|

市场调查报告书

商品编码

1940567

声学摄影机:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Acoustic Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

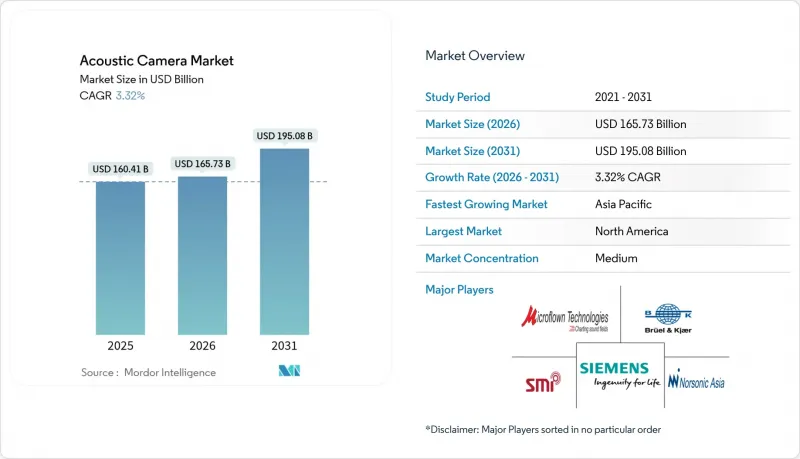

预计声学相机市场将从 2025 年的 1,604.1 亿美元成长到 2026 年的 1,657.3 亿美元,到 2031 年将达到 1950.8 亿美元,2026 年至 2031 年的复合年增长率为 3.32%。

随着MEMS麦克风阵列成本的下降和紧凑型边缘AI处理器的出现,系统物料清单成本已降至5000美元以下,声学成像技术正从研究实验室走向工厂车间和城市街道。市政部门正在部署噪音执法摄像头,汽车工程师正在将电动车的NVH测试数位化,公共产业正在将波束成形模组与预测性维护平台结合。边缘分析现在可以在设备端运行,这不仅扩展了远端资产的应用场景,还降低了云端频宽和延迟。竞争的重点不再是规模,而是演算法效率和软体生态系统,这使得小众创新者能够与各种测试设备巨头竞争。

全球声学相机市场趋势与洞察

加强全球城市噪音管制

市政机构正逐步淘汰点式声级计,转而采用太空成像技术,将违规行为归因于特定车辆。到2024年,欧洲和北美的城市将陆续安装基于摄影机的噪音雷达,例如SoundVue等解决方案可提供符合法律证据要件的1级精度。欧盟的目标是到2030年将交通噪音降低30%,这推动了对坚固耐用的户外声学摄影机的长期采购。固定式路边设备正逐渐取代移动拖车,多年期硬体需求和服务合约也成为常态。

电动出行平台NVH数位化快速发展

电动动力传动系统消除了内燃机的掩蔽效应,从而揭示了马达、逆变器和空调管道独特的声学特征。汽车製造商正在增加2024年的声学测试预算,现代汽车已部署3D扫描设备来绘製整个车内空间的声学图谱。即时波束成形技术使工程师能够在实际驾驶条件下可视化辐射模式,从而在生产开始前完成修正。越来越多的商用货车和城市公车也采用类似的调查方法,以满足舒适性和当地噪音认证法规的要求。

3D MEMS阵列元件的初始投资较高

由于数百个相位匹配麦克风、精密外壳和高频宽转换器的材料和组装成本高昂,测量级 3D 配置的成本可能超过 10 万美元。目前,光学 MEMS 麦克风的信噪比可达 80 dB,但製程工具的学习曲线和产量比率限制了价格的大幅下降。在成本低于 5 万美元的模组化阵列普及之前,小型公司通常会使用共用实验室或租赁 3D 系统。

细分市场分析

截至2025年,二维声学相机将凭藉其久经考验的可靠性和低廉的价格,维持52.40%的市场份额。它们在工厂洩漏检测和汽车零件检测领域占据主导地位。同时,受客舱噪音映射、城市空中运输测试以及复杂机械机壳内全空间定位等需求的推动,3D相机将以16.03%的复合年增长率增长。配备192个麦克风的八角形系统可提供20 Hz至10 频宽的解析度。随着MEMS成本的下降,三维平台声学相机的市场规模预计将缩小与主流产品的差距。利用人工智慧的模式识别技术的改进提高了检测精度,使得更小的孔径也能实现相当的性能。系统整合商正在CAD仪表板中整合即时视觉化功能,使工程师能够在几分钟内而非几天内完成声学处理方案的检验。这种简化的工作流程也使得航太和豪华汽车领域的产品价格更高。 2024 年出货的 3D 阵列原型售价低于 6 万美元,这标誌着中型供应商和大学实验室对 3D 阵列的采用率正在不断提高。

由于采用完善的标准和可控制的环境,近距离测量系统预计在2025年将占总收入的60.30%。舱室测试、变速箱分析和桌面研发是其主要应用场景。受风力发电机噪音审核、智慧城市声学测绘和飞机飞越测试等领域进展的推动,对长程测量的需求正以14.55%的复合年增长率增长。最小方差失真抑制响应演算法能够分离50公尺以外的声源,即使在背景杂讯强烈的环境中也能实现。因此,预计到2031年,长程声音相机市场的规模将翻倍。基础设施管理人员正在将数据整合到地理空间仪表板中,并将声学指标迭加到设施蓝图上,以加快维修人员的调度。

现场操作人员青睐坚固耐用的 IP65+机壳和低功耗边缘处理器,这些处理器可透过 4G 或 LoRaWAN 传输警报讯息。注重安装便利性和云端 API 的供应商在市政竞标和可再生能源发电电厂专案中屡获订单。

声学相机市场按阵列类型(二维阵列、3D阵列)、测量类型(近距离测量、远距离测量)、应用(杂讯源识、洩漏侦测等)、终端使用者产业(汽车及出行等)和地区进行细分。市场预测以以金额为准。

区域分析

到2025年,欧洲将占据全球声学摄影机市场30.60%的份额,主要得益于严格的环境法规和先进的汽车供应链。德国汽车製造商正在实施全车NVH(噪音、振动与声振粗糙度)项目,将摄影机资料整合到数位双胞胎孪生模型中;法国各市政当局正在进行为期多年的城市噪音摄影机试点项目,目标是到2030年将交通噪音降低30%。欧盟「地平线」计画的资助正在加速产学研联盟改进3D波束形成软体。亚太地区预计将以14.08%的复合年增长率成长。中国已根据GB/T 37153-2018标准立法规定了声学车辆预警系统,并鼓励一级供应商使用成像工具检验扬声器特性。深圳和新加坡的智慧城市计画正在十字路口安装永久性声学测绘节点。以六标准差品质着称的日本电子工厂正在贴片线上安装摄像头,以检测真空洩漏引起的嘶嘶声,从而推动了该地区的稳定订单。印度不断扩大的地铁网路要求在压缩空气煞车系统中采用声学洩漏侦测装置。

随着航太主要製造商遵守美国联邦航空管理局 (FAA) 的噪音认证要求,以及美国职业安全与健康管理局 (OSHA) 扩大噪音暴露指南,北美地区继续发挥重要作用。工业终端用户正在将声学摄影机与振动、温度和电能品质感测器整合到一个统一的控制面板中。美国墨西哥湾沿岸的石油和天然气生产商正在将摄影机安装在履带上,用于储存槽检查,以降低密闭空间作业的风险。南美洲、中东和非洲是新兴但充满潜力的市场。智利矿业公司正在试用携带式成像器来识别排气扇共振,而沿岸地区的公用事业公司正在试用摄影机进行沙漠电力线路检查,因为在沙漠中,目视无人机难以应对眩光和灰尘。虽然预计这些地区的普及速度将比已开发地区慢两到三年,但它们将为全球整体普及做出贡献。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加强全球城市噪音管制

- 电动出行平台NVH的快速数位化

- 智慧工厂中从手持式声级计转向成像感测器

- 更严格的飞机客舱舒适度认证标准

- 边缘AI波束成形模组使声学摄影机的组件成本低于5000美元*

- 整合到自主机器人检测有效载荷中*

- 市场限制

- 3D MEMS阵列元件的初始资本投入较高

- 缺乏区域现场校准标准

- 与延迟和合成波束成形技术相关的专利拥堵

- 恶劣天气条件下公共产业的加固选择有限*

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按数组类型

- 二维数组

- 3D阵列

- 按测量类型

- 近距离

- 长途

- 透过使用

- 识别噪音源

- 洩漏检测

- 机械故障诊断

- 其他(生物声学、研究与发展)

- 按最终用户行业划分

- 汽车与出行

- 航太/国防

- 电子装置和半导体

- 能源与电力

- 其他行业

- 按地区

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Hottinger Brel and Kjr Sound and Vibration Measurement A/S

- gfai tech GmbH

- Teledyne FLIR LLC

- SM Instruments Inc.

- Fluke Corporation

- CAE Software and Systems GmbH

- Norsonic AS

- Microflown Technologies BV

- SINUS Messtechnik GmbH

- Sorama BV

- Polytec GmbH

- Visisonics Corporation

- Signal Interface Group LLC

- NL Acoustics Oy

- Ziegler-Instruments GmbH

- Siemens Digital Industries Software

第七章 市场机会与未来展望

The acoustic camera market is expected to grow from USD 160.41 billion in 2025 to USD 165.73 billion in 2026 and is forecast to reach USD 195.08 billion by 2031 at 3.32% CAGR over 2026-2031.

Cost reductions in MEMS microphone arrays and the arrival of compact edge-AI processors have lowered system bills-of-materials below USD 5,000, moving acoustic imaging from research laboratories into factory floors and city streets. Municipal authorities are deploying noise-enforcement cameras, automotive engineers are digitizing NVH testing for electric vehicles, and utilities are pairing beamforming modules with predictive-maintenance platforms. Edge analytics now runs on-device, trimming cloud bandwidth and latency while widening use cases in remote assets. Competitive activity centers on algorithm efficiency and software ecosystems rather than scale, allowing niche innovators to stand alongside diversified test-instrument majors.

Global Acoustic Camera Market Trends and Insights

Tightening Global Urban-Noise Regulations

Municipal agencies are moving from point sound-level meters to spatial imaging that links violations to individual vehicles. European and North American cities installed camera-based noise radars during 2024, and solutions such as SoundVue deliver Class 1 accuracy that satisfies legal-evidence requirements. The European Union targets a 30% cut in transport noise by 2030, spurring long-term procurement of rugged outdoor acoustic cameras. Preference is shifting toward permanent roadside units over mobile trailers, anchoring multi-year hardware demand and service contracts.

Rapid NVH Digitalization in E-Mobility Platforms

Electric powertrains silence combustion masking, unveiling tonal signatures from motors, inverters, and HVAC ducts. Automakers boosted acoustic test budgets during 2024; Hyundai adopted 3-D scanning rigs for full interior mapping. Real-time beamforming lets engineers visualize radiation patterns under actual driving, closing corrective loops before start-of-production. Growing fleets of commercial vans and city buses adopt the same methodologies to meet comfort and regional noise-homologation rules.

High Upfront Capex for 3-D MEMS-Array Rigs

Research-grade 3-D configurations can exceed USD 100,000 because hundreds of phase-matched microphones, precision housings, and high-bandwidth converters raise material and assembly costs. Optical MEMS microphones now deliver 80 dB SNR, yet process tooling and yield learning curves postpone sweeping price drops. Small enterprises lean on shared-service laboratories or rent 3-D systems until modular arrays below USD 50,000 proliferate.

Other drivers and restraints analyzed in the detailed report include:

- Shift from Handheld Sound-Level Meters to Imaging Sensors on Smart Factories

- Rising Aerospace Cabin-Comfort Certification Thresholds

- Scarcity of Field-Calibration Standards Across Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

2-D architectures retained 52.40% share of the acoustic camera market in 2025 owing to proven reliability and lower pricing. They dominate plant leak surveys and automotive component checks. Meanwhile, 3-D units are moving at a 16.03% CAGR as cabin noise mapping, urban-air-mobility trials, and complex machinery enclosures call for full-volume localization. The Octagon system with 192 microphones demonstrates resolution across 20 Hz to 10 kHz bands. As MEMS costs ease, the acoustic camera market size for 3-D platforms is expected to close the gap with mainstream options. Artificial-intelligence pattern recognition is improving hit rates, allowing smaller apertures to match legacy performance.System integrators embed real-time visualization within CAD dashboards, so engineers iterate acoustic treatments in minutes rather than days. This workflow compression justifies premiums in aerospace and luxury vehicle segments. Prototype 3-D arrays shipped in 2024 at under USD 60,000, signalling a trajectory toward broader adoption among mid-tier suppliers and university labs.

Near-field setups commanded 60.30% revenue in 2025 thanks to clear standards and controlled environments. Chamber testing, gearbox analysis, and benchtop RandD remain anchor use cases. Far-field demand is climbing at a 14.55% CAGR in step with wind turbine noise audits, smart city sound mapping, and aircraft pass-by trials. Minimum variance distortion less response algorithms now separate sources more than 50 m away despite heavy background traffic. As a result, the acoustic camera market size for long-range systems is projected to double through 2031. Infrastructure managers integrate data into geospatial dashboards that overlay acoustic metrics on facility blueprints for quick dispatch of repair crews.

Field operators value rugged enclosures rated IP65 or higher and low-power edge processors that relay alerts over 4G or LoRaWAN. Vendors emphasizing ease of installation and cloud APIs are winning bids in municipal tenders and renewable-energy farms.

The Acoustic Camera Market Segmented by Array Type (2-D Arrays, 3-D Arrays), Measurement Type (Near-Field, Far-Field), Application (Noise Source Identification, Leak Detection and More), End-User Industry (Automotive & Mobility and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe held 30.60% of the acoustic camera market in 2025, anchored by stringent environmental regulations and a sophisticated automotive supply chain. German OEMs run full-vehicle NVH programs that cascade camera data into digital twins, while French municipalities engage multi-year urban noise-camera pilots to secure 30% transport noise cuts by 2030. Funding instruments from Horizon Europe accelerate academic-industry consortia that refine 3-D beamforming software.APAC is set for a 14.08% CAGR. China legislated acoustic vehicle alerting systems under GB/T 37153-2018, pushing tier-one suppliers to validate loudspeaker signatures with imaging tools. Smart-city programs in Shenzhen and Singapore embed permanent acoustic mapping nodes at intersections. Japanese electronics plants, known for Six Sigma quality, fit cameras over pick-and-place lines to catch vacuum-leak hiss, driving consistent regional orders. India's expanding metro-rail footprint is specifying acoustic leak detection on compressed-air braking systems.

North America retains an influential role as aerospace primes comply with FAA noise certification and as OSHA broadens exposure guidelines. Industrial end users integrate acoustic cameras with vibration, thermal, and power-quality sensors in unified dashboards. Oil and gas producers in the Gulf Coast mount cameras on robotic crawlers for storage tank inspections, mitigating confined-space entry risks.South America and the Middle East and Africa form nascent but promising territories. Mining operators in Chile test portable imagers to pinpoint vent fan resonance, while Gulf utilities trial cameras for desert power-line inspections where visual drones struggle with glare and sand. Uptake here is expected to trail advanced regions by two to three years yet remains additive to global volumes.

- Hottinger Brel and Kjr Sound and Vibration Measurement A/S

- gfai tech GmbH

- Teledyne FLIR LLC

- SM Instruments Inc.

- Fluke Corporation

- CAE Software and Systems GmbH

- Norsonic AS

- Microflown Technologies BV

- SINUS Messtechnik GmbH

- Sorama BV

- Polytec GmbH

- Visisonics Corporation

- Signal Interface Group LLC

- NL Acoustics Oy

- Ziegler-Instruments GmbH

- Siemens Digital Industries Software

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening global urban-noise regulations

- 4.2.2 Rapid NVH digitalisation in e-mobility platforms

- 4.2.3 Shift from handheld sound-level meters to imaging sensors on smart factories

- 4.2.4 Rising aerospace cabin-comfort certification thresholds

- 4.2.5 Edge-AI beamforming modules enable sub-$5 k BOM acoustic cameras*

- 4.2.6 Integration into autonomous-robot inspection payloads*

- 4.3 Market Restraints

- 4.3.1 High upfront capex for 3D MEMS-array rigs

- 4.3.2 Scarcity of field-calibration standards across regions

- 4.3.3 Patent thickets around delay-and-sum beam-forming IP*

- 4.3.4 Limited ruggedised options for harsh-weather utilities*

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Array Type

- 5.1.1 2-D Arrays

- 5.1.2 3-D Arrays

- 5.2 By Measurement Type

- 5.2.1 Near-Field

- 5.2.2 Far-Field

- 5.3 By Application

- 5.3.1 Noise Source Identification

- 5.3.2 Leak Detection

- 5.3.3 Mechanical Fault Diagnostics

- 5.3.4 Others (Bio-acoustics, RandD)

- 5.4 By End-user Industry

- 5.4.1 Automotive and Mobility

- 5.4.2 Aerospace and Defense

- 5.4.3 Electronics and Semiconductor

- 5.4.4 Energy and Power

- 5.4.5 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 United Arab Emirates

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 South Africa

- 5.5.4.4 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Hottinger Brel and Kjr Sound and Vibration Measurement A/S

- 6.4.2 gfai tech GmbH

- 6.4.3 Teledyne FLIR LLC

- 6.4.4 SM Instruments Inc.

- 6.4.5 Fluke Corporation

- 6.4.6 CAE Software and Systems GmbH

- 6.4.7 Norsonic AS

- 6.4.8 Microflown Technologies BV

- 6.4.9 SINUS Messtechnik GmbH

- 6.4.10 Sorama BV

- 6.4.11 Polytec GmbH

- 6.4.12 Visisonics Corporation

- 6.4.13 Signal Interface Group LLC

- 6.4.14 NL Acoustics Oy

- 6.4.15 Ziegler-Instruments GmbH

- 6.4.16 Siemens Digital Industries Software

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment