|

市场调查报告书

商品编码

1939656

磨料:市场占有率分析、产业趋势与统计资料、成长预测(2026-2031 年)Abrasives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

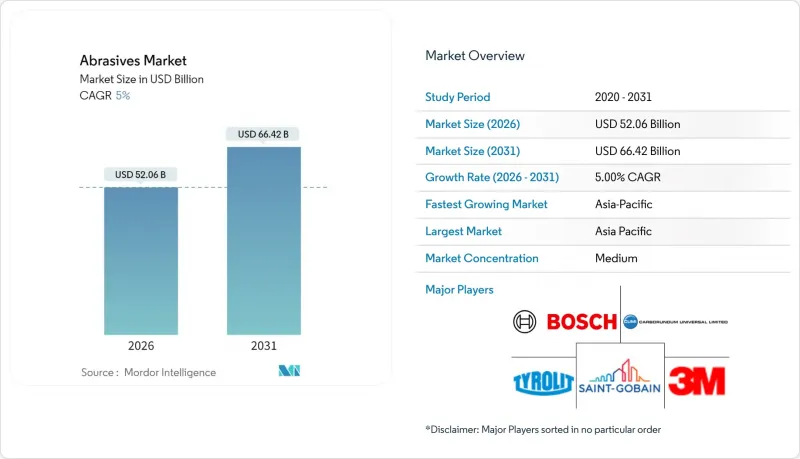

预计磨料市场将从 2025 年的 495.8 亿美元成长到 2026 年的 520.6 亿美元,到 2031 年将达到 664.2 亿美元,2026 年至 2031 年的复合年增长率为 5.0%。

销售动能反映出市场对高性能材料的需求不断增长,这些材料能够在先进的数控设备上保持严格的公差,尤其是在电动车 (EV) 和航太零件的加工领域。合成材料因其可靠的硬度和热稳定性而持续赢得订单,而结合剂材料则被定位为高温研磨的主力军。亚洲的快速工业化、向精密电子领域的转型以及增材製造(3D 列印)后后处理需求的成长,都为磨料市场的成长奠定了坚实的基础。竞争日趋激烈,随着监管机构收紧颗粒物和挥发性有机化合物 (VOC) 的标准,主要製造商正在围绕环保化学技术优化产品系列。同时,一些利基企业正在钻石基超磨粒等特殊领域中获得市场份额。

全球磨料市场趋势与洞察

航太和汽车产业的需求不断增长

对先进航空合金和轻量化电动车传动系统日益增长的需求促使製造商指定使用立方氮化硼 (CBN) 和钻石砂轮,这些砂轮即使在高速运转下也能保持形状。一级供应商正在使用玻璃态 CBN 和陶瓷研磨颗粒优化其加工生产线,以缩短加工週期并延长修整间隔,从而加工电驱动桥、转子轴和电池外壳。诺顿磨料公司报告称,钻石刀具与自动化负载感测系统相结合,可显着降低废料率,这解释了为什么原始设备製造商 (OEM) 正在标准化使用高品质等级的磨料,并注重加工的重复性。随着组装上机器人技术的普及,对錶面光洁度的要求越来越高,而这无法透过手工研磨来实现,因此磨料市场持续成长。

不断发展的金属製造和加工产业

钢铁服务中心、压力容器加工厂和合约製造商已将研磨工位升级为陶瓷研磨颗粒,在降低电力消耗的同时,提高了高达 40% 的去除率。减少因更换砂带而造成的停机时间,提高了整体设备效率 (OEE),而 OEE 在精益生产实践中变得越来越重要。诸如 VSM TOP SIZE 之类的特种面涂层可减少不銹钢工件的热变色,并允许在不产生热变形的情况下承受更高的进给压力。这些生产效率的提升有助于更快地完成订单,因此,优质陶瓷砂带在对成本敏感的大量生产环境中至关重要。

高昂的生产和设备成本

合成钻石和立方氮化硼晶体的生长需要在远超地质条件的压力和温度下进行,这使得反应釜的资本密集度远高于传统的熔融氧化铝生产线。用于钻石砂轮的单头数控研磨需要精密主轴和封闭回路型冷却系统,推高了安装成本。虽然这些工具使用寿命长、单件成本低,但在对价格敏感的经济体中,中小型加工厂仍倾向于延后更换。供应商正在尝试租赁模式和耗材信贷计划,但资金筹措了这些方案的普及。

细分市场分析

截至2025年,合成研磨颗粒占磨料市场66.35%的份额,证实了使用者对均匀晶体形态的偏好,因为均匀晶体形态能够带来可预测的生产过程中的磨损模式。氧化铝仍是主流研磨颗粒,而碳化硅则较适用于非铁金属加工,立方氮化硼(CBN)则较适用于硬化钢加工。住友电工正在研发的新型奈米多多晶钻石有望具有卓越的断裂韧性,并为磨料市场解决镍基高温合金的低砂轮损耗率铺平了道路。天然石榴石因其可回收利用的块状介质和低游离二氧化硅含量,在水射流和喷砂作业中保持着稳固的地位,这提高了现场安全性,使其成为基础设施维修计划的理想选择。

向合成产品的转变与自动化供应系统相契合,后者要求严格控製粒度分布,而此参数更容易透过工程化製造流程实现。随着亚洲熔融氧化铝产能的扩张,供应稳定性提高,但电价波动仍可能影响生产成本。为获得环保认证,製造商正投资可再生能源驱动的电弧炉和封闭回路型水冷系统,以维持在受监管地区的市场份额。因此,即使在大规模生产领域,磨料市场也不断提高品质标准。

黏结砂轮占2025年销售额的47.55%,反映了它们在汽车、航太和通用机械加工车间的切割、研磨和表面处理作业中的重要作用。树脂基和玻璃基体在深切削过程中提供热稳定性,从而确保曲轴和涡轮叶片等对冶金完整性要求极高的零件的加工精度。溶胶-凝胶法製备的氧化铝和工程化孔隙结构的进步提高了排屑排放,从而在不产生烧伤风险的情况下实现更高的金属去除率。

涂层磨料虽然吨位较低,但广泛应用于精加工和去毛边。从柔性薄膜到纤维盘,各种基材可优化其在曲面和难以触及区域的加工性能。儘管超磨粒目前仍占据小众市场,但其两位数的成长预示着磨料市场未来的发展方向。积层製造车间正在指定使用钻石磨盘和立方氮化硼(CBN)芯轴来加工薄壁钛零件,因为传统砂轮容易堵塞这些零件。像伊梅里斯这样的供应商提供客製化的熔融氧化铝和溶胶-凝胶颗粒,这些颗粒可以扩大修整器间距,从而增强黏结砂轮的优势,同时缩小与超磨粒的性能差距。

磨料市场报告按材料(天然磨料和合成磨料)、类型(粘结磨料、涂附磨料、超磨粒)、磨粒/原材料(氧化铝、碳化硅等)、最终用户行业(金属製造和加工、汽车和航太等)以及地区(亚太地区、北美、欧洲、南美、中东和非洲)进行细分。

区域分析

到2025年,亚太地区将占全球采购量的55.40%,反映了中国庞大的机械加工基地和印度快速发展的基础设施。政府对国内电动车电池製造和电子产品组装的激励措施进一步刺激了本地需求。日本和韩国正利用先进的钻石半导体研究成果,为超磨粒开发新的下游应用,例如切割大面积钻石晶片。这些因素共同帮助亚洲保持主导地位,并鼓励跨国公司将混合和压制工艺在地化。

在北美,航太、医疗和增材製造业持续保持强劲成长。日益严格的挥发性有机化合物 (VOC) 和颗粒物排放法规正推动喷砂介质向石榴石喷砂介质和水基冷却剂的转变,从而促进产品组合的日益复杂化。

在欧洲,永续性和循环经济原则日益受到重视,例如圣戈班等供应商正在引入可回收黏合剂系统以降低碳排放强度。德国精密机械丛集正在加速超磨粒的应用,而南欧则专注于建筑相关的喷砂和切割片的消耗。儘管规模仍然较小,但南美和中东及非洲地区由于工业化进程的加速,正呈现稳健成长。巴西的造船厂和沿岸地区的石化计划都反映了终端用户日益多元化的趋势。本地加工伙伴关係正在帮助全球品牌拓展这些地区市场,从而增强磨料市场的全球覆盖率。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 在航太和汽车产业中不断扩大的应用

- 不断扩大的金属製造和加工产业

- 新兴经济体製造业活动不断扩大

- 后处理需要超磨粒

- 精密机械和CNC工具机的应用日益普及

- 市场限制

- 高昂的生产和设备成本

- 对研磨剂的使用有严格的规定

- 以替代材料或方法进行替代

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 材料

- 天然磨料

- 合成磨料

- 按类型

- 磨料

- 砂纸

- 超磨粒

- 磨料/原料

- 氧化铝

- 碳化硅

- 陶瓷和氧化锆氧化铝

- 其他(包括石榴石)

- 按最终用户行业划分

- 金属製造与加工

- 汽车和航太

- 电子和半导体

- 建筑和基础设施

- 医疗设备

- 石油和天然气

- 其他(工业和农业机械)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- 3M

- Abrasive Technology

- ARC Abrasives Inc.

- Asahi Diamond Industrial Co. Ltd.

- CUMI

- Deerfos

- Fujimi Incorporated

- Imerys

- Mirka Ltd.

- NORITAKE CO., LIMITED

- Robert Bosch GmbH

- Saint-Gobain

- SAK ABRASIVES LIMITED

- Sia Abrasives Industries AG

- Tyrolit-Schleifmittelwerke Swarovski AG & Co KG

第七章 市场机会与未来展望

The Abrasives Market is expected to grow from USD 49.58 billion in 2025 to USD 52.06 billion in 2026 and is forecast to reach USD 66.42 billion by 2031 at 5.0% CAGR over 2026-2031.

Sales momentum reflects rising demand for high-performance materials that can hold tight tolerances on advanced CNC equipment, especially in electric vehicle (EV) and aerospace component machining. Synthetic grades continue to capture orders because they deliver reliable hardness and thermal stability, while bonded formats remain the workhorse for high-temperature grinding. Rapid industrialization in Asia, the pivot toward precision electronics, and the emergence of post-processing needs for additive manufacturing all reinforce the growth runway for the abrasives market. Competitive rivalry is intensifying: large incumbents are refining product portfolios around eco-friendly chemistries as regulators tighten particulate and volatile-organic-compound (VOC) standards, and niche producers are carving share in specialty niches such as diamond-based super-abrasives.

Global Abrasives Market Trends and Insights

Increasing use in aerospace and automotive industries

Demand for advanced aircraft alloys and lightweight EV drivetrains is pushing producers to specify cubic boron nitride (CBN) and diamond wheels that maintain form at high speeds. Tier-one suppliers are optimizing E-Axle, rotor shaft, and battery-housing machining lines with vitrified CBN and ceramic media that cut cycle time and extend dresser intervals. Norton Abrasives reports measurable reductions in scrap rates when diamond tools are paired with automated load-sensing systems, illustrating why OEMs are standardizing on premium grades for repeatability. As robotics proliferate on assembly lines, the abrasives market gains from consistent surface-finish requirements that manual grinding cannot meet.

Growing metal manufacturing and fabrication industries

Steel service centers, pressure-vessel shops, and contract fabricators have upgraded grinding stations with ceramic-grain belts that increase stock removal by up to 40% while lowering power draw. Lower downtime for belt changes translates into higher overall equipment effectiveness (OEE), a metric increasingly monitored under lean programs. Specialized top-coats such as VSM TOP SIZE mitigate heat discoloration on stainless workpieces, enabling higher feed pressures without thermal distortion. These productivity gains support rapid order throughput, making high-end ceramic grades essential in cost-sensitive mass-production settings.

High production and equipment cost

Synthetic diamond and CBN crystals are grown under pressures and temperatures that exceed geological conditions, pushing capital intensity for reactor vessels well above conventional fused-alumina lines. Single-head CNC grinders configured for diamond wheels require precision spindles and closed-loop coolant systems, raising acquisition costs. While these tools deliver longer life and lower per-part expense, small and midsize job shops in price-sensitive economies still defer upgrades. Vendors are experimenting with leasing models and consumable-credit programs, but adoption remains gated by financing constraints.

Other drivers and restraints analyzed in the detailed report include:

- Growing manufacturing activities in emerging economies

- Additive-manufacturing post-processing requiring super-abrasives

- Stringent regulations on usage of abrasives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic grades commanded 66.35% share of the abrasives market in 2025, underlining user preference for consistent crystal morphology that translates into predictable wear patterns during production runs. Aluminum oxide remains the volume leader; however, silicon carbide addresses non-ferrous machining, while CBN is preferred for hardened steels. Novel nano-polycrystalline diamonds under development by Sumitomo Electric promise superior fracture toughness, positioning the abrasives market to tackle nickel-based super-alloys at lower wheel wear rates. Natural garnet retains a foothold in waterjet and blasting tasks where recyclable bulk media and low free-silica content improve site safety, making it attractive for infrastructure refurbishment projects.

The shift toward synthetic offerings aligns with automated feed systems that demand tight grit distributions, a parameter easier to achieve through engineered production routes. With Asia ramping fused-alumina capacity, supply security is improving, although power-tariff volatility can swing output costs. Manufacturers pursuing eco-labels are investing in renewable-powered arc furnaces and closed-loop water quench circuits to retain share in regulated regions. As a result, the abrasives market continues to upgrade quality benchmarks even in high-volume segments.

Bonded wheels generated 47.55% of 2025 revenue, reflecting their role in cutting, sharpening, and surface-conditioning jobs across automotive, aerospace, and general engineering workshops. Resinoid and vitrified matrices provide thermal stability during deep-cut operations, enabling consistent tolerances on crankshafts and turbine blades where metallurgical integrity is critical. Advances in sol-gel alumina and engineered pore structures improve chip evacuation, permitting higher metal removal rates without risk of burn.

Coated abrasives, while lighter in tonnage, enjoy widespread use in finishing and deburring. Backings ranging from flexible film to fiber discs optimize performance across curved surfaces and hard-to-reach areas. Super-abrasives hold a niche position today, but their double-digit growth underpins the future direction of the abrasives market. Additive manufacturing shops specify diamond pads and CBN mandrels for thin-wall titanium parts where conventional wheels load quickly. Suppliers such as Imerys offer tailor-made fused alumina and sol-gel grains that extend dresser intervals, reinforcing bonded wheels' dominance while bridging performance gaps with super-abrasives.

The Abrasives Market Report is Segmented by Material (Natural Abrasives and Synthetic Abrasives), Type (Bonded Abrasives, Coated Abrasives, and Super Abrasives), Abrasives Grain/Raw Material (Aluminum Oxide, Silicon Carbide, and More), End-User Industry (Metal Manufacturing and Fabrication, Automotive and Aerospace, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific accounted for 55.40% of global purchases in 2025, reflecting China's large machining base and India's accelerated infrastructure build-out. Government incentives for domestic EV battery manufacturing and electronics assembly further stimulate local demand. Japan and South Korea leverage advanced diamond semiconductor research to create new downstream uses for super-abrasives, such as slicing large-area diamond wafers. These factors collectively sustain Asia's leadership position and encourage multinationals to localize mixing and pressing operations.

North America retains strong momentum in aerospace, medical, and additive-manufacturing segments. Regulatory scrutiny on VOCs and particulate emissions propels shifts toward garnet blasting media and water-based coolants, generating product-mix upgrades.

Europe emphasizes sustainability and circular-economy principles, with suppliers like Saint-Gobain implementing recycled-bond systems to curtail carbon intensity. Adoption of super-abrasives is accelerating in Germany's precision engineering clusters, while southern Europe focuses on construction-related blasting and cutting disc consumption. South America, the Middle East, and Africa remain smaller in volume yet register healthy growth as industrialization deepens; Brazil's shipbuilding yards and Gulf petrochemical projects illustrate expanding end-user diversity. Local converting partnerships help global brands penetrate these regions, strengthening global coverage of the abrasives market.

- 3M

- Abrasive Technology

- ARC Abrasives Inc.

- Asahi Diamond Industrial Co. Ltd.

- CUMI

- Deerfos

- Fujimi Incorporated

- Imerys

- Mirka Ltd.

- NORITAKE CO., LIMITED

- Robert Bosch GmbH

- Saint-Gobain

- SAK ABRASIVES LIMITED

- Sia Abrasives Industries AG

- Tyrolit - Schleifmittelwerke Swarovski AG & Co KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Use in the Aerospace and Automotive Industries

- 4.2.2 Growing Metal Manufacturing and Fabrication Industries

- 4.2.3 Growing Manufacturing Activities in Emerging Economies

- 4.2.4 Additive-Manufacturing Post-processing Requiring Super-abrasives

- 4.2.5 Increased Adoption of Precision and CNC Machinery

- 4.3 Market Restraints

- 4.3.1 High production and Equipment Cost

- 4.3.2 Stringent Regulations on Usage of Abrasives

- 4.3.3 Substitution by Alternative Materials or Methods

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Natural Abrasives

- 5.1.2 Synthetic Abrasives

- 5.2 By Type

- 5.2.1 Bonded Abrasives

- 5.2.2 Coated Abrasives

- 5.2.3 Super Abrasives

- 5.3 By Abrasive Grain/Raw Material

- 5.3.1 Aluminum Oxide

- 5.3.2 Silicon Carbide

- 5.3.3 Ceramic and Zirconia Alumina

- 5.3.4 Others (Including Garnet)

- 5.4 By End-user Industry

- 5.4.1 Metal Manufacturing and Fabrication

- 5.4.2 Automotive and Aerospace

- 5.4.3 Electronics and Semiconductors

- 5.4.4 Construction and Infrastructure

- 5.4.5 Medical Devices

- 5.4.6 Oil and Gas

- 5.4.7 Others (Industrial Machinery and Agriculture Equipment)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Malaysia

- 5.5.1.6 Thailand

- 5.5.1.7 Indonesia

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordic Countries

- 5.5.3.7 Turkey

- 5.5.3.8 Russia

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Qatar

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 South Africa

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Abrasive Technology

- 6.4.3 ARC Abrasives Inc.

- 6.4.4 Asahi Diamond Industrial Co. Ltd.

- 6.4.5 CUMI

- 6.4.6 Deerfos

- 6.4.7 Fujimi Incorporated

- 6.4.8 Imerys

- 6.4.9 Mirka Ltd.

- 6.4.10 NORITAKE CO., LIMITED

- 6.4.11 Robert Bosch GmbH

- 6.4.12 Saint-Gobain

- 6.4.13 SAK ABRASIVES LIMITED

- 6.4.14 Sia Abrasives Industries AG

- 6.4.15 Tyrolit - Schleifmittelwerke Swarovski AG & Co KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growing Use of Automation and Robotics

液体砂纸市场:按类型、配方、粒度、销售管道、终端用户产业和应用划分-2026-2032年全球市场预测

液体砂纸市场:按类型、配方、粒度、销售管道、终端用户产业和应用划分-2026-2032年全球市场预测 抛光剂,超磨粒·抛光产品的全球市场:终端用户,用途,竞争企业:分析与预测切割线市场:按设备类型、连接方式、应用和最终用户划分-2026-2032年全球市场预测

抛光剂,超磨粒·抛光产品的全球市场:终端用户,用途,竞争企业:分析与预测切割线市场:按设备类型、连接方式、应用和最终用户划分-2026-2032年全球市场预测 全球磨料辊市场规模、份额、趋势和成长分析报告(2026-2034年)

全球磨料辊市场规模、份额、趋势和成长分析报告(2026-2034年) 全球磨料市场:市场规模、份额和趋势分析(按产品、应用和地区划分),细分市场预测(2026-2033 年)全球钻石混凝土磨料工具市场(按产品类型、分销管道、最终用户、黏结剂类型、粒度及应用划分)预测(2026-2032年)混凝土抛光工具市场:按类型、动力来源、磨料、分销管道、应用和最终用户划分,全球预测,2026-2032年钻石磨料工具市场按类型、应用、结合剂类型、形状、最终用途和粒度划分,全球预测,2026-2032年

全球磨料市场:市场规模、份额和趋势分析(按产品、应用和地区划分),细分市场预测(2026-2033 年)全球钻石混凝土磨料工具市场(按产品类型、分销管道、最终用户、黏结剂类型、粒度及应用划分)预测(2026-2032年)混凝土抛光工具市场:按类型、动力来源、磨料、分销管道、应用和最终用户划分,全球预测,2026-2032年钻石磨料工具市场按类型、应用、结合剂类型、形状、最终用途和粒度划分,全球预测,2026-2032年 磨料市场分析及预测(至2035年):依类型、产品类型、应用、材质、技术、製程、最终用户、形状及功能划分

磨料市场分析及预测(至2035年):依类型、产品类型、应用、材质、技术、製程、最终用户、形状及功能划分 2026年全球磨料市场报告

2026年全球磨料市场报告