|

市场调查报告书

商品编码

1939712

人工智慧即服务 (AIaaS) 市场:市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)Artificial Intelligence As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

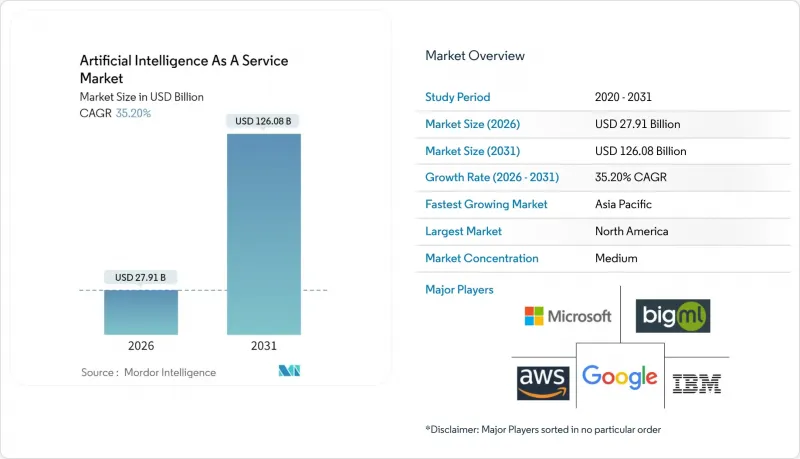

预计到 2025 年,人工智慧即服务 (AIaaS) 市场价值将达到 206.4 亿美元,从 2026 年的 279.1 亿美元成长到 2031 年的 1,260.8 亿美元。

预测期(2026-2031 年)的复合年增长率预计为 35.20%。

这项成长的驱动力在于,企业正迅速将生成式人工智慧API嵌入到面向客户和后勤部门的系统中,从而加速从先导计画向生产工作负载的过渡。订阅定价模式降低了中小企业的进入门槛,而客製化的人工智慧加速器则可将推理成本降低高达80%,帮助服务供应商提升利润率。在日本650亿美元的人工智慧计画等政府经济刺激措施的推动下,儘管短期内面临电力短缺,超大规模资料中心的扩张仍在持续提升运算能力。这些因素共同推动着人工智慧即服务(AIaaS)市场走向跨产业的广泛应用。

全球人工智慧即服务 (AIaaS) 市场趋势与洞察

对预测性和指示性分析的需求日益增长

如今,企业更倾向于主动分析而非被动分析。采用人工智慧驱动分析的製造商透过优化供应链,实现了61%的收入溢价,并降低了15%的物流成本。医疗系统透过自动化放射科工作流程,实现了五年内451%的投资报酬率。银行借助人工智慧预测技术提高了诈欺侦测的准确率,并预计到2028年将额外获得1,700亿美元的利润。即时资料撷取与自主人工智慧系统的结合正在推动这一发展势头,使预测分析成为人工智慧即服务(AIaaS)市场的核心成长引擎。

订阅式人工智慧工具可降低中小企业的整体拥有成本

低门槛定价模式打破了传统的进入障碍。全球中小企业对生成式人工智慧工具的采用率已达18%。在美国,员工人数在4人或以下的公司中,人工智慧的使用率在短短一年内就从4.6%成长到5.8%。零售商正在展现实际成效:Target在400家门市部署了人工智慧员工辅助工具,在无需大规模支出的情况下提高了生产力。透过将人工智慧从资本支出转变为营运支出,订阅平台正在向微型企业领域拓展人工智慧即服务(AIaaS)市场。

云端运算成本飙升

人工智慧工作负载正给基础设施经济带来巨大压力。到2030年,资料中心可能占美国电力消耗量的9%。预计到2025年,人工智慧的能源需求将超过比特币挖矿,达到23吉瓦。目前,财富2000强企业中有47%选择在企业内部开发生成式人工智慧,以控制不可控的成本。不断上涨的电价和半导体供应紧张预计将在短期内降低人工智慧即服务(AIaaS)市场的经济承受能力,并限制其成长。

细分市场分析

2025年,公共云端产品将维持77.35%的市场份额,巩固人工智慧即服务(AIaaS)市场对超大规模基础设施的依赖。然而,在董事会严格的成本控制要求和监管机构保护资料居住的压力下,混合云端正在崛起,成为明显的成长引擎,预计2026年至2031年将以31.05%的复合年增长率成长。许多财富2000强企业目前透过在云端训练大型模型,同时在本地运行推理处理,来平衡规模和自主性。

混合部署正在改变采购模式。医疗机构正在采用云端爆发架构,将可识别的医疗资料保留在本地伺服器上,同时利用弹性运算进行模型训练,从而满足 HIPAA 法规要求并保持价值实现速度。製造业也正在效仿类似的模式,为对延迟敏感的视觉任务分配边缘节点,并将繁重的分析处理转移到区域云区。合规性和预算确定性的双重考量,使得混合模式继续成为人工智慧即服务 (AIaaS) 市场前景的核心。

机器学习平台将占到2025年总收入的41.30%,而人工智慧基础设施服务将以42.9%的复合年增长率更快成长。这项转变使得运算优化丛集和网路架构成为不断扩展的AIaaS市场骨干工作负载的核心。客製化晶片的普及也推动了这一趋势。谷歌的TPU和亚马逊的Trainium在性价比方面实现了数倍提升,因此客户更倾向于选择提供此类晶片的供应商。

软体层也在同步演进。託管分发包将优化的核心与编配工具结合,以促进多重云端扩展。供应商正在整合自癒功能、自动修补程式和效能仪表板,以减轻运维负担。这些改进共同加强了底层基础设施与开发人员生产力之间的联繫,巩固了人工智慧即服务 (AIaaS) 市场这一细分领域的收入成长动能。

人工智慧即服务 (AIaaS) 市场按部署模式(公共云端、私有云端、混合云端)、服务类型(机器学习平台服务、认知服务(自然语言处理、电脑视觉、语音)、其他)、组织规模(中小企业、其他)、最终用户行业(银行、金融服务和保险 (BFSI)、其他)以及地区进行细分。以上所有细分市场的规模和预测均以美元计价。

区域分析

北美拥有庞大的超大规模资料安装基础和深厚的Start-Ups生态系统,预计2025年将占全球营收的37.40%。云端运算巨头承诺在2025年新增超过2,500亿美元的容量,但电网限制令人担忧,因为到2030年,美国资料中心的电力消耗量可能达到全国电力供应的9%。美国联邦贸易委员会(FTC)对云端运算与人工智慧合作的调查也可能导致竞争格局的重新调整。

亚太地区正经历最快的成长,复合年增长率高达26.55%。日本已为人工智慧和半导体领域拨款650亿美元,Softbank Corporation也已投资9.6亿美元用于生成式人工智慧基础建设。中国的阿里巴巴已为云端模型服务投入3800亿元人民币,位元组跳动的火山引擎处理了中国近一半的公共模型呼叫。一项企业调查发现,亚太地区54%的企业目前的目标是长期实现人工智慧的商业化,这显示人工智慧已超越试点阶段。

在拟议的人工智慧监管框架下,欧洲正经历稳定成长,在严格监管与创新之间寻求平衡。中东和非洲地区正在推动国家主导的人工智慧战略:阿联酋预计到2030年,该产业的市场规模将达到463.3亿美元;微软正在G42国家投资15亿美元。沙乌地阿拉伯设立的1,000亿美元人工智慧基金展现了该地区的雄心壮志,海湾合作委员会(GCC)成员国中75%的企业已部署生成式模型,高于全球平均。便利的能源供应和积极的政策框架使该地区成为连接欧洲、非洲和南亚的桥樑市场,在人工智慧即服务(AIaaS)市场的发展中发挥关键作用。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对预测性和指示性分析的需求日益增长

- 订阅式人工智慧工具可降低中小企业的整体拥有成本 (TCO)。

- 客製化AI加速器(TPU/Trainium)可显着降低推理成本

- 受监管产业的垂直整合型AIaaS套餐

- 内建于低程式码平台中的生成式人工智慧 API

- 市场限制

- 云端运算成本飙升

- MLOps人才持续短缺

- 加强对模型来源的监管审查

- 价值/价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按部署模式

- 公共云端

- 私有云端

- 混合云端

- 按服务类型

- 机器学习平台服务

- 认知服务(自然语言处理、电脑视觉、语音辨识)

- AI基础设施服务(GPU/TPU)

- 託管和专业人工智慧服务

- 按公司规模

- 小型企业

- 大公司

- 按最终用户行业划分

- BFSI

- 零售与电子商务

- 医疗保健和生命科学

- 资讯科技和电信

- 製造业

- 能源与公共产业

- 其他(媒体、农业、公共)

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 东南亚

- 中东和非洲

- 中东

- 海湾合作委员会(沙乌地阿拉伯、阿联酋、卡达)

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amazon Web Services(AWS)

- Microsoft Corporation

- Google LLC(Google Cloud)

- IBM Corporation

- Oracle Corporation

- Salesforce Inc.

- SAS Institute Inc.

- H2O.ai Inc.

- DataRobot Inc.

- Dataiku SAS

- BigML Inc.

- OpenAI LP

- Anthropic PBC

- C3.ai Inc.

- NVIDIA Corp.(DGX Cloud)

- Alibaba Cloud

- Tencent Cloud

- Baidu AI Cloud

- Huawei Cloud

- Craft AI

第七章 市场机会与未来展望

The Artificial Intelligence As A Service Market was valued at USD 20.64 billion in 2025 and estimated to grow from USD 27.91 billion in 2026 to reach USD 126.08 billion by 2031, at a CAGR of 35.20% during the forecast period (2026-2031).

Rapid migration from pilot projects to production workloads fuels this rise as enterprises embed generative-AI APIs in customer-facing and back-office systems. Subscription pricing lowers entry costs for small firms, while custom AI accelerators cut inference expenses by up to 80%, widening margins for providers. Government stimulus packages, such as Japan's USD 65 billion AI plan, add momentum, and hyperscale data-center build-outs keep compute capacity expanding despite near-term power constraints. Together, these forces push the Artificial Intelligence as a Service market toward broad, cross-industry penetration.

Global Artificial Intelligence As A Service Market Trends and Insights

Growing Demand for Predictive & Prescriptive Analytics

Enterprises now prize foresight over hindsight. Manufacturers using AI-driven analytics posted 61% revenue premiums, while supply-chain optimization shaved 15% off logistics costs. Healthcare systems gained 451% ROI over five years by automating radiology workflows. Banks boosted fraud-detection accuracy and see USD 170 billion additional profits by 2028 through AI forecasting. Real-time data ingestion plus agentic AI systems sustain this momentum, positioning predictive analytics as a core growth engine for the Artificial Intelligence as a Service market.

Subscription-Based AI Tools Lowering TCO for SMEs

Low-commitment pricing dismantles historic entry barriers. Global SME adoption of generative-AI tools reached 18%. In the United States, AI usage among firms with four workers rose from 4.6% to 5.8% in a single year. Retailers illustrate practical returns: Target deployed AI employee-assistance tools across 400 stores to raise productivity without large capital outlays. By turning AI from capex to opex, subscription platforms broaden the Artificial Intelligence as a Service market across micro-enterprise segments.

Escalating Cloud-Compute Cost Inflation

AI workloads strain infrastructure economics. Data centers may draw 9% of the United States' electricity by 2030. AI energy needs are set to top Bitcoin mining in 2025, reaching 23 GW. Forty-seven percent of Fortune 2000 firms now develop generative AI on-premises to tame runaway bills. Rising power prices plus tight chip supply lower near-term affordability and clip growth in the Artificial Intelligence as a Service market.

Other drivers and restraints analyzed in the detailed report include:

- Custom AI Accelerators Slashing Inference Cost

- Verticalised AIaaS Bundles for Regulated Sectors

- Persistent MLOps Talent Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public-cloud delivery retained 77.35% share in 2025, ensuring the Artificial Intelligence as a Service market remains anchored to hyperscale infrastructure. Hybrid cloud, however, is the clear growth engine, registering a 31.05% CAGR for 2026-2031 as boards demand tighter cost control and regulators press for data residency safeguards. Many Fortune 2000 firms now train large models in the cloud yet run inference on-premises, balancing scale with sovereignty.

Hybrid uptake redirects procurement. Hospitals adopt cloud-burst architectures to keep personally identifiable health data within local servers while exploiting elastic compute for model training, meeting HIPAA rules without losing time-to-value. Manufacturers mirror this pattern, reserving edge nodes for latency-sensitive vision tasks while pushing bulk analytics to regional cloud zones. The twin priorities of compliance and budget certainty thus keep hybrid models central to the Artificial Intelligence as a Service market outlook.

Machine-learning platforms supplied 41.30% of 2025 revenue, but AI infrastructure services are growing faster at 42.9% CAGR. This shift places compute-optimized clusters and networking fabrics at the heart of the Artificial Intelligence as a Service market size expansion for backbone workloads. Custom chip adoption underpins the trend: Google's TPUs and Amazon's Trainium deliver multi-fold price-performance gains, prompting clients to favor providers offering such silicon.

Software layers evolve in lockstep. Managed distribution bundles now pair optimized kernels with orchestration tooling to ease multi-cloud scaling. Vendors embed self-healing functions, automated patching, and performance dashboards to shrink operational toil. Together, these enhancements tighten the nexus between raw infrastructure and developer productivity, reinforcing the revenue trajectory in this segment of the Artificial Intelligence as a Service market.

The Artificial Intelligence As A Service Market is Segmented by Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Service Type (Machine-Learning Platform Services, Cognitive Services (NLP, CV, Speech), and More), Organization Size (Small and Medium Enterprises, and More), End-User Industry (BFSI, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

Geography Analysis

North America held 37.40% of global revenue in 2025, buoyed by an installed base of hyperscale data centers and a deep startup ecosystem. Cloud majors pledged more than USD 250 billion in fresh capacity during 2025, yet grid constraints loom as US data-center power draw may hit 9% of national supply by 2030. FTC probes into cloud-AI pacts could also recalibrate competitive boundaries.

Asia-Pacific charts the fastest ascent with a 26.55% CAGR. Japan earmarked USD 65 billion for AI and chips, and SoftBank invested USD 960 million in a generative-AI backbone. China's Alibaba allocated 380 billion yuan to cloud model services, while ByteDance's Volcano Engine processed nearly half of the country's public model calls. Corporate surveys show 54% of APAC firms now target long-term AI payouts, signalling depth beyond pilot activity.

Europe grows steadily, balancing innovation with strict oversight under draft AI regulations. The Middle East and Africa ride sovereign-AI strategies: the UAE expects USD 46.33 billion in sector value by 2030 as Microsoft injects USD 1.5 billion into G42. Saudi Arabia's USD 100 billion AI fund underscores regional ambition, and 75% of GCC enterprises deploy generative models, eclipsing global averages. Access to affordable energy and proactive policy frameworks position the region as a bridge market linking Europe, Africa, and South-Asia for Artificial Intelligence as a Service market rollouts.

- Amazon Web Services (AWS)

- Microsoft Corporation

- Google LLC (Google Cloud)

- IBM Corporation

- Oracle Corporation

- Salesforce Inc.

- SAS Institute Inc.

- H2O.ai Inc.

- DataRobot Inc.

- Dataiku SAS

- BigML Inc.

- OpenAI LP

- Anthropic PBC

- C3.ai Inc.

- NVIDIA Corp. (DGX Cloud)

- Alibaba Cloud

- Tencent Cloud

- Baidu AI Cloud

- Huawei Cloud

- Craft AI

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study AssumptionsandMarket Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for predictiveandprescriptive analytics (mainstream)

- 4.2.2 Subscription-based AI tools lowering TCO for SMEs (mainstream)

- 4.2.3 Custom AI accelerators (TPU/Trainium) slashing inference cost (under-radar)

- 4.2.4 Verticalised AIaaS bundles for regulated sectors (under-radar)

- 4.2.5 Generative-AI APIs embedded in low-code platforms (mainstream)

- 4.3 Market Restraints

- 4.3.1 Escalating cloud-compute cost inflation (mainstream)

- 4.3.2 Persistent MLOps talent shortage (under-radar)

- 4.3.3 Heightened regulatory scrutiny on model provenance (mainstream)

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Service Type

- 5.2.1 Machine-Learning Platform Services

- 5.2.2 Cognitive Services (NLP, CV, Speech)

- 5.2.3 AI Infrastructure Services (GPU/TPU)

- 5.2.4 ManagedandProfessional AI Services

- 5.3 By Organisation Size

- 5.3.1 SmallandMedium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 RetailandE-commerce

- 5.4.3 HealthcareandLife Sciences

- 5.4.4 ITandTelecom

- 5.4.5 Manufacturing

- 5.4.6 EnergyandUtilities

- 5.4.7 Others (Media, Agriculture, Public)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 AustraliaandNew Zealand

- 5.5.4.6 South-East Asia

- 5.5.5 Middle EastandAfrica

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC (Saudi Arabia, UAE, Qatar)

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, ProductsandServices, and Recent Developments)

- 6.4.1 Amazon Web Services (AWS)

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC (Google Cloud)

- 6.4.4 IBM Corporation

- 6.4.5 Oracle Corporation

- 6.4.6 Salesforce Inc.

- 6.4.7 SAS Institute Inc.

- 6.4.8 H2O.ai Inc.

- 6.4.9 DataRobot Inc.

- 6.4.10 Dataiku SAS

- 6.4.11 BigML Inc.

- 6.4.12 OpenAI LP

- 6.4.13 Anthropic PBC

- 6.4.14 C3.ai Inc.

- 6.4.15 NVIDIA Corp. (DGX Cloud)

- 6.4.16 Alibaba Cloud

- 6.4.17 Tencent Cloud

- 6.4.18 Baidu AI Cloud

- 6.4.19 Huawei Cloud

- 6.4.20 Craft AI

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-spaceandUnmet-need Assessment

创作者经济分析:2026年全球人工智慧市场报告

创作者经济分析:2026年全球人工智慧市场报告 全球人工智慧服务(AIaaS)市场规模、份额、趋势和成长分析报告(2026-2034年)人工智慧即服务 (AaaS) 市场规模、份额、成长和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测基于代理的人工智慧在服务自动化中的应用,可提高效率并实现个人化

全球人工智慧服务(AIaaS)市场规模、份额、趋势和成长分析报告(2026-2034年)人工智慧即服务 (AaaS) 市场规模、份额、成长和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测基于代理的人工智慧在服务自动化中的应用,可提高效率并实现个人化 人工智慧即服务 (AIaaS) 市场 - 全球产业规模、份额、趋势、机会及预测(按技术、组织规模、服务类型、云端类型、垂直产业、地区和竞争格局划分),2021-2031 年

人工智慧即服务 (AIaaS) 市场 - 全球产业规模、份额、趋势、机会及预测(按技术、组织规模、服务类型、云端类型、垂直产业、地区和竞争格局划分),2021-2031 年 日本人工智慧即服务 (AIaaS) 市场报告:按技术、组织规模、产业和地区划分 2026-2034 年

日本人工智慧即服务 (AIaaS) 市场报告:按技术、组织规模、产业和地区划分 2026-2034 年 人工智慧即服务 (AIaaS) 市场规模、份额和成长分析(按服务类型、部署方式、技术和地区划分)—产业预测,2026-2033 年

人工智慧即服务 (AIaaS) 市场规模、份额和成长分析(按服务类型、部署方式、技术和地区划分)—产业预测,2026-2033 年 全球应用人工智慧服务市场

全球应用人工智慧服务市场 2025-2029 年全球 AIaaS(人工智慧即服务)市场

2025-2029 年全球 AIaaS(人工智慧即服务)市场 全球人工智慧即服务市场(按产品类型、组织规模、业务功能、服务类型、最终用户和地区划分)- 预测至 2030 年

全球人工智慧即服务市场(按产品类型、组织规模、业务功能、服务类型、最终用户和地区划分)- 预测至 2030 年