|

市场调查报告书

商品编码

1939655

资料即服务 (DaaS):市场占有率分析、产业趋势与统计资料、成长预测 (2026-2031)Data As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

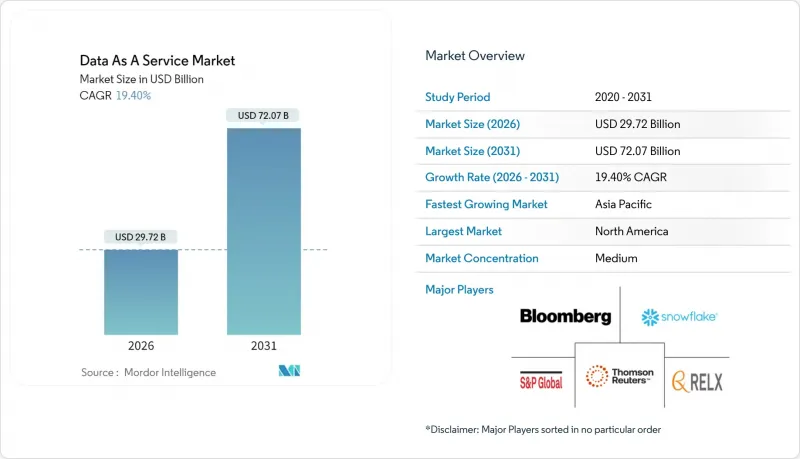

预计数据即服务 (DaaS) 市场将从 2025 年的 248.9 亿美元成长到 2026 年的 297.2 亿美元,到 2031 年将达到 720.7 亿美元,2026 年至 2031 年的复合年增长率为 19.4%。

企业正在加速投入,以实现自身资料的商业化,采用API优先的交付方式,并支援需要可刷新外部资料集的AI模型。即时分析的潜力、云端储存成本的下降以及奈米资料集市场的兴起,共同推动了潜在市场规模的扩大。经营团队报告称,这些投入带来了可衡量的成果,91%的公司表示,分析投资显着提高了效率和决策速度。产业成长仍不均衡:银行、金融和保险(BFSI)产业率先采用,而医疗保健产业则实现了最快的成长。随着企业在资料主权和成本控制之间寻求平衡,混合部署模式正在迅速普及。儘管北美仍然是最大的收入来源,但亚太地区在数据本地化法律和数位转型计画的推动下,正主导成长。

全球数据即服务 (DaaS) 市场趋势与洞察

企业向数据驱动决策转型

已实施统一资料平台的机构,其资讯搜寻速度提升了 3-5 倍,回应准确率提高了 50-70%。金融机构在强调其反诈欺计画带来的显着成效的同时,也意识到自身在高阶人工智慧应用场景方面的能力存在不足,因此加大了对强大数据基础设施的投资。随着经营团队将资料视为策略性企业资产而非单纯的 IT 产品,统一资料平台的采用速度正在加快。因此,投资正转向能够将内部记录与外部高阶资料来源即时整合的整合层。这一驱动因素支撑了各行业对可扩展、与模式无关的服务的持续需求。

非结构化资料的爆炸性成长和对即时分析的需求

非结构化内容已占企业资料的80%,但预算分配却远低于此,凸显了其尚未开发的商业潜力。针对非结构化资料工具的创业投资资金,例如一项针对人工智慧资料管道的4000万美元资金筹措,显示了投资者对专用处理平台的信心。毫秒级的即时分析正在将行销执行转变为高度个人化,从而提升转换率。已实施搜寻增强生成框架的组织报告称,人工智慧错误资讯减少了70%至90%,这进一步强化了持续数据更新的商业价值。这些趋势共同推动了数据即服务(DaaS)市场的扩张,并促进了对向量资料库和串流管道的投资。

资料隐私和网路安全问题

到2024年中期,美国将有20个州颁布全面的隐私法,而拟议的联邦立法则提案实施国家标准,这将增加合规成本。 46%的组织认为隐私是实现其资料品质目标的主要障碍。特定产业的法规增加了复杂性:医疗机构必须确保病患资料管理符合HIPAA(健康保险流通与责任法案)的要求,同时也要扩大云端采用。基于司法管辖区的资料居住要求迫使医疗机构在多个地区维护资料副本,从而增加了营运成本。在自动化和策略即程式码工具成熟之前,这些因素将阻碍云端技术的普及,尤其是在监管严格的行业。

细分市场分析

到2025年,银行、金融和保险(BFSI)产业将占总收入的28.30%,其严格的合规要求和先进的诈欺侦测工作负载将支撑资料即服务(DaaS)市场的发展。医疗保健产业将成为各产业中成长最快的产业,复合年增长率(CAGR)将达到21.8%,这主要得益于医院采用人工智慧辅助诊断和人群健康分析技术。 IT和电信公司正在整合资料集以优化网络,政府也正在扩展依赖安全资料交换的电子服务。製造业和能源产业的现有企业正在采用预测性维护模型,而这些模型需要持续的感测器资料供应。

预计到2024年,医疗机构在云端服务方面的平均支出将达到3,800万美元,对迁移结果的满意度高达72%。电子健康记录、影像库和基因组学的整合正在推动对非结构化资料管道的需求。零售商正在利用即时数据流,透过个人化推荐扩展购物车规模;教育机构正在试点融合人工智慧的学习平台。这些多样化的应用案例凸显了数据即服务(DaaS)市场的策略重要性。

到2025年,公共云端将占总收入的53.40%,这得益于其成熟的安全认证和丰富的託管服务工具包。然而,混合云和多重云端方案将以22.2%的复合年增长率呈现最强劲的成长,因为企业会优化资料放置,以降低资料传输费用并满足居住要求。在延迟和资料主权至关重要的产业,例如金融和国防,私有云端仍然是一个可行的选择。

鑑于工作负载的弹性和敏感度存在差异,90% 的企业计划在 2027 年前采用混合策略。资料架构架构和跨平台控制层正日益普及,它们能够实现流畅的资料移动,而无需依赖特定供应商。随着成本计算器能够量化资料传输成本,财务领导者正在推动相关政策,将分析表部署在更靠近 AI 运行时的位置。这些趋势扩大了标榜配置中立的数据即服务 (DaaS) 市场平台的潜在基本客群。

区域分析

北美地区将占2025年总收入的38.95%,这得益于资金雄厚的买家和强大的创投生态系统,后者正推动数据基础设施的创新。光是AWS就服务约420万全球客户,充分展现了该地区云端运算的成熟度。美国资料中心的电力消耗量将在2023年达到176太瓦时(TWh),并可能由于生成式人工智慧工作负载的激增,到2028年增至325-580太瓦时。加拿大对主权的重视推动了对符合其居住法律的国内市场节点的需求。该地区的政策组合正在促进支持安全多方分析的隐私增强技术的发展,从而推动了数据即服务(DaaS)市场的扩张。

亚太地区成长最快,年复合成长率高达24.0%,这主要得益于各国政府对数位走廊和云端区域的大力投资。印度受益于其「数位印度」计画和超大规模超大规模资料中心业者在该地区的业务扩张,而日本则已从微软和亚马逊云端服务(AWS)获得数十亿美元的投资承诺,用于建立下一代资料中心。行动服务为该地区GDP贡献了5.3%,并产生了大量的主导资料集。在资料居住规则的推动下,本地资料市场蓬勃发展,并影响全球服务供应商的部署选择。

欧洲正经历稳定成长,GDPR框架和永续性要求指导架构决策。 Global Switch等供应商承诺在2030年实现100%再生能源,使资料中心扩张与绿色能源目标保持一致。法国、德国和北欧国家凭藉其高弹性的电网和较低的PUE值(电源使用效率)吸引了大量资料中心容量。南美洲的成长主要集中在巴西,该国的财政激励措施吸引了云端服务提供者。同时,中东和非洲的资料中心部署则集中在金融科技中心。位置策略仍然是关键的采购标准,美国80%的资料中心负载集中在仅15个州,凸显了集中风险。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 市场定义与研究假设

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 企业向数据驱动决策转型

- 非结构化资料的爆炸性成长和对即时分析的需求

- 云端储存/运算成本下降

- AI RAG框架中可刷新外部资料的需求

- 数据本地化法律将有助于促进区域数据市场的发展。

- API优先的「微资料集」货币化平台

- 市场限制

- 资料隐私和网路安全问题

- 数据品质和互通性差距

- 超大规模资料中心业者不断上涨的出口费用给利润率带来压力。

- 能源密集型数据管道的ESG监测

- 价值链分析

- 关键法规结构评估

- 关键相关人员影响评估

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素的影响

第五章 市场规模与成长预测

- 按最终用户行业划分

- BFSI

- 资讯科技/通讯

- 政府和公共部门

- 零售与电子商务

- 医疗保健和生命科学

- 製造业

- 能源与公共产业

- 教育

- 其他的

- 按部署模式

- 公共云端

- 私有云端

- 混合/多重云端

- 依资料类型

- 结构化资料

- 非结构化数据

- 半结构化数据

- 最终用户公司规模

- 大公司

- 小型企业

- 透过使用

- 即时营运分析

- 客户和市场情报

- 风险与合规管理

- 供应炼和物流优化

- 诈欺检测和信用评分

- 产品和定价分析

- 其他的

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Bloomberg Finance LP

- Dow Jones and Company, Inc.

- Environmental Systems Research Institute, Inc.

- Equifax Inc.

- FactSet Research Systems Inc.

- IBM Corporation

- Oracle Corporation

- SAP SE

- Thomson Reuters Corporation

- Morningstar, Inc.

- Moody's Analytics, Inc.

- Mastercard Advisors LLC

- S&P Global Inc.

- RELX PLC(LexisNexis Risk Solutions)

- ZoomInfo Technologies Inc.

- Snowflake Inc.

- Experian PLC

- Verisk Analytics, Inc.

- CoreLogic, Inc.

- TransUnion LLC

- NielsenIQ(The Nielsen Company LLC)

- SafeGraph Inc.

- GapMaps Pty Ltd.

- Apify Technologies sro

第七章 市场机会与未来趋势

- 评估差距和未满足的需求

The Data as a Service market is expected to grow from USD 24.89 billion in 2025 to USD 29.72 billion in 2026 and is forecast to reach USD 72.07 billion by 2031 at 19.4% CAGR over 2026-2031.

Enterprises accelerate spending to monetize proprietary data, adopt API-first delivery, and support AI models that demand refreshable external datasets. Real-time analytics expectations, falling unit costs for cloud storage, and the rise of nanodataset marketplaces collectively widen the addressable opportunity. Leadership teams report measurable gains, with 91% of firms citing tangible improvements in efficiency and decision speed from analytics investments. Sector growth remains uneven: BFSI anchors early adoption, healthcare records the fastest trajectory, and hybrid deployment models surge as organizations balance data sovereignty with cost control. North America supplies the largest revenue pool, yet Asia-Pacific leads in growth as data-localization laws and digital transformation agendas converge.

Global Data As A Service Market Trends and Insights

Enterprise Shift Toward Data-Driven Decision-Making

Organizations that embed unified data platforms record information-retrieval cycles that are three to five times faster and response-accuracy improvements of 50-70% . Finance institutions highlight strong returns from anti-fraud programs yet acknowledge capability gaps in advanced AI use cases, spurring incremental spending on robust data infrastructure. Adoption accelerates as executives treat data as a strategic corporate asset rather than an IT by-product. Investment therefore shifts toward integration layers able to blend internal records with premium external feeds in real time. The driver supports sustained demand for scalable, schema-agnostic services across verticals.

Explosion of Unstructured Data and Real-Time Analytics Demand

Unstructured content already represents 80% of enterprise data while attracting disproportionately low budgets, underscoring an untapped monetization pool. Venture financing in unstructured-data tooling-exemplified by a USD 40 million round for AI-ready data pipelines-signals confidence in specialized processing platforms . Live-time analytics, measured in milliseconds, has shifted marketing execution toward hyper-personalization that raises conversion metrics. Organisations adopting retrieval-augmented generation frameworks report 70-90% reductions in AI hallucinations, reinforcing the business case for continuous data refresh. Collectively these trends widen the scope of the Data as a Service market and encourage investment in vector databases and streaming pipelines.

Data-Privacy and Cybersecurity Concerns

Twenty US states enacted comprehensive privacy statutes by mid-2024, and a proposed federal bill would introduce nationwide standards that raise compliance costs. Forty-six percent of enterprises cite privacy as their primary impediment to data-quality goals. Sector-specific rules add complexity: healthcare organisations must align patient-data controls with HIPAA while scaling cloud adoption. Jurisdiction-based residency mandates force providers to maintain multiple in-region copies, increasing operational overhead. These factors temper uptake, especially in highly regulated verticals, until automation and policy-as-code tooling mature.

Other drivers and restraints analyzed in the detailed report include:

- Falling Cloud Storage and Compute Costs

- AI RAG Frameworks' Appetite for Refreshable External Data

- Data-Quality and Interoperability Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The BFSI sector retained 28.30% of overall revenue in 2025, anchoring the Data as a Service market through stringent compliance mandates and sophisticated fraud-detection workloads. Healthcare logged a 21.8% CAGR, the fastest among industries, as hospitals embrace AI-supported diagnostics and population-health analytics. IT and telecommunications firms integrate datasets for network optimisation, while governments expand e-services that depend on secure data exchanges. Manufacturing and energy incumbents deploy predictive-maintenance models requiring continuous sensor feeds.

Healthcare organisations spent an average USD 38 million on cloud services in 2024 and reported 72% satisfaction with migration outcomes. The convergence of electronic health records, imaging repositories, and genomics drives demand for unstructured-data pipelines. Retailers leverage real-time feeds for personalised recommendations that raise basket sizes, whereas education institutions pilot AI-infused learning platforms. These varied use cases reinforce the strategic relevance of the Data as a Service market.

Public-cloud instances captured 53.40% of 2025 revenue, benefiting from mature security certifications and rich managed-service toolkits. Hybrid and multi-cloud approaches, however, post the strongest growth at 22.2% CAGR as organisations optimise data placement to mitigate egress fees and satisfy residency requirements. Private-cloud options persist where latency and sovereignty hold sway, notably in finance and defence.

Ninety percent of enterprises intend to run hybrid strategies by 2027, reflecting widespread recognition that workload characteristics vary in elasticity and sensitivity. Data-fabric architectures and cross-plane control layers thus rise in popularity, enabling fluid movement without vendor lock-in. As cost calculators quantify egress liabilities, finance chiefs lobby for placement policies that keep analytic tables close to AI runtimes. These developments enlarge the addressable base for Data as a Service market platforms that advertise deployment neutrality.

Data As A Service Market Report is Segmented by End-User Industry (BFSI, IT and Telecommunications, and More), Deployment Model (Public Cloud, Private Cloud, Hybrid/Multi-cloud), Data Type (Structured Data, Unstructured Data, Semi-Structured Data), End-User Enterprise Size (Large Enterprises, and More), Application (Real-Time Operational Analytics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.95% of 2025 revenue, sustained by well-capitalised buyers and deep venture ecosystems that refine data-infrastructure innovations. AWS alone serves an estimated 4.2 million global customers, illustrating the region's cloud maturity. United States data-centre consumption reached 176 TWh in 2023 and could rise to 325-580 TWh by 2028 as generative-AI workloads proliferate. Canada emphasises sovereignty, stimulating demand for in-country marketplace nodes that comply with residency statutes. The regional policy mix encourages privacy-enhancing technologies that underpin secure multi-party analytics and broaden the Data as a Service market.

Asia-Pacific records the fastest expansion, advancing at a 24.0% CAGR as governments channel capital toward digital corridors and cloud zones. India benefits from the Digital India programme and hyperscaler region launches, while Japan secures multi-billion-dollar commitments from Microsoft and AWS for next-generation facilities. Mobile services add 5.3% to regional GDP, creating a vast stream of localisation-driven datasets . Local data-marketplaces thrive under residency rules, shaping deployment choices for global providers.

Europe posts steady gains as the GDPR framework and sustainability mandates steer architectural decisions. Providers like Global Switch commit to 100% renewable electricity usage by 2030, aligning data-centre expansions with green-energy goals. France, Germany, and the Nordics attract capacity through resilient grids and cool climates that trim PUE ratios. South America's growth concentrates in Brazil where fiscal incentives entice cloud operators, whereas the Middle East and Africa see selective uptake clustered in fintech hubs. Location strategy remains a core purchase criterion as 80% of US data-centre load resides in just 15 states, revealing concentration risks.

- Bloomberg Finance L.P.

- Dow Jones and Company, Inc.

- Environmental Systems Research Institute, Inc.

- Equifax Inc.

- FactSet Research Systems Inc.

- IBM Corporation

- Oracle Corporation

- SAP SE

- Thomson Reuters Corporation

- Morningstar, Inc.

- Moody's Analytics, Inc.

- Mastercard Advisors LLC

- S&P Global Inc.

- RELX PLC (LexisNexis Risk Solutions)

- ZoomInfo Technologies Inc.

- Snowflake Inc.

- Experian PLC

- Verisk Analytics, Inc.

- CoreLogic, Inc.

- TransUnion LLC

- NielsenIQ (The Nielsen Company LLC)

- SafeGraph Inc.

- GapMaps Pty Ltd.

- Apify Technologies s.r.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enterprise shift toward data-driven decision-making

- 4.2.2 Explosion of unstructured data and real-time analytics demand

- 4.2.3 Falling cloud storage/compute costs

- 4.2.4 AI RAG frameworks' appetite for refreshable external data

- 4.2.5 Data-localization laws fuelling regional data marketplaces

- 4.2.6 API-first ''nano-datasets'' monetisation platforms

- 4.3 Market Restraints

- 4.3.1 Data-privacy and cybersecurity concerns

- 4.3.2 Data-quality and interoperability gaps

- 4.3.3 Rising hyperscaler egress fees compressing margins

- 4.3.4 ESG scrutiny of energy-intensive data pipelines

- 4.4 Value Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By End-User Industry

- 5.1.1 BFSI

- 5.1.2 IT and Telecommunications

- 5.1.3 Government and Public Sector

- 5.1.4 Retail and E-commerce

- 5.1.5 Healthcare and Life Sciences

- 5.1.6 Manufacturing

- 5.1.7 Energy and Utilities

- 5.1.8 Education

- 5.1.9 Others

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid / Multi-cloud

- 5.3 By Data Type

- 5.3.1 Structured Data

- 5.3.2 Unstructured Data

- 5.3.3 Semi-structured Data

- 5.4 By End-user Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Application

- 5.5.1 Real-time Operational Analytics

- 5.5.2 Customer and Marketing Intelligence

- 5.5.3 Risk and Compliance Management

- 5.5.4 Supply-Chain and Logistics Optimisation

- 5.5.5 Fraud Detection and Credit Scoring

- 5.5.6 Product and Pricing Analytics

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bloomberg Finance L.P.

- 6.4.2 Dow Jones and Company, Inc.

- 6.4.3 Environmental Systems Research Institute, Inc.

- 6.4.4 Equifax Inc.

- 6.4.5 FactSet Research Systems Inc.

- 6.4.6 IBM Corporation

- 6.4.7 Oracle Corporation

- 6.4.8 SAP SE

- 6.4.9 Thomson Reuters Corporation

- 6.4.10 Morningstar, Inc.

- 6.4.11 Moody's Analytics, Inc.

- 6.4.12 Mastercard Advisors LLC

- 6.4.13 S&P Global Inc.

- 6.4.14 RELX PLC (LexisNexis Risk Solutions)

- 6.4.15 ZoomInfo Technologies Inc.

- 6.4.16 Snowflake Inc.

- 6.4.17 Experian PLC

- 6.4.18 Verisk Analytics, Inc.

- 6.4.19 CoreLogic, Inc.

- 6.4.20 TransUnion LLC

- 6.4.21 NielsenIQ (The Nielsen Company LLC)

- 6.4.22 SafeGraph Inc.

- 6.4.23 GapMaps Pty Ltd.

- 6.4.24 Apify Technologies s.r.o.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment