|

市场调查报告书

商品编码

1939618

无机聚合物:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Geopolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

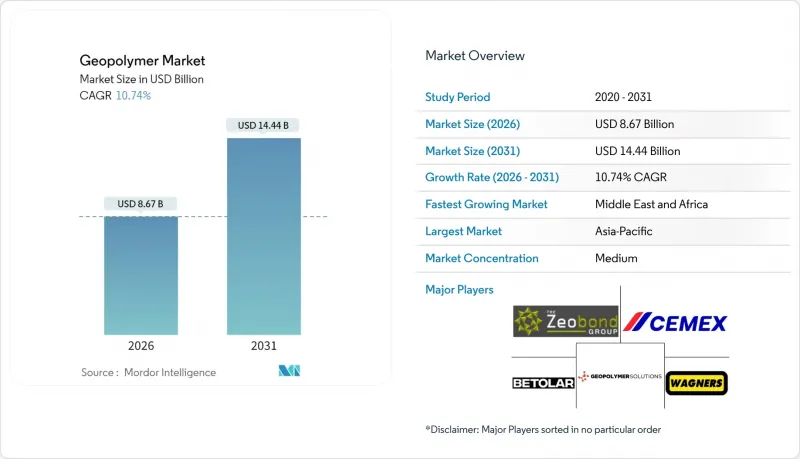

预计到 2026 年,无机聚合物市场价值将达到 86.7 亿美元,高于 2025 年的 78.3 亿美元。

预计到 2031 年将达到 144.4 亿美元,2026 年至 2031 年的复合年增长率为 10.74%。

建筑规范中日益严格的碳含量规定、稳定工业废弃物原料供应的不断增长以及单组分配方性能的持续提升,正在推动关键建筑应用领域无机聚合物的需求。亚太地区大量的基础建设项目、欧洲的碳定价机制以及北美的绿色建筑认证积分,都为市场销量的持续增长提供了支撑;而中东的大型企划则透过首次应用,为市场带来了新的成长机会。在老牌水泥企业扩大商业工厂规模以巩固现有市场份额的同时,一些专注于地聚合物领域的Start-Ups正利用其敏捷的研发能力,推出利润丰厚的利基产品。儘管短期收入会受到碱性活化剂价格波动和监管核准时间的影响,但随着技术成熟度与政策压力相契合,整体市场成长动能仍保持强劲。

全球无机聚合物市场趋势与洞察

水泥业严格的二氧化碳排放法规

强制性碳减排政策正在重塑公共和私人建设计划的材料规格标准。加州的「先进清洁汽车II」计画将采购奖励与低碳建筑材料挂钩,鼓励建筑商在面向未来的计划竞标中优先考虑无机聚合物混凝土。在欧洲,计划于2026年实施的碳边境调节机制将征收嵌入式碳关税,从而削弱进口波特兰水泥含量高的产品的成本优势。由于开发商寻求应对不断上涨的合规成本的确定性,这些措施的影响波及整个供应链。因此,市政基础设施、商业房地产和大型工业仓库对无机聚合物预铸面板和现场浇筑混凝土的订单正在成长。为此,跨国水泥製造商正在加快碱激活黏合剂专用试验生产线的早期运作,以确保其产品能够儘早列入规格清单。监管的推动作用既刺激了需求,也促使企业进行现有产品组合的多元化策略布局。

飞灰及矿渣原料供应增加

燃煤发电厂的退役释放了储存数十年的飞灰。同时,全球钢铁产能的整合正在规范炉渣品质。亚洲电力公司目前正根据循环经济准则拍卖经认证的飞灰,而中国则强制要求到2025年实现90%的粉煤灰利用率。印度和韩国也实施了类似的政策,扩大了无机聚合物配方生产商的供应来源并稳定了价格。以往受物流限制的北美F级飞灰进口,正透过服务美国西岸混凝土生产商的港口转运枢纽得到缓解。这降低了原料成本的波动性,提高了化学成分的稳定性,从而可以进行更严格的品管,并扩大结构级粉煤灰的应用。稳定的原料供应有助于公共产业和无机聚合物新兴企业之间达成长期供应协议,从而降低环境责任并创造新的收入来源。

缺乏统一的设计标准与规范

工程师在指定未完全纳入国家设计标准范围的材料时仍保持谨慎。儘管ASTM正在修订C595/C595M-24标准以引入更广泛的混合水泥类别,但专门针对无机聚合物的章节仍处于草案阶段。由于缺乏明确的长期耐久性标准,关键基础设施业主通常会采用保守的安全係数或要求设置冗余的保护层,导致成本竞争力问题。保险公司和担保公司通常会对使用非标准接合材料的计划收取额外保费,增加总安装成本。发展中国家面临额外的障碍,因为其许可机构依赖从国外引进的传统标准,即使气候政策倾向于低碳材料,也阻碍了当地标准的采用。

细分市场分析

预计到2025年,以混凝土为主的产品将占据无机聚合物市场52.20%的份额,这反映出市场对现有产品的依赖,这些产品无需对工人进行再培训即可直接应用于现有设备。这项优势提供了稳定的收入基础,并为拓展相关产品(例如预力桥樑梁体、建筑幕墙覆层和模组化墙体单元)铺平了道路。承包商正在采用地聚合物混凝土进行平板施工、大体积浇筑和预製构件,因为其抗压强度发展、养护时间和可加工性与普通无机聚合物水泥混合料相当,从而最大限度地降低了施工风险。市场领导正在为其解决方案提供技术支援、混合料设计咨询和现场品质保证服务,以增强客户对转换的信心,并确保基础设施机构在满足碳预算要求方面获得持续的订单支援。

随着资产密集型产业优先考虑快速修復解决方案,预计到2031年,水泥浆和黏合剂细分市场将以11.03%的复合年增长率成长。无机聚合物水泥浆可与输液设备无缝集成,并具有高早期强度、低收缩率和耐化学腐蚀性,这对于污水管管修復、炼油厂围护和海洋桩基覆盖至关重要。产品差异化依赖于客製化的活化剂配方、纤维增强材料和触变性添加剂,从而实现高空和垂直安装。新兴产品系列,例如抗压强度超过126 MPa的无机聚合物砂浆,拓展了可应用于高应力环境的范围,并为供应商创造了获得更高附加价值利润的机会。

无机聚合物市场报告按产品类型(水泥、混凝土和预铸面板、水泥浆和黏合剂、其他产品类型)、应用(建筑、道路和路面、跑道、管道和混凝土修復等)、前体/原料(飞灰基、矿渣基、偏高岭土基、稻壳灰和农业废弃物、其他)以及地区(亚太地区、北美地区、欧洲、中东和中东地区)。

区域分析

到2025年,亚太地区将占据全球44.20%的市场份额,这主要得益于统一的政策倡议、丰富的原材料供应以及全球规模最大的基础设施建设预算。中国的「工业固态废弃物利用」政策要求製造商在2025年实现90%的飞灰和矿渣利用率,从而为无机聚合物生产商创造了稳定的原料基础。印度的智慧城市计画和城市轨道交通的扩建确保了稳定的竞标量,而日本的一个研究联盟正在改进一种用于抗震应用的高耐久性配方。规模、监管和技术能力的综合优势将使该地区在未来十年保持主导地位。

预计中东和非洲地区将以10.87%的复合年增长率成长,这反映出无机聚合物解决方案已在沙乌地阿拉伯的NEOM新城和阿联酋的Masdar扩建等大型企划中得到基础性应用。干旱气候下的耐久性要求凸显了无机聚合物的抗硫酸盐侵蚀和耐热循环性能,从而延长了资产寿命并减少了养护过程中的用水量。各国政府正在将碳减排条款纳入建筑规范,增强了市场需求的韧性。供应商正与当地水泥公司成立合资企业,以加快监管认证并利用现有的分销网络。

随着现有基础设施碳改造计画的推进,北美和欧洲在政策主导正经历稳定成长。美国联邦税额扣抵和欧洲绿色交易正在津贴低碳材料的研究,并支持桥面、高速公路匝道和机场停机坪等试点计画。大型建筑公司正在将无机聚合物方案纳入设计建造提案,并在公共竞标中凭藉永续性指标获得高分。南美洲目前仍是小众市场,但随着稻壳灰的供应和环境政策的趋同,在符合当地标准和供应链发展的前提下,南美洲可望从中受益。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 水泥业严格的二氧化碳排放法规

- 飞灰及矿渣原料供应增加

- 绿建筑认证材料的需求

- 单组分无机聚合物技术的推广

- 新兴的深水能源和采矿基础设施应用

- 市场限制

- 缺乏统一的设计标准和准则

- 碱性活化剂(NaOH/Na2SiO3)价格波动

- 原料化学成分的差异会影响品管

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 水泥、混凝土和预铸面板

- 水泥浆和黏合剂

- 其他产品类型

- 透过使用

- 建筑学

- 道路和人行道

- 跑道

- 管道和混凝土维修

- 桥

- 隧道衬砌

- 铁路枕木

- 涂层应用

- 防火

- 核废料和其他危险废弃物的固化

- 专用模具产品

- 按原料/依原料

- 飞灰基

- 矿渣基

- 偏高岭土基

- 稻壳灰和农业废弃物

- 其他(赤泥、矾土残渣、废玻璃、玄武岩粉)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率/排名分析

- 公司简介

- Banah UK Ltd

- Betolar PLC

- CEMEX SAB de CV

- Ceskych Lupkovych Zavodech AS

- ClockSpring|NRI

- GCP Saint Gobain

- Geopolymer Solutions LLC

- Green 360 Technologies

- Heidelberg Materials

- IPR

- Murray & Roberts

- PCI Augsburg GmbH

- RENCA Inc

- Rocla Pty Limited

- Schlumberger Limited

- Wagners

- Zeobond Pty Ltd

第七章 市场机会与未来展望

Geopolymer market size in 2026 is estimated at USD 8.67 billion, growing from 2025 value of USD 7.83 billion with 2031 projections showing USD 14.44 billion, growing at 10.74% CAGR over 2026-2031.

Accelerating regulation of embodied-carbon across building codes, a widening supply of consistent industrial waste feedstocks, and continual performance gains in one-part formulations combine to lift demand for geopolymers across core construction segments. Asia-Pacific's vast infrastructure pipeline, Europe's carbon-pricing mechanisms, and North America's green-building certification credits together underpin sustained volume growth, while Middle East megaprojects provide incremental upside through first-build adoption. Established cement majors are scaling commercial plants to protect legacy share, even as specialized start-ups leverage agile R&D to launch niche high-margin products. Near-term earnings remain sensitive to alkali-activator price swings and code-approval timelines, yet the overall market's trajectory remains firmly positive as technical maturity aligns with policy pressure.

Global Geopolymer Market Trends and Insights

Stringent CO2-Emissions Regulations on Cement Industry

Mandatory carbon-reduction policies are reshaping material-specification protocols in public and private construction projects. California's Advanced Clean Cars II program ties procurement incentives to low-carbon building materials, prompting contractors to favor geopolymer concrete in their bids to future-proof their projects. In Europe, the Carbon Border Adjustment Mechanism scheduled for 2026 imposes embedded-carbon tariffs that erode the cost advantages of imported Portland-cement-intensive products. These measures cascade through supply chains as developers pursue certainty against rising compliance costs. Consequently, order books for geopolymer pre-cast panels and cast-in-place mixes are expanding in municipal infrastructure, commercial real estate, and large-format industrial warehousing. Multinational cement producers are responding by fast-tracking pilot lines dedicated to alkali-activated binders to secure early specification listings. Regulatory momentum therefore functions both as demand stimulus and as a strategic trigger for incumbent portfolio diversification.

Growing Availability of Fly-Ash and Slag Feedstocks

De-commissioning of coal-fired power plants is releasing decades of stockpiled fly ash, while global steel-capacity consolidation is standardizing slag quality. Asian utilities now auction certified fly-ash lots under circular-economy guidelines that mandate 90% utilization by 2025 in China. Comparable policies in India and South Korea widen supply pools and stabilize pricing for geopolymer formulators. North American Class-F fly ash imports, historically constrained by logistics, are easing through port-based trans-shipment hubs that service concrete producers on the U.S. West Coast. The net effect is a decrease in raw-material cost volatility and greater consistency in chemical composition, enabling tighter quality control and broader structural-grade adoption. Feedstock visibility also encourages long-term offtake contracts between utilities and geopolymer start-ups, aligning environmental-liability reduction with new revenue streams.

Lack of Uniform Design Codes and Standards

Engineers remain cautious when specifying materials not fully covered by national design codes. Although ASTM is revising C595/C595M-24 to introduce broader blended-cement categories, a geopolymer-specific chapter is still in the drafting stage. In the absence of definitive long-term durability benchmarks, critical infrastructure owners often impose conservative safety factors or require redundant protective layers, thereby eroding cost competitiveness. Insurers and bonding agencies frequently attach surcharge premiums to projects that incorporate non-codified binders, thereby raising the total installed costs. Developing nations face additional hurdles as professional-licensing bodies defer to legacy standards imported from foreign jurisdictions, delaying local adoption even when climate policies favor low-carbon materials.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Green-Building Certification Materials

- One-Part Geopolymer Technology Uptake

- Price Volatility of Alkali Activators (NaOH/Na2SiO3)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Concrete-centric offerings accounted for 52.20% of geopolymer market share in 2025, underscoring the sector's reliance on familiar form factors that slide into existing equipment fleets without retraining crews. This dominance provides a stable revenue floor and paves a gateway for adjacent products such as pre-stressed bridge beams, facade cladding, and modular wall units. Contractors embrace geopolymer concrete for flatwork, mass pours, and pre-cast elements because compressive-strength development, setting time, and workability now parallel ordinary Portland-cement mixes, minimizing scheduling risk. Market leaders bundle technical support, mix-design consultation, and on-site quality-assurance services to reinforce switching confidence, locking in repeat orders from infrastructure agencies seeking carbon-budget compliance.

The niche grout-and-binder segment is projected to deliver an 11.03% CAGR to 2031 as asset-intensive industries prioritize rapid-return repair solutions. Geopolymer grouts integrate seamlessly with pressure-injection equipment, offering high early strength, low shrinkage, and chemical resistance vital for sewer-line rehabilitation, refinery containment, and marine-pile encasements. Product differentiation hinges on tailored activator packages, fiber reinforcement, and thixotropic additives that enable overhead or vertical installation. Emerging product lines - such as geopolymer mortars exceeding 126 MPa compressive strength - broaden addressable high-stress applications and position suppliers to capture premium margins.

The Geopolymer Market Report is Segmented by Product Type (Cement, Concrete and Pre-Cast Panels, Grout and Binder, Other Product Types), Application (Building, Road and Pavement, Runway, Pipe and Concrete Repair, and More), Precursor/Raw-Material (Fly Ash Based, Slage Based, Metakaolin Based, Rice-Husk Ash and Agricultural Wastes, Others), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific posted a dominant 44.20% share in 2025, driven by synchronized policy mandates, abundant feedstock, and the world's largest infrastructure budgets. China's "Industrial Solid-Waste Utilization" policy obliges manufacturers to valorize 90% of fly ash and slag by 2025, creating a captive raw-material base for geopolymer producers. India's smart-city initiatives and urban-rail expansion add steady bid volumes, while Japanese research consortia refine high-durability formulations for seismic applications. The convergence of scale, regulation, and technological capability secures the region's leadership through the decade.

The Middle East and Africa region is forecast to grow at an 10.87% CAGR, reflecting ground-up integration of geopolymer solutions in megaprojects such as Saudi Arabia's NEOM and the UAE's Masdar expansion. Arid-climate durability requirements favor geopolymer's resistance to sulfates and thermal cycling, extending asset lifespans and reducing water demand for curing. Governments embed carbon-reduction clauses into construction codes, augmenting demand elasticity. Suppliers form joint ventures with local cement firms to fast-track regulatory certifications and leverage existing distribution networks.

North America and Europe exhibit stable, policy-driven growth as legacy infrastructure undergoes carbon-retrofit programs. Federal-level tax credits in the United States and the European Green Deal funnel grant funding toward low-carbon materials research, underwriting pilot bridge decks, highway ramps, and airport aprons. Construction majors integrate geopolymer options into design-build proposals to score higher on public-tender sustainability criteria. South America, although presently niche, stands to benefit from rice-husk-ash availability and environmental policy convergence, contingent on the development of regional standards and supply chains.

- Banah UK Ltd

- Betolar PLC

- CEMEX SAB de CV

- Ceskych Lupkovych Zavodech AS

- ClockSpring|NRI

- GCP Saint Gobain

- Geopolymer Solutions LLC

- Green 360 Technologies

- Heidelberg Materials

- IPR

- Murray & Roberts

- PCI Augsburg GmbH

- RENCA Inc

- Rocla Pty Limited

- Schlumberger Limited

- Wagners

- Zeobond Pty Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent CO2-emissions regulations on cement industry

- 4.2.2 Growing availability of fly-ash and slag feedstocks

- 4.2.3 Demand for green-building certification materials

- 4.2.4 One-part geopolymer technology uptake

- 4.2.5 Emerging deep-sea energy and mining infrastructure uses

- 4.3 Market Restraints

- 4.3.1 Lack of uniform design codes and standards

- 4.3.2 Price volatility of alkali activators (NaOH/Na2SiO3)

- 4.3.3 Feedstock chem-variability impacting quality control

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Cement, Concrete and Pre-cast Panels

- 5.1.2 Grout and Binder

- 5.1.3 Other Product Types

- 5.2 By Application

- 5.2.1 Building

- 5.2.2 Road and Pavement

- 5.2.3 Runway

- 5.2.4 Pipe and Concrete Repair

- 5.2.5 Bridge

- 5.2.6 Tunnel Lining

- 5.2.7 Railroad Sleeper

- 5.2.8 Coating Application

- 5.2.9 Fireproofing

- 5.2.10 Nuclear Other Toxic Waste Immobilization

- 5.2.11 Specific Mold Products

- 5.3 By Precursor/Raw-Material

- 5.3.1 Fly Ash Based

- 5.3.2 Slage Based

- 5.3.3 Metakaolin Based

- 5.3.4 Rice-Husk Ash and Agricultural Wastes

- 5.3.5 Others (Red-Mud and Bauxite Residue and Waste Glass and Basalt Powders)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Banah UK Ltd

- 6.4.2 Betolar PLC

- 6.4.3 CEMEX SAB de CV

- 6.4.4 Ceskych Lupkovych Zavodech AS

- 6.4.5 ClockSpring|NRI

- 6.4.6 GCP Saint Gobain

- 6.4.7 Geopolymer Solutions LLC

- 6.4.8 Green 360 Technologies

- 6.4.9 Heidelberg Materials

- 6.4.10 IPR

- 6.4.11 Murray & Roberts

- 6.4.12 PCI Augsburg GmbH

- 6.4.13 RENCA Inc

- 6.4.14 Rocla Pty Limited

- 6.4.15 Schlumberger Limited

- 6.4.16 Wagners

- 6.4.17 Zeobond Pty Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

2026年高容量飞灰混凝土全球市场报告

2026年高容量飞灰混凝土全球市场报告 无机聚合物材料市场:依原料、产品类型、製造流程和应用划分-2026年至2032年全球市场预测2026年全球无机聚合物混凝土市场报告2026年全球无机聚合物水泥市场报告

无机聚合物材料市场:依原料、产品类型、製造流程和应用划分-2026年至2032年全球市场预测2026年全球无机聚合物混凝土市场报告2026年全球无机聚合物水泥市场报告 全球无机聚合物市场规模、份额、趋势和成长分析报告(2026-2034)

全球无机聚合物市场规模、份额、趋势和成长分析报告(2026-2034) 无机聚合物市场报告:按应用、最终用途产业和地区划分(2026-2034 年)2026年全球无机聚合物市场报告日本无机聚合物市场规模、份额、趋势及预测(按应用、终端用户产业及地区划分),2026-2034年

无机聚合物市场报告:按应用、最终用途产业和地区划分(2026-2034 年)2026年全球无机聚合物市场报告日本无机聚合物市场规模、份额、趋势及预测(按应用、终端用户产业及地区划分),2026-2034年 无机聚合物市场规模、份额和成长分析(按产品类型、应用、物理形态、最终用途和地区划分)-2026-2033年产业预测

无机聚合物市场规模、份额和成长分析(按产品类型、应用、物理形态、最终用途和地区划分)-2026-2033年产业预测 全球地无机聚合物水泥替代品市场:预测至2032年-按产品类型、粘合剂类型、养护方法、原料来源、应用和地区进行分析

全球地无机聚合物水泥替代品市场:预测至2032年-按产品类型、粘合剂类型、养护方法、原料来源、应用和地区进行分析