|

市场调查报告书

商品编码

1939689

二氧化钛:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Titanium Dioxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

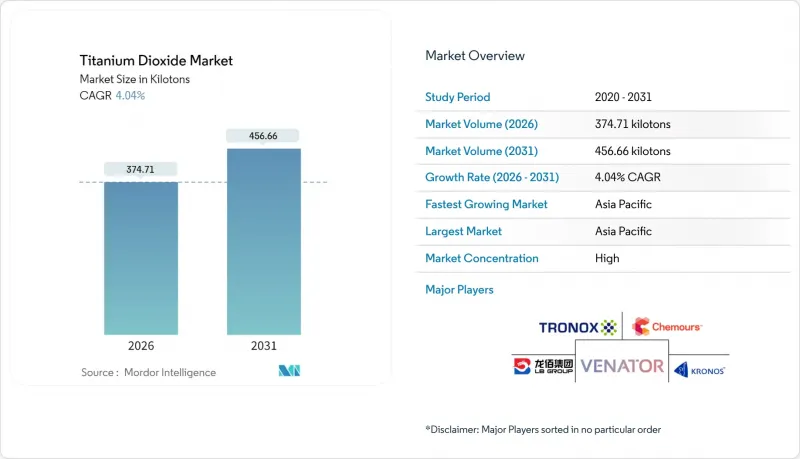

预计二氧化钛市场将从 2025 年的 360.16 千吨成长到 2026 年的 374.71 千吨,预计到 2031 年将达到 456.66 千吨,2026 年至 2031 年的复合年增长率为 4.04%。

建筑、包装、汽车塑胶和冷屋顶涂料行业需求的成长抵消了监管方面的不利因素,特别是欧洲强制标註第二类致癌性以及对中国原材料征收反倾销税的影响。亚太地区依託中国此供应基地,并受惠于印度的在地化策略,继续以4.92%的复合年增长率成长。製造商正努力平衡钛铁矿和金红石原料成本波动带来的压力与氯化製程的技术升级。例如,科慕公司透过製程优化,在不进行大规模资本投资的情况下,产能提高了15%。同时,特诺克斯公司等企业采取的垂直整合策略降低了原物料价格波动的风险。欧盟与其他地区之间的监管差异促使企业开发差异化的产品系列,并为区域套利创造了空间。

全球二氧化钛市场趋势及展望

亚太地区对水性建筑涂料的需求激增

中国、印度和印尼日益严格的挥发性有机化合物(VOC)法规正在加速水性涂料替代溶剂型涂料,从而推动该地区对金红石颜料的需求成长。区域涂料生产线正在升级分散技术以实现遮盖力与溶剂型涂料相当,这支撑了二氧化钛市场的持续成长。印度和印尼的基础设施奖励策略进一步推动了需求,而本地氯化物生产能力则确保了稳定的供应。配方师优先考虑低气味和安全的工作环境,这提高了承包商的接受度。儘管原物料价格波动,但这种转变仍构成了一个结构性利多因素。

欧洲向轻量化、高光泽汽车塑胶转型

欧盟对车辆平均二氧化碳排放的严格规定,使得轻量化成为设计策略的核心。透过将二氧化钛添加到聚丙烯和聚碳酸酯饰件中,製造商可以获得媲美喷漆金属面板的高光泽表面,同时显着降低重量。这意味着车辆重量每减轻10%,燃油经济性就能提高5-7%。豪华汽车製造商正在采用疏水性二氧化钛,例如TIOXIDE TR48,这种材料在高温加工条件下仍能保持分散性,且不会失去光泽。由于这些特种等级的二氧化钛价格较高,且能最大限度地降低法规带来的替代风险,因此二氧化钛市场在销售和价值方面都在不断增长。

欧盟将二氧化钛列为致癌性,增加了标籤检视成本

欧盟法规2025/4要求,二氧化钛含量达到或超过1%的粉末配方必须标示致癌性警告。油漆、塑性溶胶和印刷油墨供应商面临配方变更、新包装设计以及法律审查,合规成本因此增加。英国和北美不同的法规使全球产品组合管理更加复杂,并迫使企业采用双重标籤策略。生产週期缩短推高了单位成本,并抑制了DIY通路的非必需品需求。欧洲法院于2022年裁定该危险标籤无效,但在2025年经过科学重新评估后又推翻了该裁决,这进一步加剧了二氧化钛市场的不确定性。

细分市场分析

截至2025年,金红石型二氧化钛将占77.60%的二氧化钛市场份额,主要得益于其高屈光(2.7)和优异的耐候性。这些优势使其在对长期光泽保持要求极高的应用领域中占据了重要地位,例如外墙涂料、汽车面漆和聚合物母粒。而兼具光催化性能的双功能型金红石型二氧化钛则为自清洁表面开闢了新的可能性,进一步巩固了其优势。

锐钛矿满足了剩余的需求,其复合年增长率高达4.32%,主要得益于医药添加剂和光催化建筑材料等细分应用领域的成长。表面改质的锐钛矿可以延长食品接触纸的保质期,并赋予其独特的蓝色色调,这种色调在高檔办公用纸中备受青睐。

利用低品位钛铁矿和小规模资本投入的硫酸法工艺,预计到2025年将占二氧化钛市场64.30%的份额。然而,由于对酸性硫酸盐废液的监管日益严格,氯化法产能正以4.53%的复合年增长率快速成长。氯化法工厂使用高二氧化钛矿渣或天然金红石,主要生产杂质含量较低的金红石颜料,因此能够为高端涂料和母粒创造更高的价格。据科慕公司称,其专有的350-450℃低温氯化技术可降低30%的能耗并提高产量。

印度新兴生产商正采用氯化法製程来缩小与西方供应商的品质差距,并应对日益严格的排放法规。在北美和欧洲,现有氯化法製程设施的扩建计划正在进行中,旨在无需新增投资即可将产量提高5%至15%。即使即使出现区域产能下降(例如Tronox公司位于Botlek的工厂关闭),这些扩建工程仍能维持供需平衡。因此,生产过程带来的成本差异仍是决定二氧化钛市场竞争力的核心因素。

本二氧化钛市场报告按等级(金红石型和锐钛矿型)、工艺(氯化法和硫酸法)、应用领域(油漆和涂料、塑料、造纸和纸浆、化妆品及其他应用)、终端用户行业(建筑、汽车和运输、包装及其他)以及地区(亚太地区、北美地区、欧洲及其他地区)对行业进行细分。市场预测以吨为单位。

区域分析

亚太地区占全球二氧化钛市场份额的34.70%,并保持最快的成长速度,预计2031年将以4.78%的复合年增长率成长。仅中国就占据了全球二氧化钛产能的大部分,其出口与国内建筑和基础设施建设需求的成长保持平衡。政府为提高颜料品质和减少硫酸盐製程废水排放而指南,正迫使生产商转向氯化物技术,从而推动二氧化钛生产向西方标准靠拢。

北美二氧化钛市场持续受到耐用消费品、航太涂料和包装薄膜的驱动。成熟的环境法规推动了氯化二氧化钛的生产,而企业ESG(环境、社会和治理)措施则推动了低碳颜料生产方法的研发。欧洲市场受到两大限制:二类致癌性标示制度和对中国进口产品征收的严格反倾销税。虽然这些措施推高了本地生产成本,但也促进了高端产品的创新,从而支撑了更高的价格。

中东和非洲地区在大型企划建筑计画的推动下,展现出新的发展潜力。波湾合作理事会(GCC)强制推行的「冷屋顶」政策以及旅游设施的增加,正在推动对高反射率涂料的需求。然而,国内二氧化钛产量仍微乎其微,导致该地区高度依赖进口,且极易受到运费波动的影响。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚太地区对水性建筑涂料的需求激增,推动了金红石型二氧化钛颜料的消费。

- 欧洲向轻量化、高光泽汽车塑胶转型

- 层压纸板包装在电子商务物流的成长

- 中东建筑市场中抗紫外线冷屋顶涂料的采用现状

- 印度氯化二氧化钛产能的区域分布

- 市场限制

- 由于欧盟将二氧化钛列为致癌性致癌物,导致标籤成本增加。

- 钛铁矿和金红石等原料价格的波动会影响利润率。

- 其他白色颜料的竞争压力

- 价值链分析

- 贸易分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按年级

- 金红石

- 锐钛矿

- 透过流程

- 氯化物

- 硫酸盐

- 透过使用

- 油漆和涂料

- 塑胶

- 纸浆和造纸

- 化妆品

- 其他用途(皮革、纺织品、橡胶)

- 按最终用户行业划分

- 建造

- 汽车和运输设备

- 包装

- 消费品

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Cinkarna Celje

- Evonik Industries AG

- Grupa Azoty SA

- Hangzhou Harmony Chemical Co.,Ltd

- INEOS

- ISHIHARA SANGYO KAISHA, LTD.

- Kemipex

- Kronos Worldwide, Inc.

- LB Group

- Precheza

- Shandong Jinhai Titanium Resources Technology Co., Ltd.

- TAYCA Co., Ltd.

- The Chemours Company

- Titanos

- Tronox Holdings Plc

- Venator Materials PLC

- Zhejiang TITAN Design& Engineering CO., Ltd

第七章 市场机会与未来展望

The Titanium Dioxide market is expected to grow from 360.16 kilotons in 2025 to 374.71 kilotons in 2026 and is forecast to reach 456.66 kilotons by 2031 at 4.04% CAGR over 2026-2031.

Rising demand from construction, packaging, automotive plastics, and cool-roof coatings offsets regulatory headwinds, especially Europe's Category 2 carcinogen labeling and anti-dumping duties on Chinese material. Asia-Pacific, anchored by China's supply base and India's localization push, is advancing at a 4.92% CAGR. Manufacturers are balancing cost pressures from volatile ilmenite and rutile feedstock with technology upgrades in the chloride route. Process optimization by players such as Chemours is boosting capacity by 15% without major capital outlays, while vertical integration by Tronox and others mitigates raw-material volatility. Regulatory divergence between the EU and other regions is spurring differentiated product portfolios and creating scope for regional arbitrage.

Global Titanium Dioxide Market Trends and Insights

Surge in Demand for Waterborne Architectural Coatings in Asia-Pacific

Escalating volatile-organic-compound regulations across China, India and Indonesia are accelerating substitution of solvent systems by waterborne paints, driving incremental rutile pigment offtake in the region. Regional coating lines are upgrading dispersion technology to achieve hiding power parity, underpinning continuous volume growth for the titanium dioxide market. Infrastructure stimulus programs in India and Indonesia compound demand, while localized chloride-route capacity secures supply resilience. Formulators emphasize lower odor and safer worksite conditions, bolstering acceptance among contractors. The shift is adding a structural tailwind despite feedstock price swings.

Shift Toward Lightweight, High-Gloss Automotive Plastics in Europe

Stringent EU fleet-average carbon-dioxide limits have placed lightweighting at the center of design strategies. Incorporating titanium dioxide into polypropylene and polycarbonate trim delivers high-gloss surfaces that rival coated metal panels yet weigh markedly less, achieving a 5-7% fuel-efficiency gain per 10% vehicle weight reduction. Premium OEMs adopt hydrophobic grades such as TIOXIDE TR48, which disperse at high processing temperatures without loss of brightness. The titanium dioxide market gains not only in volume but in value because these specialty grades command premium pricing and carry minimal regulatory substitution risk.

EU Classification of TiO2 as Suspected Carcinogen Raising Labeling Costs

European Regulation 2025/4 mandates cancer warnings on powder formulations containing more than or equal to 1% titanium dioxide. Coating, plastisol, and printing-ink suppliers face reformulation, new packaging artwork, and legal reviews, inflating compliance costs. Divergent rules in the United Kingdom and North America complicate global portfolio management, requiring dual labeling strategies. Short-run manufacturing batches raise unit costs, dampening discretionary demand in DIY channels. Although the European Court annulled the hazard label in 2022, the ruling was reversed in 2025 after scientific reassessment, reinforcing uncertainty for the titanium dioxide market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Laminated Paperboard Packaging for E-Commerce Logistics

- Uptake of UV-Resistant Cool-Roof Coatings in Middle-East Construction

- Volatility in Ilmenite/Rutile Feedstock Prices Impacting Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rutile commanded 77.60% of the titanium dioxide market in 2025, reflecting its higher refractive index (2.7) and superior weatherability. This supremacy is entrenched in outdoor architectural coatings, automotive topcoats, and polymer masterbatches where long-term gloss retention is critical. Dual-function grades integrating photocatalytic traits are unlocking new self-cleaning surface opportunities, further entrenching the rutile's lead.

Anatase, accounting for the demand balance, is advancing at a faster 4.32% CAGR thanks to niche growth in pharmaceutical excipients and photocatalytic building materials. Surface-modified anatase grades extend shelf life in food-contact papers and offer distinct bluish undertones valued in premium office papers.

The sulfate route delivered 64.30% of the titanium dioxide market size in 2025 by leveraging lower-grade ilmenite and smaller capital footprints. Nevertheless, chloride-based capacity is expanding at 4.53% CAGR as regulators intensify scrutiny of acidic sulfate waste streams. Chloride plants use high-TiO2 slag or natural rutile and generate primarily rutile pigment with lower trace impurities, enabling higher pricing in premium coatings and masterbatch segments. Chemours reports that proprietary low-temperature chlorination at 350-450 °C can reduce energy use by 30% and improve yield.

Emerging producers in India are adopting chloride technology to achieve quality parity with Western suppliers and to hedge against evolving effluent norms. Incremental debottlenecking projects across North America and Europe aim to squeeze 5-15% extra output from existing chloride assets without greenfield spending, keeping supply balanced despite regional capacity closures such as Tronox's Botlek facility. Process-driven cost differentials, therefore, remain central to titanium dioxide market competitiveness.

The Titanium Dioxide Market Report Segments the Industry by Grade (Rutile and Anatase), Process (Chloride and Sulfate) Application (Paints and Coatings, Plastics, Paper and Pulp, Cosmetics and Other Applications), End-User Industry (Construction, Automotive and Transportation, Packaging, and More) and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons)

Geography Analysis

Asia-Pacific controls 34.70% of the titanium dioxide market and delivers the fastest 4.78% CAGR through 2031. China alone houses a major portion of global TiO2 capacity, balancing exports with rising domestic architectural and infrastructure demand. Government directives to upgrade pigment quality and curb sulfate-process effluent are pushing producers toward chloride technology, replicating Western standards.

North America's titanium dioxide market remains driven by durable goods, aerospace coatings, and packaging films. Mature environmental regulations favor chloride output, and corporate ESG commitments spur research and development into lower-carbon pigment pathways. Europe's market is shaped by dual constraints: Category 2 carcinogen labeling and definitive anti-dumping duties on Chinese imports. These measures elevate local production costs but also encourage premium-grade innovation to justify higher price points.

The Middle-East and Africa present emergent potential propelled by construction megaprojects. Cool-roof mandates in the Gulf Cooperation Council and rising tourism facilities spur high-albedo coating uptake. Domestic TiO2 production remains negligible, driving import dependency and exposure to freight fluctuations.

- Cinkarna Celje

- Evonik Industries AG

- Grupa Azoty S.A.

- Hangzhou Harmony Chemical Co.,Ltd

- INEOS

- ISHIHARA SANGYO KAISHA, LTD.

- Kemipex

- Kronos Worldwide, Inc.

- LB Group

- Precheza

- Shandong Jinhai Titanium Resources Technology Co., Ltd.

- TAYCA Co., Ltd.

- The Chemours Company

- Titanos

- Tronox Holdings Plc

- Venator Materials PLC

- Zhejiang TITAN Design& Engineering CO., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Demand for Waterborne Architectural Coatings in Asia-Pacific Boosting Rutile TiO2 Pigment Consumption

- 4.2.2 Shift Toward Lightweight, High-Gloss Automotive Plastics in Europe

- 4.2.3 Growth of Laminated Paperboard Packaging for E-Commerce Logistics

- 4.2.4 Uptake of UV-Resistant Cool-Roof Coatings in Middle-East Construction

- 4.2.5 Localization of Chloride-Route TiO2 Capacity in India

- 4.3 Market Restraints

- 4.3.1 EU Classification of TiO2 as Suspected Carcinogen Raising Labeling Costs

- 4.3.2 Volatility in Ilmenite/Rutile Feedstock Prices Impacting Margins

- 4.3.3 Competitive Pressure from Alternative White Pigments

- 4.4 Value Chain Analysis

- 4.5 Trade Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 Rutile

- 5.1.2 Anatase

- 5.2 By Process

- 5.2.1 Chloride

- 5.2.2 Sulfate

- 5.3 By Application

- 5.3.1 Paints and Coatings

- 5.3.2 Plastics

- 5.3.3 Paper and Pulp

- 5.3.4 Cosmetics

- 5.3.5 Other Applications (Leather, Textiles, Rubber)

- 5.4 By End-user Industry

- 5.4.1 Construction

- 5.4.2 Automotive and Transportation

- 5.4.3 Packaging

- 5.4.4 Consumer Goods

- 5.4.5 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Nordics

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cinkarna Celje

- 6.4.2 Evonik Industries AG

- 6.4.3 Grupa Azoty S.A.

- 6.4.4 Hangzhou Harmony Chemical Co.,Ltd

- 6.4.5 INEOS

- 6.4.6 ISHIHARA SANGYO KAISHA, LTD.

- 6.4.7 Kemipex

- 6.4.8 Kronos Worldwide, Inc.

- 6.4.9 LB Group

- 6.4.10 Precheza

- 6.4.11 Shandong Jinhai Titanium Resources Technology Co., Ltd.

- 6.4.12 TAYCA Co., Ltd.

- 6.4.13 The Chemours Company

- 6.4.14 Titanos

- 6.4.15 Tronox Holdings Plc

- 6.4.16 Venator Materials PLC

- 6.4.17 Zhejiang TITAN Design& Engineering CO., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increased Use of Ultrafine Titanium Dioxide in Cosmetics and Cool-Roofing

超细二氧化钛粉末市场:按表面处理、等级、应用和最终用途产业划分,全球预测(2026-2032年)锂铝钛磷酸盐电解液市场(按电池类型、应用、最终用途、形态、生产过程、纯度、电导率范围和动作温度划分),全球预测,2026-2032年

超细二氧化钛粉末市场:按表面处理、等级、应用和最终用途产业划分,全球预测(2026-2032年)锂铝钛磷酸盐电解液市场(按电池类型、应用、最终用途、形态、生产过程、纯度、电导率范围和动作温度划分),全球预测,2026-2032年 2026-2034年全球二氧化钛市场规模、份额、趋势和成长分析报告全球二硼化钛市场规模、份额、趋势和成长分析报告(2026-2034年)全球氟磷酸钛市场规模、份额、趋势和成长分析报告(2026-2034)

2026-2034年全球二氧化钛市场规模、份额、趋势和成长分析报告全球二硼化钛市场规模、份额、趋势和成长分析报告(2026-2034年)全球氟磷酸钛市场规模、份额、趋势和成长分析报告(2026-2034) 二氧化钛市场规模、份额和趋势分析报告:按等级、载体生产製程、最终用途、地区和细分市场预测(2026-2033 年)全球二氧化钛市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的分析、未来预测(2026-2034)

二氧化钛市场规模、份额和趋势分析报告:按等级、载体生产製程、最终用途、地区和细分市场预测(2026-2033 年)全球二氧化钛市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的分析、未来预测(2026-2034) 钛原料生产商成本比较研究 (FCS)

钛原料生产商成本比较研究 (FCS) 二氧化钛市场机会、成长要素、产业趋势分析及预测(2026年至2035年)金红石市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2033 年)

二氧化钛市场机会、成长要素、产业趋势分析及预测(2026年至2035年)金红石市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2033 年)