|

市场调查报告书

商品编码

1939624

亚太地区油漆涂料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Asia-Pacific Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

亚太地区油漆和涂料市场预计将从 2025 年的 812.2 亿美元增长到 2026 年的 850.7 亿美元,并预计在 2031 年达到 1072.2 亿美元,2026 年至 2031 年的复合年增长率为 4.74%。

日益严格的环境法规、加速的都市化以及汽车和工业生产的快速扩张将支撑持续的需求,而向水性平台的转型则使技术领导企业能够确保稳定的利润率。中国以56.42%的主导份额在2024年占据市场领先地位,但随着基础设施投资和住宅维修的不断增长,预计到2030年,印度将引领市场成长。原物料价格的波动,尤其是二氧化钛的价格波动,使得利润管理面临更大的压力。BASF和阿克苏诺贝尔等公司的策略重组表明,规模、产品组合平衡和地理覆盖深度将决定竞争优势。数位化色彩工具、高端城市住宅更短的重新粉刷週期以及政策支持的「绿色船舶」维修正在推动需求成长,并使亚太地区的涂料市场与更成熟的化学价值链区分开来。

亚太地区涂料市场趋势及洞察

新兴东协城市的建设热潮

印尼、泰国、越南、马来西亚和菲律宾的建设活动持续成长,推动了对建筑和防护涂料的需求。预计到2025年,印尼将成为世界第三大建筑市场,占国内生产总值)的9%,并维持13%的年增长率。大规模交通走廊、工业园区和经济适用住宅专案增加了涂料在混凝土、钢材和木材基材上的接触点。国际建设公司越来越多地指定使用符合绿色建筑认证的低VOC涂料,进一步推动了对水性涂料的需求。外国直接投资在汽车和电子产业丛集中的成长也带动了高性能OEM涂料、地板涂料和机械涂料的订单。虽然持续的投资流入取决于宏观经济稳定和地缘政治平静,但短期订单确保了亚太地区涂料市场在建筑相关需求成长的情况下仍能保持充足的供应。

缩短中国主要城市住宅的重新粉刷週期

在中国成熟的房地产市场,随着业主优先考虑美观提升和资产保值,房屋翻新週期正在缩短。立邦涂料报告称,一、二线城市的翻新週期已从五至七年缩短至三至五年,市场呈现成长态势。能够确保长期色彩维持的高端品牌正抓住这一趋势,引导消费者选择利润更高的产品。住宅量的结构性放缓导致可支配收入转向维修装修,使得竣工房屋数量减少,但单价上涨。市场需求集中在符合GB/T 33372-2020排放标准的内墙涂料、水性底漆和无味面漆上。虽然持续成长将取决于家庭收入的成长和整体房地产市场的发展趋势,但短期前景已显着提振了亚太地区的涂料市场。

加强对挥发性有机化合物和甲醛的监管

中国GB/T 33372-2020标准将建筑涂料中VOC(挥发性有机化合物)的允许基准值降低至120克/公升,各省的执法宣传活动也导致审核频率增加。缺乏研发能力或水性分散技术基础设施的中小型製造商,如果错过合规期限,将面临配方调整成本和供应链中断的风险。越南和马来西亚也在製定类似的法规,迫使跨境供应商实现产品线标准化、储备不同的SKU,或退出低利润的溶剂型涂料领域。虽然从长远来看,这将推动对高附加价值水性产品的需求,但短期内,产能合理化和转型成本将抑制整体产量,从而减缓亚太地区涂料市场的发展势头。

细分市场分析

预计到2025年,水性涂料将占亚太地区涂料市场份额的56.43%,并在2031年之前以5.52%的复合年增长率成长。 2018年在上海实施的外墙溶剂禁令在广东省、北京市以及沿海工业园区引发了政策连锁反应,引导建筑商转向低VOC、低气味的替代品。在此背景下,亚太地区涂料市场正从逐步采用转向系统性替代。这主要得益于新开发的丙烯酸乳液,其抗黏连性、早期耐水性和快速重涂时间与溶剂型醇酸树脂相当。汽车製造商已展示了水性底涂层和透明涂层层压技术,该技术能够承受东南亚地区频繁的湿度波动,从而消除了传统的品质问题。

粉末涂料、UV固化涂料和高固态涂料是亚太地区涂料产业中规模虽小但成长迅速的细分市场,在金属家具、家用电器和3C电子产品领域的应用日益广泛。粉末涂料零VOC的特性以及超过95%的回收率使其符合新加坡和澳洲注重ESG(环境、社会和治理)的采购政策。然而,烘箱和预处理生产线的资本投资成本阻碍了融资紧张的中小企业丛集广泛采用这些产品。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第3章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴东协城市的建设热潮

- 缩短中国主要住宅的重新粉刷週期

- 汽车製造商转向水性汽车面漆

- 政府「绿色船舶」维修补贴(韩国、日本)

- 印度智慧城市计画强制要求使用冷屋顶涂料

- 市场限制

- 加强挥发性有机化合物及甲醛排放法规(中国GB/T 33372-2020等)

- 二酸化チタンの価格変动性

- 印尼和越南缺乏合格的工业涂装技术人员

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过技术

- 水溶液

- 溶剂型

- 粉末涂装

- 其他技术(紫外线/电子束、高固态等)

- 依树脂类型

- 丙烯酸纤维

- アルキド树脂

- 聚氨酯

- 环氧树脂

- 聚酯纤维

- 其他(酚醛树脂、酮树脂等)

- 按最终用户行业划分

- 建筑与装饰

- 车

- 木头

- 保护涂料

- 一般工业

- 运输

- 包装

- 按地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 印尼

- 泰国

- 马来西亚

- 越南

- 菲律宾

- 新加坡

- 亚太其他地区

第6章 竞合情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3TREESGROUP

- Akzo Nobel NV

- Asian Paints

- Avian Brands

- Axalta Coating Systems, LLC

- BASF

- Berger Paints India

- Boysen Paints

- Chokwang Paint

- Davies Paints Philippines Inc.

- DuluxGroup Ltd

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd

- Nippon Paint Holdings Co., Ltd

- PPG Industries Inc.

- Propanraya

- The Sherwin-Williams Company

第七章 市场机会与未来展望

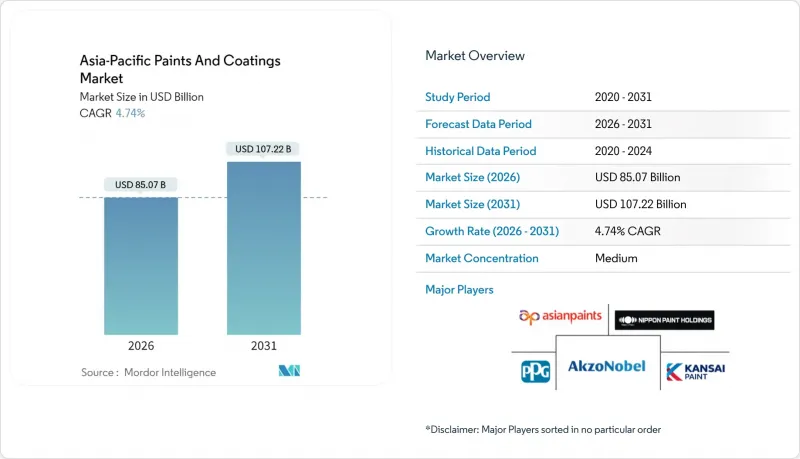

The Asia-Pacific Paints and Coatings Market is expected to grow from USD 81.22 billion in 2025 to USD 85.07 billion in 2026 and is forecast to reach USD 107.22 billion by 2031 at 4.74% CAGR over 2026-2031.

Tightening environmental regulations, accelerating urbanization, and the rapid scale-up of automotive and industrial production underpin sustained demand, while the shift to water-borne platforms positions technology leaders for margin resilience. China retained dominance with a 56.42% share in 2024, yet India is setting the growth pace through 2030 as infrastructure outlays and housing upgrades gain momentum. Raw-material volatility, especially in titanium-dioxide pricing, keeps margin management in sharp focus, and strategy realignments, such as divestitures by BASF and AkzoNobel, signal that scale, portfolio balance, and regional depth will define competitive advantage. Digitalized color tools, faster repaint cycles in premium urban housing, and policy-backed "green ship" retrofits add incremental layers of demand that distinguish the Asia-Pacific paints and coatings market from more mature chemical value chains.

Asia-Pacific Paints And Coatings Market Trends and Insights

Construction Boom in Emerging ASEAN Cities

Surging construction activity in Indonesia, Thailand, Vietnam, Malaysia, and the Philippines continues to lift architectural and protective coating volumes. Indonesia is on track to become the world's third-largest construction market by 2025, contributing 9% to national GDP while growing 13% year-on-year. Large transport corridors, industrial estates, and affordable-housing programs multiply coating touchpoints across concrete, steel, and wood substrates. International contractors typically specify low-VOC paints that align with green-building certifications, further tilting demand toward water-borne chemistry. Foreign direct investment in automotive and electronics clusters is also pushing orders for high-performance OEM, floor, and machinery coatings. Continued inflows hinge on macroeconomic stability and geopolitical calm, but near-term backlogs keep the Asia-Pacific paints and coatings market well supplied with construction-linked volume upside.

Re-painting Cycle Compression in Tier-1 Chinese Housing

China's mature property markets are experiencing shorter repaint intervals as owners prioritize aesthetic upgrades and asset preservation. Nippon Paint reported growth in Tier-1 and Tier-2 cities where repaint cycles have narrowed from 5-7 years to 3-5 years. Premium brands able to guarantee color retention for extended periods are exploiting the trend to trade customers up to higher-margin SKUs. Structural deceleration in new housing starts has redirected disposable incomes toward renovation outlays, raising value per dwelling even as unit completions soften. Demand is concentrated in interior finishes, water-borne primers and odor-free top-coats that meet GB/T 33372-2020 emission limits. Sustained momentum will depend on household income growth and sentiment in the broader real-estate market, yet the near-term uplift is already material for the Asia-Pacific paints and coatings market.

Tightening VOC and Formaldehyde Caps

China's GB/T 33372-2020 standard lowered permissible VOC thresholds for architectural coatings to 120 g/L, and provincial enforcement campaigns have intensified audit frequency. Smaller manufacturers lacking research and development and water-borne dispersion infrastructure face reformulation expenses and risk supply-chain disruptions if compliance deadlines lapse. Similar directives are taking shape in Vietnam and Malaysia, pushing cross-border suppliers to harmonize product lines, stock separate SKUs or exit low-margin solvent categories. While the long-term net effect channels demand into higher-value water-borne offerings, near-term capacity rationalization and transition costs suppress overall output, trimming Asia-Pacific paints and coatings market momentum.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift to Water-borne Auto Topcoats

- Mandated Cool-Roof Coatings in India's Smart-City Program

- Skills Deficit of Certified Industrial Coaters in Indonesia and Vietnam

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne formulations captured 56.43% of the Asia-Pacific paints and coatings market share in 2025 and are projected to record a 5.52% CAGR through 2031. Shanghai's 2018 exterior-wall solvent ban crystallized a wider policy wave across Guangdong, Beijing, and coastal industrial parks, steering builders toward low-VOC and low-odor alternatives. The Asia-Pacific paints and coatings market has therefore shifted from incremental adoption to systemic replacement, helped by new acrylic emulsions that deliver block resistance, early-water resistance, and rapid re-coat times comparable with solvent-borne alkyds. Automotive OEMs have validated water-borne base-coat clear-coat stacks that withstand humidity swings common to Southeast Asia, erasing previous quality concerns.

Powder, UV-curable, and high-solids systems together account for a smaller but fast-growing slice of the Asia-Pacific paints and coatings industry, particularly in metal furniture, appliances, and 3C electronics. Powder's zero-VOC credentials, plus reclamation efficiencies above 95%, appeal to ESG-driven procurement policies in Singapore and Australia. However, capital costs for ovens and pre-treatment lines limit penetration in cash-constrained SME clusters.

The Asia-Pacific Paints and Coatings Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Powder Coating, and Other Technologies), Resin Type (Acrylic, Alkyd, Polyurethane, and More), End-User Industry (Architectural/Decorative, Automotive, Wood, and More), and Geography (China, India, Japan, South Korea, Australia and New Zealand, Indonesia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3TREESGROUP

- Akzo Nobel N.V.

- Asian Paints

- Avian Brands

- Axalta Coating Systems, LLC

- BASF

- Berger Paints India

- Boysen Paints

- Chokwang Paint

- Davies Paints Philippines Inc.

- DuluxGroup Ltd

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd

- Nippon Paint Holdings Co., Ltd

- PPG Industries Inc.

- Propanraya

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction Boom in Emerging ASEAN Cities

- 4.2.2 Re-Painting Cycle Compression in Tier-1 Chinese Housing

- 4.2.3 OEM Shift to Water-Borne Auto Topcoats

- 4.2.4 Government "Green Ship" Retro-Fit Subsidies (Korea, Japan)

- 4.2.5 Mandated Cool-Roof Coatings in India's Smart-City Program

- 4.3 Market Restraints

- 4.3.1 Tightening VOC and Formaldehyde Caps (China GB/T 33372-2020, Etc.)

- 4.3.2 Titanium-Dioxide Price Volatility

- 4.3.3 Skills Deficit of Certified Industrial Coaters in Indonesia and Vietnam

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-Borne

- 5.1.2 Solvent-Borne

- 5.1.3 Powder Coating

- 5.1.4 Other Technologies (UV/ EB, High-Solids, etc.)

- 5.2 By Resin Type

- 5.2.1 Acrylic

- 5.2.2 Alkyd

- 5.2.3 Polyurethane

- 5.2.4 Epoxy

- 5.2.5 Polyester

- 5.2.6 Others (Phenolic, Ketonic, etc.)

- 5.3 By End-user Industry

- 5.3.1 Architectural/ Decorative

- 5.3.2 Automotive

- 5.3.3 Wood

- 5.3.4 Protective Coatings

- 5.3.5 General Industrial

- 5.3.6 Transportation

- 5.3.7 Packaging

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia and New Zealand

- 5.4.6 Indonesia

- 5.4.7 Thailand

- 5.4.8 Malaysia

- 5.4.9 Vietnam

- 5.4.10 Philippines

- 5.4.11 Singapore

- 5.4.12 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3TREESGROUP

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Asian Paints

- 6.4.4 Avian Brands

- 6.4.5 Axalta Coating Systems, LLC

- 6.4.6 BASF

- 6.4.7 Berger Paints India

- 6.4.8 Boysen Paints

- 6.4.9 Chokwang Paint

- 6.4.10 Davies Paints Philippines Inc.

- 6.4.11 DuluxGroup Ltd

- 6.4.12 Hempel A/S

- 6.4.13 Jotun

- 6.4.14 Kansai Paint Co., Ltd

- 6.4.15 Nippon Paint Holdings Co., Ltd

- 6.4.16 PPG Industries Inc.

- 6.4.17 Propanraya

- 6.4.18 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

建筑涂料市场:依树脂类型、技术、应用、最终用途及通路划分-2026-2032年全球市场预测涂料市场:2026-2032年全球市场预测(依树脂类型、技术、产品类型、基材、终端用户产业及通路划分)

建筑涂料市场:依树脂类型、技术、应用、最终用途及通路划分-2026-2032年全球市场预测涂料市场:2026-2032年全球市场预测(依树脂类型、技术、产品类型、基材、终端用户产业及通路划分) 2026年全球石膏板和保温承包商市场报告木材提取油市场:2026-2032年全球预测(按产品类型、应用、分销管道和最终用户划分)

2026年全球石膏板和保温承包商市场报告木材提取油市场:2026-2032年全球预测(按产品类型、应用、分销管道和最终用户划分) 2026年油漆涂料产业十大策略要务煅烧页岩市场:2026-2032年全球市场预测(依产品类型、应用、终端用户产业及通路划分)

2026年油漆涂料产业十大策略要务煅烧页岩市场:2026-2032年全球市场预测(依产品类型、应用、终端用户产业及通路划分) 瓷砖涂料市场规模、份额和成长分析:按产品类型、表面类型、应用、安装方法、最终用户、分销管道和地区划分-2026-2033年产业预测

瓷砖涂料市场规模、份额和成长分析:按产品类型、表面类型、应用、安装方法、最终用户、分销管道和地区划分-2026-2033年产业预测 2026-2030年全球油漆涂料市场

2026-2030年全球油漆涂料市场 涂料市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、製程、最终用户、功能、安装类型及解决方案划分

涂料市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、製程、最终用户、功能、安装类型及解决方案划分 欧洲油漆和涂料:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)

欧洲油漆和涂料:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)