可堆肥材料正以4.33%的复合年增长率快速增长,品牌所有者正积极调整产品系列以适应不断扩大的生产者责任延伸制度(EPR)。包装袋和包装盒仍是成本效益最高的包装形式,占产品类型总收入的47.63%。同时,小袋装和条状包装的成长率为3.67%,反映了单份包装产品在亚洲二、三线城市的成本效益。数位印刷每年增长 4.76%,使得 10,000 公尺以下的短版印刷有利可图,并透过支持日本和韩国的限量版产品发布,重塑了加工商的经济效益。

亚太地区软质包装市场趋势与洞察

对便利包装的需求日益增长

中国超过60%的都市化以及日本单人家庭比例的不断上升,推动了对分量控制、可重复密封包装袋的需求,这种包装袋能够缩短备餐时间并减少食物浪费。东南亚零售商计画在2025年将软质包装产品种类增加22%,证明了加工商投资伺服驱动软包装生产线的合理性。 15分钟内完成产品种类切换的能力提高了产能运转率,并支援快速促销。消费者愿意支付8-12%的便利溢价,进而缓解树脂价格波动带来的利润压力。可支配收入的成长使得软质包装成为新兴大都市地区零食、饮料和蒸馏食品的首选包装。

包装商品电子商务渗透率不断提高

印度线上杂货市场份额预计将从2020年的3.2%增长到2024年的7.8%,越南的电子商务物流网络预计到2024年将覆盖85%的人口。为了应对「最后一公里」配送的挑战,需要使用耐穿刺、雾面饰面且能承受多次搬运并在移动萤幕上清晰可见的薄膜。加工商目前正在设计抗穿刺强度达到4牛顿或更高的多层结构,并愿意为此增加6-8%的材料成本,以避免高成本的退货成本。数位印刷的可变数据码能够提升品牌互动,并将包装与忠诚度计画连接起来。兼具性能和美观的软包装正巩固其作为电商理想包装容器的地位。

人们担忧塑胶包装和回收对环境的影响

在越南、泰国和菲律宾,生产者延伸责任制(EPR)的成本(占厂价的0.8%至2.1%)使加工商的利润率下降了40至60个基点。印度在2026年实现80%回收率的目标在农村地区仍然难以实现,这阻碍了品牌遵守相关规定。调查显示,在日本和韩国,64%的消费者在有可回收替代品的情况下会避免使用多层包装袋,这给传统包装形式带来了压力。可堆肥薄膜的价格仍然高出25%至30%,并且在潮湿环境中也面临挑战。在建立健全的回收系统之前,品牌所有者将面临永续性与成本现实之间的矛盾。

细分市场分析

到2025年,塑胶将以67.35%的市场份额占据主导地位,其中聚乙烯仍将是高速立式填充封口生产线的主要材料。在此基础上,生质塑胶和可堆肥材料将以4.17%的复合年增长率实现最快增长,因为品牌商正在采用PLA和PHA混合物以满足日本和澳洲即将出台的回收标准。随着全球供应链一体化程度的提高,亚太地区生质塑胶软质包装市场规模预计将会扩大,但来自欧洲的运费溢价仍将影响最终到岸成本结构。双向拉伸聚丙烯(BOPP)凭藉其透明度和可印刷性,将继续在零嘴零食领域保持领先地位,而铝箔将在医疗和咖啡应用领域保持其市场地位,因为这些应用氧气透过率低于0.5 cc/m²/天的要求非常严格。

整体包装的普及迫使聚乙烯供应商开发阻隔性配方,以金属化聚乙烯(PE)或高密度聚乙烯(HDPE)涂层取代聚对苯二甲酸乙二醇酯(PET)和尼龙层,以保持其可回收性。 Uflex 的 Flex-PET(预计于 2024 年商业化)的氧气透过率达到 1.2 cc/m²/天,巩固了聚乙烯在零食薄膜领域的领先地位。纸基复合材料在韩国化妆品市场日益受到青睐,儘管其成本溢价高达 18-22%,但其富含纤维,具有可持续性优势。金属的阻隔性在製药领域仍然无可匹敌,但其回收过程中的能源消耗正受到检验。整体而言,亚太地区软质包装市场正在经历树脂混合物的重新平衡,可回收聚烯比复杂的多层结构更受青睐。

预计到2025年,袋装和软包装产品将占据46.95%的市场份额,这主要得益于其在食品、宠物食品和农业领域的广泛应用。然而,小袋装和条状包装预计到2031年将以3.55%的复合年增长率成长。在亚太地区,小袋软质包装的市占率正在成长,因为跨国公司正瞄准价格敏感型消费者,推出洗髮精、护髮素和护肤霜等一次性产品。联合利华和宝洁公司计划在2024年将小袋产品种类增加14%,以覆盖月收入低于300美元的家庭。

薄膜和包装材料的需求与产量密切相关,但由于日本和韩国进行可重复使用商品搭售的试验,拉伸薄膜面临不利影响。在液体清洁剂领域,带有吸嘴的立式袋正在取代硬质瓶,重量减轻了40%,并提高了其对循环经济的贡献。亚太地区的软质包装市场继续青睐适合电商物流的柔性包装形式,因为更轻的重量可以降低最后一公里配送成本。诸如封盖膜之类的细分产品正在寻求高利润的烘焙食品和农产品外包装。产品类型的多元化有助于加工商在树脂价格波动的情况下保持其产品组合的韧性。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对便利包装的需求日益增长

- 长保质期和创新包装的需求

- 包装商品电子商务渗透率不断提高

- 采用单一材料软质包装,以符合回收义务

- 东南亚生鲜食品出口低温运输扩张迅猛

- 品牌所有者转向数位印刷,以实现小批量、个性化生产。

- 市场限制

- 人们担忧塑胶包装和回收对环境的影响

- 石油化学原料价格波动

- 日本和澳洲对多层级结构的监管限制

- 食品级再生材料(用于软质包装)的供应限制

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素如何影响市场

第五章 市场规模与成长预测

- 材料

- 塑胶

- 聚乙烯(PE)

- 双轴延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 其他塑料

- 纸

- 金属箔

- 生质塑胶和可堆肥材料

- 塑胶

- 依产品类型

- 袋子和小袋

- 薄膜和包装

- 小袋装和条状包装

- 其他产品类型

- 按最终用户行业划分

- 食物

- 烘焙产品

- 小吃

- 肉类、家禽和水产品

- 糖果甜点

- 宠物食品

- 其他食品

- 饮料

- 医疗和药品

- 个人护理和化妆品

- 农业和园艺

- 其他终端用户产业

- 食物

- 透过印刷技术

- 柔版印刷

- 凹版印刷

- 数位印刷

- 其他印刷技术

- 按国家/地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor plc

- Mondi plc

- Sonoco Products Company

- Rengo Co., Ltd.

- Sealed Air Corporation

- Formosa Flexible Packaging Corp.

- Wapo Corporation Ltd.

- Chuan Peng Enterprise Co., Ltd.

- TCPL Packaging Ltd.

- Ester Industries Limited

- Huhtamaki Oyj

- Uflex Ltd.

- ProAmpac Holdings Inc.

- Constantia Flexibles Group GmbH

- Winpak Ltd.

- Cosmo Films Ltd.

- Glenroy Inc.

- Toppan Printing Co., Ltd.

- Fujimori Kogyo Co., Ltd.

第七章 市场机会与未来展望

Asia-Pacific flexible packaging market size in 2026 is estimated at USD 87.05 billion, growing from 2025 value of USD 84.82 billion with 2031 projections showing USD 99.13 billion, growing at 2.63% CAGR over 2026-2031.

Capital now flows toward high-barrier, recyclable designs rather than raw tonnage, as regulators tighten mandates on mono-material formats in Japan, Australia, and pilot cities in China and India. China still offers scale advantages, yet India's 4.89% CAGR signals a geographic pivot as converters seek lower labor costs and rising demand for snacks and personal care. Plastics held a 68.12% share in 2024, but bioplastics and compostables are gaining momentum, expanding at a rate of 4.33% annually as brand owners future-proof their portfolios against extended producer responsibility schemes. Bags and pouches remained the cost-efficient workhorse, accounting for 47.63% of product-type revenue. Meanwhile, sachets and stick packs gained ground, with a 3.67% growth curve that speaks to the affordability of single-serve products across tier-2 and tier-3 Asian cities. Digital printing, growing at a rate of 4.76% per year, is reshaping converter economics by enabling profitable runs of less than 10,000 linear meters and supporting limited-edition launches in Japan and South Korea.

Asia-Pacific Flexible Packaging Market Trends and Insights

Increased Demand for Convenient Packaging

Urbanization exceeding 60% in China and a rising share of single-person households in Japan are shrinking meal-prep time, prompting demand for portion-controlled, resealable pouches that minimize food waste. Southeast Asian retailers have raised shelf allocation for flexible SKUs by 22% in 2025, validating converters' investments in servo-driven pouch lines. The ability to switch SKUs within 15 minutes boosts asset utilization and supports rapid promotions. Consumers pay a convenience premium of 8-12%, cushioning margin pressure from resin fluctuations. As disposable incomes increase, flexible packaging becomes the preferred choice for snacks, beverages, and ready-to-eat meals in emerging urban clusters.

Growing E-Commerce Penetration for Packaged Goods

India's online grocery share rose from 3.2% in 2020 to 7.8% in 2024, and Vietnam's e-commerce logistics network reached 85% population coverage in 2024. Last-mile realities demand puncture-resistant, matte-finish films that can withstand multiple handling points and display well on mobile screens. Converters now engineer multi-layer structures with a puncture strength of> 4 newtons, accepting a 6-8% material premium to avoid costly returns. Variable-data codes printed digitally drive brand engagement, tying packaging to loyalty programs. The performance-plus-aesthetics combination cements flexible packs as the logical e-commerce container.

Concerns About Environmental Impact and Recycling of Plastic Packaging

Extended producer responsibility fees of 0.8-2.1% of the ex-factory price in Vietnam, Thailand, and the Philippines shave 40-60 basis points off converter margins. India's 80% collection target by 2026 remains elusive in rural districts, hindering brand-owner compliance. Surveys show 64% of consumers in Japan and South Korea avoid multilayer pouches when recyclable alternatives exist, pressuring legacy formats. Compostable films still command premiums of 25-30% and struggle in humid, high-moisture environments. Until robust recycling streams emerge, brand owners face a tension between their sustainability pledges and the realities of cost.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Mono-Material Flexible Packaging to Meet Recycling Mandates

- Surge in Cold Chain Expansion for Fresh Produce Exports in Southeast Asia

- Volatility in Raw Material Prices for Petrochemical Feedstocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics dominated 2025 with 67.35% share, and polyethylene remained the workhorse for high-speed vertical form-fill-seal lines. Within this base, bioplastics and compostables chart the fastest expansion at a 4.17% CAGR as brand owners adopt PLA and PHA blends to meet Japan and Australia's upcoming recyclability thresholds. The Asia-Pacific flexible packaging market size for bioplastics is on track to expand as global supply chains become more integrated, although freight premiums from Europe continue to impact landed cost structures. BOPP continues to excel in snacks and confectionery due to its clarity and printability, while aluminum foil maintains a niche in medical and coffee applications where sub-0.5 cc/m2/day oxygen levels are non-negotiable.

The drive to mono-material pushes polyethylene suppliers into higher-barrier formulations, replacing PET and nylon layers with metallized PE and HDPE coatings to maintain recyclability. Uflex's Flex-PET, commercialized in 2024, achieves 1.2 cc/m2/day oxygen transmission and reinforces polyethylene's claim on snack films. Paper-based laminates are gaining traction in South Korean cosmetics, trading at 18-22% cost premiums while offering a fiber-rich sustainability story. Metal's high barrier remains unmatched for pharmaceuticals yet faces scrutiny for recycling energy intensity. Net-net, the Asia-Pacific flexible packaging market faces a resin-mix recalibration favoring recyclable polyolefins over complex multilayers.

Bags and pouches held 46.95% share in 2025, powered by versatility across food, pet food, and agriculture. However, sachets and stick packs are projected to grow at a 3.55% CAGR through 2031. The Asia-Pacific flexible packaging market share for sachets is increasing as multinationals target price-sensitive consumers with single-use products such as shampoos, conditioners, and skincare creams. Unilever and Procter & Gamble expanded sachet SKUs by 14% in India in 2024 to reach households with monthly incomes of less than USD 300.

Films and wraps tie demand to manufacturing output, with stretch film facing headwinds from reusable bundling trials in Japan and South Korea. Stand-up pouches with spouts are replacing rigid bottles in liquid detergents, reducing weight by 40% and strengthening circular-economy credentials. The Asia-Pacific flexible packaging market continues to favor flexible formats that align with e-commerce logistics, as lighter parcels lower last-mile delivery costs. Niche types such as lidding films chase higher-margin bakery and produce overwraps. Collectively, product-type diversification supports converters' portfolio resilience amid fluctuating resin prices.

The Asia-Pacific Flexible Packaging Market Report is Segmented by Material (Plastics, Paper, Metal Foil, Bioplastics and Compostable Materials), Product Type (Bags and Pouches, Films and Wraps, and More), End-User Industry (Beverage, Healthcare and Pharmaceutical, Personal Care and Cosmetics, and More), Printing Technology (Flexography, Rotogravure, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor plc

- Mondi plc

- Sonoco Products Company

- Rengo Co., Ltd.

- Sealed Air Corporation

- Formosa Flexible Packaging Corp.

- Wapo Corporation Ltd.

- Chuan Peng Enterprise Co., Ltd.

- TCPL Packaging Ltd.

- Ester Industries Limited

- Huhtamaki Oyj

- Uflex Ltd.

- ProAmpac Holdings Inc.

- Constantia Flexibles Group GmbH

- Winpak Ltd.

- Cosmo Films Ltd.

- Glenroy Inc.

- Toppan Printing Co., Ltd.

- Fujimori Kogyo Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Demand for Convenient Packaging

- 4.2.2 Demand for Longer Shelf Life and Innovative Packaging

- 4.2.3 Growing E-Commerce Penetration for Packaged Goods

- 4.2.4 Adoption of Mono-Material Flexible Packaging to Meet Recycling Mandates

- 4.2.5 Surge in Cold Chain Expansion for Fresh Produce Exports in Southeast Asia

- 4.2.6 Brand Owner Shift Toward Digital Printing for Short-Run Personalization

- 4.3 Market Restraints

- 4.3.1 Concerns About Environmental Impact and Recycling of Plastic Packaging

- 4.3.2 Volatility in Raw Material Prices for Petrochemical Feedstocks

- 4.3.3 Regulatory Restrictions on Multilayer Structures in Japan and Australia

- 4.3.4 Limited Food-Grade Recyclate Availability for Flexible Formats

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.1.3 Cast Polypropylene (CPP)

- 5.1.1.4 Other Plastics

- 5.1.2 Paper

- 5.1.3 Metal Foil

- 5.1.4 Bioplastics and Compostable Materials

- 5.1.1 Plastics

- 5.2 By Product Type

- 5.2.1 Bags and Pouches

- 5.2.2 Films and Wraps

- 5.2.3 Sachets and Stick Packs

- 5.2.4 Other Product Types

- 5.3 BY End-user Industry

- 5.3.1 Food

- 5.3.1.1 Baked Goods

- 5.3.1.2 Snacks

- 5.3.1.3 Meat, Poultry and Seafood

- 5.3.1.4 Confectionery

- 5.3.1.5 Pet Food

- 5.3.1.6 Other Food Products

- 5.3.2 Beverage

- 5.3.3 Healthcare and Pharmaceutical

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Agriculture and Horticulture

- 5.3.6 Other End-User Industries

- 5.3.1 Food

- 5.4 By Printing Technology

- 5.4.1 Flexography

- 5.4.2 Rotogravure

- 5.4.3 Digital Printing

- 5.4.4 Other Printing Technologies

- 5.5 By Country

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 Australia

- 5.5.5 South Korea

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Mondi plc

- 6.4.3 Sonoco Products Company

- 6.4.4 Rengo Co., Ltd.

- 6.4.5 Sealed Air Corporation

- 6.4.6 Formosa Flexible Packaging Corp.

- 6.4.7 Wapo Corporation Ltd.

- 6.4.8 Chuan Peng Enterprise Co., Ltd.

- 6.4.9 TCPL Packaging Ltd.

- 6.4.10 Ester Industries Limited

- 6.4.11 Huhtamaki Oyj

- 6.4.12 Uflex Ltd.

- 6.4.13 ProAmpac Holdings Inc.

- 6.4.14 Constantia Flexibles Group GmbH

- 6.4.15 Winpak Ltd.

- 6.4.16 Cosmo Films Ltd.

- 6.4.17 Glenroy Inc.

- 6.4.18 Toppan Printing Co., Ltd.

- 6.4.19 Fujimori Kogyo Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

柔性工业包装市场:按材料、产品类型、包装形式、最终用途和分销管道划分-2026-2032年全球市场预测

柔性工业包装市场:按材料、产品类型、包装形式、最终用途和分销管道划分-2026-2032年全球市场预测 软包装市场规模、份额、趋势和预测:按产品类型、原材料、印刷技术、应用和地区划分,2026-2034年非食品麦芽酚市场依用途、等级和形态划分,全球预测(2026-2032年)

软包装市场规模、份额、趋势和预测:按产品类型、原材料、印刷技术、应用和地区划分,2026-2034年非食品麦芽酚市场依用途、等级和形态划分,全球预测(2026-2032年) 柔性胶合板市场规模、份额和成长分析:按胶合板类型、产品厚度、等级、最终用户产业和地区划分-2026-2033年产业预测

柔性胶合板市场规模、份额和成长分析:按胶合板类型、产品厚度、等级、最终用户产业和地区划分-2026-2033年产业预测 柔性包装市场分析及预测(至2035年):依类型、产品类型、材料类型、应用、技术、组件、最终用户、功能及製程划分

柔性包装市场分析及预测(至2035年):依类型、产品类型、材料类型、应用、技术、组件、最终用户、功能及製程划分 全球软包装市场规模、份额、趋势和成长分析报告(2026-2034年)软包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

全球软包装市场规模、份额、趋势和成长分析报告(2026-2034年)软包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 2026年全球真空袋市场报告2026年全球软包装市场报告

2026年全球真空袋市场报告2026年全球软包装市场报告 金属化软质包装市场规模、份额和趋势分析报告:按产品、包装类型、最终用途、地区和细分市场预测(2026-2033 年)

金属化软质包装市场规模、份额和趋势分析报告:按产品、包装类型、最终用途、地区和细分市场预测(2026-2033 年)