|

市场调查报告书

商品编码

1939653

苯乙烯嵌段共聚物(SBC):市场份额分析、产业趋势与统计、成长预测(2026-2031)Styrenic Block Copolymers (SBCs) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

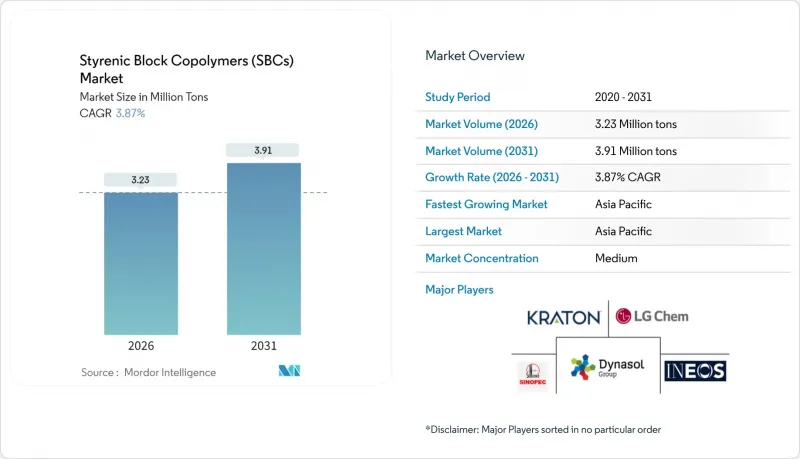

预计到 2026 年,苯乙烯嵌段共聚物 (SBC) 的市场规模将达到 323 万吨。

这意味着产量将从 2025 年的 311 万吨增加到 2031 年的 391 万吨。从 2026 年到 2031 年,预计年复合成长率为 3.87%。

儘管市场需求已趋于成熟,但苯乙烯嵌段共聚物 (SBC) 市场仍受益于其广泛的应用领域,从沥青改质剂和防水卷材到高价值介电薄膜,无所不包。多角化经营使生产者免受单一产业週期性波动的影响,而原料整合和接近性终端用户的区域优势也日益成为竞争优势的关键所在。亚太地区持续推动市场成长,各国政府对指定使用聚合物改质沥青和防水卷材的建设计划(包括高速公路、铁路网和高层建筑)进行投资。同时,氢化级苯乙烯嵌段专利到期为中端供应商创造了发展空间,而电动汽车电容器磺酸盐化学的突破性进展也预示着苯乙烯嵌段共聚物 (SBC) 市场未来可能出现更多高价值细分领域。

全球苯乙烯嵌段共聚物(SBC)市场趋势及展望

沥青回收强制令推动性能要求

欧盟和美国的立法者已将最低再生材料含量要求纳入道路建设标准,鼓励设计人员优先选择即使在使用轮胎或塑胶衍生油替代原生沥青的情况下也能保持机械完整性的聚合物体系。近期测试证实,SBS改质混合料在反覆冻融循环和氧化压力作用下性能优于未改质沥青,满足更严格的使用寿命标准。由于再生材料的多样性增加了配方的复杂性,能够提供满足高杂质含量要求的苯乙烯嵌段共聚物(SBC)的供应商享有价格优势。虽然资金筹措机制正在推动市场需求,但区域回收网路的缺乏以及热解装置许可证审批耗时较长,导致短期供应受限。因此,随着回收要求从联邦立法逐步落实到地方政府采购,苯乙烯嵌段共聚物(SBC)市场正经历稳定的吨位成长。

亚太地区基础建设热潮推动了防水材料的需求。

中国、印度、越南和印尼创纪录的公共支出持续刺激桥樑、地铁和大型住宅开发项目对聚合物改质防水卷材的需求。 SCG Chemicals公司斥资7亿美元对其龙山工厂进行升级改造,标誌着这家综合性生产商正转向使用柔性乙烷原料,以满足沥青和建筑防水卷材对苯乙烯嵌段共聚物(SBC)的结构性接近性。区域建筑商在热带、沙漠和高山气候条件下的高速公路建设中指定使用苯乙烯嵌段共聚物(SBS)改性黏合剂,以确保低温抗裂性和高温路面抗车辙性能。靠近建筑中心降低了运输成本并缩短了交货时间,这些优势预计将推动亚太地区苯乙烯嵌段共聚物(SBC)的市场份额在2024年超过57%。儘管劳动力短缺和审批延误在某些情况下导致计划进度停滞,但多年的政府预算为製造商制定到2030年的产能扩张计划提供了支持。

冷拌技术面临的挑战与传统路面技术进行比较。

加拿大、德国和美国多个州的政府机构正在试行使用室温固化的乳液型冷拌路面,以减少沥青搅拌站的温室气体排放。早期现场性能评估表明,无聚合物配方可能满足地方和次要道路的规范要求,从而有可能降低交通流量相对较低的地区对苯乙烯嵌段共聚物(SBS)的需求。然而,在交通繁忙的城市主干道上,SBS提供的抗车辙性能仍然是必要的。推广应用的障碍包括施工人员的熟悉程度、长期耐久性检验、特殊乳化剂供应有限。因此,儘管冷拌替代技术可能会限制某些细分市场的成长潜力,但苯乙烯嵌段共聚物(SBC)市场的核心预计仍将集中在高性能路面领域。

细分市场分析

到2025年,苯乙烯-丁二烯-苯乙烯(SBS)将继续占据苯乙烯嵌段共聚物(SBC)市场71.48%的主导份额,这印证了其在沥青、鞋类和压敏黏着剂等领域的高性价比优势。该聚合物成熟的供应链、广泛的加工技术和配方灵活性降低了其在大规模生产应用中的替代风险。儘管SEBS和SEPS等氢化级苯乙烯嵌段共聚物的产量较低,但由于汽车製造商、家电品牌以及电线电缆製造商对耐热性、抗紫外线线性和耐油性等基准值的不断提高,预计到2031年,其复合年增长率将达到4.43%,成为增长最快的产品。在专利相关费用取消以及基于云端的CAE平台商业化加速等级选择等因素的推动下,预计氢化级苯乙烯嵌段共聚物市场规模在预测期内将增加约15万吨。

同时,SIS在溶剂型压敏黏着剂、造口护理用品和医用敷料胶带等特殊应用领域保持领先地位,其固有的黏性和抗泛化性能弥补了其价格溢价。製造商正在进一步改进氢化SIS,以减少热熔加工过程中的氧化交联,从而扩大其在卫生用品领域的应用范围。原料的柔软性,特别是优先使用异戊二烯而非价格较高的丁二烯,为SIS生产商提供了抵御原料价格波动的有效途径。这些趋势,加上聚合物类型的多样化,正在保护苯乙烯嵌段共聚物(SBC)市场免受宏观经济週期性波动的影响,同时为长期创新蓝图奠定基础。

《苯乙烯嵌段共聚物 (SBC) 报告》按聚合物类型(苯乙烯-丁二烯-苯乙烯 (SBS)、苯乙烯-异戊二烯-苯乙烯 (SIS)、氢化苯乙烯嵌段共聚物 (HSBC))、应用领域(沥青、欧洲地区、鞋类、聚合物改性、黏合剂和密封剂等)以及地区(南美洲亚地区进行分析)。市场预测以吨为单位。

区域分析

亚太地区在苯乙烯嵌段共聚物(SBC)市场占据主导地位,预计到2025年将占全球市场份额的56.63%,这反映了其作为全球製造地和重要基础设施建设重点区域的地位。位置中国沿海地区、韩国和东协炼油走廊的资本密集型乙烯-丙烯联合装置提供了具有竞争力的原料,而国内建筑公司透过多年期的高速公路、港口和地铁计划确保了稳定的需求。越南决定扩大其乙烷裂解产能,显示该地区在原料供应方面柔软性,而印度的快速都市化则为防水卷材的需求提供了可持续的基础。政策主导的工业化、电子产业群聚以及加速的汽车电气化正在推动氢化SBC的应用,预计到2031年,该地区的复合年增长率将达到4.21%,高于全球平均水平。

在北美,联邦政府的基础设施支出计画将投入数十亿美元用于州际公路维修和机场跑道重铺,这正在推动市场发展。同时,在苯乙烯嵌段共聚物(SBC)市场,由于英力士苯领公司永久关闭了其位于萨尼亚工厂的年产43万吨的苯乙烯生产线,国内苯乙烯供应量有所下降。这导致商业单体供应紧张,进一步巩固了垂直整合企业的市场主导地位。沥青回收的强制性规定推动了黏合剂混合物中聚合物浓度的提高,而该地区的Start-Ups企业生态系统则推动了用于电动车电力电子的SBC基介电薄膜的发展。然而,由于页岩气液化产品和墨西哥湾沿岸飓风的影响,原物料价格波动,造成了不确定性,并限制了企业的扩张计画。

欧洲是苯乙烯嵌段共聚物 (SBC) 市场中一个成熟且技术先进的细分市场,优先考虑永续性和循环经济。高昂的能源价格和严格的环境法规迫使生产商以最佳运转率运营,推动工厂合理化,同时也提高了製程效率。诸如「绿色交易」和「生产者延伸责任制」等监管驱动因素刺激了对可回收和可再生聚合物系统的需求,其中SEBS 和磺酸盐SBC 在食品接触材料和医用导管应用领域备受青睐。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧盟和美国的沥青回收强制令

- 亚太地区基础建设蓬勃发展(高速公路、防水工程)

- 疫情导致一次性卫生薄膜需求增加

- 科腾公司汇丰银行级专利到期,鼓励新进业者。

- 用于下一代电动汽车电容器的磺酸盐SBC

- 市场限制

- 与原油相关的苯乙烯-丁二烯原料价格波动

- 无沥青冷拌铺路技术

- POE/POP弹性体可作为包装中SBC的替代品

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按聚合物类型

- 苯乙烯-丁二烯-苯乙烯(SBS)

- 苯乙烯-异戊二烯-苯乙烯(SIS)

- 氢化SBC(HSBC)

- 透过使用

- 沥青改质(铺路和屋顶)

- 鞋类

- 聚合物改性

- 黏合剂和密封剂

- 其他用途(医疗设备、电线电缆等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 土耳其

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 埃及

- 奈及利亚

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势(併购、合资、产能)

- 市占率(%)/排名分析

- 公司简介

- Asahi Kasei Corporation

- Avient Corporation

- Dynasol Group

- Eni SpA

- INEOS

- Kraton Corporation

- Kuraray Co., Ltd.

- LCY

- LG Chem

- Sibur

- Sinopec

- TSRC

- ZEON Corporation

第七章 市场机会与未来展望

Styrenic Block Copolymers market size in 2026 is estimated at 3.23 Million tons, growing from 2025 value of 3.11 Million tons with 2031 projections showing 3.91 Million tons, growing at 3.87% CAGR over 2026-2031.

Despite a mature demand base, the styrenic block copolymers market continues to benefit from its wide application spread, ranging from asphalt modification and waterproofing membranes to high-value dielectric films. Diversification protects producers from single-sector cyclicality, while feedstock integration and regional proximity to end users increasingly dictate competitive advantage. The Asia-Pacific region remains the growth engine as governments channel capital toward expressways, rail links, and high-rise construction that specify polymer-modified bitumen and membranes. Simultaneously, patent expiries in hydrogenated grades open space for mid-tier suppliers, and breakthroughs in sulfonated chemistries for EV capacitors hint at future premium niches for the styrenic block copolymers market.

Global Styrenic Block Copolymers (SBCs) Market Trends and Insights

Asphalt-Recycling Mandates Drive Performance Requirements

Legislators in the EU and United States have embedded minimum recycled-content thresholds into road construction codes, prompting designers to favor polymer systems that preserve mechanical integrity when tire-derived or plastic-derived oils replace virgin bitumen. Recent trials confirm that SBS-modified mixes outperform unmodified asphalt under repeated freeze-thaw cycles and oxidative stress, thereby meeting tougher service-life criteria. Suppliers capable of tailoring styrenic block copolymers to higher impurity loads enjoy a pricing premium, because recyclate variability increases formulation complexity. Although funding mechanisms accelerate market pull, gaps in regional collection networks and lengthy permitting cycles for pyrolysis units keep short-term supply tight. Consequently, the styrenic block copolymers market secures incremental tonnage growth as recycling mandates cascade from federal statutes to municipal procurement.

APAC Infrastructure Boom Accelerates Waterproofing Demand

Record-level public spending across China, India, Vietnam, and Indonesia continues to stimulate consumption of polymer-modified membranes for bridges, subways, and mega-residential complexes. SCG Chemicals' USD 700 million upgrade at its Long Son complex illustrates how integrated producers pivot to flexible ethane feedstock in anticipation of structural demand for SBCs in asphalt and building membranes. Regional contractors specify SBS-modified binders for expressways that traverse tropical, desert, and alpine climates, thereby guaranteeing low-temperature crack resistance and high-temperature rutting stability. Proximity to construction centers lowers freight cost and shortens delivery lead times, advantages that push APAC's share of the styrenic block copolymers market beyond 57% in 2024. While labor shortages and permitting delays occasionally stall project timelines, multi-year government budgets underpin visibility for producers mapping capacity additions through 2030.

Cold-Mix Technologies Challenge Traditional Applications

Government agencies in Canada, Germany, and several U.S. states have trialed emulsion-based cold-mix pavements that cure at ambient temperature, reducing greenhouse-gas emissions from asphalt plants. Early-stage field performance suggests that polymer-free recipes can meet rural and secondary road specifications, potentially eroding SBS demand where traffic loads are modest. Nonetheless, heavy-traffic urban arterials still require the rutting resistance imparted by SBS. Implementation barriers include contractor familiarity, untested long-term durability, and limited supply of specialized emulsifiers. Hence, although cold-mix alternatives cap upside in certain subsegments, the styrenic block copolymers market retains its core in high-performance pavements.

Other drivers and restraints analyzed in the detailed report include:

- Pandemic-Driven Hygiene Film Applications Create New Demand Vectors

- Sulfonated SBCs Unlock High-Value EV Capacitor Space

- POE/POP Elastomers Replace SBCs in Flexible Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Styrene-Butadiene-Styrene retained a commanding 71.48% share of the styrenic block copolymers market in 2025, underscoring cost-aligned performance in asphalt, footwear, and pressure-sensitive adhesives. The polymer enjoys a well-established supply chain, broad processing familiarity, and formulation versatility that limit substitution risk in mass-volume applications. Hydrogenated members such as SEBS and SEPS contributed a smaller tonnage base but registered the fastest 4.43% CAGR to 2031 as automakers, consumer-electronics brands, and wire-and-cable producers specified higher thermal, UV, and oil-resistance thresholds. The styrenic block copolymers market size for hydrogenated grades is projected to increase by nearly 0.15 million tons during the forecast window, buoyed by the collapse of patent-related royalties and the commercialization of cloud-enabled CAE platforms that accelerate grade selection.

In parallel, SIS maintained a specialized role in solvent-borne pressure-sensitive adhesives, ostomy-care appliances, and medical drape tapes where intrinsic tack and bloom resistance outweigh price premiums. Producers have optimized hydrogenated SIS variants to cut oxidative cross-linking during hot-melt processing, broadening their fit for hygiene applications. Feedstock mix flexibility, especially the ability to favor isoprene over high-priced butadiene, gives SIS producers a hedge against raw-material volatility. Collectively, these dynamics ensure that polymer-type diversification shields the styrenic block copolymers market from macroeconomic cyclicality while anchoring long-term innovation roadmaps.

The Styrenic Block Copolymers Report is Segmented by Polymer Type (Styrene-Butadiene-Styrene (SBS), Styrene-Isoprene-Styrene (SIS), and Hydrogenated SBCs (HSBC)), Application (Asphalt Modification, Footwear, Polymer Modification, Adhesives and Sealants, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific's dominant 56.63% 2025 share of the styrenic block copolymers market reflects its combined status as a global manufacturing hub and infrastructure hot spot. Capital-intensive ethylene and propylene complexes along the Chinese coast, in South Korea, and within the ASEAN refinery corridor provide competitive feedstock; meanwhile, domestic contractors ensure stable off-take through multi-year freeway, port, and metro projects. Vietnam's decision to retrofit ethane cracking capacity underscores the region's flexibility in sourcing, while India's rapid urban migration underpins sustained waterproofing-membrane demand. The region's 4.21% projected CAGR to 2031 outpaces global averages thanks to policy-driven industrialization, electronics clustering, and accelerating vehicle electrification, all catalysts for hydrogenated SBC uptake.

North America is buoyed by federal infrastructure-spending packages that allocate billions toward Interstate rehabilitation and airport runway resurfacing. The styrenic block copolymers market faces reduced domestic styrene supply after INEOS Styrolution permanently idled its 430,000-ton Sarnia unit, tightening merchant monomer availability and advantaging vertically integrated players. Asphalt-recycling mandates drive higher polymer concentrations in binder blends, while the region's start-up ecosystem pushes SBC-based dielectric films for EV power electronics. However, feedstock volatility tied to shale gas liquids and hurricanes along the Gulf Coast introduces uncertainty that tempers expansion plans.

Europe commands a mature yet technologically sophisticated slice of the styrenic block copolymers market, prioritizing sustainability and circularity. High energy tariffs and strict environmental regulations compel producers to operate at optimized utilizations, leading to plant rationalizations but also encouraging process efficiency gains. Regulatory drivers such as the Green Deal and extended producer-responsibility frameworks stimulate demand for recyclable and recycled-compatible polymer systems, favoring SEBS and sulfonated SBCs in food-contact and medical tubing applications.

- Asahi Kasei Corporation

- Avient Corporation

- Dynasol Group

- Eni S.p.A.

- INEOS

- Kraton Corporation

- Kuraray Co., Ltd.

- LCY

- LG Chem

- Sibur

- Sinopec

- TSRC

- ZEON Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Asphalt-Recycling Mandates in EU and U.S.

- 4.2.2 APAC Infrastructure Boom (Expressways, Waterproofing)

- 4.2.3 Pandemic-Driven Rise in Single-Use Hygiene Films

- 4.2.4 Patent Expiry of Kraton's HSBC Grades Unlocking New Entrants

- 4.2.5 Sulfonated SBCs for Next-Gen EV Capacitors

- 4.3 Market Restraints

- 4.3.1 Volatility of Crude-Linked Styrene and Butadiene Feedstocks

- 4.3.2 Asphalt-Free Cold-Mix Road Technologies

- 4.3.3 POE/POP Elastomers Replacing SBCs in Packaging

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Polymer Type

- 5.1.1 Styrene-Butadiene-Styrene (SBS)

- 5.1.2 Styrene-Isoprene-Styrene (SIS)

- 5.1.3 Hydrogenated SBCs (HSBC)

- 5.2 By Application

- 5.2.1 Asphalt Modification (Paving and Roofing)

- 5.2.2 Footwear

- 5.2.3 Polymer Modification

- 5.2.4 Adhesives and Sealants

- 5.2.5 Other Applications (Medical devices and Wires and Cables)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 Nordic Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, JV, Capacity)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 Avient Corporation

- 6.4.3 Dynasol Group

- 6.4.4 Eni S.p.A.

- 6.4.5 INEOS

- 6.4.6 Kraton Corporation

- 6.4.7 Kuraray Co., Ltd.

- 6.4.8 LCY

- 6.4.9 LG Chem

- 6.4.10 Sibur

- 6.4.11 Sinopec

- 6.4.12 TSRC

- 6.4.13 ZEON Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

苯乙烯嵌段共聚物市场规模、份额及成长分析(依产品、应用、最终用户及地区划分)-2026-2033年产业预测

苯乙烯嵌段共聚物市场规模、份额及成长分析(依产品、应用、最终用户及地区划分)-2026-2033年产业预测 2025年全球医用苯乙烯嵌段共聚物市场报告

2025年全球医用苯乙烯嵌段共聚物市场报告 苯乙烯共聚物 ABS 和 SAN 的全球市场

苯乙烯共聚物 ABS 和 SAN 的全球市场 全球苯乙烯共聚物(SBC) 市场,依类型、应用进行需求分析,预测至 2034 年

全球苯乙烯共聚物(SBC) 市场,依类型、应用进行需求分析,预测至 2034 年 医用苯乙烯嵌段共聚物市场(依产品、应用、国家及地区)-2025 年至 2032 年全球产业分析、市场规模、市场占有率及预测

医用苯乙烯嵌段共聚物市场(依产品、应用、国家及地区)-2025 年至 2032 年全球产业分析、市场规模、市场占有率及预测 苯乙烯共聚物(ABS 和 SAN) -市场占有率分析、产业趋势和成长预测(2024-2029)

苯乙烯共聚物(ABS 和 SAN) -市场占有率分析、产业趋势和成长预测(2024-2029) 苯乙烯嵌段共聚物市场按产品类型、形式、加工技术、应用、分销管道和最终用途划分 - 2025 年至 2030 年全球预测

苯乙烯嵌段共聚物市场按产品类型、形式、加工技术、应用、分销管道和最终用途划分 - 2025 年至 2030 年全球预测 SBC 及其衍生物市场按产品类型(苯乙烯-异戊二烯-苯乙烯、苯乙烯-丁二烯-苯乙烯、苯乙烯-乙烯-丁二烯-苯乙烯、SEPS 和其他 H-SBC)、应用和地区划分,2025 年至 2033 年苯乙烯嵌段共聚物(SBC)市场(全球)(2018-2034)

SBC 及其衍生物市场按产品类型(苯乙烯-异戊二烯-苯乙烯、苯乙烯-丁二烯-苯乙烯、苯乙烯-乙烯-丁二烯-苯乙烯、SEPS 和其他 H-SBC)、应用和地区划分,2025 年至 2033 年苯乙烯嵌段共聚物(SBC)市场(全球)(2018-2034) 医用苯乙烯嵌段共聚物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

医用苯乙烯嵌段共聚物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测