|

市场调查报告书

商品编码

1939677

夹芯板:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Sandwich Panels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

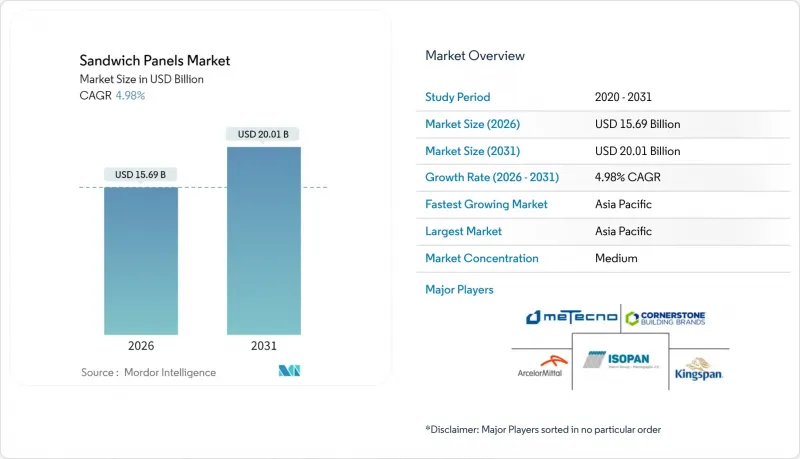

The Sandwich Panels market is expected to grow from USD 14.95 billion in 2025 to USD 15.69 billion in 2026 and is forecast to reach USD 20.01 billion by 2031 at 4.98% CAGR over 2026-2031.

Sustained demand for high-performance building envelopes in data centers, cold-storage hubs, and modular prefabrication lines anchors this expansion. Industrial developers favor factory-produced panels that combine structural integrity, thermal efficiency, and rapid installation, while public policy is moving building codes toward higher R-values and lower embodied carbon. Manufacturers are therefore scaling continuous production, experimenting with recyclable core chemistries, and integrating digital design tools that shorten project cycles. Consolidation remains moderate: leading multinationals deepen vertical integration, yet a long tail of regional specialists continues to supply localized configurations, keeping pricing discipline tight. The sandwich panels market benefits additionally from power-hungry digital infrastructure; hyperscale operators prefer robust, airtight envelopes that expedite commissioning and reduce mechanical loads.

Global Sandwich Panels Market Trends and Insights

Growing Cold-Storage Applications of Structural Insulated Panels

Polyurethane panels, rated R-7 to R-8 and operational from -45 °C to +80 °C, outperform EPS and fiberglass and thus dominate new cold-room specifications. Developers increasingly replace aging 37-year-old warehouses rather than retrofit, preferring factory-finished, hygienic panels that answer HACCP cleaning protocols. Speculative cold-store starts reached 2.5 million ft2 in 2024, signaling long-range confidence among institutional investors. Energy-intensive freezers also trigger utility rebates for better-insulated envelopes, further lifting orders for high-R sandwich assemblies.

Increasing Demand for PVDF-Based Aluminum Composite Panels

Architects and facade engineers value the 15-year-plus service life of PVDF-coated aluminum skins, while nano-PVDF formulations add self-cleaning properties that reduce OPEX in high-profile curtain walls. AAMA 2605-05 test compliance underlines scratch hardness, boiling-water adhesion, and color-fastness (ΔE < 1.3) performance metrics. The lightweight, design-flexible profile-paired with fire-retardant cores-simplifies facade anchoring, accelerates installation, and supports digitally printed graphics for brand-centric cladding projects.

Fire-Performance Limitations of Certain Panel Types

Organic foam cores such as PUR, PIR, EPS, and XPS can degrade rapidly above 250 °C, shedding mass and releasing toxic effluent that accelerates flashover conditions. European insurers often decline or surcharge facilities finished with combustible cores, especially in food-processing plants. Mineral-wool alternatives withstand higher temperatures but add weight and cost. Innovations such as intumescent inter-layers, fire stops at joints, and mineral-fiber fire barriers are being mainstreamed, yet full-scale burn tests remain the gold standard for regulatory acceptance. Countries such as Germany apply some of the strictest facade combustibility rules, constraining project-team material choices.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Prefabricated and Modular Construction

- Energy-Efficiency Regulations for Building Envelopes

- Oriented-Strand-Board VOC Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PUR panels contributed 41.32% to the sandwich panels market share in 2025 and are forecast to lead with a 5.34% CAGR, buoyed by R-7 to R-8 performance that outclasses polyisocyanurate, EPS, and fiberglass in freezer construction. The sandwich panels market size tied to PUR cores should widen as cold-storage developers retro-commission older stock and adopt continuous-manufactured modules that arrive with concealed-fastener joints and food-safe finishes.

Emerging supply bottlenecks in MDI feedstock have prompted producers to finetune catalyst packages, trimming cycle times without sacrificing closed-cell content. Environmental scrutiny, however, is nudging manufacturers to explore bio-sourced polyols and blowing agents with lower global-warming potential.

Aluminum captured 45.29% of the sandwich panels market share in 2025, underpinned by widespread extrusion capacity, corrosion resistance, and anodizing versatility. PVDF-coated coils boast 15-year color warranties, and nano-PVDF upgrades prolong facade cleanliness, minimizing service downtime. Continuous fiber reinforced thermoplastics, projected at 5.38% CAGR, are finding traction in data-center cladding where lightweight panels mitigate seismic loads, and carbon-fiber tapes allow double-digit span reductions without stiffener back-plates.

CFRT skins can be thermo-formed into complex radii, eliminating kerf-cutting and post-bonding labor. They also enable closed-loop recycling because both matrix and reinforcement remain thermoplastic. By contrast, steel skins dominate when point-load resistance trumps weight, especially in refrigerated logistics parks that specify heavy-duty racking ties. Fiberglass reinforced panels win in corrosive atmospheres such as aquaculture, where salt spray degrades metal fast.

The Sandwich Panels Report is Segmented by Core Material (Polyurethane (PUR), Polyisocyanurate (PIR), and More), Skin Material (Aluminum, Steel, Fiberglass Reinforced Panel (FRP), and More), Technology (Continuous and Discontinuous), Application (Wall Panels, Roof Panels, and More), End-Use Sector (Residential, Commercial, and More), and Geography (Asia-Pacific, North America, and More).

Geography Analysis

Asia-Pacific dominated with a 49.85% share in 2025 and posts the fastest 5.78% CAGR through 2031. India's data-center pipeline, Singapore's green-energy logistics, and Malaysia's semiconductor fabs all mandate thermally efficient, rapidly deployable envelopes. China's growth moderates yet remains structurally sizable; Beijing's shift to renovation programs favors thin, over-clad insulation retrofits that suit lightweight sandwich skins.

North America benefits from the Infrastructure Investment and Jobs Act. Cold-chain expansion in the Sunbelt and Mid-Atlantic integrates 200 mm PUR panels that satisfy Title 24 and IGCC code pathways. Canada's carbon-pricing framework steers public projects toward mineral-wool cores with EPD documentation. Mexico's maquiladora corridor is adding insulated roofing to comply with USMCA energy stipulations, a shift that spurs local panel lamination capacity.

Europe is rebounding from a low base; EU-wide construction. Still, the Energy Performance Directive's zero-emission targets drive retrofit vouchers, funneling budget toward thin-profile, high-lambda facades.

Middle East megaprojects, Datacenter campuses in KSA, free-zone warehouses in UAE, demand low-combustible cladding systems rated for 50 °C ambient. Latin America remains patchy: Brazilian logistics clusters adopt PIR panels, but political flux dampens larger public procurements.

- Alubel

- ArcelorMittal

- Areco

- Assan Panel A.S.

- Building Component Solutions LLC

- Cornerstone Building Brands, Inc.

- DANA Group of Companies

- EPACK Prefab

- Isopan

- Jiangsu Jingxue Energy Saving Technology Co., Ltd.

- Kingspan Group

- Lattonedil

- Marcegaglia Steel S.p.A.

- Metecno Group

- NAV SYSTEM

- Rautaruukki Corporation

- Romakowski GmbH and Co. KG

- Sintex

- Structural Panels

- Tata Steel

- Teknopanel

- Tonmat Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing cold-storage applications of structural insulated panels

- 4.2.2 Increasing demand for PVDF-based aluminium composite panels

- 4.2.3 Rapid growth of prefabricated and modular construction

- 4.2.4 Energy-efficiency regulations for building envelopes

- 4.2.5 Data-centre boom requiring high-performance envelopes

- 4.3 Market Restraints

- 4.3.1 Fire-performance limitations of certain panel types

- 4.3.2 Oriented-strand-board VOC emissions

- 4.3.3 Moisture ingress and long-term degradation in PUR/PIR cores

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Core Material

- 5.1.1 Polyurethane (PUR)

- 5.1.2 Polyisocyanurate (PIR)

- 5.1.3 Mineral Wool

- 5.1.4 Expanded Polystyrene (EPS)

- 5.1.5 Other Core Materials

- 5.2 By Skin Material

- 5.2.1 Continuous Fiber Reinforced Thermoplastics (CFRT)

- 5.2.2 Fiberglass Reinforced Panel (FRP)

- 5.2.3 Aluminum

- 5.2.4 Steel

- 5.2.5 Other Skin Materials

- 5.3 By Technology

- 5.3.1 Continuous

- 5.3.2 Discontinuous

- 5.4 By Application

- 5.4.1 Wall Panels

- 5.4.2 Roof Panels

- 5.4.3 Insulated Panels

- 5.4.4 Other Applications

- 5.5 By End-use Sector

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.5.4 Institutional and Infrastructure

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 Italy

- 5.6.3.4 France

- 5.6.3.5 Spain

- 5.6.3.6 Poland

- 5.6.3.7 NORDIC Countries

- 5.6.3.8 Hungary

- 5.6.3.9 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alubel

- 6.4.2 ArcelorMittal

- 6.4.3 Areco

- 6.4.4 Assan Panel A.S.

- 6.4.5 Building Component Solutions LLC

- 6.4.6 Cornerstone Building Brands, Inc.

- 6.4.7 DANA Group of Companies

- 6.4.8 EPACK Prefab

- 6.4.9 Isopan

- 6.4.10 Jiangsu Jingxue Energy Saving Technology Co., Ltd.

- 6.4.11 Kingspan Group

- 6.4.12 Lattonedil

- 6.4.13 Marcegaglia Steel S.p.A.

- 6.4.14 Metecno Group

- 6.4.15 NAV SYSTEM

- 6.4.16 Rautaruukki Corporation

- 6.4.17 Romakowski GmbH and Co. KG

- 6.4.18 Sintex

- 6.4.19 Structural Panels

- 6.4.20 Tata Steel

- 6.4.21 Teknopanel

- 6.4.22 Tonmat Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

夹芯板市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、面板材料、地区和竞争格局划分,2021-2031年

夹芯板市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、面板材料、地区和竞争格局划分,2021-2031年 全球夹芯板市场:市场规模、份额、成长率、产业分析、类型、应用和地区因素及未来预测(2026-2034)

全球夹芯板市场:市场规模、份额、成长率、产业分析、类型、应用和地区因素及未来预测(2026-2034) 夹芯板市场规模、份额、成长分析(按产品、应用、覆材、最终用途和地区划分)-2026-2033年产业预测

夹芯板市场规模、份额、成长分析(按产品、应用、覆材、最终用途和地区划分)-2026-2033年产业预测 2025年全球聚异氰酸酯(PIR)隔热夹芯板市场报告2025年全球夹芯板市场报告

2025年全球聚异氰酸酯(PIR)隔热夹芯板市场报告2025年全球夹芯板市场报告 全球夹层板市场

全球夹层板市场 钢製夹层板市场规模、份额和成长分析(按产品类型、应用、最终用途和地区)- 产业预测 2025-2032

钢製夹层板市场规模、份额和成长分析(按产品类型、应用、最终用途和地区)- 产业预测 2025-2032 夹芯板的印度市场评估:各芯材类型,厚度,各用途,各建设类型,各最终用途产业,各地区,机会,预测(2018年度~2032年度)日本的夹芯板市场评估:核心木材类型·厚度·用途·建筑类型·终端用户产业·各地区的机会及预测 (2018-2032年)夹芯板市场:各核心材料类型,各厚度,各用途,各建设类型,各最终用途产业,各地区,机会,预测,2017年~2031年

夹芯板的印度市场评估:各芯材类型,厚度,各用途,各建设类型,各最终用途产业,各地区,机会,预测(2018年度~2032年度)日本的夹芯板市场评估:核心木材类型·厚度·用途·建筑类型·终端用户产业·各地区的机会及预测 (2018-2032年)夹芯板市场:各核心材料类型,各厚度,各用途,各建设类型,各最终用途产业,各地区,机会,预测,2017年~2031年