|

市场调查报告书

商品编码

1939658

复合材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Composite Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

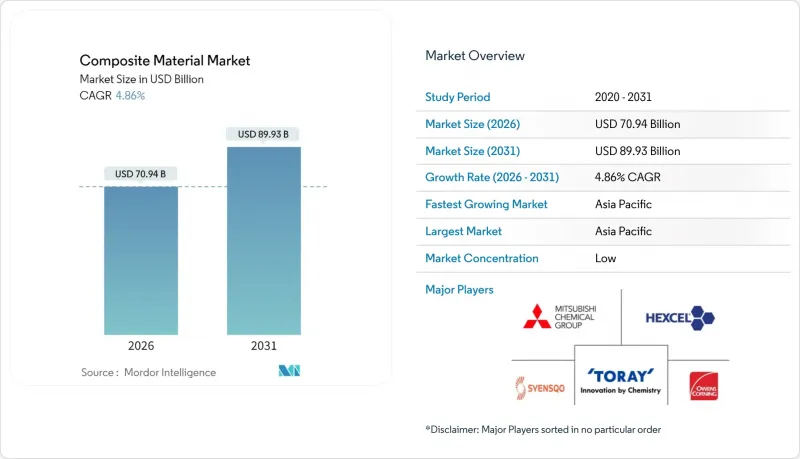

预计复合材料市场将从 2025 年的 676.5 亿美元成长到 2026 年的 709.4 亿美元,到 2031 年将达到 899.3 亿美元,2026 年至 2031 年的复合年增长率为 4.86%。

交通运输、能源、基础设施和电子产业对轻质高性能材料的强劲需求正在拓展其应用范围,而持续的製程自动化则正在缩短生产週期并减少缺陷。亚太地区预计在2024年将占全球收入的45.12%,并将继续保持销售成长的中心地位,因为风力发电机的扩张、电气化项目和大型基础设施计划将推动区域消费。陶瓷基体技术的快速发展、聚合物基体材料对金属的持续替代以及特种增强材料的供应基础不断完善,都增强了新进入者的竞争障碍。然而,回收的限制仍然存在不确定性,而无法跟上安装速度的报废处理方案可能会阻碍其应用。

全球复合材料市场趋势与洞察

电动化驱动的电动交通领域对碳纤维的需求

电动车大约使用450磅塑胶和聚合物复合材料,比内燃机平台增加了18%,因为车辆重量每减轻10%,续航里程通常就能提高6-8%。电池机壳是关键应用领域,碳纤维增强聚合物比铝製外壳轻30%,且不牺牲热稳定性。玻璃纤维增强热塑性塑胶模塑车身面板具有成本优势,可实现轻量化,而内装中的天然纤维层压板则提升了永续性。汽车製造商正在向碳纤维、玻璃纤维和生物增强材料相结合的复合材料结构转型,以优化刚度、碰撞安全性能和生命週期排放。在供应链方面,北美、欧洲和东亚正在扩大丝束产能和认证预浸料生产线,以避免在2026-2028年新车上市期间出现供应瓶颈。

在风力发电机叶片製造的应用日益广泛

预计2024年全球风电装置容量将成长17%,2025年将成长35%,到2035年累积装置容量将达到450吉瓦。目前,新一代离岸风力发电涡轮机的功率已超过15兆瓦,需要长度超过110公尺的叶片,而这只能透过客製化复合材料铺层来实现。到2020年代末,预计每年用于叶片製造的玻璃纤维和碳纤维增强材料将超过100万吨,这将对玻璃纤维熔炼能力和高模量碳纤维的供应造成越来越大的压力。虽然玻璃纤维增强塑料在单位成本方面仍然占据主导地位,但选择性碳纤维帽盖正被越来越多地采用,以减少叶尖挠度和叶根质量。欧洲正在试用可焊接根部接头的热塑性树脂叶片,这有望开闢一条避免在水泥窑中进行共处理的回收途径。业界正在持续实施叶片循环使用法规,这使得材料可追溯性和树脂配方改良成为原始设备製造商(OEM)和製造商的当务之急。

复合材料高成本

碳纤维复合材料的单价通常是钢材的5到10倍,这限制了其在对成本敏感的应用交付的广泛应用。航太级预浸料需要高压釜固化、严格的环境控制和大量的无损检测,所有这些都推高了单位成本。汽车工程也面临类似的障碍,儘管碳纤维具有优异的重量效益比,但其应用主要限于豪华品牌。规模仍然是一个重要的障碍,因为纤维纺丝生产线和前体工厂都需要大量资金投入。诸如美国国家可再生能源实验室的热成型製程等创新技术可望将可回收碳纤维片材的成本降低90%到95%,但商业化需要多年的认证工作。许多潜在的采用者可能会推迟大规模替换,直到原材料价格下降或设计工程师发现系统层面能够大幅降低成本。

细分市场分析

聚合物基复合复合材料(PMC)预计将占2025年市场收入的55.62%,这进一步巩固了复合材料市场在性能和可製造性之间取得最佳平衡的地位。儘管热固性环氧树脂在航太、船舶和风力涡轮机叶片领域仍占据主导地位,但可再生热塑性塑胶在汽车和消费品领域的市场份额正在稳步增长。目前,商用热塑性单向带材的宽度已超过1米,因此能够实现电池托盘和座椅结构的高通量压模成型。同时,受航太推进系统和聚光型太阳热能发电接收复合材料需求成长的推动,陶瓷基质复合材料(CMC)预计将在2026年至2031年间以8.12%的复合年增长率成长。

陶瓷基复合材料(CMCs)可承受超过1600°C的高温,取代镍基高温合金,显着降低冷却需求,进而达到无与伦比的热效率。虽然初始投资较高,但一旦生产稳定,其生命週期内减重、降低油耗和减少维护成本的价值将超过初始成本。金属基复合复合材料(MMCs)目前占据的市场份额小规模,但由于其优异的导热性和耐磨性,在电子基板和刹车盘等应用领域持续成长。积层製造和五轴数控加工技术的进步,使得设计更加自由,预示其市场渗透率将在2020年代后半期逐步提高。

区域分析

亚太地区将成为复合材料市场的支柱,预计到2025年将占全球收入的44.85%,并预计在2031年之前以7.45%的年均复合成长率成长。这主要得益于中国离岸风力发电的扩张、印度地铁网路的扩建以及东南亚电网基础设施的更新换代。此外,碳纤维产能的提升也促进了亚太地区复合材料市场规模的成长。韩国晓星集团(Hyosung Corporation)正将其年产量提高至9,000吨,以满足航太和氢气罐的需求。日本的价值链则专注于高精度丝束铺展和预浸料技术,服务国内飞机框架专案和出口客户。

北美紧随其后,这得益于航太领域的持续交付、联邦政府对可再生能源的投资以及休閒海洋领域的復苏。美国能源局拨款2000万美元用于促进风力发电机复合材料的回收利用,显示政策正朝着循环经济的方向发展。加拿大各省正在支持先进材料丛集,将学术研发与射出成型试生产线结合,并致力于维护生物基热塑性塑胶的国家智慧财产权。

欧洲先进的设计能力和严格的环境法规正在推动生物基树脂和闭合迴路製程的快速普及。儘管受供应链中断和能源成本飙升的影响,欧洲生物基树脂产量在2024年底有所下降,但该地区仍占全球产量的21.74%。维斯塔斯(Vestas)的闭环叶片和低排放塔等倡议表明,欧盟的气候政策正引导原始设备製造商(OEM)将全面永续性作为优先事项。东欧国家正利用其熟练的劳动力资源和接近性西方市场的地理优势,吸引对拉挤成型和缠绕成型工厂的投资。

儘管规模较小,但南美洲和中东及非洲地区也呈现出显着的成长势头,因为复合材料解决方案被广泛应用于基础设施现代化和海水淡化计划中。值得关注的需求来源包括巴西风能走廊、沙乌地阿拉伯的海水淡化输在线连续以及南非的电动公车车身。跨国公司的技术转让,加上当地增强材料(剑麻、黄麻)的供应,正在推动本土创新,并逐步缩小与进口零件的成本差距。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电动化驱动的电动交通领域对碳纤维的需求

- 在风力发电机製造中应用日益广泛

- 热塑性复合材料在大规模生产车的应用日益广泛

- 材料科学的技术进步

- 航太和国防工业中复合材料的日益广泛应用

- 市场限制

- 复合材料高成本

- 这些材料回收利用面临的挑战

- 自动化层压工艺中技术纯熟劳工短缺

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过基体材料

- 高分子复合材料(PMC)

- 热固性树脂

- 热塑性树脂

- 陶瓷/碳基复合材料(CMCs)

- 其他基体(金属基复合材料)

- 高分子复合材料(PMC)

- 透过增强纤维

- 玻璃纤维

- 碳纤维

- 酰胺纤维

- 其他纤维(天然/生物纤维)

- 按最终用途行业划分

- 汽车和运输设备

- 风力发电

- 航太/国防

- 管道和储罐

- 建造

- 电气和电子设备

- 运动与休閒

- 其他终端用户产业(医疗、海事等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 马来西亚

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 土耳其

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3M

- Arkema

- BASF

- CPIC BRASIL Fibras de Vidro Ltda

- DuPont

- Exel Composites

- Gurit Services AG

- Hexcel Corporation

- HS HYOSUNG ADVANCED MATERIALS

- Lanxess

- Mitsubishi Chemical Group Corporation.

- Nippon Graphite Fiber Co., Ltd.

- Owens Corning

- SGL Carbon

- Syensqo

- Teijin Limited

- Toray Industries Inc.

第七章 市场机会与未来展望

The Composite Material market is expected to grow from USD 67.65 billion in 2025 to USD 70.94 billion in 2026 and is forecast to reach USD 89.93 billion by 2031 at 4.86% CAGR over 2026-2031.

Robust demand for lightweight, high-performance materials in transportation, energy, infrastructure and electronics is widening the application portfolio, while continuous process automation is lowering cycle times and defects. Asia-Pacific, holding 45.12% of global revenue in 2024, remains the epicenter of volume growth as wind-turbine expansion, electrification programs and large-scale infrastructure projects accelerate regional consumption. Rapid progress in ceramic matrix technologies, steady substitution of metals by polymer matrix grades and an improving supply base for specialty reinforcements are strengthening competitive barriers for late entrants. Recycling limitations, however, continue to cloud long-term circularity targets and could restrain adoption if end-of-life solutions do not keep pace with installation rates.

Global Composite Material Market Trends and Insights

Electrification-Driven Carbon-Fiber Demand in E-Mobility

Electric vehicles integrate roughly 450 lb of plastics and polymer composites-an 18% rise compared with internal-combustion platforms-because every 10% curb in curb weight typically stretches driving range by 6-8%. Battery enclosures have become a flagship application, where carbon-fiber reinforced polymers deliver a 30% mass cut versus aluminum without sacrificing thermal stability. Body panels molded from glass-fiber reinforced thermoplastics enable cost-competitive lightweighting, while natural-fiber laminates in interior trim broaden sustainability credentials. Automakers are converging on multi-material architectures that blend carbon, glass and bio reinforcements to optimise stiffness, crashworthiness and lifecycle emissions. Supply chains are responding by expanding tow capacity and qualified prepreg lines across North America, Europe and East Asia to avert bottlenecks during the 2026-2028 model-launch window.

Increasing Usage in the Manufacturing of Wind Turbine Blades

Global wind installations climbed 17% in 2024 and 35% in 2025, pushing cumulative capacity toward the 450 GW mark envisaged for 2035. Next-generation offshore machines now exceed 15 MW, requiring blades longer than 110 m that can only be realised with tailored composite lay-ups. More than 1 million t of glass and carbon reinforcements will be consumed annually for blade manufacture by the end of the decade, intensifying pressure on glass-fiber melt capacity and high-modulus carbon supply. While glass-fiber reinforced plastics continue to dominate on a cost-per-meter basis, selective carbon spar caps are proliferating to curb tip deflection and blade-root mass. Europe is piloting thermoplastic blades for weldable root joints, potentially enabling recycling routes that avoid co-processing in cement kilns. The sector's emerging blade-circularity regulations make material traceability and resin reformulation urgent priorities for OEMs and fabricators.

High Cost of Composite Materials

Carbon-fiber composites typically price at five-to-ten times steel on a delivered-part basis, deterring penetration into cost-sensitive segments. Aerospace-grade prepregs entail autoclave curing, tight environmental controls and extensive non-destructive testing, each inflating unit expense. Automotive programs confront similar hurdles, confining carbon-fiber usage largely to premium marques despite favorable weight-benefit ratios. Production scale remains a pivotal barrier, since fiber-spinning lines and precursor plants run capital-intensive. Breakthroughs such as National Renewable Energy Laboratory's thermoforming route promise 90-95% cost savings for recyclable carbon sheets, yet commercial deployment will require multi-year qualification campaigns. Until raw-material prices drop or design engineers capture superior system-level savings, many potential adopters may defer high-volume substitution.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Thermoplastic Composites in Mass-Production Automotive

- Increasing Use of Composites in the Aerospace and Defense Industry

- Challenges in Recycling Composite Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer matrix composites (PMCs) delivered 55.62% of 2025 revenue, reinforcing the composites market as the preferred option for balanced performance and manufacturability. Thermoset epoxies remain mainstream in aerospace, marine and wind blades, yet recyclable thermoplastics are steadily eroding share in automotive and consumer goods. Commercial thermoplastic UD-tape lines now exceed 1 m wide, favouring high-throughput press forming for battery trays and seat structures. In parallel, the composites market size attributable to ceramic matrix composites is projected to post an 8.12% CAGR between 2026 and 2031, propelled by aerospace propulsion and concentrated solar-power receivers.

CMCs withstand more than 1 600 °C, replacing nickel super-alloys and slashing cooling demands, thereby unlocking unrivalled thermal efficiencies. Investment outlays are significant, but once quiver production stabilises, their life-cycle value proposition offsets initial premiums through weight savings, fuel burn reductions and lower maintenance. Metal matrix composites occupy a smaller niche that thrives on extraordinary thermal conductivity and wear resistance for electronic substrate carriers and brake rotors. Additive-manufacturing pathways and five-axis CNC finishing are broadening design envelopes, hinting at incremental penetration in the latter half of the decade.

The Composites Market Report Segments the Industry by Matrix Material (Polymer Matrix Composites (PMC), Ceramic/Carbon Matrix Composites (CMCs), Other Matrices), Reinforcement Fiber (Glass Fiber, Carbon Fiber, and More), End-Use Industry (Automotive and Transportation, Wind Energy, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchors the composites market with 44.85% revenue in 2025 and is projected to grow at 7.45% through 2031 as China escalates offshore wind installations, India expands metro rail networks and Southeast Asia upgrades grid infrastructure. The regional composites market size also benefits from escalating carbon-fiber capacity; South Korea's Hyosung is lifting annual output to 9 000 t to meet aerospace and hydrogen-tank demand. Japan's value chain focuses on high-precision tow spreading and prepreg technologies, serving both domestic air-frame programs and export customers.

North America trails closely, propelled by sustained aerospace deliveries, federal investments in renewable energy and a resurgent recreational-marine segment. The United States Department of Energy earmarked USD 20 million to advance wind-turbine composite recycling, signalling policy momentum toward circularity. Canadian provinces sponsor advanced-materials clusters that couple academic R&D with injection over-molding pilot lines, aiming to retain domestic IP around bio-based thermoplastics.

Europe commands sophisticated design capabilities and stringent environmental regulations that foster rapid adoption of bio-resins and closed-loop processes. Although supply-chain disruptions and energy-cost spikes trimmed production in late-2024, the bloc maintains a 21.74% share of global volumes. Initiatives such as Vestas's circular blades and low-emission towers illustrate how EU climate policy is steering OEM priorities toward holistic sustainability. Eastern European nations, leveraging skilled labor and proximity to Western markets, are courting investment in pultrusion and filament-winding plants.

South America and the Middle East & Africa, while collectively smaller, are registering outsized percentage gains as infrastructure modernization and desalination projects specify composite solutions. Brazilian wind corridors, Saudi desalination brine lines and South African electric-bus bodies are notable demand pockets. Technology transfer from multinational players, combined with local reinforcement supply (sisal, jute), is catalysing indigenous innovation and gradually narrowing cost gaps with imported parts.

- 3M

- Arkema

- BASF

- CPIC BRASIL Fibras de Vidro Ltda

- DuPont

- Exel Composites

- Gurit Services AG

- Hexcel Corporation

- HS HYOSUNG ADVANCED MATERIALS

- Lanxess

- Mitsubishi Chemical Group Corporation.

- Nippon Graphite Fiber Co., Ltd.

- Owens Corning

- SGL Carbon

- Syensqo

- Teijin Limited

- Toray Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification-Driven Carbon-Fiber Demand in E-Mobility

- 4.2.2 Increasing Usage in the Manufacturing of Wind Turbine

- 4.2.3 Growing Adoption of Thermoplastic Composites in Mass-Production Automotive

- 4.2.4 Technological Advancement in the Field of Material Science

- 4.2.5 Increasing Use of Composites in the Aerospace and Defense Industry

- 4.3 Market Restraints

- 4.3.1 High Cost of Composite Materials

- 4.3.2 Challenges in Recycling of these Materials

- 4.3.3 Skilled-Labour Gap in Automated Lay-up Processes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Matrix Material

- 5.1.1 Polymer Matrix Composites (PMC)

- 5.1.1.1 Thermoset Resins

- 5.1.1.2 Thermoplastic Resins

- 5.1.2 Ceramic/Carbon Matrix Composites (CMCs)

- 5.1.3 Other Matrices (Metal Matrix Composites)

- 5.1.1 Polymer Matrix Composites (PMC)

- 5.2 By Reinforcement Fiber

- 5.2.1 Glass Fiber

- 5.2.2 Carbon Fiber

- 5.2.3 Aramid Fiber

- 5.2.4 Other Fibers (Natural/Bio Fiber)

- 5.3 By End-use Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Wind Energy

- 5.3.3 Aerospace and Defense

- 5.3.4 Pipes and Tanks

- 5.3.5 Construction

- 5.3.6 Electrical and Electronics

- 5.3.7 Sports and Recreation

- 5.3.8 Other End user Industries (Healthcare, Marine, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Malaysia

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)}

- 6.3.1 3M

- 6.3.2 Arkema

- 6.3.3 BASF

- 6.3.4 CPIC BRASIL Fibras de Vidro Ltda

- 6.3.5 DuPont

- 6.3.6 Exel Composites

- 6.3.7 Gurit Services AG

- 6.3.8 Hexcel Corporation

- 6.3.9 HS HYOSUNG ADVANCED MATERIALS

- 6.3.10 Lanxess

- 6.3.11 Mitsubishi Chemical Group Corporation.

- 6.3.12 Nippon Graphite Fiber Co., Ltd.

- 6.3.13 Owens Corning

- 6.3.14 SGL Carbon

- 6.3.15 Syensqo

- 6.3.16 Teijin Limited

- 6.3.17 Toray Industries Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

编织复合材料市场:依纤维类型、编织技术、製造流程、树脂类型和最终用途产业划分-2026-2032年全球市场预测复合材料预成型体市场:依材料、终端应用产业及销售管道划分-2026-2032年全球市场预测

编织复合材料市场:依纤维类型、编织技术、製造流程、树脂类型和最终用途产业划分-2026-2032年全球市场预测复合材料预成型体市场:依材料、终端应用产业及销售管道划分-2026-2032年全球市场预测 耐热材料市场预测至2034年-按材料类型、温度范围、产品形式、应用、最终用户和地区分類的全球分析PP芯复合毡市场:依产品类型、产品厚度、涂层类型、最终用途产业、通路划分,全球预测(2026-2032年)聚合物改质硅酸盐水泥砂浆市场:依产品种类、应用、最终用途及通路-2026-2032年全球预测阻尼复合材料市场:依材料类型、形状、技术和应用划分-2026-2032年全球预测斜纹碳纤维布市场按产品类型、织造类型、纤维类型、製程和应用划分-全球预测,2026-2032年软管橡胶化合物市场按化合物类型、增强类型、终端用户产业和分销管道划分,全球预测(2026-2032年)

耐热材料市场预测至2034年-按材料类型、温度范围、产品形式、应用、最终用户和地区分類的全球分析PP芯复合毡市场:依产品类型、产品厚度、涂层类型、最终用途产业、通路划分,全球预测(2026-2032年)聚合物改质硅酸盐水泥砂浆市场:依产品种类、应用、最终用途及通路-2026-2032年全球预测阻尼复合材料市场:依材料类型、形状、技术和应用划分-2026-2032年全球预测斜纹碳纤维布市场按产品类型、织造类型、纤维类型、製程和应用划分-全球预测,2026-2032年软管橡胶化合物市场按化合物类型、增强类型、终端用户产业和分销管道划分,全球预测(2026-2032年) 复合材料市场分析及预测(至2035年):类型、产品、应用、技术、材料类型、最终用户、製程、组件、功能与部署方法

复合材料市场分析及预测(至2035年):类型、产品、应用、技术、材料类型、最终用户、製程、组件、功能与部署方法 全球结构复合材料市场规模、份额、趋势和成长分析报告(2026-2034)

全球结构复合材料市场规模、份额、趋势和成长分析报告(2026-2034)