|

市场调查报告书

商品编码

1940566

伺服马达及驱动器:市场占有率分析、产业趋势及统计数据、成长预测(2026-2031)Servo Motors And Drives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

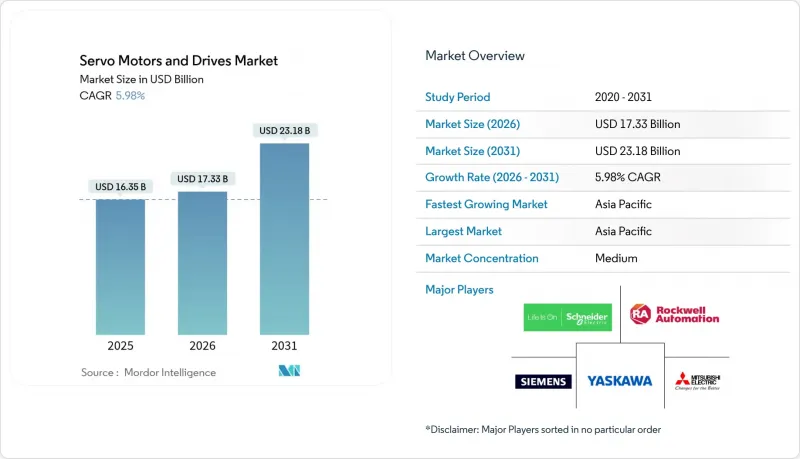

伺服马达和驱动器市场预计将从 2025 年的 163.5 亿美元成长到 2026 年的 173.3 亿美元,预计到 2031 年将达到 231.8 亿美元,2026 年至 2031 年的复合年增长率为 5.98%。

这一成长主要得益于工厂对联网运动系统的升级改造,这些系统融合了碳化硅功率电子装置、数位双胞胎模拟和协作机器人技术。半导体工厂和精密封装生产线采用线性设计以消除机械平移,而汽车製造商则投资于电池和电力驱动桥组装的中压高功率解决方案。能源效率法规迫使製造商用IE4级伺服封装取代感应电机,而800V电动车架构的扩展则推动了对高压驱动器的需求。来自碳化硅专家和网路安全供应商日益激烈的竞争,正迫使传统製造商将机械技术与数位智慧结合。

全球伺服马达和驱动器市场趋势及洞察

工业自动化快速发展和智慧工厂的引入

2024年,一家德国汽车集团将其多轴机器人单元连接到数位双胞胎平台,以缩短生产线切换时间并提高生产效率。在安装了FANUC伺服驱动生产线后,Closure Systems International公司的整体设备效率(OEE)提升至97.5%,计画外停机时间降至2.5%。支援EtherCAT的驱动器可在微秒级内同步操作,从而支援弹性製造,并为基于5G的机器协作铺平道路。

协作机器人和移动机器人的应用日益普及

协作机器人需要结构紧凑、符合安全标准且内建扭力感测功能的致动器。安川马达的C系列致动器符合ISO/TS 15066:2016力限制标准,并嵌入式监控功能,可实现组装上的人机直接互动。科尔摩根提供的高扭矩密度马达驱动全球约一百万个机器人关节,这表明伺服马达和驱动器市场正朝着轻量化、用户友好平台的方向发展。

高初始成本与感应马达/步进马达替代方案的比较

印度和东南亚的中小型製造商通常选择价格较高的伺服组件,而不是变频驱动感应马达。然而,《包装世界》的一项研究发现,考虑到降低生命週期能耗和维护成本的优势,伺服再次展现出其优越性。以电动执行致动器取代气压致动器,可显着降低年度营运成本,从7,320美元降至388.8美元。

细分市场分析

到2025年,伺服马达和驱动器市场份额将达到65.02%,这主要得益于三相电网和成熟的生产线有利于旋转式设计的发展。线性设计则广泛应用于半导体封装、微影和高速装盒等领域,并以9.64%的复合年增长率成长。德尔科的装盒生产线透过取消旋转式到线性式的转换,实现了高产能。

线性模型的功能已超越了简单的定位。 Tolomatic伺服压力机的效率比液压压力机(50%)高出80%,吸引了那些需要卫生、无油操作的包装公司的注意。平台供应商也积极回应,推出了分散式驱动系统,例如罗克韦尔自动化公司的ArmorKinetix,该系统可将布线减少90%,安装时间缩短30%。

低压设备保持了61.88%的市场份额,而1-35kV等级的设备则以每年7.05%的速度增长,这主要得益于工厂采用更高电压架构以减小电缆尺寸和发热量。艾睿电子重点介绍了碳化硅MOSFET,这种元件具有更高的开关频率和更低的损耗。中压驱动器则为电动汽车马达外壳製造中使用的100kW以上工具机提供支持,以满足日益增长的扭矩需求。

西门子推出了超低压单元 MICRO-DRIVE,用于需要安全 24-48V 电压等级的自主移动机器人;同时,800V 电动汽车产品线采用中压伺服来减小导体直径和电阻损耗,从而在伺服电机和驱动器市场中获得一个虽小但不断增长的份额。

伺服马达和驱动器市场报告按产品类型(马达、驱动器)、电压范围(低压≤1kV、中压1kV-35kV、高压>35kV)、用户产业(汽车和电动汽车製造、石油和天然气、医疗和医疗设备、包装和标籤等)、功率等级(<1kW、1kW-5kW、5-155kW>5kW15kW)。

区域分析

到2025年,亚太地区将占全球收入的45.92%,这主要得益于中国电子产品生产、日本的技术领先地位以及印度工厂的扩张。该地区维持最高的成长率,年复合成长率达7.62%,主要得益于东南亚国协为增强自身竞争力而大力推进自动化。中国在稀土元素供应方面的优势降低了当地成本,但出口限制对海外买家造成了影响。日本谐波驱动系统公司已加强在东京和长野的技术丛集建设,目标是2026财年实现900亿日圆的净销售额。

北美扩大了製造业回流计划,以增强供应链的韧性。三菱电机在肯塔基州投资1.435亿美元兴建的压缩机工厂,反映了在地化生产和缩短前置作业时间的趋势。日立收购Joliet Electric Motors公司,扩大了售后服务范围,以提升其已安装设备的生命週期价值。协作机器人在美国的日益普及,抵消了重工业成长放缓的影响。

欧洲重点关注脱碳数位双胞胎分析。 IE4法规推动了德国和北欧国家的维修需求,而网路安全问题则促使美国网路安全和基础设施安全局(CISA)在ABB Drive Composer和Rockwell Powerflex中发现韧体漏洞后展开审核。随着汽车製造商向800V电池生产线转型,中压驱动器在巴伐利亚和Piemonte的汽车产业丛集中迅速渗透,儘管面临宏观经济压力,仍保持了中等个位数的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 工业自动化快速发展和智慧工厂的引入

- 协作机器人和移动机器人的日益普及

- 严格的全球和区域能源效率法规

- 推进汽车製造和电动车平台的电气化

- 碳化硅功率模组提高伺服驱动效率

- 利用数位双胞胎技术对伺服系统进行预测性尺寸设计与最佳化

- 市场限制

- 初始成本高昂与感应马达/步进马达替代方案相比

- 低成本步进马达和变频器控制的感应电动机已广泛应用

- 高等级稀土元素永磁体的供应链风险

- 连网伺服驱动器因网路漏洞停止运作

- 重要法规结构评估

- 价值链分析

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 关键相关人员影响评估

- 主要用例和案例研究

- 宏观经济因素对市场的影响

- 投资分析

第五章 市场区隔

- 依产品类型

- 引擎

- 交流伺服电机

- 直流无刷伺服电机

- 有刷直流伺服电机

- 直线伺服电机

- 驾驶

- 交流伺服驱动器

- 直流伺服驱动器

- 可调/多轴伺服驱动器

- 引擎

- 按电压范围

- 低电压(1千伏特或以下)

- 中压(1千伏至35千伏)

- 高压(超过35千伏特)

- 按最终用户行业划分

- 汽车和电动车 (EV) 製造

- 石油和天然气(上游、中游、下游)

- 医疗和医疗设备

- 包装和标籤

- 半导体和电子学

- 化学品和石油化工

- 食品/饮料

- 其他行业(纺织、印刷等)

- 额定功率

- 小于1千瓦

- 1kW~5kW

- 5kW~15kW

- 超过15千瓦

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- ASEAN

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- Rockwell Automation, Inc.

- ABB Ltd.

- Delta Electronics, Inc.

- FANUC Corporation

- Kollmorgen Corporation(Regal Rexnord Corporation)

- Bosch Rexroth AG

- Panasonic Holdings Corporation

- Nidec Corporation

- Omron Corporation

- Oriental Motor Co., Ltd.

- Lenze SE

- Parker-Hannifin Corporation

- Inovance Technology Co., Ltd.

- Moog Inc.

- WEG Equipamentos El-tricos SA

- Emerson Electric Co.

- AMETEK, Inc.

- TECO Electric & Machinery Co., Ltd.

- Nanotec Electronic GmbH & Co. KG

- SANYO DENKI Co., Ltd.

- Fuji Electric Co., Ltd.

第七章 市场机会与未来展望

The servo motors and drives market is expected to grow from USD 16.35 billion in 2025 to USD 17.33 billion in 2026 and is forecast to reach USD 23.18 billion by 2031 at 5.98% CAGR over 2026-2031.

Growth stemmed from factories upgrading to networked motion systems that combine silicon-carbide power electronics, digital twin simulation and collaborative robotics. Semiconductor plants and precision packaging lines adopted linear designs to eliminate mechanical conversions, while automotive producers invested in mid-voltage, high-power solutions for battery and e-axle assembly. Energy-efficiency legislation prompted manufacturers to replace induction units with IE4-class servo packages, and the expanding 800 V electric-vehicle architecture spurred demand for higher-voltage drives. Intensifying competition arrived from silicon-carbide specialists and cybersecurity vendors, pressuring traditional incumbents to blend mechanical expertise with digital intelligence.

Global Servo Motors And Drives Market Trends and Insights

Rapid industrial automation and smart-factory rollout

During 2024, automotive groups in Germany connected multi-axis robotic cells to digital-twin platforms, cutting line-change times and increasing throughput. Closure Systems International lifted overall equipment effectiveness to 97.5% after installing FANUC servo-driven lines that dropped unplanned downtime to 2.5%. EtherCAT-enabled drives synchronised motion within microseconds, supporting flexible manufacturing and paving the way for 5G-based machine coordination.

Rising adoption of collaborative and mobile robotics

Cobots require compact, safety-rated actuators with integrated torque sensing. Yaskawa's HC series met ISO/TS 15066:2016 force limits through embedded monitoring, allowing direct human interaction on assembly lines. High-torque-density motors supplied by Kollmorgen powered almost 1 million robotic joints worldwide, demonstrating the servo motors and drives market's shift toward lighter, user-friendly platforms.

High upfront cost vs. induction/stepper alternatives

Small manufacturers in India and Southeast Asia compared premium servo packages with variable-frequency-drive induction sets and frequently chose the latter. Yet studies by Packaging World showed lifetime energy and maintenance savings tilting favour back toward servos, with annual operating cost dropping from USD 7,320 to USD 388.8 when pneumatics were replaced by electric actuators.

Other drivers and restraints analyzed in the detailed report include:

- Stringent global and regional energy-efficiency mandates

- Electrification push in automotive manufacturing and EV platforms

- Supply-chain risk for high-grade rare-earth permanent magnets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AC units kept 65.02% of the servo motors and drives market in 2025 because three-phase grids and mature manufacturing lines favoured rotary designs. Linear variants captured semiconductor packaging, lithography and high-speed cartooning, expanding at 9.64% CAGR. Delkor's cartoning lines achieved higher throughputs by eliminating rotary-to-linear conversions.

Linear models extended beyond simple positioning. Tolomatic servo presses delivered 80% efficiency versus 50% for hydraulics, attracting packaging firms that needed hygienic, oil-free motion. Platform suppliers responded with distributed drives such as Rockwell Automation's ArmorKinetix, cutting cabling 90% and installation time 30%.

Low-voltage installations held 61.88% share but the 1-35 kV class grew 7.05% annually as plants adopted higher-voltage architectures to reduce cable size and heat. Arrow Electronics highlighted silicon-carbide MOSFETs running at higher switching frequencies with lower losses. Medium-voltage drives supported 100 kW-plus machine tools used for EV motor housings, matching growing torque demands.

Siemens introduced MICRO-DRIVE extra-low-voltage units for autonomous mobile robots that need safe 24-48 V levels. Conversely, 800 V EV lines deployed mid-voltage servos to shrink conductor diameters and lower resistive loss, holding a niche but rising share in the servo motors and drives market.

The Servo Motors and Drives Market Report is Segmented by Product Type (Motor, and Drive), Voltage Range (Low Voltage <=1kV, Medium Voltage 1kV-35kV, and High Voltage >35kV), End-User Industry (Automotive and EV Manufacturing, Oil and Gas, Healthcare and Medical Devices, Packaging and Labelling, and More), Power Rating (<=1kW, 1kW-5kW, 5kW-15kW, and >15kW), and Geography.

Geography Analysis

Asia-Pacific captured 45.92% of global revenue in 2025 on the back of Chinese electronics production, Japanese technology leadership and India's factory expansions. Regional growth remained the fastest at 7.62% CAGR as ASEAN nations incentivised automation to raise competitiveness. China's dominance in rare-earth supply lowered local costs but exposed foreign buyers to export controls. Japan's Harmonic Drive Systems aimed for JPY 90 billion net sales by FY 2026, reinforcing the technology cluster in Tokyo and Nagano.

North America increased its reshoring programmes to improve supply resilience. Mitsubishi Electric's USD 143.5 million compressor plant in Kentucky illustrated the trend toward localised production and shorter lead times. Hitachi's purchase of Joliet Electric Motors broadened aftermarket services, supporting lifecycle value across installed fleets. Rising collaborative-robot utilisation in the United States offset softness in heavy industry.

Europe focused on decarbonisation and digital-twin analytics. IE4 mandates spurred retrofits in Germany and the Nordics, while cybersecurity concerns prompted audits after CISA flagged vulnerabilities in ABB Drive Composer and Rockwell PowerFlex firmware. Medium-voltage drives penetrated automotive clusters in Bavaria and Piedmont as OEMs migrated to 800 V battery lines, sustaining mid-single-digit growth despite macroeconomic pressures.

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- Rockwell Automation, Inc.

- ABB Ltd.

- Delta Electronics, Inc.

- FANUC Corporation

- Kollmorgen Corporation (Regal Rexnord Corporation)

- Bosch Rexroth AG

- Panasonic Holdings Corporation

- Nidec Corporation

- Omron Corporation

- Oriental Motor Co., Ltd.

- Lenze SE

- Parker-Hannifin Corporation

- Inovance Technology Co., Ltd.

- Moog Inc.

- WEG Equipamentos El-tricos S.A.

- Emerson Electric Co.

- AMETEK, Inc.

- TECO Electric & Machinery Co., Ltd.

- Nanotec Electronic GmbH & Co. KG

- SANYO DENKI Co., Ltd.

- Fuji Electric Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid industrial automation and smart-factory rollout

- 4.2.2 Rising adoption of collaborative and mobile robotics

- 4.2.3 Stringent global and regional energy-efficiency mandates

- 4.2.4 Electrification push in automotive manufacturing and EV platforms

- 4.2.5 Silicon-carbide power modules boosting servo-drive efficiency

- 4.2.6 Digital-twin-enabled predictive sizing and optimisation of servo systems

- 4.3 Market Restraints

- 4.3.1 High upfront cost vs. induction/stepper alternatives

- 4.3.2 Proliferation of low-cost stepper and VFD-controlled induction motors

- 4.3.3 Supply-chain risk for high-grade rare-earth permanent magnets

- 4.3.4 Cyber-vulnerabilities in networked servo drives causing downtime

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Motor

- 5.1.1.1 AC Servo Motor

- 5.1.1.2 DC Brushless Servo Motor

- 5.1.1.3 Brushed DC Servo Motor

- 5.1.1.4 Linear Servo Motor

- 5.1.2 Drive

- 5.1.2.1 AC Servo Drive

- 5.1.2.2 DC Servo Drive

- 5.1.2.3 Adjustable / Multi-axis Servo Drive

- 5.1.1 Motor

- 5.2 By Voltage Range

- 5.2.1 Low Voltage (<=1 kV)

- 5.2.2 Medium Voltage (1 kV-35 kV)

- 5.2.3 High Voltage (>35 kV)

- 5.3 By End-user Industry

- 5.3.1 Automotive and EV Manufacturing

- 5.3.2 Oil and Gas (Up-, Mid-, Down-stream)

- 5.3.3 Healthcare and Medical Devices

- 5.3.4 Packaging and Labelling

- 5.3.5 Semiconductor and Electronics

- 5.3.6 Chemicals and Petrochemicals

- 5.3.7 Food and Beverage

- 5.3.8 Other Industries (Textile, Printing, etc.)

- 5.4 By Power Rating

- 5.4.1 ?1 kW

- 5.4.2 1 kW-5 kW

- 5.4.3 5 kW-15 kW

- 5.4.4 >15 kW

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Yaskawa Electric Corporation

- 6.4.2 Mitsubishi Electric Corporation

- 6.4.3 Siemens AG

- 6.4.4 Schneider Electric SE

- 6.4.5 Rockwell Automation, Inc.

- 6.4.6 ABB Ltd.

- 6.4.7 Delta Electronics, Inc.

- 6.4.8 FANUC Corporation

- 6.4.9 Kollmorgen Corporation (Regal Rexnord Corporation)

- 6.4.10 Bosch Rexroth AG

- 6.4.11 Panasonic Holdings Corporation

- 6.4.12 Nidec Corporation

- 6.4.13 Omron Corporation

- 6.4.14 Oriental Motor Co., Ltd.

- 6.4.15 Lenze SE

- 6.4.16 Parker-Hannifin Corporation

- 6.4.17 Inovance Technology Co., Ltd.

- 6.4.18 Moog Inc.

- 6.4.19 WEG Equipamentos El-tricos S.A.

- 6.4.20 Emerson Electric Co.

- 6.4.21 AMETEK, Inc.

- 6.4.22 TECO Electric & Machinery Co., Ltd.

- 6.4.23 Nanotec Electronic GmbH & Co. KG

- 6.4.24 SANYO DENKI Co., Ltd.

- 6.4.25 Fuji Electric Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

无铁心直线伺服马达市场:依马达类型、行程长度、工作电压、组件、安装方式、应用、终端用户产业划分,全球预测,2026-2032年

无铁心直线伺服马达市场:依马达类型、行程长度、工作电压、组件、安装方式、应用、终端用户产业划分,全球预测,2026-2032年 数位伺服马达及驱动器市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型、设备划分

数位伺服马达及驱动器市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型、设备划分 全球交流伺服马达及驱动器市场规模、份额、趋势及成长分析报告(2026-2034年)全球伺服马达市场规模、份额、趋势和成长分析报告(2026-2034)

全球交流伺服马达及驱动器市场规模、份额、趋势及成长分析报告(2026-2034年)全球伺服马达市场规模、份额、趋势和成长分析报告(2026-2034) 伺服马达和驱动器市场报告:按产品类型、电压范围、系统、通讯协定、最终用户产业和地区划分(2026-2034 年)

伺服马达和驱动器市场报告:按产品类型、电压范围、系统、通讯协定、最终用户产业和地区划分(2026-2034 年) 2026年全球伺服马达及驱动器市场报告2026年全球类比伺服马达及驱动器市场报告

2026年全球伺服马达及驱动器市场报告2026年全球类比伺服马达及驱动器市场报告 直流伺服马达及驱动器市场:机会、成长要素、产业趋势分析及预测(2026-2035年)交流伺服系统市场伺服类型、马达类型、回馈类型、控制类型、输出转矩范围和应用划分-全球预测,2026-2032年交流伺服马达市场按类型、输出功率、产品、分销管道、回馈方式和应用划分-全球预测(2026-2032)

直流伺服马达及驱动器市场:机会、成长要素、产业趋势分析及预测(2026-2035年)交流伺服系统市场伺服类型、马达类型、回馈类型、控制类型、输出转矩范围和应用划分-全球预测,2026-2032年交流伺服马达市场按类型、输出功率、产品、分销管道、回馈方式和应用划分-全球预测(2026-2032)