|

市场调查报告书

商品编码

1939669

语音辨识:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Voice Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

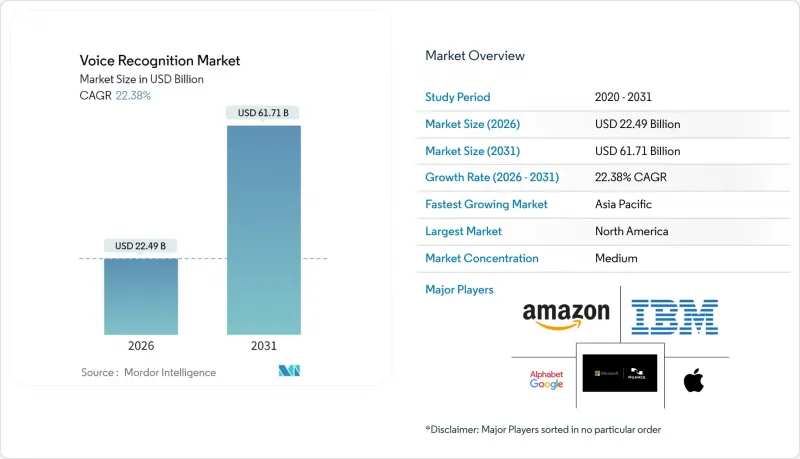

2025年全球语音辨识市场价值为183.9亿美元,预计2031年将达到617.1亿美元,而2026年为224.9亿美元。

预测期(2026-2031 年)的复合年增长率预计为 22.38%。

市场扩张反映了三大因素的共同作用:边缘人工智慧 (AI) 晶片组的快速普及、监管机构对紧急通讯网路现代化施加的压力,以及企业转向语音生物识别技术进行客户身份验证。目前,以软体为中心的架构占据主导地位,70.7% 的市场份额集中在软体开发工具包 (SDK) 和应用程式介面 (API) 平台。同时,到 2024 年,62.1% 的部署将云端部署。从区域来看,亚洲将在 2024 年占据榜首,市占率达到 32.5%,这主要得益于对多语言介面的需求以及强大的晶片製造生态系统。虽然语音辨识技术仍是主导技术平台,市占率高达 81.2%,但设备端处理将实现 25% 的复合年增长率,这标誌着从纯云设计到混合或完全本地推理引擎的决定性转变。

全球语音辨识市场趋势与洞察

亚洲边缘设备语音AI晶片激增

Chipintelli发表14款离线AI语音晶片,以及联发科推出MR Breeze ASR 25型号,都显示企业正在加速投资研发针对区域语言优化的专用晶片。在地化技术能够降低延迟,解决与云端串流相关的隐私问题,并巩固传统上依赖北美超大规模资料中心业者的国内供应链。亚洲半导体公司正利用这一优势,透过向设备OEM厂商提供可处理印尼、越南和印度等市场语码切换的承包语音协定栈,来巩固该地区在边缘推理创新领域的领先地位。

北美地区加强对语音911和紧急呼叫系统的监管

美国联邦通讯委员会 (FCC) 的新规要求美国通讯业者使用基于 IP 的对话启动协定(SIP) 路由 911 紧急呼叫,在 165 公尺半径范围内以 90% 的可靠性降低误路由,并支援即时文字和视讯。专注于紧急服务的语音辨识供应商预计将实现收入成长,因为国家和区域层面的合规期限将在未来 6-12 个月内设定。这项强制性规定树立了一个模板,很可能也会影响欧洲的公共网络,从而扩大对语音分析的潜在需求。语音分析技术能够利用转录音讯和元资料来丰富事件资料。

口音和方言识别方面的挑战阻碍了其在非洲的广泛应用。

93种非洲口音的测试表明,医疗实体识别错误率仍需提高25%至34%。 NaijaVoices的1800小时资料集将Whisper模型的字词辨识错误率降低了75.86%,但建构文化丰富的语料库的成本和复杂性阻碍了其商业部署。 Intron Health的160万美元种子轮融资显示投资者已意识到这个问题,同时也凸显了在地化模型训练的高额资金需求。

细分市场分析

预计到2025年,云端服务将占全球收入的61.60%,随着企业优先考虑快速部署、持续模型更新和广泛的语言支持,这一比例预计还将继续增长。金融机构和医疗保健提供者越来越多地选择混合架构,将原始资料保留在本地,同时在云端共用模型训练结果。这种方法在合规性和集中式学习带来的表现提升之间取得了平衡。因此,本地部署对于满足企业自主资料需求仍然至关重要,这将推动该领域在2031年之前保持两位数的持续成长。

对高可用性语音终端日益增长的需求正促使超大规模资料中心业者提供承包API,从而降低中型企业的整体拥有成本 (TCO),并降低独立开发者的准入门槛。这正在扩大语音辨识市场的应用范围,使其从消费性设备扩展到流程自动化、物流和现场服务工作流程等领域。预计到2031年,云端语音辨识市场规模将接近385亿美元,这反映了新增工作负载和现有部署的成长。

到2025年,软体平台将占全球支出的70.05%,这一关键差异推动了产业从专有硬体向模组化、开发者友善工具的转型。 RESTful API和预先建构语言模型的普及,使得许多应用场景不再需要客製化晶片。服务领域虽然规模较小,但正以23.20%的复合年增长率快速成长,因为企业越来越多地将网域优化、语音辨识和安全合规等工作外包给专业供应商。

硬体在边缘延迟、离线可用性和声波束成形至关重要的领域(例如汽车资讯娱乐和工业头戴式显示器)仍然占有一席之地,但许多新进入者正在透过使用平台即服务 (PaaS) 解决方案来绕过硬件,这表明横向软体提供商和垂直整合的硬体专家之间的差距正在扩大。

语音辨识市场依部署类型(云端/本地部署)、组件(软体/SDK、硬体、服务)、技术(语音辨识、语音生物识别、边缘语音AI)、装置类型(智慧型手机、智慧音箱、车载设备、穿戴式装置、POS机)、应用程式(身分验证、语音搜寻等)、终端用户市场预测以美元以金额为准。

区域分析

到2025年,亚洲将占全球收入的32.10%,这反映了该地区的半导体製造能力和语言多样性。各国国内政策都在支持人工智慧的应用,例如日本资助东南亚语言模式的倡议。北美仍然是这项技术的早期采用者,但由于积极的本地化和低成本设备,其市场份额已被亚洲蚕食。欧洲则在汽车和银行、金融服务及保险(BFSI)产业应用日益广泛,推动了其稳定成长。

中东地区以22.60%的复合年增长率领跑,这主要得益于海湾国家智慧城市规划,这些规划将对话式自助服务终端融入了市民服务基础设施。南美洲的成长率也达到了15%左右,这主要得益于语音搜寻在电子商务和银行身分验证领域的广泛应用。非洲的成长相对滞后,因为各地口音的多样性使得建构统一的模式变得复杂,但捐助者资助的语言计划和通讯基础设施升级有望从2027年起释放市场需求潜力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚洲边缘设备语音AI晶片激增

- 北美地区加强对语音911和紧急呼叫系统的监管

- 汽车製造商转向嵌入式语音操作系统以实现驾驶座个性化

- 欧洲银行、金融服务和保险 (BFSI) 产业采用语音生物识别取代基于知识的身份验证

- 智慧音箱家庭中语音商务的快速普及

- 亚太新兴市场对多语言语音使用者体验的需求日益增长

- 市场限制

- 口音和方言辨识方面的差距限制了非洲地区的普及。

- 隐私法规(GDPR、印度资料保护资料保护法)限制了云端语音资料保存。

- 标註特定领域语音语料库的高成本

- 在吵杂的工业环境中,精度持续下降

- 价值/供应链分析

- 监理展望

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

第五章 市场规模与成长预测

- 透过部署

- 云

- 本地部署

- 按组件

- 软体/SDK

- 硬体(ASIC、DSP、麦克风阵列)

- 服务(託管服务和专业服务)

- 透过技术

- 语音辨识

- 语音认证/语音生物识别

- 嵌入式/边缘语音人工智慧

- 依设备类型

- 智慧型手机和平板电脑

- 智慧音箱和显示器

- 汽车资讯娱乐和远端资讯处理

- 穿戴式装置(全无线耳机、智慧型手錶、AR/VR)

- 商用自助服务终端和POS机

- 透过使用

- 身份验证和安全

- 语音搜寻和语音指令

- 转录和字幕

- 虚拟助理和聊天机器人

- 医疗文件

- 终端用户产业

- 车

- 银行和金融服务

- 沟通

- 医疗保健提供者

- 政府和国防部

- 家用电子电器

- 零售与电子商务

- 工业和製造业

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- ASEAN

- 澳洲

- 纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- GCC

- 土耳其

- 以色列

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Apple Inc.

- Alphabet Inc.(Google LLC)

- Amazon.com Inc.

- Nuance Communications Inc.(Microsoft)

- IBM Corporation

- Baidu Inc.

- Samsung Electronics Co. Ltd.

- SoundHound AI Inc.

- iFLYTEK Co. Ltd.

- Sensory Inc.

- Cerence Inc.

- Verint Systems Inc.

- NICE Ltd.

- ElevenLabs

- Auraya Systems Pty Ltd.

- Intron Health

- PlayAI

- Mobvoi Information Technology Co. Ltd.

- Deepgram Inc.

- AssemblyAI Inc.

- Speechmatics Ltd.

第七章 市场机会与未来展望

The global voice recognition market was valued at USD 18.39 billion in 2025 and estimated to grow from USD 22.49 billion in 2026 to reach USD 61.71 billion by 2031, at a CAGR of 22.38% during the forecast period (2026-2031).

Market expansion reflects three concurrent forces: the rapid roll-out of edge artificial intelligence (AI) chipsets, regulatory pressure for modernising emergency communications networks, and enterprise migration to voice biometrics for customer authentication. Software-centric architectures now dominate because 70.7% of market value sits in software development kits and application-programming-interface platforms, while cloud deployment accounts for 62.1% of implementations in 2024. Regionally, Asia led with 32.5% market share in 2024 on the back of multilingual interface demand and strong chip manufacturing ecosystems; speech recognition technology remained the principal technology pillar with 81.2% share, yet embedded on-device processing delivered the fastest 25% CAGR, showing a decisive shift from cloud-only designs to hybrid or fully local inference engines.

Global Voice Recognition Market Trends and Insights

Explosion of Voice-AI Chips in Edge Devices across Asia

The release of 14 offline AI speech chips by Chipintelli and MediaTek's MR Breeze ASR 25 model signal escalating investment in specialised silicon optimised for regional languages. Localisation delivers lower latency, resolves privacy concerns tied to cloud streaming, and entrenches domestic supply chains that historically depended on North American hyperscalers. Asian semiconductor firms leverage this advantage to offer device OEMs turnkey voice stacks that handle code-switching in markets such as Indonesia, Vietnam, and India, reinforcing the region's leadership in edge inference innovation.

Regulatory Push for Voice-Enabled 911 and Emergency Dispatch Upgrades in North America

New FCC rules obligate US carriers to route 911 calls via IP-based Session Initiation Protocol, cut misrouting below a 165-meter radius at 90% confidence, and support real-time text and video. Voice recognition vendors positioned around emergency services gain a predictable revenue ramp because compliance deadlines fall within a 6-12-month horizon for nationwide and regional operators. The mandate creates a template likely to influence European public safety networks, expanding total addressable demand for voice analytics that enrich incident data with transcribed speech and metadata.

Accent and Dialect Recognition Gaps Limiting Adoption in Africa

Tests across 93 African accents showed medical entity error rates that still required 25-34% refinement via accent-specific fine-tuning. NaijaVoices' 1,800-hour dataset cut word-error rates for Whisper models by 75.86%, but the cost and complexity of curating culturally rich corpora slow commercial roll-outs. Intron Health's USD 1.6 million seed round underlines investor recognition of the problem, yet it also highlights the capital demands of localised model training.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift to Embedded Voice OS for Cockpit Personalisation

- BFSI Adoption of Voice Biometrics to Replace Knowledge-Based Authentication in Europe

- Privacy Regulations (GDPR, India DPDP) Restricting Cloud Voice-Data Retention

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud delivery generated 61.60% of global revenue in 2025, and that share is projected to widen as enterprises prioritise rapid rollout, continuous model updates, and broad language coverage. Financial institutions and healthcare providers increasingly select hybrid architectures that keep raw recordings on premises but pool model-training insights in the cloud. The approach balances compliance with the performance gains of aggregated learning. On-premise deployments therefore remain relevant for sovereign-data mandates, explaining why the segment still posts double-digit growth through 2031.

Demand for high-availability voice endpoints has pushed hyperscalers to expose turnkey APIs. Consequently, total cost of ownership falls for mid-sized enterprises, and barriers to entry lower for independent developers. The result is a wider application funnel for voice recognition market adoption, extending beyond consumer devices into process automation, logistics, and field-service workflows. The voice recognition market size for cloud implementations is set to approach USD 38.5 billion by 2031, reflecting both new workloads and expansion of existing deployments.

Software platforms captured 70.05% of global spend in 2025, a decisive margin that underpins the industry's pivot from proprietary hardware to modular, developer-friendly tooling. The availability of RESTful APIs and pre-built language models removes the need for bespoke silicon in many use cases. Services, although representing a smaller base, rise at 23.20% CAGR as enterprises engage specialist vendors for domain tuning, accent adaptation, and security compliance.

Hardware maintains relevance where edge latency, offline availability, or acoustic beam-forming matter, such as in automotive infotainment or industrial head-mounted displays. Yet most new entrants bypass hardware by consuming platform-as-a-service offerings, illustrating an expanding gap between horizontally oriented software providers and vertically integrated hardware specialists.

Voice Recognition Market is Segmented by Deployment (Cloud, On-Premise), Component (Software/SDK, Hardware, Services), Technology (Speech Recognition, Voice Biometrics, Edge Voice AI), Device Type (Smartphones, Smart Speakers, Automotive, Wearables, POS), Application (Authentication, Voice Search, and More), End-User Vertical (Automotive, BFSI, and Morel), and by Geography. Market Forecasts in Value (USD).

Geography Analysis

Asia generated 32.10% of 2025 turnover, reflecting the region's semiconductor capacity and linguistic diversity. Domestic policy supports AI acceleration; Japan's initiative to fund Southeast Asian language models is one example. North America remains technology's early-adopter hub but ceded share to Asia because of aggressive localisation and lower device costs. Europe grew steadily, influenced by automotive and BFSI thematic adoption.

The Middle East exhibits the quickest 22.60% CAGR as Gulf smart-city programmes embed conversational kiosks in citizen-services infrastructure. South America records mid-teens growth from e-commerce voice search and banking authentication. Africa faces a lag because accent diversity complicates universal models; however, donor-funded language projects and telecom upgrades may unlock latent demand from 2027 onward.

- Apple Inc.

- Alphabet Inc. (Google LLC)

- Amazon.com Inc.

- Nuance Communications Inc. (Microsoft)

- IBM Corporation

- Baidu Inc.

- Samsung Electronics Co. Ltd.

- SoundHound AI Inc.

- iFLYTEK Co. Ltd.

- Sensory Inc.

- Cerence Inc.

- Verint Systems Inc.

- NICE Ltd.

- ElevenLabs

- Auraya Systems Pty Ltd.

- Intron Health

- PlayAI

- Mobvoi Information Technology Co. Ltd.

- Deepgram Inc.

- AssemblyAI Inc.

- Speechmatics Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion of Voice-AI Chips in Edge Devices across Asia

- 4.2.2 Regulatory Push for Voice-Enabled 911 and Emergency Dispatch Upgrades in North America

- 4.2.3 Automotive OEM Shift to Embedded Voice OS for Cockpit Personalisation

- 4.2.4 BFSI Adoption of Voice Biometrics to Replace Knowledge-Based Authentication in Europe

- 4.2.5 Rapid Proliferation of Voice Commerce in Smart-Speaker Centric Households

- 4.2.6 Growth of Multilingual Voice UX Demand in Emerging APAC Markets

- 4.3 Market Restraints

- 4.3.1 Accent and Dialect Recognition Gaps Limiting Adoption in Africa

- 4.3.2 Privacy Regulations (GDPR, India DPDP) Restricting Cloud Voice Data Retention

- 4.3.3 High Cost of Annotated Domain-Specific Speech Corpora

- 4.3.4 Persistent Accuracy Lags in Noisy Industrial Environments

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Component

- 5.2.1 Software/SDK

- 5.2.2 Hardware (ASIC, DSP, Microphone Arrays)

- 5.2.3 Services (Managed and Professional)

- 5.3 By Technology

- 5.3.1 Speech Recognition

- 5.3.2 Speaker/Voice Biometrics

- 5.3.3 Embedded/Edge Voice AI

- 5.4 By Device Type

- 5.4.1 Smartphones and Tablets

- 5.4.2 Smart Speakers and Displays

- 5.4.3 Automotive Infotainment and Telematics

- 5.4.4 Wearables (TWS, Smart-watch, AR/VR)

- 5.4.5 Commercial Kiosks and POS

- 5.5 By Application

- 5.5.1 Authentication and Security

- 5.5.2 Voice Search and Command

- 5.5.3 Transcription and Captioning

- 5.5.4 Virtual Assistants and Chatbots

- 5.5.5 Medical Documentation

- 5.6 By End-user Vertical

- 5.6.1 Automotive

- 5.6.2 Banking and Financial Services

- 5.6.3 Telecommunications

- 5.6.4 Healthcare Providers

- 5.6.5 Government and Defence

- 5.6.6 Consumer Electronics

- 5.6.7 Retail and E-commerce

- 5.6.8 Industrial and Manufacturing

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 ASEAN

- 5.7.4.6 Australia

- 5.7.4.7 New Zealand

- 5.7.4.8 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 GCC

- 5.7.5.1.2 Turkey

- 5.7.5.1.3 Israel

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Egypt

- 5.7.5.2.4 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 Apple Inc.

- 6.4.2 Alphabet Inc. (Google LLC)

- 6.4.3 Amazon.com Inc.

- 6.4.4 Nuance Communications Inc. (Microsoft)

- 6.4.5 IBM Corporation

- 6.4.6 Baidu Inc.

- 6.4.7 Samsung Electronics Co. Ltd.

- 6.4.8 SoundHound AI Inc.

- 6.4.9 iFLYTEK Co. Ltd.

- 6.4.10 Sensory Inc.

- 6.4.11 Cerence Inc.

- 6.4.12 Verint Systems Inc.

- 6.4.13 NICE Ltd.

- 6.4.14 ElevenLabs

- 6.4.15 Auraya Systems Pty Ltd.

- 6.4.16 Intron Health

- 6.4.17 PlayAI

- 6.4.18 Mobvoi Information Technology Co. Ltd.

- 6.4.19 Deepgram Inc.

- 6.4.20 AssemblyAI Inc.

- 6.4.21 Speechmatics Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

人工智慧语音辨识晶片市场报告:趋势、预测与竞争分析(至2035年)

人工智慧语音辨识晶片市场报告:趋势、预测与竞争分析(至2035年) 2026年全球语音技术市场报告2026年全球语音支付软体市场报告2026年全球语音辨识市场报告2026年全球语音辨识与语音辨识市场报告2026年全球行动语音辨识软体市场报告

2026年全球语音技术市场报告2026年全球语音支付软体市场报告2026年全球语音辨识市场报告2026年全球语音辨识与语音辨识市场报告2026年全球行动语音辨识软体市场报告 全球语音辨识(SR/VR)市场规模、份额、趋势和成长分析报告:2026-2034年

全球语音辨识(SR/VR)市场规模、份额、趋势和成长分析报告:2026-2034年 2025-2029年全球人工智慧语音实验室市场

2025-2029年全球人工智慧语音实验室市场 语音辨识市场-全球产业规模、份额、趋势、机会及预测(依部署类型、最终用户、地区及竞争格局划分,2021-2031年)远距离语音辨识市场-全球产业规模、份额、趋势、机会、预测:按组件、应用、麦克风解决方案、地区和竞争对手划分,2021-2031年

语音辨识市场-全球产业规模、份额、趋势、机会及预测(依部署类型、最终用户、地区及竞争格局划分,2021-2031年)远距离语音辨识市场-全球产业规模、份额、趋势、机会、预测:按组件、应用、麦克风解决方案、地区和竞争对手划分,2021-2031年