|

市场调查报告书

商品编码

1939717

东协仓储业与配送物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)ASEAN Warehousing And Distribution Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

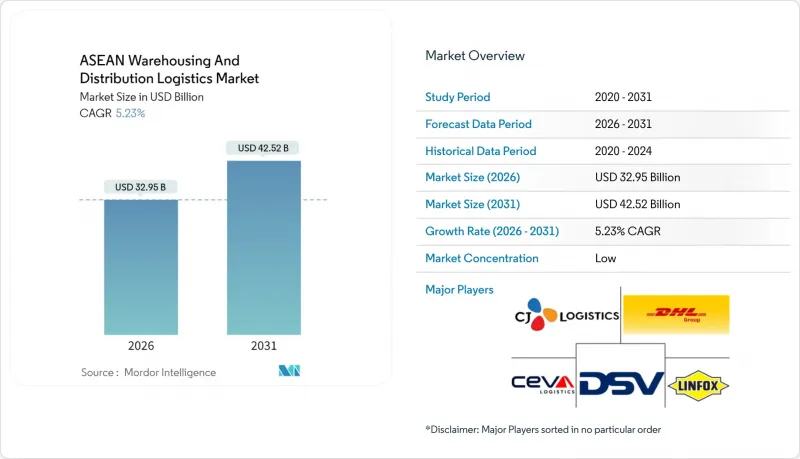

预计到 2026 年,东协仓储业和配送物流市场规模将达到 329.5 亿美元,高于 2025 年的 313.1 亿美元。

预计到 2031 年,该产业规模将达到 425.2 亿美元,2026 年至 2031 年的复合年增长率为 5.23%。

东协地区电子商务的快速成长、大规模基础设施发展计画以及不断扩大的贸易协定,共同推动东协仓储业物流市场成为全球最具吸引力的供应链机会之一。线上零售带来的需求,加上泰国183亿美元的东部经济走廊计画和越南到2025年360亿美元的基础建设目标,正推动仓库向功能更强大的资产转型。第三方物流(3PL)供应商之间的整合,例如GEODIS收购吉宝物流,持续重塑着服务能力。同时,气候变迁预计将在2024年对全球供应链造成超过1,000亿美元的损失,促使东协仓储业物流市场加大对弹性网路设计和自动化仓库的投资。

东协仓储业及配送物流市场趋势及洞察

电子商务需求激增推动了最后一公里配送。

东协仓储业和配送物流市场正积极回应线上零售的蓬勃发展,推动东南亚数位经济在2025年达到1,860亿美元。越南的末端配送领域年增率高达39%,预计2024年包裹处理量将达30亿件。暗店(dark store)的数量正在增加,营运商计划到2026年在全部区域建造5000至5500个微型仓配中心,这迫使投资者转向人口密集城区内紧凑且自动化程度更高的配送点。印尼和泰国的行动商务渗透率超过80%,显示距离终端消费者3公里以内的地理位置在服务差异化方面发挥决定性作用。

政府对物流基础建设的投资

大规模公共支出正在建造新的走廊、码头和干线铁路,刺激仓储需求。泰国东部经济走廊正在投资183亿美元用于机场、港口和高铁升级。越南的2025年计画(总额达360亿美元)为公路和深水港建设拨出了创纪录的资金。同时,马来西亚巴生港的扩建计画(年吞吐量达2700万标准箱)是港口吞吐能力提升如何刺激内陆仓储扩张的典型例子。在内陆国家柬埔寨,新建的高速公路正在催生新的物流中心群。

海关和监管流程脱节

儘管试点计画取得成功,东协海关运输系统目前仍仅限于部分通道。印尼2025年进口法规新增了许可程序,延长了清关週期。越南2025年实施的更新版电子表格需要对平台进行整合调整。超过5000项已确定的非关税措施增加了合规复杂性,延缓了仓储网路合理化进程,并推高了营运资金需求。

细分市场分析

受疫苗分发、生鲜食品电商和温控化学品需求的推动,东协仓储业物流市场的冷藏设施预计将以5.24%的复合年增长率成长。在印尼,随着水产品出口商升级设施以符合欧盟可追溯性标准,到2024年,冷藏仓库面积预计将增加14%。营运商正在维修混合建筑,在常温仓库内安装模组化冷库以保持柔软性。采用节能冷媒、人工智慧压缩机和可再生能源,已使营运成本降低了12%,儘管资本密集度较高,但仍能维持利润率。

随着零售商为缩短前置作业时间而转向分散式网络,越南和菲律宾等区域性城市的低温运输网络正在不断扩展。马来西亚首个碳中和冷库(由Equalbase营运)的能耗降低了50%,展现了环境、社会和治理(ESG)要求与公用事业成本节约之间的协同效应。跨国公司目前正将温度保障与库存融资解决方案结合,以开拓新的收入来源。东协地区的仓储业和配送物流市场持续呈现这样的趋势:与通用仓库相比,A级冷藏资产的开发预算分配比例明显偏高。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务需求激增推动了最后一公里配送。

- 政府对物流基础建设的投资

- 低温运输产能需求不断成长

- 透过东协贸易协定(RCEP、CPTPP)加速跨境分销

- 引进城市暗店和微型仓配

- 以环境、社会和治理(ESG)主导的「绿色仓库」融资

- 市场限制

- 分散的海关和监管流程

- 主要城市地价上涨

- 自动化职位技术纯熟劳工短缺

- 面临气候风险(洪水、颱风)

- 价值/供应链分析

- 监管环境

- 技术展望

- 仓库租金洞察

- 自由贸易区和工业园区分析

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 新冠疫情与地缘政治事件的影响

第五章 市场规模与成长预测

- 按仓库类型

- 普通仓库/存储

- 冷藏仓库/存储

- 依所有权类型

- 私人仓库

- 公共仓库

- 按最终用户行业划分

- 电子商务与零售

- 食品/饮料

- 製药和医疗保健

- 车

- 製造和工程产品

- 其他的

- 按地区

- 新加坡

- 泰国

- 马来西亚

- 越南

- 印尼

- 菲律宾

- 其他东南亚国协

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- DHL Supply Chain

- CEVA Logistics

- CJ Century Logistics

- DSV

- Linfox

- Kuehne+Nagel

- Yusen Logistics(Part of NYK Line)

- Kerry Logistics

- CWT Ltd

- Tiong Nam Logistics

- YCH Group

- Singapore Post

- Geodis

- Ninja Van

- J&T Express

- Pos Malaysia Logistics

- Nippon Express

- WeFreight

- Omni Logistics

- AIT Worldwide Logistics

第七章 市场机会与未来展望

The ASEAN Warehousing And Distribution Logistics Market size in 2026 is estimated at USD 32.95 billion, growing from 2025 value of USD 31.31 billion with 2031 projections showing USD 42.52 billion, growing at 5.23% CAGR over 2026-2031.

The region's rapid e-commerce growth, large-scale infrastructure programs, and expanding trade pacts combine to make the ASEAN warehousing and distribution logistics market one of the most attractive supply-chain opportunities worldwide. Induced demand from online retail, together with Thailand's USD 18.3 billion Eastern Economic Corridor program and Vietnam's USD 36 billion 2025 infrastructure target, is re-ordering warehouse footprints toward higher specification assets. Consolidation among third-party logistics providers (3PLs), exemplified by GEODIS acquiring Keppel Logistics, continues to reshape service capabilities. Meanwhile, climate shocks costing global supply chains more than USD 100 billion in 2024 are prompting resilient network design and automated warehouse investments across the ASEAN warehousing and distribution logistics market.

ASEAN Warehousing And Distribution Logistics Market Trends and Insights

Surge in e-commerce demand boosting last-mile fulfilment

The ASEAN warehousing and distribution logistics market is responding to an online retail boom that propelled Southeast Asia's digital economy toward USD 186 billion in 2025. Vietnam's last-mile delivery segment recorded a 39% annual growth rate with 3 billion parcels handled in 2024. Dark-store footprints are multiplying; operators plan 5,000-5,500 micro-fulfilment sites region-wide by 2026, forcing investors to pivot toward compact, automation-ready nodes inside dense city districts. Indonesia and Thailand, where mobile commerce penetration exceeds 80% demonstrate how proximity facilities within 3 kilometers of end consumers now determine service differentiation.

Government investment in logistics infrastructure

Large public outlays are adding new corridors, terminals, and rail spines that catalyze warehouse demand. Thailand's Eastern Economic Corridor is absorbing USD 18.3 billion for airport, seaport, and high-speed rail upgrades. Vietnam's USD 36 billion 2025 plan allocates record sums for expressways and deep-sea ports, while Malaysia's Port Klang expansion to 27 million TEUs underscores how port capacity growth forces hinterland storage expansion. Landlocked Cambodia benefits from new expressways that open fresh catchments for distribution centers.

Fragmented customs and regulatory processes

Despite pilot successes, the ASEAN Customs Transit System still reaches only selected corridors. Indonesia's 2025 import rules added new licensing layers that lengthen clearance cycles. Vietnam's updated electronic forms introduced in 2025 require platform integration tweaks. Over 5,000 identified non-tariff measures raise compliance complexity, slowing warehouse network rationalization and inflating working capital needs.

Other drivers and restraints analyzed in the detailed report include:

- Growing demand for cold-chain capacity

- ASEAN trade pacts (RCEP, CPTPP) accelerating cross-border flows

- Escalating land prices in tier-1 hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated facilities in the ASEAN warehousing and distribution logistics market are forecast to grow at a 5.24% CAGR. Demand springs from vaccine distribution, fresh food e-commerce, and temperature-controlled chemicals. In Indonesia, cold-store footprints grew 14% in 2024 as seafood exporters upgraded to meet EU traceability protocols. Operators retrofit hybrid buildings, inserting modular chill rooms inside ambient sheds to retain flexibility. Energy-efficient refrigerants, AI-enabled compressors, and renewable power purchasing lower operating costs by 12%, preserving margins despite high capital intensity.

Second-tier cities across Vietnam and the Philippines join the cold-chain map as grocery retailers decentralize networks to shorten lead times. Malaysia's first carbon-neutral cold-store by Equalbase cut energy use 50%, showcasing how ESG mandates and utility savings intersect. Multinationals now bundle temperature assurance with inventory financing solutions, opening ancillary revenue lines. The ASEAN warehousing and distribution logistics market continues to allocate development budgets disproportionately toward Grade-A refrigerated assets to outpace generic stock.

The ASEAN Warehousing and Distribution Logistics Market Report is Segmented by Warehouse Type (General Warehousing and Storage, Refrigerated Warehousing and Storage), Ownership (Private Warehouses, Public Warehouses), End-User Industry (E-Commerce & Retail, Food & Beverage, Pharma & Healthcare, and More), and Geography (Singapore, Thailand, Malaysia, Indonesia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Supply Chain

- CEVA Logistics

- CJ Century Logistics

- DSV

- Linfox

- Kuehne + Nagel

- Yusen Logistics (Part of NYK Line)

- Kerry Logistics

- CWT Ltd

- Tiong Nam Logistics

- YCH Group

- Singapore Post

- Geodis

- Ninja Van

- J&T Express

- Pos Malaysia Logistics

- Nippon Express

- WeFreight

- Omni Logistics

- AIT Worldwide Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in e-commerce demand boosting last-mile fulfilment

- 4.2.2 Government investment in logistics infrastructure

- 4.2.3 Growing demand for cold-chain capacity

- 4.2.4 ASEAN trade pacts (RCEP, CPTPP) accelerating cross-border flows

- 4.2.5 Urban dark-store and micro-fulfilment adoption

- 4.2.6 ESG-driven "green warehouse" financing

- 4.3 Market Restraints

- 4.3.1 Fragmented customs and regulatory processes

- 4.3.2 Escalating land prices in tier-1 hubs

- 4.3.3 Skilled-labour shortage for automated operations

- 4.3.4 Climate-risk exposure (floods, typhoons)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Insights into Warehouse Rents

- 4.8 Free Zones and Industrial Parks Analysis

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

- 4.10 Impact of COVID-19 and Geo-Political Events

5 Market Size and Growth Forecasts (Value)

- 5.1 By Warehouse Type (Value)

- 5.1.1 General Warehousing and Storage

- 5.1.2 Refrigerated Warehousing and Storage

- 5.2 By Ownership (Value)

- 5.2.1 Private Warehouses

- 5.2.2 Public Warehouses

- 5.3 By End-User Industry (Value)

- 5.3.1 E-commerce and Retail

- 5.3.2 Food and Beverage

- 5.3.3 Pharma and Healthcare

- 5.3.4 Automotive

- 5.3.5 Manufacturing and Engineering Goods

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 Singapore

- 5.4.2 Thailand

- 5.4.3 Malaysia

- 5.4.4 Vietnam

- 5.4.5 Indonesia

- 5.4.6 Philippines

- 5.4.7 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Supply Chain

- 6.4.2 CEVA Logistics

- 6.4.3 CJ Century Logistics

- 6.4.4 DSV

- 6.4.5 Linfox

- 6.4.6 Kuehne + Nagel

- 6.4.7 Yusen Logistics (Part of NYK Line)

- 6.4.8 Kerry Logistics

- 6.4.9 CWT Ltd

- 6.4.10 Tiong Nam Logistics

- 6.4.11 YCH Group

- 6.4.12 Singapore Post

- 6.4.13 Geodis

- 6.4.14 Ninja Van

- 6.4.15 J&T Express

- 6.4.16 Pos Malaysia Logistics

- 6.4.17 Nippon Express

- 6.4.18 WeFreight

- 6.4.19 Omni Logistics

- 6.4.20 AIT Worldwide Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment