|

市场调查报告书

商品编码

1940554

应用容器:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Application Container - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

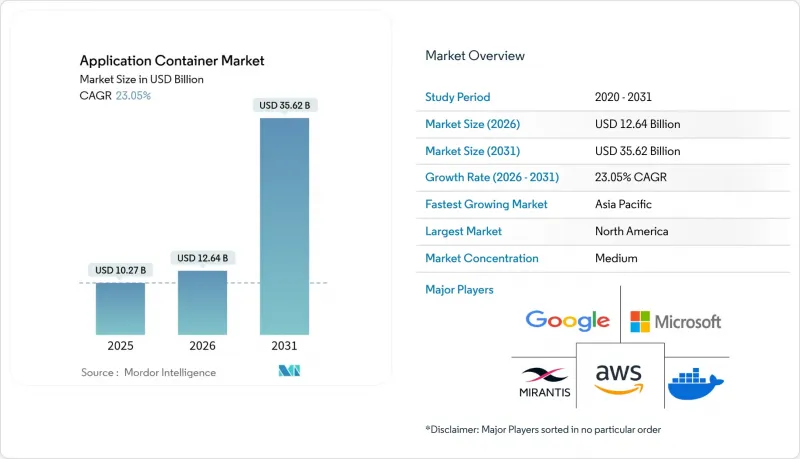

应用容器市场预计将从 2025 年的 102.7 亿美元成长到 2026 年的 126.4 亿美元,预计到 2031 年将达到 356.2 亿美元,2026 年至 2031 年的复合年增长率为 23.05%。

这一成长主要得益于企业加速向微服务转型、DevOps 管线的普及以及对混合云和多重云端架构日益增长的偏好。到 2024 年,平台解决方案将占总收入的 57.1%,这表明基于 Kubernetes 的编配将发挥核心作用。然而,随着企业寻求部署、迁移和託管方面的专业知识,服务领域的成长速度更快,年复合成长率 (CAGR) 达到 18.20%。公共云端部署以 64.3% 的市占率主导,但混合云和多重云端环境的成长速度最快,年复合成长率达到 24.50%,这主要受工作负载可移植性和合规性需求的驱动。大型企业保持着 68.2% 的市场份额,而中小企业也以 21.30% 的年复合成长率扩大采用率,因为託管容器服务的可用性降低了进入门槛。按产业垂直领域划分,IT 和电信(占 35.8%)的采用率仍然最高,而医疗保健产业则展现出最强劲的成长潜力,复合年增长率达到 19.70%,这主要得益于数位医疗政策和严格的资料隐私法规。

全球应用容器市场趋势与洞察

加速采用微服务架构

截至2025年,受访技术领导企业中容器化采用率将达到88%,微服务被视为关键驱动因素。德意志银行在其集中式平台上运作超过3100个活跃计划,透过容器化,已将其发布週期从六个月缩短至三週。将单体系统解耦为可独立部署的服务,实现了弹性扩展和高效的故障隔离。曼迪利银行等金融机构就是一个典型的例子:其数位银行基础设施现在每秒可处理12,000个请求,同时维持99.95%的运转率。这种架构转型也促成了持续交付方法的实施,使开发迭代与业务需求保持一致。因此,企业不仅将微服务视为一种开发方法,更将其视为加速产品上市的策略槓桿。

对混合云和多重云端敏捷性的需求

到 2024 年,76% 的企业将运行两个或多个公共云端,他们认为避免厂商锁定和提高监管柔软性是主要原因。加利西亚银行 (Banco Galicia) 整合了分布在本地和多个公共云端上的工作负载,并在采用统一的 Kubernetes 控制平面后,将停机时间减少了 40%。服务网格覆盖层现在可以安全地路由不同区域丛集之间的东西向流量,并提供统一的策略执行,而无需考虑底层提供者。基础架构即程式码 (IaC) 实务进一步标准化了资源配置,使企业能够根据价格、延迟和管治触发条件迁移工作负载,而无需重构程式码。由此带来的营运敏捷性正在推动应用容器市场的发展,使应用环境能够应对不断变化的合规性和效能限制。

容器安全漏洞和错误配置

容器平均有超过 600 个已知漏洞,97% 的受访团队对 Kubernetes 的安全状况表示担忧。 Gartner 预测,配置错误是最大的风险因素,到 2026 年,99% 的云端安全漏洞将由客户错误而非服务供应商缺陷造成。 NVIDIA Container Toolkit 中最近发现的一个漏洞(CVE-2024-0132,CVSS 9.0)揭示了一种潜在的主机资料外洩途径,威胁着多租户丛集的安全。儘管企业正在透过整合镜像扫描、运行时监控和零信任网路策略来应对,但技能短缺和工具氾滥使得应对措施更加复杂。在企业加强其端到端安全管道之前,安全问题可能会限制应用容器市场的复合年增长率 (CAGR)。

细分市场分析

到2025年,平台软体将占总营收的56.45%,企业将普遍采用OpenShift和Tanzu等Kubernetes发行版。然而,服务业务的复合年增长率将达到17.55%,超过所有其他细分市场。随着企业面临技能短缺和监管审核,应用容器即服务市场预计将持续扩张。咨询和託管服务能够加速新部署,同时降低将传统工作负载迁移到微服务架构的风险。多重云端环境日益复杂,进一步巩固了对整合合作伙伴和全天候支援服务的长期需求。

供应商的产品蓝图通常会将培训和财务营运指导与纯技术产品打包在一起。德意志银行与红帽公司的合作就是这种模式的典范,该银行利用红帽的架构师将发布週期缩短了三分之二,这表明知识转移可以像软体许可一样成为宝贵的资产。这种工具和专业知识的良性循环将使服务在预测期内成为应用容器市场中最具活力的收入来源。

到2025年,公共云端将占据63.55%的收入份额,这主要得益于Amazon EKS、Google GKE和Azure AKS等託管Kubernetes服务的成熟。然而,混合云和多重云端的采用率正以24.05%的复合年增长率快速成长,是整体应用容器市场成长率的两倍,这主要得益于企业分散运作以优化延迟、主权和正常运作时间。随着受监管产业将关键资料库迁移到私人区域,而无状态微服务仍保留在超大规模环境中,公共云端应用容器的市场份额可能会略有下降。

边缘网关、5G核心功能和AI推理丛集正在推动对裸机、虚拟化堆迭和公共IaaS进行统一管治的需求。加利西亚银行在部署多重云端网状网路后,停机时间减少了40%,这充分体现了统一策略引擎带来的营运优势。未来五年,工作负载部署决策将更受资料管辖权和永续性的限制,而非简单的运算价格,这将强化应用容器市场的混合设计模式。

区域分析

北美地区将贡献 2025 年 43.65% 的收入,这充分证明了其强大的 DevOps 文化、充裕的创业投资以及美国超大规模资料中心业者的主导地位。 Docker 近期完成的 Seacoa Capital主导的4,000 万美元 C 轮资金筹措,也显示投资者对其持续充满信心。联邦政府的现代化计画和金融科技领域的放鬆管制进一步推动了容器技术的普及。加拿大大力发展数位化医疗以及墨西哥蓬勃发展的电子商务,正将容器技术的应用范围扩展到北美最大的几个经济体之外。

亚太地区以22.35%的复合年增长率 (CAGR) 保持最快的成长速度。政府对智慧城市建设的津贴、行动商务交易量的激增以及5G部署正在推动中国、印度、日本和韩国等国发展容器化边缘基础设施。新加坡资讯通讯媒体发展局 (IMDA) 正在发放云端服务额度以降低Start-Ups的准入门槛,而澳洲各州政府机构正在试行基于Kubernetes的数位身分平台。这些因素共同推动亚太地区的应用容器市场规模以超过其他任何地区的速度成长。

欧洲在GDPR的基础上稳步推进,资料主权正从混合云部署的障碍转变为驱动力。德国的工业4.0工厂、法国的公共云端权力倡议以及英国的开放银行标准,都在增强对策略驱动型容器堆迭的需求。西班牙和荷兰的多厂商联盟表明,中型经济体可以透过采用云端原生蓝图标准,实现跨越式发展,超越传统基础设施。中东和非洲地区虽然落后,但正在加速发展,例如沙乌地阿拉伯一家能源集团正在部署容器进行预测性维护,南非一家银行正在实现零售通路的数位化。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 市场驱动因素

- 加速采用微服务架构

- 对混合云和多重云端敏捷性的需求

- DevOps 和 CI/CD 流水线的普及

- 资源优化和成本效益的需求

- 需要轻量级运行时的边缘原生AI工作负载

- 基于 ARM 的伺服器可提升容器效能

- 市场限制

- 容器安全漏洞和错误配置

- 大规模编配的复杂性

- 对开放原始码许可证合规性的不确定性

- 多区域部署中的资料主权约束

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业生态系分析

- 主要用例和案例研究

- 宏观经济趋势评估

- 投资分析

第五章 市场规模与成长预测

- 按组件

- 平台

- 服务

- 按部署模式

- 公共云端

- 私有云端

- 混合云端和多重云端

- 按组织规模

- 大公司

- 中小企业

- 按行业

- 资讯科技和电信

- BFSI

- 卫生保健

- 零售与电子商务

- 製造业

- 政府和公共部门

- 按字段分類的容器用例

- 管理与协调

- 监测

- DevOps 工具链

- 安全

- 网路

- 贮存

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 新加坡

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Red Hat, Inc.

- Mirantis, Inc.

- VMware, Inc.

- SUSE SE

- Canonical Ltd.

- Docker, Inc.

- Amazon Web Services, Inc.

- Google LLC

- Microsoft Corporation

- Oracle Corporation

- IBM Corporation

- Rancher Labs, Inc.

- Alibaba Cloud Computing Co., Ltd.

- Hewlett Packard Enterprise Company

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Portainer Ltd.

- Heroku LLC(Salesforce, Inc.)

- NetApp, Inc.

- HashiCorp, Inc.

第七章 市场机会与未来展望

The application container market is expected to grow from USD 10.27 billion in 2025 to USD 12.64 billion in 2026 and is forecast to reach USD 35.62 billion by 2031 at 23.05% CAGR over 2026-2031.

Strong enterprise migration toward micro-services, the proliferation of DevOps pipelines and the growing preference for hybrid, multi-cloud architectures are sustaining this momentum. Platform solutions accounted for 57.1% revenue in 2024, reflecting the central role of Kubernetes-based orchestration, yet services are expanding faster at an 18.20% CAGR as organizations seek implementation, migration, and managed expertise . Public-cloud deployments led with 64.3% share, but hybrid and multi-cloud setups are the fastest risers at 24.50% CAGR, driven by workload portability and compliance demands. Large enterprises retained a 68.2% share, although small and medium enterprises are scaling adoption at a 21.30% CAGR as managed container offerings lower entry barriers. Industry uptake remains highest in IT and telecom (35.8% share), while healthcare shows the strongest vertical upside at 19.70% CAGR, propelled by digital health mandates and stringent data-privacy regulations.

Global Application Container Market Trends and Insights

Accelerating Adoption of Micro-services Architecture

Container penetration reached 88% among surveyed technology leaders in 2025, with micro-services framed as the principal catalyst . Deutsche Bank's centralized platform runs more than 3,100 active projects and cut release cycles from six months to three weeks once workloads were containerized. Decoupling monoliths into independently deployable services enables elastic scaling and streamlined incident isolation, illustrated by financial institutions such as Bank Mandiri, whose digital banking backbone now processes 12,000 requests per second while sustaining 99.95% uptime. The architectural shift has also unlocked continuous delivery patterns that align development sprints with business imperatives. As a result, enterprises view micro-services not merely as a development paradigm but as a strategic lever for time-to-market acceleration.

Demand for Hybrid and Multi-Cloud Agility

Seventy-six percent of organizations operated two or more public clouds in 2024, citing vendor lock-in avoidance and regulatory flexibility as top rationales. Banco Galicia consolidated disparate workloads across on-premises and multiple public clouds, realizing a 40% downtime reduction after adopting a unified Kubernetes control plane. Service-mesh overlays now route east-west traffic securely among clusters residing in different regions, providing uniform policy enforcement regardless of underlying provider. Infrastructure-as-Code practices further standardize provisioning, allowing enterprises to shift workloads in response to price, latency or governance triggers without refactoring code. The resulting operational agility propels the application container market as organizations future-proof application estates against evolving compliance and performance constraints.

Container Security Vulnerabilities and Misconfigurations

Containers harbor more than 600 disclosed vulnerabilities on average, and 97% of surveyed teams voice concerns about Kubernetes security posture. Misconfigurations top the risk list, prompting Gartner to forecast that 99% of cloud breaches will stem from customer error rather than provider flaws by 2026. A recent NVIDIA Container Toolkit flaw (CVE-2024-0132, CVSS 9.0) illustrated potential host-escape vectors that threaten multi-tenant clusters. Enterprises respond by integrating image scanning, runtime monitoring, and zero-trust network policies, yet skills gaps and tool sprawl complicate remediation. Until organizations harden pipelines end-to-end, security fears will temper the CAGR of the application container market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in DevOps and CI/CD Pipelines

- Need for Resource Optimization and Cost Efficiency

- Complexity of Large-Scale Orchestration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform software constituted 56.45% of 2025 revenue as enterprises standardized on Kubernetes distributions such as OpenShift and Tanzu, yet services exhibited an 17.55% CAGR that outpaced every other component. The application container market size for services is projected to swell as firms confront skills shortages and regulatory audits. Consulting and managed engagements accelerate greenfield rollouts while de-risking migrations of legacy workloads into micro-services. The rising complexity of multi-cloud estates further cements long-term demand for integration partners and 24x7 support desks.

Vendor roadmaps now bundle training and FinOps guidance alongside pure technology deliverables. Deutsche Bank's partnership with Red Hat exemplifies the model: the bank leaned on vendor architects to cut release cycles by two-thirds, proving that knowledge transfer can be as valuable as software licenses. The virtuous loop of tooling plus expertise positions services as the most vibrant profit pool within the application container market over the forecast horizon.

Public cloud captured 63.55% of revenue in 2025, a figure buoyed by the maturity of managed Kubernetes offerings like Amazon EKS, Google GKE, and Azure AKS. However, hybrid and multi-cloud footprints are scaling at a 24.05% CAGR-double the broader application container market-because companies now distribute workloads to optimize latency, sovereignty, and uptime. The application container market share for public cloud may narrow modestly as regulated industries shift critical databases to private regions while keeping stateless micro-services at hyperscale.

Edge gateways, 5G core functions, and AI inference clusters intensify the need for uniform governance spanning bare metal, virtualized stacks, and public IaaS. Banco Galicia's 40% downtime reduction after adopting a multi-cloud mesh demonstrates the operational upside of unified policy engines. Over the next five years, workload placement decisions will hinge less on raw compute pricing and more on data jurisdiction and sustainability constraints, reinforcing hybrid design patterns across the application container market.

Application Container Market Report is Segmented by Component (Platform and Services), Deployment Model (Public Cloud, Private Cloud and Hybrid and Multi-Cloud), Organization Size (Large Enterprises, and SMEs), Industry Vertical (IT and Telecom, BFSI, and More), Container Use-Case Area (Management and Orchestration, Monitoring, Devops Tool-Chain, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America produced 43.65% of 2025 revenue, a testament to entrenched DevOps cultures, abundant venture capital and the dominance of U.S. hyperscalers. Docker's recent USD 40 million Series C, steered by Sequoia Capital, typifies continued investor confidence. Federal modernization programs and fintech deregulation further spur adoption. Canada's healthcare digitization push and Mexico's e-commerce boom extend North America's container footprint beyond its largest economy.

Asia-Pacific records the steepest growth profile at 22.35% CAGR. Government smart-city grants, surging mobile-commerce volumes, and 5G rollouts stimulate containerized edge infrastructure in China, India, Japan, and South Korea. Singapore's Infocomm Media Development Authority allocates cloud credits that lower onboarding costs for start-ups, while Australian state agencies pilot Kubernetes-based digital-identity platforms. Collectively these efforts grow the application container market size across APAC faster than any other region.

Europe maintains steady progress underpinned by GDPR, which turns data sovereignty from an obstacle to an enabler for hybrid adoption. Germany's Industrie 4.0 factories, France's public-cloud sovereignty initiative, and the United Kingdom's open-banking benchmarks reinforce demand for policy-aware container stacks. Multi-vendor alliances in Spain and the Netherlands show how mid-tier economies can leapfrog legacy infrastructure by standardizing on cloud-native blueprints. The Middle East and Africa trail but accelerate as energy conglomerates in Saudi Arabia deploy containers for predictive maintenance and South African banks digitize retail channels.

- Red Hat, Inc.

- Mirantis, Inc.

- VMware, Inc.

- SUSE SE

- Canonical Ltd.

- Docker, Inc.

- Amazon Web Services, Inc.

- Google LLC

- Microsoft Corporation

- Oracle Corporation

- IBM Corporation

- Rancher Labs, Inc.

- Alibaba Cloud Computing Co., Ltd.

- Hewlett Packard Enterprise Company

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Portainer Ltd.

- Heroku LLC (Salesforce, Inc.)

- NetApp, Inc.

- HashiCorp, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating adoption of micro-services architecture

- 4.2.2 Demand for hybrid and multi-cloud agility

- 4.2.3 Surge in DevOps and CI/CD pipelines

- 4.2.4 Need for resource optimisation and cost efficiency

- 4.2.5 Edge-native AI workloads needing lightweight runtimes

- 4.2.6 Arm-based servers boosting container performance

- 4.3 Market Restraints

- 4.3.1 Container security vulnerabilities and misconfigurations

- 4.3.2 Complexity of large-scale orchestration

- 4.3.3 Open-source licence-compliance uncertainty

- 4.3.4 Data-sovereignty limits on multi-region deployment

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Use Cases and Case Studies

- 4.10 Assessment of Macroeconomic Trends

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid and Multi-Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Retail and e-Commerce

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.5 By Container Use-Case Area

- 5.5.1 Management and Orchestration

- 5.5.2 Monitoring

- 5.5.3 DevOps Tool-chain

- 5.5.4 Security

- 5.5.5 Networking

- 5.5.6 Storage

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Colombia

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Red Hat, Inc.

- 6.4.2 Mirantis, Inc.

- 6.4.3 VMware, Inc.

- 6.4.4 SUSE SE

- 6.4.5 Canonical Ltd.

- 6.4.6 Docker, Inc.

- 6.4.7 Amazon Web Services, Inc.

- 6.4.8 Google LLC

- 6.4.9 Microsoft Corporation

- 6.4.10 Oracle Corporation

- 6.4.11 IBM Corporation

- 6.4.12 Rancher Labs, Inc.

- 6.4.13 Alibaba Cloud Computing Co., Ltd.

- 6.4.14 Hewlett Packard Enterprise Company

- 6.4.15 Cisco Systems, Inc.

- 6.4.16 Palo Alto Networks, Inc.

- 6.4.17 Portainer Ltd.

- 6.4.18 Heroku LLC (Salesforce, Inc.)

- 6.4.19 NetApp, Inc.

- 6.4.20 HashiCorp, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

应用容器市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

应用容器市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 应用容器市场 - 全球产业规模、份额、趋势、机会、预测:按服务、平台、组织规模、地区和竞争对手划分,2021-2031 年

应用容器市场 - 全球产业规模、份额、趋势、机会、预测:按服务、平台、组织规模、地区和竞争对手划分,2021-2031 年 PP圆形容器市场依产品类型、产能、製造流程、终端用户产业及通路划分,全球预测(2026-2032年)

PP圆形容器市场依产品类型、产能、製造流程、终端用户产业及通路划分,全球预测(2026-2032年) 应用容器市场规模、份额和成长分析(按服务、部署模式、应用领域和地区划分)-产业预测(2026-2033 年)

应用容器市场规模、份额和成长分析(按服务、部署模式、应用领域和地区划分)-产业预测(2026-2033 年) 应用容器市场规模、份额、趋势分析报告:按服务、部署、公司规模、最终用途、地区、细分市场预测,2025 年至 2030 年

应用容器市场规模、份额、趋势分析报告:按服务、部署、公司规模、最终用途、地区、细分市场预测,2025 年至 2030 年 全球应用容器市场,2024-2028

全球应用容器市场,2024-2028 全球应用容器市场规模(按地区、范围和预测)

全球应用容器市场规模(按地区、范围和预测) 全球应用程式容器市场规模研究,按服务、类型、组织规模、部署、应用程式、最终用户和区域预测 2022-2032

全球应用程式容器市场规模研究,按服务、类型、组织规模、部署、应用程式、最终用户和区域预测 2022-2032