|

市场调查报告书

商品编码

1939694

越南铝业:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Vietnam Aluminum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

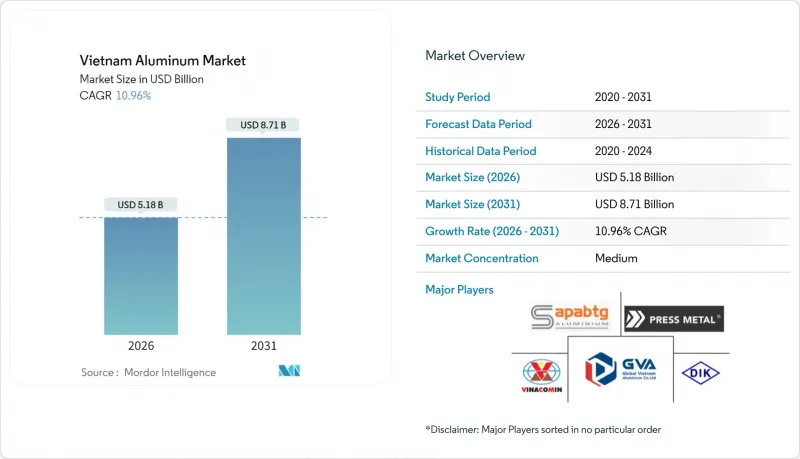

预计越南铝市场规模将从 2025 年的 46.7 亿美元成长到 2026 年的 51.8 亿美元,到 2031 年将达到 87.1 亿美元,2026 年至 2031 年的复合年增长率为 10.96%。

这一上升趋势,加上丰富的矾土蕴藏量、新增氧化铝产能以及交通运输和建筑行业的需求,使越南铝市场成为亚洲成长最快的价值链之一。电动车产量的成长、绿建筑法规的推行以及包装循环利用目标的实现,正在推动结构性需求的成长,而上游58亿吨矾土蕴藏量的稳定供应则为长期供应提供了保障。政府第866号决议批准到2030年建造8座加工厂和19个探勘计划,进一步促进了市场成长,儘管目前的运转率平均仍高达70%,显示仍有发展空间。

越南铝市场趋势及展望

汽车产业轻量化发展的趋势

越南拥有858家通过IATF 16949认证的供应商,这推动了汽车铝材的需求成长,并将越南纳入区域汽车平臺。在电动车生产中,电池机壳和温度控管系统所需的铝材用量比传统车型高出约30%,越南的目标是到2030年实现都市区车辆50%的电动化。儘管在地采购政策鼓励零件外包,但商用车辆车队正在采用铝製零件,以最大限度地提高负载容量并满足排放标准。世界银行估计,到2050年,向电动车的转型将创造650万个製造业就业岗位,这将支撑铸造、挤压和扁钢供应链的金属需求。随着整车製造商扩大产能,越南铝市场将受益于铝坯和铝锭需求的成长,从而吸引新的二次冶炼厂进入市场。

公共和绿色建筑建设快速成长

2024年,公共支出300亿美元,这将在短期内刺激对帷幕墙、屋顶材料和结构型材的需求。 2024年第一季,获得绿色认证的建筑数量达到430座,其中EDGE和LEED认证占比高达75.69%。铝材因其可回收性和良好的热效率而被广泛应用。到2030年,政府将累计1,350亿美元用于电力发展第八期规划,将推动高压结构和太阳能板框架对铝材的需求。胡志明市耗资115亿美元的高速公路规划和12亿美元的交通基础设施改善项目也将促进型材消费量的成长。

电力价格上涨和碳价格风险

稳定且低成本的电力对铝提炼至关重要,但越南工业平均电价预计将在2024年上涨,这将挤压利润空间。一些工厂的运转率被限制在30%至40%。欧盟的碳边境调节机制(CBAM)可能影响价值3.0766亿美元的铝出口,导致出货量减少4%,相当于每年损失1,200万美元的收入。第八个电力发展计画要求实施市场定价,除非可再生能源得到保障,否则将对电解计划带来压力。出口商将不得不降低碳排放强度或支付CBAM费用,这将削弱越南在铝市场的成本优势。

细分市场分析

到2025年,挤压件将占越南铝材市场的39.42%,主要得益于对窗框、帷幕墙和汽车型材的持续需求。预计到2027年,基础设施投资将达到958亿美元,这将使挤压厂保持较高的运转率。同时,严格的LEED和EDGE标准也认可采用阳极氧化和隔热系统的产品。为因应美国的反倾销令,出口合作伙伴正在改善製程流程,从而巩固其品质领先地位。预计到2031年,铸件市场将以13.62%的复合年增长率成长,因为汽车製造商正在寻求在本地生产用于电动车平台的轻量化零件。

IATF 16949认证仍是OEM供货的先决条件,也是越南作为东协第二大认证中心地位的基础。像美华精密工业这样的製造商,60%的销售额来自国内,其余部分出口到日本、美国和澳大利亚,这反映了越南在中游加工领域日益增强的竞争力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 汽车产业轻量化发展的趋势

- 公共和绿色建筑建设快速成长

- 包装需求復苏(食品、饮料和製药业)

- 国内矾土及氧化铝计划扩张

- 电动车和电池外壳的快速本地化

- 市场限制

- 面临高电价和碳定价风险

- 低成本的钢材、塑胶和复合材料替代品

- 对初级金属和钢坯的进口依赖

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 产业间竞争

第五章 市场规模与成长预测

- 透过加工方法

- 铸件

- 挤出成型

- 锻件

- 扁钢产品

- 颜料和粉末

- 按最终用户行业划分

- 车

- 航太与国防

- 建筑/施工

- 电气和电子行业

- 包装

- 工业的

- 其他终端用户产业

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Alcoa Corporation

- Daiki Aluminium Industry Co. Ltd

- Emirates Global Aluminium PJSC

- GARMCO

- Global Vietnam Aluminum Co., Ltd(GVA)

- Kobe Steel Ltd

- Norsk Hydro ASA

- Press Metal

- RusAL

- Sapa Ben Thanh Aluminium Profiles Co., Ltd.(Sapa BTG)

- Vietnam Coal and Mineral Industries Group

第七章 市场机会与未来展望

The Vietnam Aluminum Market is expected to grow from USD 4.67 billion in 2025 to USD 5.18 billion in 2026 and is forecast to reach USD 8.71 billion by 2031 at 10.96% CAGR over 2026-2031.

This uptrend positions the Vietnam aluminum market among the fastest-growing value chains in Asia as abundant bauxite reserves, new alumina capacity, and demand from mobility and construction converge. Rising EV production, green-building mandates, and packaging circularity targets foster structural demand, while upstream security from 5.8 billion tonnes of bauxite supports long-term supply. Government Decision 866 authorizing eight processing facilities plus 19 exploration projects through 2030 further underpins growth, although capacity utilization still averages 70%, highlighting operational headroom.

Vietnam Aluminum Market Trends and Insights

Auto-sector Lightweighting Push

Automotive aluminum demand is reinforced by 858 IATF 16949-certified suppliers that integrate Vietnam into regional vehicle platforms. EV production uses nearly 30% more aluminum per unit than conventional models for battery enclosures and thermal systems, and Vietnam targets 50% electric urban vehicles by 2030. Local content policies fuel component outsourcing, while commercial fleets adopt aluminum parts to maximize payload and comply with emission norms. The World Bank estimates the EV transition could generate 6.5 million manufacturing jobs by 2050, a scenario that sustains metal demand across casting, extrusion, and flat-rolled supply chains. As OEMs expand capacity, the Vietnam aluminum market benefits from rising billet and ingot off-take, incentivizing new secondary smelters.

Booming Public and Green-Building Construction

Public spending of USD 30 billion in 2024 on transport and power facilities injected near-term demand for curtain walls, roofing, and structural extrusions. Green-certified buildings rose to 430 in Q1 2024, with EDGE and LEED accounting for 75.69% of certifications, favoring aluminum for its recyclability and thermal efficiency. Power Development Plan VIII earmarks USD 135 billion through 2030, driving aluminum demand for high-voltage structures and solar frames. Ho Chi Minh City's USD 11.5 billion highway program and USD 1.2 billion of transport upgrades boost extruded profile consumption.

High Electricity Tariffs and Carbon-Pricing Exposure

Aluminum smelting requires constant low-cost power, yet Vietnam's average industrial tariff rose in 2024, compressing margins and limiting capacity use to 30-40% in some plants. The EU's Carbon Border Adjustment Mechanism affects USD 307.66 million of aluminum exports and could trim shipments by 4%, translating into USD 12 million revenue loss per year. Power Development Plan VIII calls for market-based pricing, pressuring electrolysis projects unless they secure renewables. Exporters must cut carbon intensity or pay CBAM fees that erode the Vietnam aluminum market's cost advantage.

Other drivers and restraints analyzed in the detailed report include:

- Rebound in Packaging Demand (Food-Drink and Pharmaceuticals)

- Expansion of Domestic Bauxite and Alumina Projects

- Import Dependence for Primary Metal and Billets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Extrusions commanded 39.42% of the Vietnam aluminum market in 2025 on the back of sustained demand for window frames, curtain walls, and vehicle profiles. Rising infrastructure outlays valued at USD 95.8 billion through 2027 keep extrusion mills running at high throughput, while strict LEED and EDGE criteria reward anodized and thermally broken systems. Compliance with U.S. antidumping orders incentivizes process upgrades among cooperative exporters, reinforcing quality leadership. Castings are projected to grow at a 13.62% CAGR to 2031 as automakers localize lightweight components for EV platforms.

Certification under IATF 16949 remains a prerequisite for OEM supply and underpins Vietnam's ranking as ASEAN's second-largest certified base. Producers like Mien Hua Precision generate 60% of sales domestically and export the remainder to Japan, the U.S., and Australia, reflecting the country's expanding mid-stream competitiveness.

The Vietnam Aluminum Market Report is Segmented by Processing Type (Castings, Extrusions, Forgings, Flat Rolled Products, and Pigments and Powders) and End-User Industry (Automotive, Aerospace and Defense, Building and Construction, Electrical and Electronics, Packaging, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alcoa Corporation

- Daiki Aluminium Industry Co. Ltd

- Emirates Global Aluminium PJSC

- GARMCO

- Global Vietnam Aluminum Co., Ltd (GVA)

- Kobe Steel Ltd

- Norsk Hydro ASA

- Press Metal

- RusAL

- Sapa Ben Thanh Aluminium Profiles Co., Ltd. (Sapa BTG)

- Vietnam Coal and Mineral Industries Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Auto-sector lightweighting push

- 4.2.2 Booming public and green-building construction

- 4.2.3 Rebound in packaging demand (food-drink and pharmaceuticals)

- 4.2.4 Expansion of domestic bauxite and alumina projects

- 4.2.5 Rapid EV/battery-housing localisation

- 4.3 Market Restraints

- 4.3.1 High electricity tariffs and carbon-pricing exposure

- 4.3.2 Cheap steel/plastics and composite substitutes

- 4.3.3 Import dependence for primary metal and billets

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Processing Type

- 5.1.1 Castings

- 5.1.2 Extrusions

- 5.1.3 Forgings

- 5.1.4 Flat Rolled Products

- 5.1.5 Pigments and Powders

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Packaging

- 5.2.6 Industrial

- 5.2.7 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alcoa Corporation

- 6.4.2 Daiki Aluminium Industry Co. Ltd

- 6.4.3 Emirates Global Aluminium PJSC

- 6.4.4 GARMCO

- 6.4.5 Global Vietnam Aluminum Co., Ltd (GVA)

- 6.4.6 Kobe Steel Ltd

- 6.4.7 Norsk Hydro ASA

- 6.4.8 Press Metal

- 6.4.9 RusAL

- 6.4.10 Sapa Ben Thanh Aluminium Profiles Co., Ltd. (Sapa BTG)

- 6.4.11 Vietnam Coal and Mineral Industries Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Aluminium Recycling and Circular-Economy Plays

- 7.3 High-end EV and Battery-pack Components

铝系统市场:依製造流程、形状、产品类型和应用划分-2026-2032年全球市场预测铝市场:按类型、形状、原料、等级、加工方法和应用划分-2026-2032年全球市场预测铝导体市场:依导体类型、绝缘方式、额定电压和应用划分-2026-2032年全球市场预测磷酸铝市场:依形态、等级、应用和分销管道划分-2026-2032年全球市场预测乙酰丙酮铝市场:依等级、形态、应用、终端用户产业和分销管道划分-2026-2032年全球预测二氧化碳铝瓶市场:依容量、瓶型、压力、最终用途及通路划分,全球预测(2026-2032年)

铝系统市场:依製造流程、形状、产品类型和应用划分-2026-2032年全球市场预测铝市场:按类型、形状、原料、等级、加工方法和应用划分-2026-2032年全球市场预测铝导体市场:依导体类型、绝缘方式、额定电压和应用划分-2026-2032年全球市场预测磷酸铝市场:依形态、等级、应用和分销管道划分-2026-2032年全球市场预测乙酰丙酮铝市场:依等级、形态、应用、终端用户产业和分销管道划分-2026-2032年全球预测二氧化碳铝瓶市场:依容量、瓶型、压力、最终用途及通路划分,全球预测(2026-2032年) 多金属铝夹芯板市场报告:按金属、发泡材、应用和地区划分(2026-2034 年)

多金属铝夹芯板市场报告:按金属、发泡材、应用和地区划分(2026-2034 年) 铝製炊具市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

铝製炊具市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 铝市场分析及预测(至2035年):类型、产品类型、应用、形式、材质类型、技术、最终用户、组件、功能

铝市场分析及预测(至2035年):类型、产品类型、应用、形式、材质类型、技术、最终用户、组件、功能 铝:市占率分析、产业趋势与统计、成长预测(2026-2031)

铝:市占率分析、产业趋势与统计、成长预测(2026-2031)