|

市场调查报告书

商品编码

1939733

英国包装业:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United Kingdom Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

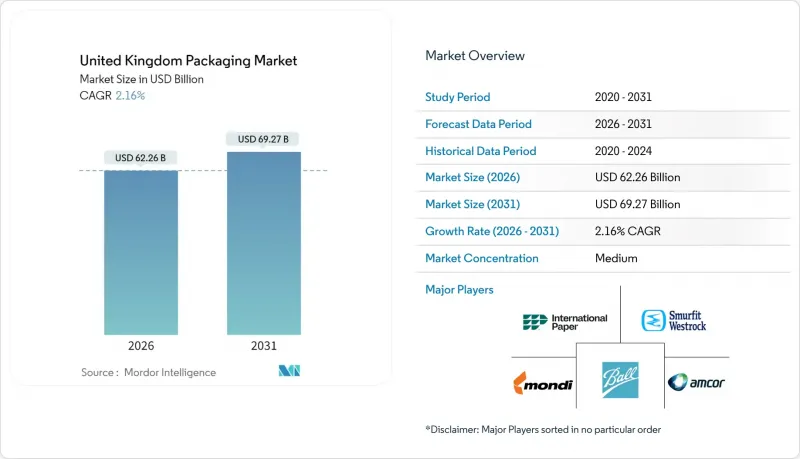

英国包装市场预计到 2026 年价值将达到 622.6 亿美元,高于 2025 年的 609.4 亿美元。

预计到 2031 年将达到 692.7 亿美元,2026 年至 2031 年的复合年增长率为 2.16%。

目前的市场动能反映了一个日益成熟且不断演变的格局,其形成受到英国脱欧后边境规则、更严格的环境法规、电子商务加速发展以及成本上涨。边境目标营运模式(BTOM)下的结构调整增加了合规工作量和交付前置作业时间,促使生产商在在地采购并实现海关文件的自动化。同时,英国塑胶包装税的扩大和生产者延伸责任制的全面实施,提高了人们对可回收性的关注,推动了纸张、单一材料塑胶和生物基薄膜的快速替代。线上零售额占国内销售额的31.3%,提升了软包装的市场份额,而增值印刷能力则使品牌能够以更具成本效益的方式瞄准细分客户群。产业整合仍在持续,其中最引人注目的是国际纸业以75.4亿美元收购DS Smith,此举不仅打造了该地区最大的瓦楞纸包装供应商,也加剧了反垄断审查。

英国包装市场趋势与洞察

电子商务的扩张推动了对瓦楞纸包装和软包装袋的需求。

到2024年,线上零售额将占国内总销售额的31.3%,瓦楞纸箱和软包装袋的出货量增加了23%。 Getil等电商平台推广了兼具防篡改和隔热功能的单件包装。亚马逊的自动化包装线减少了15%的包装材料用量,提高了出货效率,并树立了新的效率标竿。 HelloFresh的订阅模式增加了对可回收隔热材料的需求,而电商卖家也越来越多地选择尺寸合适的邮寄袋以降低体积重量收费。这些趋势都支撑着瓦楞纸箱和软包装在英国包装市场的持续扩张。

英国塑胶税转向可再生和生物基材料

2024年塑胶包装税的扩大将对再生材料含量低于30%的聚合物征收每吨200英镑(263美元)的课税,这将推动再生材料含量提高35%。联合利华在英国的个人保健产品线中已实现了50%的再生塑胶使用率,雀巢也承诺在2025年实现完全可回收解决方案。原生树脂与再生材料之间的价格差距已扩大至18%,这有利于垂直整合的回收企业。大型加工商的平均监管成本已达230万英镑(302万美元),推动了对水洗薄片产能和化学回收试点计画的资金投入。这些永续发展要求正在加速英国包装市场材料组合的重组。

树脂和造纸原物料价格飙升

预计到2024年,聚乙烯树脂价格将上涨22%,而由于能源成本上升和供应受限,再生纸价格也将上涨18%。蒙迪英国业务的利润率下降了340个基点,导致下游价格上涨,需求弹性降低。加工商将安全库存水准提高了25%至30%,以确保供应的连续性,但仓储成本给营运资金带来了压力。高能耗挤出生产线在价格高峰期减产,凸显了英国包装市场短期内面临的拖累。

细分市场分析

到2025年,塑胶将占英国包装市场份额的48.02%,这主要得益于其在食品、饮料和个人护理行业的广泛应用。过去十年,硬质宝特瓶的轻量化设计已使材料重量减少了25%,而消费后回收树脂的整合也提高了再生材料的可靠性。然而,税收阈值的收紧以及零售商的无塑胶承诺正推动成长重点转向纸质基材。受电子商务对瓦楞纸板需求成长的推动,纸质基材将呈现最快的成长速度,到2031年复合年增长率将达到4.62%。随着单一材料设计简化家庭垃圾收集,英国包装纸质基材市场规模预计将持续扩大。

由于玻璃和金属具有无限可回收性和良好的品质感,它们在高端饮品领域重新占据一席之地,分别推动了3.2%和4.1%的年增长率。随着精酿啤酒厂利用铝罐的轻盈和快速冷却特性,并透过提高产量来抵消不断上涨的原材料成本,饮料罐的需求激增。同时,可生物降解的聚合物薄膜也已渗透到一些特殊用途领域,在这些领域,可堆肥性决定了其价格溢价。这些变化表明,儘管塑胶的主导地位略有下降,但其仍然占据主导地位,因为永续性标准正在影响英国包装市场的材料选择。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 由于电子商务的扩张,对瓦楞纸板和软包装邮件的需求增加。

- 英国塑胶税与向可再生和生物基材料的转型

- 千禧世代和旅游需求优质化和对豪华包装的需求。

- 快速消费品自有品牌在折扣通路的扩张需要经济高效的包装。

- 暗厨房的兴起和快速零售的扩张催生了对单件包装的需求。

- 采用数位印刷技术进行小批量生产,使小型企业品牌能够客製化产品。

- 市场限制

- 树脂和造纸原料价格波动剧烈

- 英国对一次性塑胶製品的监管更加严格,以及生产者延伸责任制(EPR)的成本

- 英国脱欧后供应链中断对进口包装组件的影响

- 製造业和物流业劳动力短缺推高了营运成本。

- 产业价值链分析

- 技术展望

- 监管环境

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素的影响

第五章 市场规模与成长预测

- 按包装类型

- 塑胶包装

- 按类型

- 硬质塑胶包装

- 依材料类型

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚氯乙烯(PVC)

- 聚苯乙烯(PS)和发泡聚苯乙烯(EPS)

- 其他材料类型

- 依产品类型

- 瓶子和罐子

- 瓶盖和封装

- 托盘和容器

- 其他产品类型

- 按最终用途行业划分

- 食物

- 饮料

- 製药

- 化妆品和个人护理

- 工业的

- 其他终端用户产业

- 依材料类型

- 软塑胶包装

- 依材料类型

- 聚乙烯(PE)

- 双轴延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 其他材料类型

- 依产品类型

- 麻袋

- 薄膜和包装

- 其他产品类型

- 按最终用途行业划分

- 食物

- 饮料

- 製药

- 化妆品和个人护理

- 工业的

- 其他终端用户产业

- 依材料类型

- 硬质塑胶包装

- 依产品类型

- 瓶子和罐子

- 麻袋

- 散装产品

- 其他产品类型

- 按最终用途行业划分

- 食物

- 饮料

- 化妆品和个人护理

- 製药

- 工业的

- 其他终端用户产业

- 按类型

- 纸包装

- 依产品类型

- 折迭纸箱

- 瓦楞纸箱

- 液态纸板

- 其他产品类型

- 按最终用途行业划分

- 食物

- 饮料

- 电子商务

- 其他终端用户产业

- 依产品类型

- 容器玻璃

- 按颜色

- 绿色的

- 琥珀色

- 燧石

- 其他颜色

- 按最终用途行业划分

- 食物

- 饮料

- 酒精饮料

- 不含酒精的饮料

- 个人护理和化妆品

- 药品(不含管瓶和安瓿瓶)

- 香水

- 按颜色

- 金属罐和容器

- 依材料类型

- 钢材

- 铝

- 依产品类型

- 能

- 鼓和桶

- 瓶盖和封装

- 其他产品类型

- 按最终用途行业划分

- 食物

- 饮料

- 化学品/石油

- 工业的

- 油漆和涂料

- 其他终端用户产业

- 依材料类型

- 塑胶包装

- 按包装类型

- 灵活的

- 难的

- 按最终用途行业划分

- 食物

- 饮料

- 製药和医疗保健

- 个人护理和化妆品

- 工业的

- 电子商务

- 其他终端用户产业

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- International Paper Company

- Smurfit WestRock

- Amcor plc

- Mondi plc

- Ball Corporation

- Crown Holdings Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Graphic Packaging International LLC

- Greif Inc.

- Silgan Holdings Inc.

- AptarGroup Inc.

- Huhtamaki Oyj

- Tetra Pak International SA

- CAN-PACK UK Ltd.

- Ardagh Group SA

- RPC Group Ltd.

- Klckner Pentaplast Ltd.

- Coveris Holdings SA

第七章 市场机会与未来展望

United Kingdom packaging market size in 2026 is estimated at USD 62.26 billion, growing from 2025 value of USD 60.94 billion with 2031 projections showing USD 69.27 billion, growing at 2.16% CAGR over 2026-2031.

Current momentum reflects a mature yet steadily evolving landscape shaped by post-Brexit border rules, tighter environmental mandates, e-commerce acceleration and pronounced cost inflation. Structural adjustments under the Border Target Operating Model raised compliance workloads and stretched lead times, prompting producers to localize inputs and automate customs documentation. Parallel expansion of the United Kingdom Plastic Packaging Tax and full roll-out of Extended Producer Responsibility sharpened the focus on recyclability, driving rapid substitution toward paper, mono-material plastics and bio-based films. Flexible formats gained share as online retail reached 31.3% of national sales, and value-added printing capabilities helped brands target niche audiences cost-effectively. Consolidation continued, highlighted by International Paper's USD 7.54 billion acquisition of DS Smith, which created the region's largest corrugated supplier but intensified antitrust scrutiny.

United Kingdom Packaging Market Trends and Insights

Rising E-commerce Driven Demand for Corrugated and Flexible Mailers

Online retail sales surged to 31.3% of national turnover in 2024, lifting shipment volumes for corrugated boxes and flexible mailers by 23%. Quick-commerce operators such as Getir stimulated single-portion packaging that combines tamper evidence with thermal integrity. Amazon's automated packing lines cut packaging material intensity 15% and accelerated outbound throughput, setting new efficiency benchmarks. Subscription models from HelloFresh amplified demand for returnable insulation, while marketplace sellers gravitated toward right-sized mailers that curb dimensional-weight charges. These developments support continued expansion of corrugated and flexible formats within the United Kingdom packaging market.

Shift Toward Recyclable and Biobased Materials Due to United Kingdom Plastic Tax

The Plastic Packaging Tax extension in 2024 imposed a GBP 200 (USD 263) per-tonne levy on polymers lacking 30% recycled content, encouraging a 35% jump in reclaimed feedstock adoption. Unilever achieved 50% recycled plastic in United Kingdom personal-care lines, while Nestle pledged fully recyclable solutions by 2025. Rising virgin resin differentials 18% above recycled inputs favor vertically integrated recyclers. Average compliance outlays reached GBP 2.3 million (USD 3.02 million) for large converters, prompting capital flows into wash-flake capacity and chemical recycling pilots. Sustainability requirements therefore accelerate material portfolio realignment across the United Kingdom packaging market.

High Raw-Material Price Volatility for Resins and Paper

Polyethylene resin prices jumped 22% in 2024, while recycled paper climbed 18% on energy cost spikes and supply constraints. Mondi's United Kingdom operations reported 340-basis-point margin erosion, triggering downstream price hikes that tempered demand elasticity. Converters raised safety-stock thresholds 25-30% to secure continuity, yet carrying costs strained working capital. Energy-intensive extrusion lines curtailed output during peak tariff windows, underscoring volatility as a short-term drag on the United Kingdom packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization and Luxury Packaging Demand from Millennials and Tourism

- Growing FMCG Private Label Expansion in Discount Channels Requiring Cost-Efficient Packaging

- Strict United Kingdom Regulations on Single-Use Plastics and Extended Producer Responsibility Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic accounted for 48.02% of the United Kingdom packaging market share in 2025, underpinned by its versatility across food, beverage and personal-care categories. Rigid PET bottle light-weighting shaved 25% material mass over the decade while integration of post-consumer resin boosted recycled content credibility. Yet tightening tax thresholds and retailer zero-plastic pledges pivot growth toward paper, which delivers the fastest 4.62% CAGR through 2031 on expanding e-commerce corrugated volumes. The United Kingdom packaging market size for paper substrates will continue to widen as mono-material designs simplify curbside recycling.

Glass and metal regained relevance in premium drinks due to infinite recyclability and high perceived quality, contributing 3.2% and 4.1% respective annual growth. Beverage can volumes surged as craft breweries exploited aluminum's light weight and rapid chilling properties, offsetting higher input costs via volume efficiencies. Meanwhile, bio-polymer films entered specialty applications where compostability commands price premiums. These shifts indicate that plastic's leadership persists but erodes marginally as sustainability criteria increasingly influence material selection within the United Kingdom packaging market.

The United Kingdom Packaging Market Report is Segmented by Packaging Type (Plastic, Paper, Container Glass, Metal Cans), Packaging Format (Flexible, Rigid), End-Use Industry (Food, Beverage, Pharmaceuticals, Personal Care, Industrial, E-Commerce). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- International Paper Company

- Smurfit WestRock

- Amcor plc

- Mondi plc

- Ball Corporation

- Crown Holdings Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Graphic Packaging International LLC

- Greif Inc.

- Silgan Holdings Inc.

- AptarGroup Inc.

- Huhtamaki Oyj

- Tetra Pak International SA

- CAN-PACK UK Ltd.

- Ardagh Group S.A.

- RPC Group Ltd.

- Klckner Pentaplast Ltd.

- Coveris Holdings S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising e Commerce driven demand for corrugated and flexible mailers

- 4.2.2 Shift towards recyclable and biobased materials due to United Kingdom Plastic Tax

- 4.2.3 Premiumization and luxury packaging demand from millennials and tourism

- 4.2.4 Growing FMCG private label expansion in discount channels requiring cost-efficient packaging

- 4.2.5 Growth of dark kitchens and quick commerce creating single-portion packaging needs

- 4.2.6 Adoption of digital printing for short runs enabling customization for SME brands

- 4.3 Market Restraints

- 4.3.1 High raw-material price volatility for resins and paper

- 4.3.2 Strict United Kingdom regulations on single-use plastics and Extended Producer Responsibility costs

- 4.3.3 Supply-chain disruptions post-Brexit impacting imported packaging components

- 4.3.4 Labor shortages in manufacturing and logistics escalating operational costs

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Type

- 5.1.1 Plastic Packaging

- 5.1.1.1 By Type

- 5.1.1.1.1 Rigid Plastic Packaging

- 5.1.1.1.1.1 By Material Type

- 5.1.1.1.1.1.1 Polyethylene (PE)

- 5.1.1.1.1.1.2 Polypropylene (PP)

- 5.1.1.1.1.1.3 Polyethylene Terephthalate (PET)

- 5.1.1.1.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.1.1.1.1.5 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.1.1.1.1.1.6 Other Material Types

- 5.1.1.1.1.2 By Product Type

- 5.1.1.1.1.2.1 Bottles and Jars

- 5.1.1.1.1.2.2 Caps and Closures

- 5.1.1.1.1.2.3 Trays and Containers

- 5.1.1.1.1.2.4 Other Product Types

- 5.1.1.1.1.3 By End-use Industry

- 5.1.1.1.1.3.1 Food

- 5.1.1.1.1.3.2 Beverage

- 5.1.1.1.1.3.3 Pharmaceutical

- 5.1.1.1.1.3.4 Cosmetics and Personal Care

- 5.1.1.1.1.3.5 Industrial

- 5.1.1.1.1.3.6 Other End-use Industry

- 5.1.1.1.1.1 By Material Type

- 5.1.1.1.2 Flexible Plastic Packaging

- 5.1.1.1.2.1 By Material Type

- 5.1.1.1.2.1.1 Polyethylene (PE)

- 5.1.1.1.2.1.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.1.1.2.1.3 Cast Polypropylene (CPP)

- 5.1.1.1.2.1.4 Other Material Types

- 5.1.1.1.2.2 By Product Type

- 5.1.1.1.2.2.1 Pouches and Bags

- 5.1.1.1.2.2.2 Films and Wraps

- 5.1.1.1.2.2.3 Other Product Types

- 5.1.1.1.2.3 By End-use Industry

- 5.1.1.1.2.3.1 Food

- 5.1.1.1.2.3.2 Beverage

- 5.1.1.1.2.3.3 Pharmaceutical

- 5.1.1.1.2.3.4 Cosmetics and Personal Care

- 5.1.1.1.2.3.5 Industrial

- 5.1.1.1.2.3.6 Other End-use Industry

- 5.1.1.1.2.1 By Material Type

- 5.1.1.1.1 Rigid Plastic Packaging

- 5.1.1.2 By Product Type

- 5.1.1.2.1 Bottles and Jars

- 5.1.1.2.2 Pouches and Bags

- 5.1.1.2.3 Bulk-Grade Products

- 5.1.1.2.4 Other Product Types

- 5.1.1.3 By End-use Industry

- 5.1.1.3.1 Food

- 5.1.1.3.2 Beverages

- 5.1.1.3.3 Cosmetics and Personal Care

- 5.1.1.3.4 Pharamceuticals

- 5.1.1.3.5 Industrial

- 5.1.1.3.6 Other End-use Industry

- 5.1.1.1 By Type

- 5.1.2 Paper Packaging

- 5.1.2.1 By Product Type

- 5.1.2.1.1 Folding Carton

- 5.1.2.1.2 Corrugated Boxes

- 5.1.2.1.3 Liquid Paperboard

- 5.1.2.1.4 Other Product Type

- 5.1.2.2 By End-use Industry

- 5.1.2.2.1 Food

- 5.1.2.2.2 Beverages

- 5.1.2.2.3 E-commerce

- 5.1.2.2.4 Other End-use Industry

- 5.1.2.1 By Product Type

- 5.1.3 Container Glass

- 5.1.3.1 By Color

- 5.1.3.1.1 Green

- 5.1.3.1.2 Amber

- 5.1.3.1.3 Flint

- 5.1.3.1.4 Other Colors

- 5.1.3.2 By End-use Industry

- 5.1.3.2.1 Food

- 5.1.3.2.2 Beverage

- 5.1.3.2.2.1 Alcoholic

- 5.1.3.2.2.2 Non-Alcoholic

- 5.1.3.2.3 Personal Care and Cosmetics

- 5.1.3.2.4 Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.3.2.5 Perfumery

- 5.1.3.1 By Color

- 5.1.4 Metal Cans and Containers

- 5.1.4.1 By Material Type

- 5.1.4.1.1 Steel

- 5.1.4.1.2 Aluminum

- 5.1.4.2 By Product Type

- 5.1.4.2.1 Cans

- 5.1.4.2.2 Drums and Barrels

- 5.1.4.2.3 Caps and Closures

- 5.1.4.2.4 Other Product Type

- 5.1.4.3 By End-use Industry

- 5.1.4.3.1 Food

- 5.1.4.3.2 Beverage

- 5.1.4.3.3 Chemicals and Petroleum

- 5.1.4.3.4 Industrial

- 5.1.4.3.5 Paints and coatings

- 5.1.4.3.6 Other End-use Industry

- 5.1.4.1 By Material Type

- 5.1.1 Plastic Packaging

- 5.2 By Packaging Format

- 5.2.1 Flexible

- 5.2.2 Rigid

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceuticals and Healthcare

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Industrial

- 5.3.6 E-commerce

- 5.3.7 Other End-use Industry

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core segments, Financials as available, Strategic information, Market rank/share for key companies, Products and Services, and Recent developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit WestRock

- 6.4.3 Amcor plc

- 6.4.4 Mondi plc

- 6.4.5 Ball Corporation

- 6.4.6 Crown Holdings Inc.

- 6.4.7 Sealed Air Corporation

- 6.4.8 Sonoco Products Company

- 6.4.9 Graphic Packaging International LLC

- 6.4.10 Greif Inc.

- 6.4.11 Silgan Holdings Inc.

- 6.4.12 AptarGroup Inc.

- 6.4.13 Huhtamaki Oyj

- 6.4.14 Tetra Pak International SA

- 6.4.15 CAN-PACK UK Ltd.

- 6.4.16 Ardagh Group S.A.

- 6.4.17 RPC Group Ltd.

- 6.4.18 Klckner Pentaplast Ltd.

- 6.4.19 Coveris Holdings S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

轻量化包装市场预测至2034年-按材料、产品类型、技术、分销管道、最终用户和地区分類的全球分析湿度控制包装市场预测至2034年-按产品类型、材料、包装形式、通路、最终用户和地区分類的全球分析

轻量化包装市场预测至2034年-按材料、产品类型、技术、分销管道、最终用户和地区分類的全球分析湿度控制包装市场预测至2034年-按产品类型、材料、包装形式、通路、最终用户和地区分類的全球分析 感官包装市场:依技术、材料、感测器类型、包装形式和应用划分-2026-2032年全球市场预测

感官包装市场:依技术、材料、感测器类型、包装形式和应用划分-2026-2032年全球市场预测 2026年全球包装与标籤服务市场报告

2026年全球包装与标籤服务市场报告 全球枕式包装市场:市场规模、份额、趋势和成长分析(2026-2034)气泡膜市场:2026-2032年全球市场预测(依材料、厚度、应用、最终用户及通路划分)復古包装市场:按材料、类型、最终用途、印刷技术和通路-2026-2032年全球预测纸质復古包装市场:依材料、包装类型、销售管道、最终用户、应用程式划分,全球预测(2026-2032)多功能零件市场按产品类型、价格范围、应用、垂直产业和分销管道划分,全球预测(2026-2032年)纸塑包装器材市场:依机器类型、材料、操作类型和应用划分,全球预测(2026-2032年)

全球枕式包装市场:市场规模、份额、趋势和成长分析(2026-2034)气泡膜市场:2026-2032年全球市场预测(依材料、厚度、应用、最终用户及通路划分)復古包装市场:按材料、类型、最终用途、印刷技术和通路-2026-2032年全球预测纸质復古包装市场:依材料、包装类型、销售管道、最终用户、应用程式划分,全球预测(2026-2032)多功能零件市场按产品类型、价格范围、应用、垂直产业和分销管道划分,全球预测(2026-2032年)纸塑包装器材市场:依机器类型、材料、操作类型和应用划分,全球预测(2026-2032年)