|

市场调查报告书

商品编码

1939639

海底光缆:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Submarine Optical Fiber Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

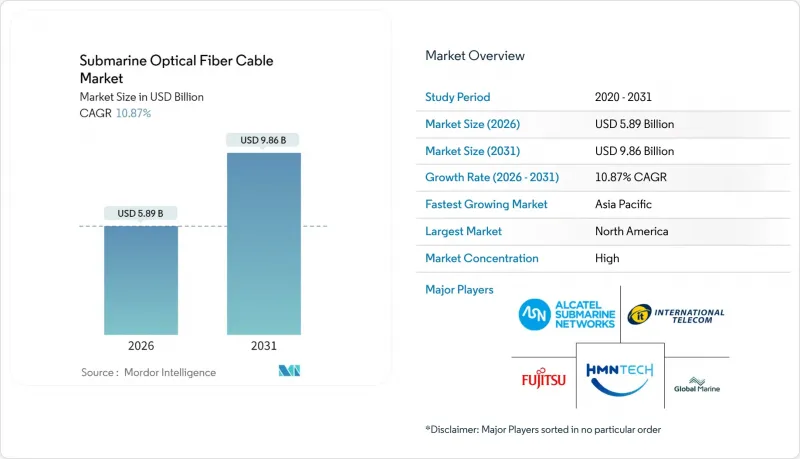

预计到 2026 年,海底光缆市场规模将达到 58.9 亿美元,高于 2025 年的 53.1 亿美元,预计到 2031 年将达到 98.6 亿美元。

预计2026年至2031年年复合成长率(CAGR)为10.87%。

超大规模云端服务供应商不断扩大投资,加速向400GbE/800GbE升级,以及空间復用(SDM)系统的商业部署,正在重塑洲际互联的竞争格局和经济模式。 60Tbps及以上的系统设计正逐渐成为标准,降低了单位频宽成本,并支援人工智慧密集资料流。容量扩展策略与国家安全相关的监管发展日益交织,例如,美国联邦通讯委员会(FCC)的2024-2025年海底光缆许可审查正在指导路由选择和供应商认证。同时,维修船的瓶颈和波罗的海的反覆中断显示地缘政治风险日益增加,推高了营运成本和保险费。

全球海底光缆市场趋势与洞察

智慧型手机普及率不断提高,对网路频宽的需求日益增长

受5G和新兴人工智慧工作负载对频宽需求不断增长的推动,洲际流量预计到2029年将以每年39%的速度成长。海底电缆的延迟仅为1-5毫秒,比卫星星系的延迟低几个数量级,使其在高频交易和工业IoT应用场景中保持竞争力。即将推出的6G规范旨在实现1Tbps的峰值速率,这推动了对能够处理800GbE波长的中继器的需求。南海路由核准的延误限制了新增容量,并导致流向东南亚的流量价格上涨。

超大规模云端和OTT在专用电缆领域的投资

Meta、Google、亚马逊和微软的私有化程度超过了传统的财团资金筹措,总投资超过200亿美元。超大规模资料中心业者资料中心内部的直接终端连接无需地面回程传输,从而降低了延迟和营运成本,同时增强了资料主权控制。谷歌的250Tbps「Dunant」计画和Meta的5万公里「沃特沃斯计画」正是这种新型垂直整合模式的典范。

运作高成本的维护和修理船舶

仅有60艘专用船舶维护600多个运作的系统,一旦发生多处故障,恢復时间将非常漫长。北极和太平洋地区的维修成本每次事故超过100万美元,且维修工作仅限于季节性天气窗口期,这使得高风险地区的年度保费上涨了15%至20%。

细分市场分析

到2025年,湿式设备将占海底光缆市场规模的52.74%,这主要得益于对20对及以上光纤设计的中继器需求不断增长。 Subcom公司正积极拓展其海上服务能力,以因应这项需求激增。随着地缘政治局势日益复杂,维修周期延长,专业维修船的价值也随之提升,辅助和海上服务正以11.86%的复合年增长率快速增长。

在长达25年的营运寿命期内,持续的维护收入为服务供应商提供了可预测的现金流。虽然陆基设施由于登陆站电力和监控系统的老化而面临稳定的更换需求,但它们对海底光缆市场的贡献仍然很小。

儘管单模光纤在2025年将占总收入的67.02%,但空分复用(SDM)多芯光纤预计到2031年将以每年13.62%的速度成长。诸如OFS公司的TeraWave SCUBA 4X等SDM设备可将容量提升四倍,从而缓解即将到来的香农极限。住友电工的耦合多芯光纤实现了0.158 dB/km的衰减,证明了SDM性能即使在跨越海洋的距离上也依然可靠。

Google在 Dunant 卫星上部署的 12 对光纤 SDM 架构已证明商业性可行性,并正在加速其更广泛的应用,而多模光纤仍仅限于办公室内部应用。

区域分析

北美在2025年将占据海底光缆市场36.25%的份额,这主要得益于超大规模丛集和健全的法规结构。谷歌投资10亿美元建造美日海底光缆将有助于提升太平洋地区的输电能力,而LS Cable在维吉尼亚投资6.81亿美元的设施将确保美国国内光缆供应的稳定性。

亚太地区预计将以11.40%的复合年增长率成长,这主要得益于数位经济项目和避开地缘政治热点的替代路线,例如印度的蓝色起源着陆项目和Softbank Corporation新建的跨太平洋海底光缆。中国供应商HMN Technologies和中天科技正在扩大生产,但美国的製裁迫使它们转向「一带一路」沿线市场。

欧洲正利用其成熟的跨大西洋走廊,同时推进远北光纤计划,以期为亚洲带来低延迟优势。欧盟范围内的海底电缆安全行动计画以及法国政府对阿尔卡特海底网路公司的收购,凸显了各国在基础建设方面的优先事项。欧盟的海底电缆安全行动计画制定了强有力的措施,以预防、侦测和应对海底电缆面临的威胁,并强调了欧盟保护关键基础设施的承诺。诺基亚完成对阿尔卡特海底网路公司向法国政府的出售,此举显示了海底电缆技术的战略重要性,也显示欧洲各国政府将这项技术视为重要的国家资产,并需要主权监管。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第3章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 智慧型手机普及率不断提高,对网路频宽的需求日益增长

- 扩大新兴地区的光纤连接

- 超大规模云端和OTT营运商投资专用电缆

- 通讯业者间400GbE/800GbE快速升级週期

- 推动建设低延迟的区域间路由

- 使用混合动力和数据电缆的离岸风力发电

- 市场限制

- 高昂的维修和维修成本

- 增加对低地球轨道卫星星系的投资

- 海底电缆登陆许可的地缘政治延误

- 浅水区光纤电缆被盗和破坏

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 宏观趋势(包括新冠肺炎疫情)的影响

- 投资分析

- 海底电缆计划资料库

第五章 市场规模与成长预测

- 按组件

- ウェットプラント设备

- 干式设备

- 补助サービスおよび船舶サービス

- 其他部件

- ケーブルタイプ别

- 单模光纤

- 多模光纤

- SDM/マルチコアファイバー

- クライアントタイプ别

- 通讯业者

- 内容和超大规模云端供应商

- 政府および研究机関ネットワーク

- 洋上エネルギー事业者

- その他のクライアントタイプ

- 容量设计别

- 16 Tbps 或更低的系统

- 16~60 Tbpsシステム

- 60 Tbps超システム

- 按地区

- 北美洲

- 我们

- 加拿大

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 法国

- 英国

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第6章 竞合情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Alcatel Submarine Networks Ltd.

- HMN Technologies Co., Ltd.

- Nexans SA

- Fujitsu Ltd.

- Global Marine Group Ltd.

- Orange Marine SAS

- Sumitomo Electric Industries Ltd.

- LS Cable and System Ltd.

- Jiangsu Hengtong Marine Cable Systems Co., Ltd.

- SB Submarine Systems Co., Ltd.

- IT International Telecom Inc.

- PT Communication Cable Systems Indonesia Tbk

- NTT Communications Corporation

- Verizon Communications Inc.

- Telstra Group Limited

- China Unicom Global Limited

- Telekom Malaysia Berhad

- Oman Telecommunications Company SAOG(Omantel)

- Meta Platforms, Inc.

- Amazon.com, Inc.

- Google LLC

第七章 市场机会与未来展望

The submarine optical fiber cable market size in 2026 is estimated at USD 5.89 billion, growing from 2025 value of USD 5.31 billion with 2031 projections showing USD 9.86 billion, growing at 10.87% CAGR over 2026-2031.

Heightened investment by hyperscale cloud providers, accelerating 400 GbE/800 GbE upgrade cycles, and the commercial roll-out of Space Division Multiplexing (SDM) systems are reshaping the competitive landscape and economics of intercontinental connectivity. Systems designed for 60 + Tbps are now routine, lowering unit bandwidth costs and enabling AI-intensive data flows. Capacity expansion strategies increasingly intersect with national-security rule-making, exemplified by the FCC's 2024-2025 overhaul of cable-licensing procedures, which is steering route selection and vendor qualification. At the same time, repair-ship bottlenecks and repeated Baltic-Sea disruptions reveal a growing exposure to geopolitical risks that elevate operating expenditure and insurance premiums.

Global Submarine Optical Fiber Cable Market Trends and Insights

Growing Smartphone Penetration and Rising Internet Bandwidth Demand

Intercontinental traffic is projected to climb 39% annually through 2029 as 5G and emerging AI workloads multiply bandwidth requirements. Submarine links sustain 1-5 millisecond latency, an order of magnitude lower than satellite constellations, preserving competitiveness for high-frequency trading and industrial IoT use cases. Forthcoming 6G specifications targeting 1 Tbps peak rates intensify the call for repeaters able to handle 800 GbE wavelengths. Unresolved route-approval delays in the South China Sea restrict new capacity, creating price premiums for Southeast-Asian traffic.

Hyperscale Cloud and OTT Investment in Private Cables

Private ownership by Meta, Google, Amazon, and Microsoft now eclipses traditional consortium funding and exceeds USD 20 billion in aggregate commitments. Direct termination inside hyperscaler data centers eliminates terrestrial backhaul, trimming latency and OPEX while tightening data-sovereignty control. Google's 250 Tbps Dunant and Meta's 50,000 km Project Waterworth exemplify the new vertical-integration model.

High Maintenance and Repair-Ship Costs

Just 60 specialized vessels support more than 600 active systems, extending restoration timelines when multiple outages occur. Arctic and trans-Pacific repairs exceed USD 1 million per incident and face seasonal weather windows, elevating insurance premiums by 15-20% annually in high-risk zones.

Other drivers and restraints analyzed in the detailed report include:

- Rapid 400 GbE/800 GbE Upgrade Cycle Among Carriers

- Push Toward Low-Latency Trans-Polar Routes

- Growing Investment in LEO Satellite Constellations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wet-plant equipment contributed 52.74% of the submarine optical fiber cable market size in 2025 and benefits from 20 + fiber-pair designs that intensify repeater demand. SubCom's expansion of marine fulfillment capabilities is aligned with this demand surge. Auxiliary and marine services are scaling at a 11.86% CAGR as complex geopolitical disruptions lengthen repair cycles and raise the value of specialized intervention vessels.

Continued maintenance revenue over a 25-year operational life adds predictable cash flows for service providers. Dry-plant equipment enjoys steady replacement demand as landing-station power and monitoring systems age, though it remains a smaller contributor to the submarine optical fiber cable market.

Single-mode fiber represented 67.02% of 2025 revenue; however, SDM multi-core fiber is forecast to grow at an annual rate of 13.62% to 2031. SDM units such as OFS's TeraWave SCUBA 4X deliver fourfold capacity improvements, mitigating the looming Shannon-limit crunch. Sumitomo Electric's coupled multi-core fiber achieves 0.158 dB/km attenuation, validating SDM performance over trans-oceanic spans.

Google's deployment of 12 fiber-pair SDM architecture on Dunant proves commercial viability and accelerates broader adoption. Multimode fiber remains limited to intra-station applications.

The Submarine Optical Fiber Cable Market Report is Segmented by Component (Wet-Plant Equipment, Dry-Plant Equipment, and More), Cable Type (Single-Mode Fiber, Multimode Fiber, and More), Client Type (Telecom Operators, Content and Hyperscale Cloud Providers, and More), Capacity Design (less Than or Equal To 16 Tbps Systems, 16-60 Tbps Systems, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 36.25% share of the submarine optical fiber cable market in 2025 is driven by a hyperscale cluster and strong regulatory frameworks. Google's USD 1 billion US-Japan cable commitment reinforces Pacific capacity while LS Cable's USD 681 million Virginia plant secures domestic supply resilience.

The Asia Pacific is projected to expand at a 11.40% CAGR, driven by digital economy programs and alternative routes that circumvent geopolitical flashpoints. India's Blue Origin landing and SoftBank's new trans-Pacific build typify this activity. Chinese vendors HMN Technologies and ZTT scale up production, although U.S. sanctions prompt them to shift toward Belt-and-Road markets.

Europe leverages mature trans-Atlantic corridors while championing the Far North Fiber project for Asia latency advantages. EU-wide cable-security action plans and the French State's acquisition of Alcatel Submarine Networks highlight sovereign-infrastructure priorities. The European Union's Action Plan on Cable Security establishes robust measures for preventing, detecting, and responding to threats against submarine cables, underscoring the EU's commitment to safeguarding its critical infrastructure. In a move highlighting the strategic importance of submarine cable technology, Nokia finalized the sale of Alcatel Submarine Networks to the French State, signaling European governments' view of this technology as a vital national asset warranting sovereign oversight.

- Alcatel Submarine Networks Ltd.

- HMN Technologies Co., Ltd.

- Nexans S.A.

- Fujitsu Ltd.

- Global Marine Group Ltd.

- Orange Marine SAS

- Sumitomo Electric Industries Ltd.

- LS Cable and System Ltd.

- Jiangsu Hengtong Marine Cable Systems Co., Ltd.

- S.B. Submarine Systems Co., Ltd.

- IT International Telecom Inc.

- PT Communication Cable Systems Indonesia Tbk

- NTT Communications Corporation

- Verizon Communications Inc.

- Telstra Group Limited

- China Unicom Global Limited

- Telekom Malaysia Berhad

- Oman Telecommunications Company S.A.O.G. (Omantel)

- Meta Platforms, Inc.

- Amazon.com, Inc.

- Google LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing smartphone penetration and rising internet bandwidth demand

- 4.2.2 Increasing fiber connectivity in emerging regions

- 4.2.3 Hyperscale cloud and OTT investment in private cables

- 4.2.4 Rapid 400 GbE/800 GbE upgrade cycle among carriers

- 4.2.5 Push toward Low-Latency trans-polar routes

- 4.2.6 Offshore wind farms adopting hybrid power-data cables

- 4.3 Market Restraints

- 4.3.1 High maintenance and repair-ship costs

- 4.3.2 Growing investment in LEO satellite constellations

- 4.3.3 Geopolitical cable-landing permit delays

- 4.3.4 Fiber-optic theft/vandalism in shallow waters

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Degree of Competition

- 4.7 Impact of Macro Trends (incl. COVID-19)

- 4.8 Investment Analysis

- 4.9 Submarine Cable Projects Database

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Wet-Plant Equipment

- 5.1.2 Dry-Plant Equipment

- 5.1.3 Auxiliary and Marine Services

- 5.1.4 Other Components

- 5.2 By Cable Type

- 5.2.1 Single-mode Fiber

- 5.2.2 Multimode Fiber

- 5.2.3 SDM / Multi-core Fiber

- 5.3 By Client Type

- 5.3.1 Telecom Operators

- 5.3.2 Content and Hyperscale Cloud Providers

- 5.3.3 Government and Research Networks

- 5.3.4 Offshore Energy Operators

- 5.3.5 Other Clinet Types

- 5.4 By Capacity Design

- 5.4.1 less than or equal to 16 Tbps Systems

- 5.4.2 16 - 60 Tbps Systems

- 5.4.3 above 60 Tbps Systems

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alcatel Submarine Networks Ltd.

- 6.4.2 HMN Technologies Co., Ltd.

- 6.4.3 Nexans S.A.

- 6.4.4 Fujitsu Ltd.

- 6.4.5 Global Marine Group Ltd.

- 6.4.6 Orange Marine SAS

- 6.4.7 Sumitomo Electric Industries Ltd.

- 6.4.8 LS Cable and System Ltd.

- 6.4.9 Jiangsu Hengtong Marine Cable Systems Co., Ltd.

- 6.4.10 S.B. Submarine Systems Co., Ltd.

- 6.4.11 IT International Telecom Inc.

- 6.4.12 PT Communication Cable Systems Indonesia Tbk

- 6.4.13 NTT Communications Corporation

- 6.4.14 Verizon Communications Inc.

- 6.4.15 Telstra Group Limited

- 6.4.16 China Unicom Global Limited

- 6.4.17 Telekom Malaysia Berhad

- 6.4.18 Oman Telecommunications Company S.A.O.G. (Omantel)

- 6.4.19 Meta Platforms, Inc.

- 6.4.20 Amazon.com, Inc.

- 6.4.21 Google LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

海底光缆市场:2026-2032年全球市场预测(依交付方式、光缆类型、敷设深度、最终用户及所有权模式划分)海底通讯电缆系统市场:2026-2032年全球市场预测(依资料传输速率、技术、部署类型、网路所有权类型、光纤对数、电缆长度和应用划分)

海底光缆市场:2026-2032年全球市场预测(依交付方式、光缆类型、敷设深度、最终用户及所有权模式划分)海底通讯电缆系统市场:2026-2032年全球市场预测(依资料传输速率、技术、部署类型、网路所有权类型、光纤对数、电缆长度和应用划分) 海底电缆市场规模、份额和趋势分析报告:按电压、组件、应用、最终用途、产品、地区和细分市场预测(2026-2033 年)UBM电镀服务市场(按电镀材料、基材、技术、应用和最终用途产业划分),全球预测,2026-2032年

海底电缆市场规模、份额和趋势分析报告:按电压、组件、应用、最终用途、产品、地区和细分市场预测(2026-2033 年)UBM电镀服务市场(按电镀材料、基材、技术、应用和最终用途产业划分),全球预测,2026-2032年 海底电缆市场规模、份额和成长分析(按服务类型、类型、电压、最终用途、绝缘材料和地区划分)-2026-2033年产业预测

海底电缆市场规模、份额和成长分析(按服务类型、类型、电压、最终用途、绝缘材料和地区划分)-2026-2033年产业预测 全球海底电缆检测设备市场

全球海底电缆检测设备市场 海底电缆检测设备市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、部署模式、地区和竞争细分,2020-2030 年预测)

海底电缆检测设备市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、部署模式、地区和竞争细分,2020-2030 年预测) 2032 年海底电缆市场预测:按组件、电缆类型、电压、服务、应用、最终用户和地区进行的全球分析

2032 年海底电缆市场预测:按组件、电缆类型、电压、服务、应用、最终用户和地区进行的全球分析 全球海底电缆市场(2025-2029)

全球海底电缆市场(2025-2029) 海底电缆的全球市场:市场预测(2023年~2029年)

海底电缆的全球市场:市场预测(2023年~2029年)