|

市场调查报告书

商品编码

1939746

亚太地区纺织品:市占率分析、产业趋势与统计、成长预测(2026-2031)Asia-Pacific Textile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

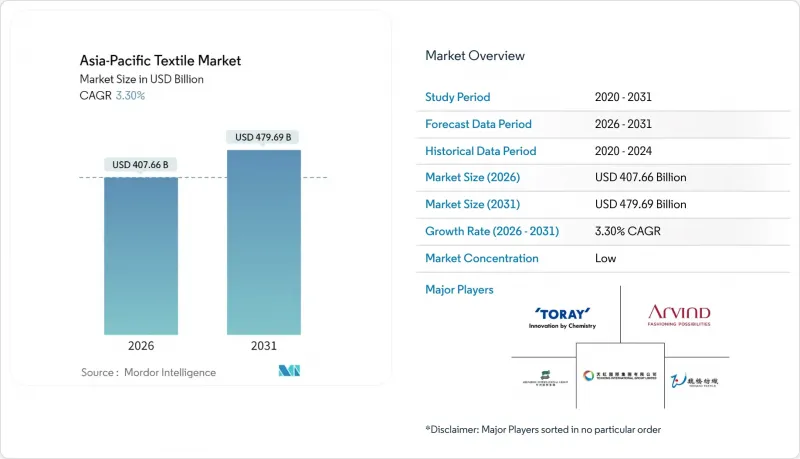

亚太地区纺织品市场预计将从 2025 年的 3,946.4 亿美元成长到 2026 年的 4,076.6 亿美元,预计到 2031 年将达到 4,796.9 亿美元,2026 年至 2031 年的复合年增长率为 3.3%。

这些稳定成长数据的另一面是,低利润的大众商品与高价值技术应用(如今价格更高)之间的差距日益扩大。成本敏感型生产集中在传统地区,而技术密集型製造业则正向拥有先进机械和技术熟练劳动力的新兴次区域转移。能源成本上涨、ESG合规要求以及自动化投资正在重塑竞争优势,推动供应链多元化和垂直整合营运。因此,亚太纺织品市场正朝着两极化的成长模式发展,效率提升和产品创新,而非单纯的产量,将决定盈利。

亚太地区纺织品市场趋势与洞察

服装消费正变得越来越高端。

亚太地区都市区可支配收入的成长推动了对奢侈品和功能性服饰的需求。品牌纷纷回应,投资于可追溯性平台和环保生产流程,使製造商能够透过垂直整合获得更高的利润率。例如,杰尼亚(Ermenegildo Zegna)公布2023年亚太地区纺织品销售额达1.661亿美元,证实了其高端策略对原物料价格波动的缓衝作用。功能性纤维供应商将从中受益最多,因为其产品的性能特性使其价格比普通面料高出三到五倍。

有组织的时尚零售业的发展

大型零售连锁店主导着分销管道,对品质、交货和合规性有严格的要求。获得认证的工厂能够满足这些买家的要求,因此预计印度2025财年的出口将达到366亿美元。随着门市网路的扩张,竞争的焦点从价格转向服务水准、环境审核和数位化协作工具,这使得规模小规模、不合规的工厂被淘汰。

能源价格波动

纺纱过程耗电量占纺织厂电力消耗量的70%之多,因此电价大幅上涨将对毛利率造成压力。虽然印度部分邦提供补贴,但大多数邦仅涵盖部分成本,迫使小规模纺织厂关闭或合併。大型集团已透过长期购电协议和安装现场太阳能发电设施进行对冲来缓解即时影响,但预计成长仍然低迷。

细分市场分析

工业和技术类纺织品正以4.65%的复合年增长率快速增长,其在亚太纺织品市场的份额逐年攀升,这主要得益于汽车、医疗和过滤行业的买家对高性能基材的需求。同时,时尚服装类纺织品市场占有率为46.55%,但由于永续发展方面的阻力抵消了快时尚的销售成长,其成长势头较为缓慢。医用不织布在疫情期间及之后蓬勃发展,而汽车纺织品则受惠于电动车的温度控管需求。由于都市化,家用纺织品市场保持稳定,而防护装备市场则因职业安全法规的加强而成长。先进的传感器整合技术正在模糊服装和智慧面料之间的界限,从而扩大高端订单的潜在市场。

短期内,技术供应商预计将透过监管障碍、医疗保健产业的ISO 13485标准以及运输业严格的OEM规范来阻碍新进业者。现有供应商将透过投资自动化织造设备和先进涂层技术,巩固其在高附加价值细分市场的地位。预计在预测期内,这些发展趋势将扩大亚太地区纺织品市场技术型和商品型细分市场之间的盈利差距。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 奢侈品服装消费趋势

- 有组织的时尚零售业的发展

- 全球品牌的ESG相关采购义务

- 新兴的「近岸外包」模式正在向东协和印度地区兴起

- 生物基纺织品研发取得突破;

- 人工智慧需求预测的采用现状

- 市场限制

- 能源价格波动会影响纺织业的利润率。

- 对染料厂污水有严格的规定

- 中美贸易政策的不确定性

- 区域城市织布工人短缺

- 价值/供应链分析

- 监理展望

- 技术展望

- 电子商务市场洞察

- 产业吸引力—五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值,十亿美元)

- 透过使用

- 时尚与服装

- 工业/技术纺织品

- 家用纺织品

- 医疗和保健纺织品

- 汽车和运输纺织品

- 其他(防护用纺织品、运动用纺织品等)

- 按原料

- 天然纤维

- 棉布

- 羊毛

- 丝绸

- 合成纤维

- 聚酯纤维

- 尼龙

- 人造丝/粘胶纤维

- 丙烯酸纤维

- 聚丙烯

- 再生纤维

- 其他(特殊高性能纤维(芳香聚酰胺、碳纤维、超高分子量聚乙烯))

- 天然纤维

- 透过製造工艺/技术

- 织物

- 针织

- 不织布

- 纺丝成网(纺粘/熔喷)

- 干式和水刺式

- 湿法成网

- 针刺加工

- 3D编织和间隔织物

- 按地区

- 中国

- 印度

- 孟加拉

- 澳洲

- 韩国

- 日本

- 东协(印尼、泰国、菲律宾、马来西亚、越南)

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Shenzhou International Group

- Weiqiao Textile

- Texhong Textile Group

- Toray Industries

- Arvind Ltd

- Vardhman Textiles Ltd

- Far Eastern New Century(FENC)

- Hyosung TNC

- Bombay Dyeing & Mfg Co

- Bombay Rayon Fashions

- Pacific Textiles

- Luthai Textile

- Nisshinbo Holdings

- PT Sri Rejeki Isman(Sritex)

- Raymond Ltd

- Fabindia Overseas

- Youngone Corp

- Indorama Ventures(IVL Fibres)

- Teijin Ltd

- Cotton Corporation of India

第七章 市场机会与未来展望

The APAC Textile Industry Market is expected to grow from USD 394.64 billion in 2025 to USD 407.66 billion in 2026 and is forecast to reach USD 479.69 billion by 2031 at 3.3% CAGR over 2026-2031.

This steady headline number masks a widening gap between low-margin bulk products and higher-value technical applications that now attract premium pricing. Cost-sensitive output continues to cluster in traditional hubs, while technology-intensive manufacturing migrates to newer sub-regions equipped with advanced machinery and skilled labor. Rising energy costs, ESG compliance mandates, and automation investments are reshaping competitive advantages, prompting both supply-chain diversification and vertically integrated operations. The APAC textile industry market, therefore, moves toward a dual-track growth pattern in which efficiency gains and product innovation, rather than volume alone, determine profitability.

Asia-Pacific Textile Market Trends and Insights

Premiumization of Apparel Spend

Growing disposable incomes in APAC's metropolitan areas lift demand for luxury and performance garments. Brands respond by investing in traceability platforms and low-impact production, which lets manufacturers capture higher margins through vertical integration. Ermenegildo Zegna, for instance, reported USD 166.1 million in regional textile revenue in 2023, underscoring the insulating effect of premium positioning against raw-material volatility. Technical-textile suppliers benefit most because their performance attributes justify price points that are three to five times above commodity fabrics.

Growth of Organized Fashion Retail

Large retail chains now dominate distribution and insist on strict quality, delivery, and compliance standards. India's exports reached USD 36.6 billion in FY 2025, in part because certified mills could meet these buyer requirements. As store networks scale, they shift competition away from price and toward service levels, environmental audits, and digital collaboration tools, edging out small, non-compliant factories.

Energy-Price Volatility

Spinning consumes up to 70% of a mill's electricity, so sudden rate hikes compress gross margins. While some Indian states offer subsidies, most cover only a fraction of costs, pushing small mills toward closure or merger. Larger groups hedge through long-term power-purchase agreements and on-site solar arrays, dampening the immediate impact but still trimming forecast growth.

Other drivers and restraints analyzed in the detailed report include:

- Near-shoring to ASEAN + India

- ESG-linked Sourcing Mandates

- Stringent Wastewater Norms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial and technical categories are on a 4.65% CAGR, lifting their portion of the APAC textile industry market size each year as automotive, medical, and filtration buyers specify higher-performance substrates. In contrast, fashion and apparel's 46.55% share shows minimal expansion because sustainability headwinds offset fast-fashion volume. Medical non-wovens surged during and after the pandemic, and automotive textiles benefit from electric-vehicle heat-management needs. Household segments hold steady due to urbanization, while protective gear grows alongside occupational-safety legislation. Greater sensor integration blurs lines between apparel and smart-fabric niches, expanding the addressable pool of premium orders.

The near-term outlook sees technical providers capitalizing on regulatory barriers, ISO 13485 in healthcare, and stringent OEM specifications in transport, which discourage new entrants. Existing suppliers invest in automated looms and advanced coatings, reinforcing their grip on value-added niches. Over the forecast period, these moves will widen the profitability gap between technical and commodity segments within the broader APAC textile industry market.

The Asia-Pacific Textile Market Report is Segmented by Application (Fashion & Apparel, Industrial/Technical Textiles, Household & Home Textiles, and More), by Raw Material (Natural Fibers, Synthetic Fibers, and More), by Process (Woven, Knitted, Non-Woven, and More), and by Geography (China, India, Bangladesh, Australia, South Korea, Japan, ASEAN, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Shenzhou International Group

- Weiqiao Textile

- Texhong Textile Group

- Toray Industries

- Arvind Ltd

- Vardhman Textiles Ltd

- Far Eastern New Century (FENC)

- Hyosung TNC

- Bombay Dyeing & Mfg Co

- Bombay Rayon Fashions

- Pacific Textiles

- Luthai Textile

- Nisshinbo Holdings

- PT Sri Rejeki Isman (Sritex)

- Raymond Ltd

- Fabindia Overseas

- Youngone Corp

- Indorama Ventures (IVL Fibres)

- Teijin Ltd

- Cotton Corporation of India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumisation of apparel spend

- 4.2.2 Growth of organised fashion retail

- 4.2.3 ESG-linked sourcing mandates by global brands

- 4.2.4 Emerging "near-shoring" to ASEAN+India

- 4.2.5 Breakthroughs in bio-based fibre R&D

- 4.2.6 AI-driven demand-forecasting adoption

- 4.3 Market Restraints

- 4.3.1 Energy-price volatility hitting spinning margins

- 4.3.2 Stringent wastewater norms for dye-houses

- 4.3.3 US-China trade policy uncertainty

- 4.3.4 Loom-level labour shortages in tier-2 clusters

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Insights into the E-commerce Market

- 4.8 Industry Attractiveness - Porter's Five Forces

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Application

- 5.1.1 Fashion & Apparel

- 5.1.2 Industrial/Technical Textiles

- 5.1.3 Household & Home Textiles

- 5.1.4 Medical & Healthcare Textiles

- 5.1.5 Automotive & Transport Textiles

- 5.1.6 Others (Protective, Sports Textiles, etc.)

- 5.2 By Raw Material

- 5.2.1 Natural Fibers

- 5.2.1.1 Cotton

- 5.2.1.2 Wool

- 5.2.1.3 Silk

- 5.2.2 Synthetic Fibers

- 5.2.2.1 Polyester

- 5.2.2.2 Nylon

- 5.2.2.3 Rayon / Viscose

- 5.2.2.4 Acrylic

- 5.2.2.5 Polypropylene

- 5.2.3 Recycled Fibers

- 5.2.4 Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE))

- 5.2.1 Natural Fibers

- 5.3 By Process / Technology

- 5.3.1 Woven

- 5.3.2 Knitted

- 5.3.3 Non-woven

- 5.3.3.1 Spunlaid (Spunbond / Melt-blown)

- 5.3.3.2 Dry-laid Hydro-entangled

- 5.3.3.3 Wet-Laid

- 5.3.3.4 Needle-punched

- 5.3.4 3-D Weaving & Spacer Fabrics

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Bangladesh

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 Japan

- 5.4.7 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.4.8 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Shenzhou International Group

- 6.4.2 Weiqiao Textile

- 6.4.3 Texhong Textile Group

- 6.4.4 Toray Industries

- 6.4.5 Arvind Ltd

- 6.4.6 Vardhman Textiles Ltd

- 6.4.7 Far Eastern New Century (FENC)

- 6.4.8 Hyosung TNC

- 6.4.9 Bombay Dyeing & Mfg Co

- 6.4.10 Bombay Rayon Fashions

- 6.4.11 Pacific Textiles

- 6.4.12 Luthai Textile

- 6.4.13 Nisshinbo Holdings

- 6.4.14 PT Sri Rejeki Isman (Sritex)

- 6.4.15 Raymond Ltd

- 6.4.16 Fabindia Overseas

- 6.4.17 Youngone Corp

- 6.4.18 Indorama Ventures (IVL Fibres)

- 6.4.19 Teijin Ltd

- 6.4.20 Cotton Corporation of India

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

防护纺织品市场:按类型、产品类型、最终用途和分销管道划分 - 2026-2032年全球市场预测动物源性纺织品市场:2026-2032年全球市场按形态、产品类型、通路和应用分類的预测纺织品市场:按材料、应用和分销管道划分-2026-2032年全球市场预测纱线、纤维和线材市场:按产品类型、原料、製造流程、捻度、应用、分销通路和最终用途产业划分-全球预测,2026-2032年

防护纺织品市场:按类型、产品类型、最终用途和分销管道划分 - 2026-2032年全球市场预测动物源性纺织品市场:2026-2032年全球市场按形态、产品类型、通路和应用分類的预测纺织品市场:按材料、应用和分销管道划分-2026-2032年全球市场预测纱线、纤维和线材市场:按产品类型、原料、製造流程、捻度、应用、分销通路和最终用途产业划分-全球预测,2026-2032年 纺织品市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、最终用户、製程、组件及采用度划分

纺织品市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、最终用户、製程、组件及采用度划分 纺织品市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

纺织品市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 日本纺织品市场:规模、份额、趋势和预测:按原材料、产品、应用和地区划分,2026-2034年日本防水纺织品市场规模、份额、趋势及预测(按原料、织物类型、应用和地区划分,2026-2034年)纺织品市场规模、份额、趋势及预测(依原料、产品、应用及地区划分),2026-2034年

日本纺织品市场:规模、份额、趋势和预测:按原材料、产品、应用和地区划分,2026-2034年日本防水纺织品市场规模、份额、趋势及预测(按原料、织物类型、应用和地区划分,2026-2034年)纺织品市场规模、份额、趋势及预测(依原料、产品、应用及地区划分),2026-2034年 2026年全球纱线、纤维和线市场报告

2026年全球纱线、纤维和线市场报告