|

市场调查报告书

商品编码

1939647

气雾剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Aerosol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

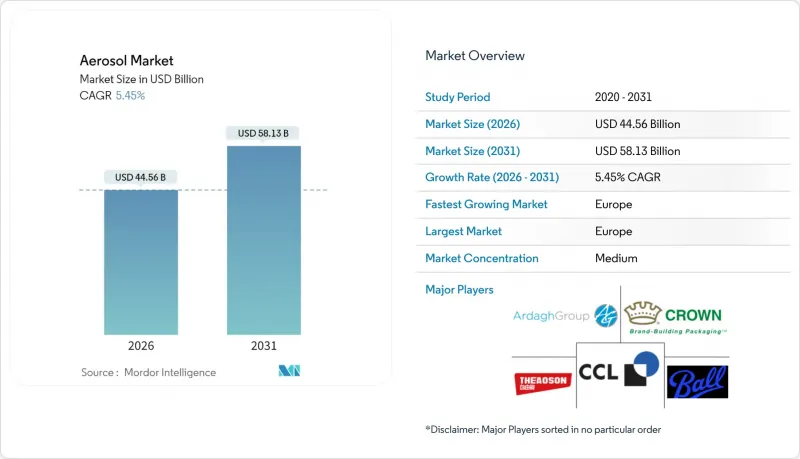

2025年气雾剂市值为422.6亿美元,预计2031年将达到581.3亿美元,2026年为445.6亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.45%。

这种稳定成长主要源自于消费者对便捷加压包装产品在个人护理、医疗和工业应用领域的偏好。尤其是在欧洲,儘早遵守氟碳化合物法规正在加速从氢氟碳化合物 (HFC) 向氢氟烯烃 (HFO) 的过渡。欧洲的监管主导正在影响全球产品设计,而电子商务和直销管道则扩大了产品覆盖范围,并增强了对轻质可回收罐的需求。对低碳包装的追求,加上铝价的持续波动,加剧了材料供应商之间的竞争,但也为透过使用再生材料和遵守通用废弃物计划实现了产品差异化创造了机会。

全球气雾剂市场趋势与洞察

个人护理和卫生用品对气雾剂的需求不断增长

美容和个人护理行业的优质化正在推动加压容器的普及。加压容器具有精准计量、卫生易用和保质期长的优点。印度护肤市场正经历成长,这主要得益于防晒喷雾和混合型保湿产品的流行。全球品牌所有者正在加强可重复填充金属罐和无气系统的创新研发,以满足挥发性有机化合物(VOC)法规的要求,同时保持产品的便利性。低VOC干洗髮的专利申请表明,主要企业正在优先考虑排放规性和对头皮友好的配方。欧洲製造商透过强调气雾剂能够保护内容物免受氧化和污染,从而提升品牌价值。整体而言,高阶产品的价格稳定性抵消了推进剂配方调整的成本,从而维持了气雾剂市场的成长。

扩大油漆和涂料喷涂应用

工业用户正在采用静电喷涂技术,以减少高达 30% 的过喷,从而提高大面积应用的材料利用率。东南亚的基础设施建设蓬勃发展(预计到 2024 年,印尼的油漆需求将超过 100 万吨),带动了对用于钢材、混凝土和复合材料表面的防护气雾剂的需求增长。汽车修补漆行业青睐补漆气雾剂,因为它们柔软性。即使是符合更严格 VOC 排放标准的水性组合药物,仍需要推进剂来维持雾化,这促使人们采用二甲醚等替代推进剂。农业无人机现在依靠气雾剂相容组合药物在狭窄的作物行间均匀喷洒农药,这为推进剂供应商开闢了新的收入来源。符合 ISO 14001 标准正在指导环保溶剂和添加剂的采购。

严格的VOC/CFC法规

不同地区对挥发性有机化合物的监管限值各不相同,导致需要针对特定地区制定配方,并增加双重认证成本。在韩国测试的消费者除臭剂在距离一公尺处释放的总挥发性有机化合物浓度为13.89 ppm,某些苯的浓度超过了美国政府工业卫生学家协会(ACGIH)提案的基准值,这使得浓香型气雾剂产品的合规性面临挑战。欧盟的氟碳化合物配额竞标推高了高全球暖化潜值(GWP)混合物的价格,迫使即使是小规模的品牌也采用更干净的化学配方。空气标籤评分(ALS)标准要求提供室内低排放的证明,并延长了新产品上市时间。如果旧推进剂的淘汰日期提前,则与其相关的库存可能面临减损风险。全球经销商必须应对错综复杂的法规,这增加了跨国营运的物流成本。

细分市场分析

2025年,氢氟碳化合物(HFCs)在气雾剂市场占据40.62%的份额,这得益于其成熟的供应链和广泛的配方相容性。然而,日益严格的淘汰配额正促使客户转向氢氟烯烃(HFOs),预计到2031年,HFOs的年复合成长率将达到6.58%。生物甲醇衍生的二甲醚因其负碳排放特性以及世界卫生组织核准其用于医疗用途而备受关注。氧化亚氮和二氧化碳在食品和工业领域仍然占据主导地位,因为这些领域对不可燃性要求极高。儘早完成使用HFO推进剂的医疗设备认证的公司可以享受更高的价格和更长期的合约条款。

不同地区的采用率各不相同,欧洲领先限制了氯氟烃(CFC)的使用,而北美各州的法规正在加速这一转变。在亚太地区,大型跨国个人护理公司遵循全球配方标准,而本土品牌则逐步推出替代品。能够同时提供推进剂和永续性认证的供应商需求稳定。重油(HFO)产能的投资有助于降低长期供应风险,并稳定下游填料的成本结构。

区域分析

预计到2025年,欧洲将占全球气雾剂市场32.12%的份额,并在2031年之前以6.41%的复合年增长率持续成长。严格的氟碳化合物法规和完善的回收基础设施正在推动重油推进剂和低碳金属罐的快速普及。德国、法国和英国在研发投资方面处于主导,并专注于高端个人保健产品和工业配方技术。零售商正在推广带有环保标籤的产品,强调气雾剂产品作为无污染产品的优势。早期监管政策的推出使欧洲灌装商能够将技术授权给海外企业,并在新兴市场中抢占份额。

亚太地区预计将迎来最快的销售量成长,这主要得益于基础设施的改善和自由裁量权支出的增加。中国已在铝生产领域占据主导地位,并在供应链中获得了成本优势。然而,其煤炭密集型冶炼製程引发了人们对碳排放的担忧,从而推动了对再生铝的需求。印度不断扩张的护肤市场刺激了当地的灌装产能,而印尼年产百万吨的涂料产业则支撑了对工业喷漆的需求。日本和韩国则更加重视精密阀门和安全认证,并向该地区出口高性能零件。

北美市场虽已成熟,但仍是主要贡献者,其每年约40亿罐气雾剂的销量便是主要驱动力。 36个州已实施通用废弃物法规,降低了废弃物处理的门槛,并鼓励推行上门回收计画。电子商务的蓬勃发展加速了无需低温运输的便携式食品和清洁气雾剂产品的普及。拜尔斯道夫斥资3.5亿欧元扩建位于锡劳的工厂后,墨西哥正崛起为战略出口枢纽,以满足区域个人照护需求。加拿大对低挥发性有机化合物(VOC)标准的重视,与美国的法规相呼应,正在简化跨国产品上市流程。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 个人护理和卫生气雾剂的需求不断增长

- 扩大油漆和涂料喷涂应用

- 各行业广泛使用便利的便携式包装

- 监管部门向低全球暖化潜势推进剂过渡,推动设备升级

- 食品和乳製品气雾剂容器的电子商务成长

- 市场限制

- 严格的VOC/CFC法规

- 易燃性和安全风险

- 能源密集型铝供应趋紧可能会对利润率造成压力。

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按推进剂类型

- 二甲醚(DME)

- 氢氟碳化合物(HFCs)

- 氢氟烯烃(HFOs)

- 其他类型(氧化亚氮、二氧化碳等)

- 可以透过类型

- 钢

- 铝

- 塑胶

- 其他类型的罐(玻璃罐和锡罐)

- 透过使用

- 车

- 个人护理

- 食物

- 农业

- 家居用品

- 工业和技术

- 医疗保健

- 油漆和涂料

- 其他用途(清洁用品、喷雾等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- ACT Aerosol Chemie Technik GmbH

- Ardagh Group SA,

- Ball Corporation

- Beiersdorf AG

- CCL Container

- Coster Tecnologie Speciali SpA

- Crown

- Guangdong Theaoson Technology Co. Ltd.

- Henkel AG & Co. KGaA

- Honeywell International Inc.

- Hydrokem Aerosols Limited

- Reckitt Benckiser Group PLC

- SC Johnson & Son Inc.

- Shenzhen Sunrise New Energy Co. Ltd.

- Suhan Aerosol

- Toyo Seikan Group Holdings Ltd.

第七章 市场机会与未来展望

The Aerosol Market was valued at USD 42.26 billion in 2025 and estimated to grow from USD 44.56 billion in 2026 to reach USD 58.13 billion by 2031, at a CAGR of 5.45% during the forecast period (2026-2031).

Steady gains stem from consumer preference for convenient, pressurized dispensing across personal care, medical, and industrial uses. Early compliance with evolving F-gas regulations, particularly in Europe, is accelerating the transition from hydrofluorocarbons (HFCs) to hydrofluoroolefins (HFOs). Europe's regulatory leadership is shaping global formulations, while e-commerce and direct-to-consumer channels are extending product reach and reinforcing demand for lightweight, recyclable cans. Ongoing aluminum price fluctuations and the pursuit of lower-carbon packaging intensify competition among material suppliers, yet they also create opportunities for product differentiation through recycled content and universal waste program coverage.

Global Aerosol Market Trends and Insights

Rising Demand for Personal-Care and Hygiene Aerosols

Premiumization in beauty and grooming drives the wider use of pressurized formats, which offer precise dosing, hygienic delivery, and longer product shelf life. India's skincare segment is experiencing growth, driven by the popularity of SPF-infused sprays and hybrid moisturizers. Global brand owners are bolstering innovation pipelines around refillable metal cans and airless systems to address VOC caps while retaining convenience credentials. Patent filings for low-VOC dry shampoo underscore how leading firms prioritize both emissions compliance and scalp-friendly formulations. European makers strengthen brand equity by spotlighting aerosols' ability to shield contents from oxidation and contamination. Collective effect: premium price elasticity offsets propellant reformulation costs and sustains aerosol market growth.

Expansion of Paints-and-Coatings Spray Applications

Industrial users adopt electrostatic spray technology to curb overspray by up to 30%, enhancing material efficiency in large-area coatings. Southeast Asian infrastructure booms-Indonesia's paint demand topped 1 million tons in 2024-support higher volumes for protective aerosols used on steel, concrete, and composite surfaces. Auto refinish segments favor touch-up aerosols for color-matching versatility. Water-based formulas compliant with stricter VOC ceilings still require propellants that maintain atomization, thereby driving the uptake of dimethyl ether and other alternatives. Agricultural drones now rely on aerosol-compatible formulations to spread pesticides evenly across narrow rows, opening new revenue streams for propellant suppliers. Compliance with ISO 14001 standards guides the procurement of eco-optimized solvents and additives.

Stringent VOC/F-gas Regulations

Divergent limits on volatile organic compounds oblige region-specific formulations and double certification costs. Consumer deodorants tested in Korea emitted 13.89 ppm of total VOC at a 1-meter distance, with certain benzene levels exceeding proposed ACGIH limits, indicating compliance hurdles for fragrance-heavy aerosols. The European Union's F-gas quota auction elevates the price of high-GWP blends, compelling even small brands to adopt cleaner chemistries. Air Label Score criteria force proof of low indoor emissions, extending time-to-market for new SKUs. Inventory tied to legacy propellants risks write-downs if phaseout dates accelerate. Global distributors must navigate a patchwork of rules, which raises logistics overhead for multi-country rollouts.

Other drivers and restraints analyzed in the detailed report include:

- Convenience-Driven Portable Packaging Across Sectors

- Regulatory Shift to Low-GWP Propellants Spurring Re-tooling

- Energy-Intensive Aluminum Supply Tightening Can Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydrofluorocarbons held a 40.62% market share in the aerosol sector in 2025, underpinned by well-established supply chains and broad formulation compatibility. Yet tightening phase-down quotas are steering customers toward hydrofluoro-olefins, which are projected to post a 6.58% CAGR through 2031. Dimethyl ether, produced from bio-methanol, is drawing attention for its negative carbon intensity profile and WHO endorsement for medical uses. Nitrous oxide and carbon dioxide still dominate edible and technical segments where non-flammability is mandatory. Early movers completing medical device validations with HFO propellants enjoy premium pricing and longer contract tenures.

Adoption rates vary by region, with Europe leading due to earlier F-gas restrictions, while North America accelerates the transition through state-level mandates. In the Asia-Pacific region, larger multinational personal care players follow global formulation standards, whereas local brands gradually phase in alternatives. Suppliers capable of offering bundled propellant plus sustainability certification packages capture loyal demand. Investments in HFO capacity mitigate long-term supply risk and stabilize cost structures for downstream fillers.

The Aerosol Market Report is Segmented by Propellant Type (Dimethyl Ether, Hydrofluorocarbons, Hydrofluoro Olefins, and Other Types), Can Type (Steel, Aluminum, Plastic, and Other Can Types), Application (Automotive, Personal Care, Food Products, Agriculture, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe accounted for 32.12% of the global aerosol market in 2025 and is forecast to grow at a 6.41% CAGR through 2031. Stringent F-gas legislation and robust recycling infrastructure are spurring the rapid uptake of HFO propellants and low-carbon metal cans. Germany, France, and the United Kingdom lead research and development investments focused on premium personal-care and industrial formulations. Retailers promote products bearing eco-labels that highlight the aerosols' benefits of contamination-free delivery. Earlier compliance timetables enable European fillers to license technology abroad and capture a share in emerging markets.

Asia-Pacific shows the fastest incremental volume gains, driven by infrastructure growth and rising discretionary spending. China's aluminum dominance secures supply-chain cost advantages, although coal-intensive smelting raises concerns about its carbon footprint, which stimulates demand for recycled aluminum. India's expanding skincare market stimulates local filling capacity, while Indonesia's one-million-ton paint sector buoys industrial sprays. Japan and South Korea emphasize precision valves and safety certifications, exporting high-performance components across the region.

North America remains a mature but sizable contributor, buoyed by almost 4 billion aerosol cans sold annually. Universal waste rules adopted by 36 states lower disposal barriers and promote curbside collection schemes. E-commerce accelerates adoption of portable food and cleaning aerosols that bypass cold chains. Mexico emerges as a strategic export platform after Beiersdorf's EUR 350 million Silao expansion, feeding regional personal-care demand. Canada's focus on low-VOC standards parallels U.S. regulations, streamlining multi-country product launches.

- ACT Aerosol Chemie Technik GmbH

- Ardagh Group S.A,

- Ball Corporation

- Beiersdorf AG

- CCL Container

- Coster Tecnologie Speciali S.p.A.

- Crown

- Guangdong Theaoson Technology Co. Ltd.

- Henkel AG & Co. KGaA

- Honeywell International Inc.

- Hydrokem Aerosols Limited

- Reckitt Benckiser Group PLC

- S.C. Johnson & Son Inc.

- Shenzhen Sunrise New Energy Co. Ltd.

- Suhan Aerosol

- Toyo Seikan Group Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for personal-care and hygiene aerosols

- 4.2.2 Expansion of paints-and-coatings spray applications

- 4.2.3 Convenience-driven portable packaging across sectors

- 4.2.4 Regulatory shift to low-GWP propellants spurring re-tooling

- 4.2.5 E-commerce growth of food/dairy dispensing aerosols

- 4.3 Market Restraints

- 4.3.1 Stringent VOC/F-gas regulations

- 4.3.2 Flammability and safety liabilities

- 4.3.3 Energy-intensive aluminium supply tightening can margins

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Propellant Type

- 5.1.1 Dimethyl Ether (DME)

- 5.1.2 Hydrofluorocarbons (HFC)

- 5.1.3 Hydrofluoro Olefins (HFO)

- 5.1.4 Other Types (Nitrous Oxide, Carbon Dioxide, etc.)

- 5.2 By Can Type

- 5.2.1 Steel

- 5.2.2 Aluminum

- 5.2.3 Plastic

- 5.2.4 Other Can Types (Glass and Tin)

- 5.3 By Application

- 5.3.1 Automotive

- 5.3.2 Personal Care

- 5.3.3 Food Products

- 5.3.4 Agriculture

- 5.3.5 Household Products

- 5.3.6 Industrial and Technical

- 5.3.7 Medical

- 5.3.8 Paints and Coatings

- 5.3.9 Other Applications (Cleaning Products, Sprays, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ACT Aerosol Chemie Technik GmbH

- 6.4.2 Ardagh Group S.A,

- 6.4.3 Ball Corporation

- 6.4.4 Beiersdorf AG

- 6.4.5 CCL Container

- 6.4.6 Coster Tecnologie Speciali S.p.A.

- 6.4.7 Crown

- 6.4.8 Guangdong Theaoson Technology Co. Ltd.

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Honeywell International Inc.

- 6.4.11 Hydrokem Aerosols Limited

- 6.4.12 Reckitt Benckiser Group PLC

- 6.4.13 S.C. Johnson & Son Inc.

- 6.4.14 Shenzhen Sunrise New Energy Co. Ltd.

- 6.4.15 Suhan Aerosol

- 6.4.16 Toyo Seikan Group Holdings Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

气雾剂稀释剂市场:依推进剂类型、产品类型、通路、应用和最终用户划分-2026-2032年全球预测

气雾剂稀释剂市场:依推进剂类型、产品类型、通路、应用和最终用户划分-2026-2032年全球预测 全球气雾剂市场规模、份额、趋势和成长分析报告(2026-2034)

全球气雾剂市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球气雾剂市场报告

2026年全球气雾剂市场报告 气雾剂市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)

气雾剂市场机会、成长驱动因素、产业趋势分析及预测(2026-2035) 气雾剂市场规模、份额和成长分析(按推进剂类型、推进方式、阀门类型、材料、类型、最终用途、应用和地区划分):产业预测(2026-2033 年)气雾剂市场(按应用、产品类型、推进剂类型、分销管道和包装材料)—2025-2032 年全球预测气雾剂盖市场按材料类型、分销管道、封闭类型、最终用途行业和应用划分 - 全球预测,2025-2032气雾剂致动器市场按应用、推进剂类型、致动器类型、分销管道、容器材料和最终用户划分 - 全球预测 2025-2032

气雾剂市场规模、份额和成长分析(按推进剂类型、推进方式、阀门类型、材料、类型、最终用途、应用和地区划分):产业预测(2026-2033 年)气雾剂市场(按应用、产品类型、推进剂类型、分销管道和包装材料)—2025-2032 年全球预测气雾剂盖市场按材料类型、分销管道、封闭类型、最终用途行业和应用划分 - 全球预测,2025-2032气雾剂致动器市场按应用、推进剂类型、致动器类型、分销管道、容器材料和最终用户划分 - 全球预测 2025-2032 美国气雾剂市场规模、份额和趋势分析报告:按材料、类型、推进剂类型、应用和细分市场预测,2025 年至 2033 年

美国气雾剂市场规模、份额和趋势分析报告:按材料、类型、推进剂类型、应用和细分市场预测,2025 年至 2033 年 到 2030 年气溶胶致动器市场预测:按类型、材料、应用和地区分類的全球分析

到 2030 年气溶胶致动器市场预测:按类型、材料、应用和地区分類的全球分析