|

市场调查报告书

商品编码

1939751

切割机:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Cutting Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

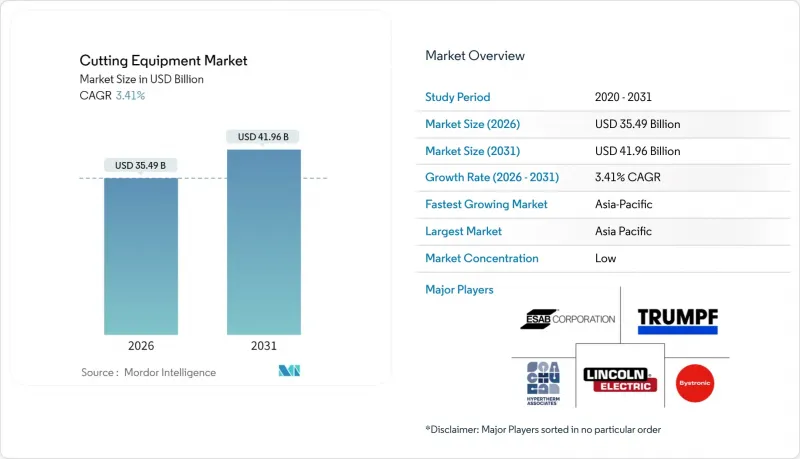

2025年切割机市值为343.2亿美元,预计到2031年将达到419.6亿美元,而2026年为354.9亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.41%。

持续投资光纤雷射系统、自动化程度不断提高以及材料组合的不断扩展,即使在市场日趋成熟的情况下,也支撑着产业的稳定成长。光纤雷射技术已在雷射领域占据领先地位,预计到2024年将占据45.65%的市场份额,而超音波和人工智慧赋能的系统则进一步拓展了竞争格局。亚太地区製造业的快速成长支撑着全球近一半的需求,而汽车产业的电气化以及电子产业对精度的需求,正在推动对先进机械设备的投资。同时,高资本密集度和熟练劳动力短缺限制产业的扩张,供应商正转向提供承包、软体丰富且节能的产品,以保障利润并刺激其他需求。

全球切割机市场趋势与洞察

精密加工在电动车/内燃机汽车和航太领域的重要性

电动车电池外壳和下一代航太零件的设计公差如今已远低于一毫米,这要求工厂采用雷射、水刀和超音波加工等技术来避免因高温造成的变形。安德里茨·舒勒公司的雷射落料生产线每分钟可切割45个高抗拉强度钢零件,并透过智慧排料技术减少了17%的原料浪费。复合材料回收也面临类似的精度要求,风力发电机纤维在回收利用前必须达到完美的机械阈值。对复合材料车身结构日益增长的需求推动了自适应切割参数和在线连续品管的发展,促使视觉系统和人工智慧分析技术被整合到每个工作站中。因此,即使在成熟的工厂中,高规格设备的更新换代需求也预计将持续存在。

工业4.0推动CNC/机器人自动化快速成长

製造商正日益将切割机与整合感测器的单元连接起来,这些单元能够自我诊断磨损情况、规划维护,并在工厂网路内共用生产数据。通快(TRUMPF)的 TruMatic 5000 将冲压和雷射技术与 SheetMaster 处理系统结合,可在单一封闭回路型中完成零件的装载、切割和排放,从而减少閒置时间和人工投入。像 Miller Electric 和 Novarc 这样的合作伙伴正在将人工智慧应用于焊接接头这一以往无法自动化的工艺,以帮助缓解熟练劳动力短缺的问题。 Bystronic 和 NanoLock 的网路安全解决方案可保护连网雷射装置免受勒索软体攻击。这些创新使工厂能够以更少的操作人员生产多品种、小批量产品,从而重塑成本结构,并加速切割市场对机器人技术的采用。

高昂的初始投资和整合成本

引入智慧雷射、机器人和储存塔不仅需要购买机器,还需要加固地面、升级电力系统和整合ERP系统,所有这些都使许多中小型工厂的计划预算超出了承受范围。通快(TRUMPF)的全自动单元也构成了一大障碍:雷射、冲压头和SheetMaster装载机需要同步授权和安全防护装置,导致低产量用户的投资回收期超过三年。公共部门津贴可涵盖高达50%的支出,但申请週期和配套资金规则可能会延误采购决策。同时,符合ISO 12100机器安全标准需要防护装置和风险评估,这又增加了成本。在价格下降或租赁模式普及之前,高额的资本投入可能会限制中小企业采用这些设备。

细分市场分析

光纤雷射在切割机市场中占最大份额,预计到2025年将占总收入的45.12%。其高电光转换效率、低维护成本和窄切割宽度使其适用于黑色金属和非铁金属的加工。 nLIGHT的电晕光束整形单元代表了该领域的突破,无需更换光学元件即可在厚薄板材的环形模式之间进行即时切换。虽然CO2平台仍在一些专门加工厚不銹钢的车间中使用,但随着光纤雷射器拥有成本的持续下降,其市场份额正在不断增长。

雷射设备的需求也受惠于更有效率的占地面积利用率,单头雷射切割机即可实现以往只有大型龙门式系统才能达到的千瓦级功率输出。超音波和混合雷射-等离子切割设备预计将在2026年至2031年间以4.98%的复合年增长率快速成长,但其基数较小。供应商正在将人工智慧视觉、自动喷嘴更换和预测性镜头清洁等技术纳入产品蓝图,进一步巩固光纤雷射在切割机市场的地位。

到2025年,半自动设备将占切割机市场规模的42.06%,反映出穿梭台、套料软体和操作员辅助装载技术的普及。半自动化已成为许多中小企业的入门选择,因为它使工厂能够在保持柔软性的同时减少人员配置。然而,随着ISO 10218-2:2025标准的实施,整合龙门式装载机和AGV的全机器人单元预计将在2031年之前以5.07%的复合年增长率增长,因为该标准使协作机器人的应用更加便捷。

将去毛边、零件分类等多个外围任务整合到同一工作单元中,可以提高投资报酬率。 TRUMPF 感测器即时监控吸盘的真空状态,防止切削误差,提高无人操作的可靠性。同时,运作载荷达 15 公斤的低成本协作机器人售价低于 3 万美元,即使在小规模的加工车间也能实现无人值守的夜间运作。这些趋势表明,即使人机协作的工作流程仍在继续,自动化在切削设备市场中仍将扮演越来越重要的角色。

区域分析

预计到2025年,亚太地区将占全球收入的48.62%,并在2031年之前维持4.31%的复合年增长率,这主要得益于中国-印度-东协走廊的产能扩张。 HSG Laser投资6,830万美元在济南兴建的园区便是此规模的典型例证,园区承诺每年生产1万台高功率设备,并缩短本地客户的前置作业时间。电动车、航太和造船业的政策扶持预计将持续推动订单成长,同时,国内工具製造商也拓展海外售后服务基地以支持出口。

北美拥有强大的现有设备基础,并受益于旨在降低升级成本的新激励措施。美国能源局2024年提供的4,000万美元津贴将支持38个州219家工厂的节能维修,加速光纤雷射的普及应用。此外,7.5亿美元的先进能源製造和回收计画专门用于煤炭生产影响地区的工厂维修,并促进金属加工厂向更清洁、更自动化的生产线转型。加拿大的汽车产业丛集和墨西哥的近岸外包热潮也进一步推动了区域需求。

欧洲精密工程的传统和严格的监管体系帮助其在宏观经济成长放缓的情况下仍维持了销售成长。百超(Bystronic)的「智慧切割製程」自主套件荣获瑞士技术奖,展现了其在全无人雷射研发领域的领先地位。德国透过其DIN委员会主导国际标准制定,并积极参与制定强调高规格安全架构的ISO法规。欧盟环境指令也推动了对复合材料回收工厂的投资,间接带动了超音波切割机和水刀切割机的订单。中东、非洲和南美洲正在崛起新的成长中心,这些地区的基础设施建设正在推动中价位等电浆切割机切割机和氧气切割机的首次引入。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 为电动车 (EV)/内燃机 (ICE) 汽车和航太工业製造精密关键零件

- 工业4.0主导CNC/机器人自动化蓬勃发展

- 亚太地区製造业产能快速扩张

- 疫情后促进节能型光纤雷射器进行资本投资的措施

- 先进复合材料的回收需要冷切割工艺

- 电动出行平台对轻量化电池外壳的需求

- 市场限制

- 高昂的初始投资和整合成本

- 全球熟练的CNC/电脑辅助製造工程师短缺

- 关键电子和光学元件的供应链波动

- 石榴石磨料短缺影响水刀作业成本。

- 价值/供应链分析

- 监管环境

- 技术展望

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 全球製造业概览

- 金属加工产业概览

第五章 市场规模及成长预测(金额)

- 透过技术

- 雷射

- 纤维

- CO2

- 固体/其他

- 电浆

- 高解析度

- 传统的

- 水刀

- 磨料

- 纯的

- 火焰/氧气燃料

- 超音波和新兴技术

- 雷射

- 按自动化级别

- 手动的

- 半自动

- 机器人/全自动

- 按最终用户行业划分

- 车

- 航太/国防

- 电气和电子设备

- 建筑和基础设施

- 金属加工合约工厂

- 造船

- 能源与电力

- 其他(医疗设备等)

- 依材料类型

- 钢

- 非铁金属

- 复合材料

- 玻璃/陶瓷/石材

- 其他(聚合物/塑胶/木材等)

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东协(印尼、泰国、菲律宾、马来西亚、越南)

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- TRUMPF SE+Co. KG

- Lincoln Electric Holdings, Inc.

- ESAB Corp.(ex-Colfax)

- Bystronic AG

- Hypertherm Associates

- IPG Photonics Corp.

- Mitsubishi Electric/Mazak Optonics

- Han's Laser Technology

- Messer Cutting Systems

- Flow International

- OMAX Corp.

- KMT Waterjet Systems

- Amada Miyachi

- Kennametal Inc.

- DAIHEN Corp.

- Koike Aronson, Inc.

- GCE Group

- Linde plc(Cutting gases)

- Prima Power

- Struers(sample-prep niche)

第七章 市场机会与未来展望

The cutting equipment market was valued at USD 34.32 billion in 2025 and estimated to grow from USD 35.49 billion in 2026 to reach USD 41.96 billion by 2031, at a CAGR of 3.41% during the forecast period (2026-2031).

Ongoing investments in fiber laser systems, rising automation adoption, and widening material portfolios sustain steady growth even as the marketplace matures. Fiber laser technology already leads the laser segment with a 45.65% share in 2024, and ultrasonic plus AI-enabled systems are broadening the competitive set. Asia-Pacific's manufacturing surge underpins nearly half the global demand, while electrification in automotive and precision needs in electronics pull advanced machinery spending. At the same time, high capital intensity and gaps in skilled labor temper expansion, pushing suppliers toward turnkey, software-rich, and energy-efficient offerings to defend margins and unlock replacement demand.

Global Cutting Equipment Market Trends and Insights

Precision-Critical Fabrication in EV/ICE Automotive & Aerospace

Design tolerances for EV battery housings and next-generation aerospace parts now fall below a millimeter, forcing plants to adopt lasers, water-jets, and ultrasonics that avoid heat-affected distortion. ANDRITZ Schuler's Laser Blanking Line cuts high-strength steel at 45 parts per minute and trims raw-material waste by 17% through intelligent nesting. Similar precision requirements extend to composite recycling, where reclaimed wind-turbine fibers must remain intact to meet mechanical thresholds for reuse. Demand for mixed-material body structures amplifies the need for adaptive cutting parameters and in-line quality control, pushing vendors to embed vision systems and AI analytics within every workstation. As a result, high-specification machinery sees durable replacement demand even in mature plants.

Industry 4.0 Driven CNC/Robotic Automation Surge

Manufacturers increasingly link cutting machines into sensor-rich cells that self-diagnose wear, schedule service, and share production data across the factory network. TRUMPF's TruMatic 5000 couples punch-laser tech with SheetMaster handling to load, cut, and unload parts in one closed loop, shrinking idle time and labor input. Partnerships such as Miller Electric-Novarc apply AI to weld joints previously impossible to automate, easing skilled-worker shortages. Cyber-security solutions from Bystronic and NanoLock now guard connected lasers against ransomware breaches. Collectively, these innovations let plants run small, high-mix batches with fewer operators, reshaping cost structures and accelerating the diffusion of robotics into the cutting equipment market.

High Upfront Capital & Integration Costs

Smart lasers, robots, and storage towers demand not only machine purchase but also reinforced floors, power upgrades, and ERP links, all of which raise project budgets beyond many smaller shops. TRUMPF's fully automated cells illustrate the hurdle: the laser, punch head, and SheetMaster loader require synchronized software licenses and safety fencing that push payback periods past three years for low-volume users. Public-sector grants cover up to 50% of outlays, yet application cycles and matching-fund rules can defer purchase decisions. Meanwhile, compliance with ISO 12100 machine-safety norms mandates guarding and risk assessments that add further cost layers. Until prices taper or leasing models proliferate, capital intensity will cap penetration rates among SMEs.

Other drivers and restraints analyzed in the detailed report include:

- Manufacturing Capacity Boom Across APAC

- Post-Pandemic Cap-Ex Incentives for Energy-Efficient Fiber Lasers

- Global Shortage of Skilled CNC/CAM Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber lasers accounted for 45.12% of 2025 revenue, maintaining the largest slice of the cutting equipment market. Their high electrical-to-optical efficiency, lower service needs, and tight kerf widths suit both ferrous and non-ferrous metals. nLIGHT's Corona beam-shaping unit showcases the segment's pace, letting users toggle ring modes on the fly for thick or thin plates without optics swaps. CO2 platforms still survive in shops focused on thicker stainless edges, but incremental sales now gravitate toward fiber as ownership costs continue to compress.

Laser demand also benefits from tighter floor-space utilization, as single-head machines reach kilowatt ratings once reserved for large gantry systems. Over 2026-2031, ultrasonic and hybrid laser-plasma rigs are expected to post the fastest 4.98% CAGR, yet they start from a narrower base. Supplier roadmaps bundle AI vision, automated nozzle changeovers, and predictive lens cleaning, further cementing fiber's hold on the cutting equipment market.

Semi-automated setups held 42.06% of the cutting equipment market size in 2025, reflecting widespread use of shuttle tables, nesting software, and operator-assisted loading. Plants enjoy flexibility while trimming manpower, making semi-auto the entry point for many SMEs. Yet fully robotic cells, integrating gantry loaders and AGVs, look set for a 5.07% CAGR through 2031 as ISO 10218-2:2025 eases cobot adoption.

Return-on-investment improves when multiple peripheral tasks, such as deburring and part sorting, join the same work cell. TRUMPF's sensors check suction-cup vacuum in real time, avoiding crashed cuts and raising lights-out reliability. Meanwhile, low-cost cobots with 15 kg payloads now operate at under USD 30,000, putting unattended night shifts within reach for job shops. These trends point to automation's rising share of the cutting equipment market, even if human-in-the-loop workflows persist.

The Cutting Equipment Market Report is Segmented by Technology (Laser, Plasma, and More), by Automation Level (Manual, Semi-Automated, and Robotic/Fully-automated), by End-User Industry (Automotive, Aerospace & Defense, and More), by Material Type (Ferrous Metals, Non-Ferrous Metals, Composites, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 48.62% of 2025 revenue and is on course for a 4.31% CAGR to 2031, buoyed by capacity additions across China, India, and the ASEAN corridor. HSG Laser's USD 68.3 million Jinan campus exemplifies the scale, promising 10,000 high-power units per year and shortening lead times for local buyers. Policy push for EVs, aerospace, and shipbuilding funnels continuous orders, while domestic toolmakers extend overseas after-sales centers to support exports.

North America holds a robust installed base and benefits from fresh incentives that defray upgrade costs. The Department of Energy's USD 40 million grant pool in 2024 subsidized efficiency retrofits for 219 factories across 38 states, accelerating fiber laser adoption. In addition, the USD 750 million Advanced Energy Manufacturing and Recycling program earmarks funds for plant rehabs in coal-impacted regions, nudging metal shops toward cleaner, automated lines. Canada's automotive cluster and Mexico's near-shoring boom further lift regional demand.

Europe leverages precision-engineering heritage and regulatory heft to sustain sales, even amid slower macro growth. Bystronic's Intelligent Cutting Process autonomy kit, winner of the Swiss Technology Award, underscores R&D leadership in fully unattended lasers. Germany drives global standards through DIN committees, shaping ISO rules that favor high-spec safety architectures. EU environmental directives also spur investments in composite recycling plants, indirectly pulling orders for ultrasonics and water-jets. Secondary growth pockets appear in the Middle East, Africa, and South America, where infrastructure build-outs prompt first-time purchases of mid-range plasma and oxy-fuel machines.

- TRUMPF SE + Co. KG

- Lincoln Electric Holdings, Inc.

- ESAB Corp. (ex-Colfax)

- Bystronic AG

- Hypertherm Associates

- IPG Photonics Corp.

- Mitsubishi Electric / Mazak Optonics

- Han's Laser Technology

- Messer Cutting Systems

- Flow International

- OMAX Corp.

- KMT Waterjet Systems

- Amada Miyachi

- Kennametal Inc.

- DAIHEN Corp.

- Koike Aronson, Inc.

- GCE Group

- Linde plc (Cutting gases)

- Prima Power

- Struers (sample-prep niche)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision-critical fabrication in EV/ICE automotive & aerospace

- 4.2.2 Industry 4.0 driven CNC/robotic automation surge

- 4.2.3 Manufacturing capacity boom across APAC

- 4.2.4 Post-pandemic cap-ex incentives for energy-efficient fiber lasers

- 4.2.5 Recycling of advanced composites requiring cold-cutting processes

- 4.2.6 Lightweight battery-housing demand in e-mobility platforms

- 4.3 Market Restraints

- 4.3.1 High upfront capital & integration costs

- 4.3.2 Global shortage of skilled CNC / CAM technicians

- 4.3.3 Supply-chain volatility for critical electronic & optical components

- 4.3.4 Garnet-abrasive scarcity disrupting water-jet OPEX

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Global Manufacturing-Sector Snapshot

- 4.9 Metalworking Industry Snapshot

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Technology

- 5.1.1 Laser

- 5.1.1.1 Fiber

- 5.1.1.2 CO2

- 5.1.1.3 Solid-state / Other

- 5.1.2 Plasma

- 5.1.2.1 High-definition

- 5.1.2.2 Conventional

- 5.1.3 Water-Jet

- 5.1.3.1 Abrasive

- 5.1.3.2 Pure

- 5.1.4 Flame / Oxy-fuel

- 5.1.5 Ultrasonic & Emerging

- 5.1.1 Laser

- 5.2 By Automation Level

- 5.2.1 Manual

- 5.2.2 Semi-automated

- 5.2.3 Robotic / Fully-automated

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace & Defense

- 5.3.3 Electrical & Electronics

- 5.3.4 Construction & Infrastructure

- 5.3.5 Metal-Fabrication Job Shops

- 5.3.6 Shipbuilding

- 5.3.7 Energy & Power

- 5.3.8 Others (Medical Devices, etc.)

- 5.4 By Material Type

- 5.4.1 Ferrous Metals

- 5.4.2 Non-Ferrous Metals

- 5.4.3 Composites

- 5.4.4 Glass/Ceramics/Stone

- 5.4.5 Others (Polymers/Plastics/Wood, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global overview, Core segments, Financials, Strategic info, Products, Recent developments)

- 6.4.1 TRUMPF SE + Co. KG

- 6.4.2 Lincoln Electric Holdings, Inc.

- 6.4.3 ESAB Corp. (ex-Colfax)

- 6.4.4 Bystronic AG

- 6.4.5 Hypertherm Associates

- 6.4.6 IPG Photonics Corp.

- 6.4.7 Mitsubishi Electric / Mazak Optonics

- 6.4.8 Han's Laser Technology

- 6.4.9 Messer Cutting Systems

- 6.4.10 Flow International

- 6.4.11 OMAX Corp.

- 6.4.12 KMT Waterjet Systems

- 6.4.13 Amada Miyachi

- 6.4.14 Kennametal Inc.

- 6.4.15 DAIHEN Corp.

- 6.4.16 Koike Aronson, Inc.

- 6.4.17 GCE Group

- 6.4.18 Linde plc (Cutting gases)

- 6.4.19 Prima Power

- 6.4.20 Struers (sample-prep niche)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

拉片切割设备市场:全球预测(按最终用户产业、技术、自动化程度、产品类型、应用和销售管道),2026-2032年盾形滚刀市场:依产品类型、材料、应用、最终用户、通路划分,全球预测(2026-2032)顶管机切割器市场:依切割器类型、土壤条件、直径范围、操作模式和应用划分-全球预测,2026-2032年全球微型/小型LED雷射切割设备市场:按应用、最终用户、雷射源、设备类型、雷射功率和分销渠道划分,2026-2032年预测工业PCB分板路由器市场依自动化程度、客户类型、PCB配置、分板方法、销售管道和最终用户产业划分,全球预测,2026-2032年

拉片切割设备市场:全球预测(按最终用户产业、技术、自动化程度、产品类型、应用和销售管道),2026-2032年盾形滚刀市场:依产品类型、材料、应用、最终用户、通路划分,全球预测(2026-2032)顶管机切割器市场:依切割器类型、土壤条件、直径范围、操作模式和应用划分-全球预测,2026-2032年全球微型/小型LED雷射切割设备市场:按应用、最终用户、雷射源、设备类型、雷射功率和分销渠道划分,2026-2032年预测工业PCB分板路由器市场依自动化程度、客户类型、PCB配置、分板方法、销售管道和最终用户产业划分,全球预测,2026-2032年 切割设备市场:依设备类型、依技术类型、依最终用户产业、按地区划分海底切割服务市场:依切割技术、作业模式、应用和最终用户产业划分,全球预测(2026-2032年)火焰切割服务市场按切割製程类型、材料类型、材料厚度、切割方式、服务提供者类型和终端用户产业划分-全球预测,2026-2032年切割机械市场按机器类型、电源、控制类型、机器尺寸、最终用户行业、应用和分销管道划分 - 全球预测,2025-2032

切割设备市场:依设备类型、依技术类型、依最终用户产业、按地区划分海底切割服务市场:依切割技术、作业模式、应用和最终用户产业划分,全球预测(2026-2032年)火焰切割服务市场按切割製程类型、材料类型、材料厚度、切割方式、服务提供者类型和终端用户产业划分-全球预测,2026-2032年切割机械市场按机器类型、电源、控制类型、机器尺寸、最终用户行业、应用和分销管道划分 - 全球预测,2025-2032 到 2030 年切割设备市场预测:按产品、材料、动力来源、营运模式、分销管道、最终用户和地区进行的全球分析

到 2030 年切割设备市场预测:按产品、材料、动力来源、营运模式、分销管道、最终用户和地区进行的全球分析