|

市场调查报告书

商品编码

1939679

UV固化黏合剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)UV-Curable Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

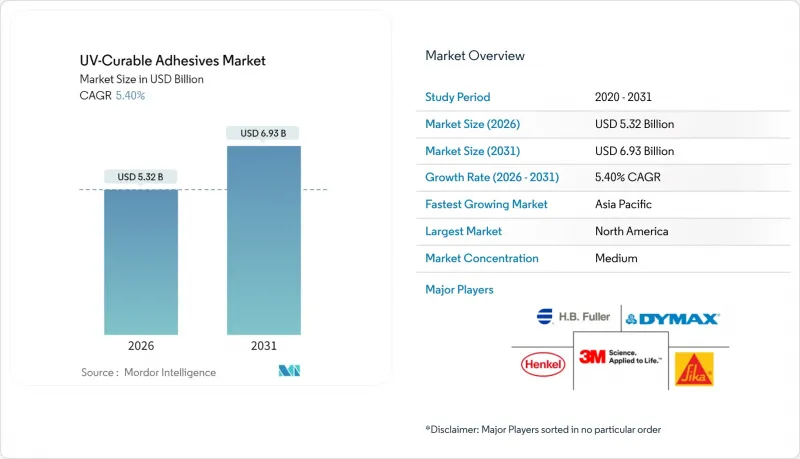

预计紫外线固化黏合剂市场将从 2025 年的 50.5 亿美元成长到 2026 年的 53.2 亿美元,到 2031 年将达到 69.3 亿美元,2026 年至 2031 年的复合年增长率为 5.4%。

紫外光固化黏合剂市场正从利基应用发展成为各大终端应用领域(包括医疗设备、家用电子电器、汽车复合材料和包装)不可或缺的生产投入品。这主要归功于其即时固化的特性,无需烘箱固化,减少了挥发性有机化合物 (VOC) 的排放,并有助于实现轻量化复合材料组件。半导体规模的缩小、欧美严格的 VOC 法规(推动了无溶剂化学的发展)以及确保光光引发剂稳定供应的垂直整合供应链也促进了市场成长。北美凭藉先进的医疗设备製造技术和汽车产业对光固化结构黏合剂的早期应用,保持着技术优势;而亚太地区则受益于半导体封装产能的提升,正在加速成长。在这种竞争激烈的市场环境中,拥有产品创新和法规专业知识的公司,尤其是那些拥有符合 ISO 10993 和 REACH 法规的配方技术的公司,正在获得竞争优势。

全球紫外光固化黏合剂市场趋势及洞察

UV固化黏合剂在汽车和航太领域的应用

随着电动车产量的成长,汽车製造商面临着在不发生热变形的情况下黏合不同基材(例如铝和碳纤维)的压力。紫外光固化黏合剂市场提供可在数秒内完全固化并保持高搭接剪切强度的配方。 Polestar 1 和伦敦的 TX5 计程车平台已证明该方法在大规模生产中的可行性,实现了减重和车内噪音控制的双重目标。航太生产也呈现类似的趋势,因为紫外光固化技术缩短了高压釜製程时间并降低了复合材料层压板的能耗。随着全球电池组产量的扩大,相关人员预测,到 2030 年,对耐高温紫外固化环氧树脂的需求将进一步成长。

更严格的VOC/REACH法规推动了无溶剂化学品的发展。

欧盟于2023年8月生效的二异氰酸酯含量上限(超过0.1%)迫使加工商转向零排放解决方案,这为紫外光固化黏合剂市场带来了即时的监管推动作用。加拿大将于2024年1月生效的VOC(挥发性有机化合物)排放上限也将反映这一趋势,并进一步促进北美软包装生产线采用此技术。随着生命週期评估指标逐渐成为采购标准,无溶剂固化技术可望获得更优的环保认证,并提升品牌的ESG(环境、社会和治理)声誉。汉高等主要供应商目前正在将二氧化碳回收原料製程商业化,降低成品黏合剂的碳含量。亚太地区也考虑类似的VOC指令,这有望在两年内实现全球无溶剂标准的统一,从而加速紫外光固化技术在竞争激烈的双组分环氧树脂市场中的普及。

UV LED固化系统高昂的购置成本

工业LED阵列的成本在5万至50万美元之间。虽然大批量生产可以透过降低电力成本来收回投资,但中小企业难以获得设备升级所需的资金筹措,从而延缓了整个生产线的改造。波长变更的製程检验有停机风险,而快速的技术创新週期也令人担忧LED会在投资收回之前就被淘汰。儘管供应商正在透过租赁模式和模组化组件来应对,但全球融资仍然不平衡。欧盟和美国的能源效率补贴奖励或许有助于弥合这一差距,但在LED得到广泛应用之前,资本成本可能仍会继续抑制某些黏合剂的需求。

细分市场分析

到2025年,丙烯酸类配方将占据紫外光固化黏合剂市场47.10%的份额,这得益于其成熟的供应炼和在各种基材上的广泛适用性。丙烯酸类产品的市场规模得益于大宗商品规模的原料供应,这确保了价格稳定和全球采购。然而,预计到2031年将以5.55%的复合年增长率增长的环氧基产品,正在蚕食丙烯酸类产品在汽车结构连接和半导体底部填充等领域的市场主导地位,这些领域对高模量和耐热循环性能的要求极高。

阳离子光引发剂的最新创新使得环氧树脂的固化时间从几分钟缩短到几秒钟,且不影响玻璃化转变温度,从而提高了生产线速度。硅酮和聚氨酯在一些细分市场中仍然占有一席之地,在这些市场中,极端温度波动和高柔软性比拉伸强度更为重要。在预测期内,REACH法规对某些丙烯酸酯单体的持续审查可能会降低丙烯酸树脂的成本优势。这可能会进一步推动特种环氧树脂在紫外光固化黏合剂市场中进入主流应用领域。

这份紫外光固化黏合剂报告按树脂类型(硅酮、丙烯酸酯、聚氨酯、环氧树脂及其他树脂类型)、终端用户行业(医疗、电气电子、交通运输、包装、家具及其他终端用户行业)和地区(亚太地区、北美、欧洲、南美以及中东和非洲)进行细分。市场预测以美元计价。

区域分析

到2025年,北美将占全球收入的42.80%,这主要得益于明尼苏达州、加利福尼亚州和安大略省的原始设备製造商(OEM)采用经FDA批准的导管和诊断感测器材料,以及底特律的电动汽车工厂引入用于电池组的紫外线结构黏合剂。此外,该地区还受益于透明的监管路径,缩短了新化学产品的上市时间,从而鼓励供应商加强研发投入。

亚太地区预计将以5.65%的复合年增长率实现最快成长,主要得益于中国大陆、台湾和韩国半导体封装产能的快速扩张。长虹聚合物投资16亿美元的丙烯酸联合装置以及杜邦在新舄的光阻剂扩建项目,都为该地区的原料和先进材料生态系统提供了支撑。随着日本和中国汽车製造商加大复合材料底盘的应用,汽车产业对高模量UV环氧树脂的需求不断增长,从而创造了新的市场需求。

在欧洲,由于严格的REACH法规淘汰了溶剂型竞争对手并增加了合规成本,导致市场平衡正在扩大。对永续性的需求推动了循环设计的应用,例如汉高塞拉尼斯公司提供的二氧化碳衍生原料以及采用Saperatec技术的黏合剂回收。中东、非洲和南美洲虽然仍处于起步阶段,但食品出口所需的软包装产能建设正蓬勃发展,这为紫外光固化黏合剂市场带来了额外的需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 汽车和航太工业中的紫外光固化黏合剂

- 更严格的VOC/REACH法规有利于无溶剂化学品

- 家用电子电器的微型化

- 穿戴式医疗设备的快速普及

- 在线连续数位包装印刷生产线对即时黏合的需求

- 市场限制

- UV LED固化系统高昂的购置成本

- 替代性双组分环氧树脂和氰基丙烯酸酯的可用性

- 关键光引发剂供应的不确定性

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依树脂类型

- 硅

- 丙烯酸纤维

- 聚氨酯

- 环氧树脂

- 其他树脂类型

- 按最终用户行业划分

- 医疗保健

- 电气和电子设备

- 运输

- 包装

- 家具

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 印尼

- 马来西亚

- 泰国

- 越南

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 埃及

- 奈及利亚

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3M

- Arkema

- artience Co., Ltd.

- AVERY DENNISON CORPORATION

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dymax

- HB Fuller Company

- Henkel AG & Co. KGaA

- Master Bond Inc.

- Panacol-Elosol GmbH

- Parson Adhesives, Inc.

- Permabond LLC

- Sika AG

第七章 市场机会与未来展望

The UV-Curable Adhesives Market is expected to grow from USD 5.05 billion in 2025 to USD 5.32 billion in 2026 and is forecast to reach USD 6.93 billion by 2031 at 5.4% CAGR over 2026-2031.

Across every major end-use domain, such as medical devices, consumer electronics, automotive composites, and packaging, the UV-curable adhesives market is evolving from niche usage to an essential production input, primarily because instant on-demand curing eliminates oven dwell time, removes volatile organic compound emissions, and supports lightweight mixed-material assemblies. Growth momentum also benefits from semiconductor miniaturization, stricter VOC caps in Europe and North America that favor solvent-free chemistries, and vertically integrated supply chains that secure photoinitiator availability. North America keeps its technological edge through advanced medical manufacturing and early automotive adoption of light-curing structural bonds, while Asia-Pacific accelerates on the back of semiconductor packaging capacity additions. Competitive dynamics reward firms that pair product innovation with regulatory expertise, especially in formulations meeting ISO 10993 and REACH guidelines.

Global UV-Curable Adhesives Market Trends and Insights

UV-Curable Adhesives Adoption in Automotive and Aerospace

Rising electric-vehicle production pushes automakers to bond dissimilar substrates such as aluminum and carbon fiber without inducing thermal distortion, and the UV-curable adhesives market supplies formulations that fully cure in seconds while retaining high lap-shear strength. Polestar 1 and London's TX5 taxi platforms demonstrate the mass-manufacturing viability of this approach, achieving both weight reduction and cabin noise management. Aerospace production mirrors automotive trends as UV-curing shortens autoclave schedules and lowers energy consumption for composite laminates. With global battery-pack production ramping, stakeholders expect demand for high-temperature-tolerant UV-curable epoxies to intensify through 2030.

Stricter VOC/REACH Regulations Favor Solvent-Free Chemistries

The August 2023 EU restriction on diisocyanates above 0.1% content forces converters to shift toward zero-emission solutions, giving the UV-curable adhesives market an immediate regulatory tailwind. Canada's January 2024 VOC limits mirror these caps and further raise adoption in North American flexible-packaging lines. As life-cycle-assessment metrics become procurement criteria, zero-solvent curing scores superior eco-labels, and enhance brand ESG credentials. Leading suppliers like Henkel now commercialize CO2-captured raw-material routes, lowering the embedded carbon of finished adhesives. Because similar VOC directives are under review in APAC, global alignment on solvent-free standards is likely within two years, accelerating UV penetration ahead of competing two-part epoxies.

High Capital Cost of UV-LED Curing Systems

Industrial LED arrays cost USD 50,000-500,000, and although electricity savings recover cash over high-volume runs, small firms struggle to finance upgrades, slowing full-line conversions. Process re-validation for wavelength changes adds downtime risk, and fast innovation cycles create perceived obsolescence before payback concludes. Vendors respond with leasing models and modular head units, yet credit access remains uneven worldwide. Incentives linked to energy-efficiency grants in the EU and U.S. can close gaps, but until uptake broadens, equipment expense will restrain some adhesives volumes.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturization in Consumer Electronics

- Rapid Uptake in Wearable Medical Devices

- Supply Volatility of Key Photoinitiators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic formulations captured 47.10% of the UV-curable adhesives market share in 2025, owing to mature supply chains and multi-substrate compatibility. The UV-curable adhesives market size for acrylic grades benefits from commodity-scale raw materials that steady pricing and facilitate global sourcing. Yet epoxies, forecast to compound at 5.55% through 2031, are eroding acrylic headroom in automotive structural joints and semiconductor under-fills where high modulus and thermal cycling endurance are non-negotiable.

Recent innovations in cationic photoinitiators shorten epoxy cure from minutes to seconds without compromising glass-transition temperature, enabling high-speed line takt. Silicone and polyurethane niches persist where extreme temperature swing or high flexibility outweigh tensile strength needs. Over the forecast horizon, ongoing REACH scrutiny of certain acrylate monomers may narrow the acrylic cost advantage, potentially pushing specialty epoxies further into mainstream applications of the UV-curable adhesives market.

The UV-Curable Adhesives Report is Segmented by Resin Type (Silicon, Acrylic, Polyurethane, Epoxy, and Other Resin Types), End-User Industry (Medical, Electrical and Electronics, Transportation, Packaging, Furniture, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 42.80% of global revenue in 2025 as OEMs in Minnesota, California, and Ontario relied on FDA-cleared grades for catheters and diagnostic sensors, while Detroit electric-vehicle plants adopted UV structural bonds for battery packs. The region also benefits from transparent regulatory pathways that shorten time-to-market for new chemistries, reinforcing supplier research and development investment.

Asia-Pacific delivers the fastest 5.65% CAGR on the back of surging semiconductor packaging capacity in China, Taiwan, and South Korea. Changhong Polymer's USD 1.6 billion acrylic-acid complex and DuPont's photoresist expansion in Niigata shore up regional raw-material and advanced-material ecosystems. Automotive demand rises as Japanese and Chinese OEMs scale mixed-material chassis, creating fresh pull for high-modulus UV epoxies.

Europe's balance grows under the weight of stringent REACH rules that both eliminate solvent competitors and add compliance costs. Sustainability mandates drive the adoption of Henkel-Celanese CO2-derived feedstocks and circular designs like Saperatec-enabled adhesive recycling. Middle East and Africa and South America remain emerging but show momentum in flexible-packaging installations targeting food exports, adding incremental volume to the UV-curable adhesives market

- 3M

- Arkema

- artience Co., Ltd.

- AVERY DENNISON CORPORATION

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Master Bond Inc.

- Panacol-Elosol GmbH

- Parson Adhesives, Inc.

- Permabond LLC

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 UV-Curable Adhesives Adoption in Automotive and Aerospace

- 4.2.2 Stricter VOC/REACH Regulations Favor Solvent-Free Chemistries

- 4.2.3 Miniaturisation in Consumer Electronics

- 4.2.4 Rapid Uptake in Wearable Medical Devices

- 4.2.5 In-Line Digital Packaging Print Lines Demanding Instant Bonding

- 4.3 Market Restraints

- 4.3.1 High Capital Cost of UV-LED Curing Systems

- 4.3.2 Availability of Alternative 2-Part Epoxies and Cyanoacrylates

- 4.3.3 Supply Volatility of Key Photoinitiators

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Silicon

- 5.1.2 Acrylic

- 5.1.3 Polyurethane

- 5.1.4 Epoxy

- 5.1.5 Other Resin Types

- 5.2 By End-user Industry

- 5.2.1 Medical

- 5.2.2 Electrical and Electronics

- 5.2.3 Transportation

- 5.2.4 Packaging

- 5.2.5 Furniture

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 South Korea

- 5.3.1.4 India

- 5.3.1.5 Indonesia

- 5.3.1.6 Malaysia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 artience Co., Ltd.

- 6.4.4 AVERY DENNISON CORPORATION

- 6.4.5 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.6 Dymax

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Master Bond Inc.

- 6.4.10 Panacol-Elosol GmbH

- 6.4.11 Parson Adhesives, Inc.

- 6.4.12 Permabond LLC

- 6.4.13 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

UV黏合剂市场机会、成长要素、产业趋势分析及2026年至2035年预测。

UV黏合剂市场机会、成长要素、产业趋势分析及2026年至2035年预测。 2026年全球UV固化黏合剂市场报告2026年全球紫外线黏合剂市场报告

2026年全球UV固化黏合剂市场报告2026年全球紫外线黏合剂市场报告 2026-2030年全球紫外光固化黏合剂市场

2026-2030年全球紫外光固化黏合剂市场 UV黏合剂市场规模、份额及成长分析(按产品类型、应用和地区划分)-2026-2033年产业预测

UV黏合剂市场规模、份额及成长分析(按产品类型、应用和地区划分)-2026-2033年产业预测 紫外线固化胶合剂市场-全球产业规模、份额、趋势、机会和预测,按树脂类型、应用、地区和竞争情况细分,2020-2030 年

紫外线固化胶合剂市场-全球产业规模、份额、趋势、机会和预测,按树脂类型、应用、地区和竞争情况细分,2020-2030 年 紫外线黏合剂市场 - 预测 2025-2030

紫外线黏合剂市场 - 预测 2025-2030 紫外线黏合剂市场(按产品类型、应用和地区)

紫外线黏合剂市场(按产品类型、应用和地区) 2025-2033年紫外光固化胶黏剂市场报告(依树脂类型、基材、最终用户和地区)

2025-2033年紫外光固化胶黏剂市场报告(依树脂类型、基材、最终用户和地区) UV硬化型黏剂的全球市场:树脂类型·基材·终端用户·不同地区的预测 (~2032年)

UV硬化型黏剂的全球市场:树脂类型·基材·终端用户·不同地区的预测 (~2032年)