|

市场调查报告书

商品编码

1940572

美国汽车售后市场零件:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)United States Aftermarket Automotive Parts And Components - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

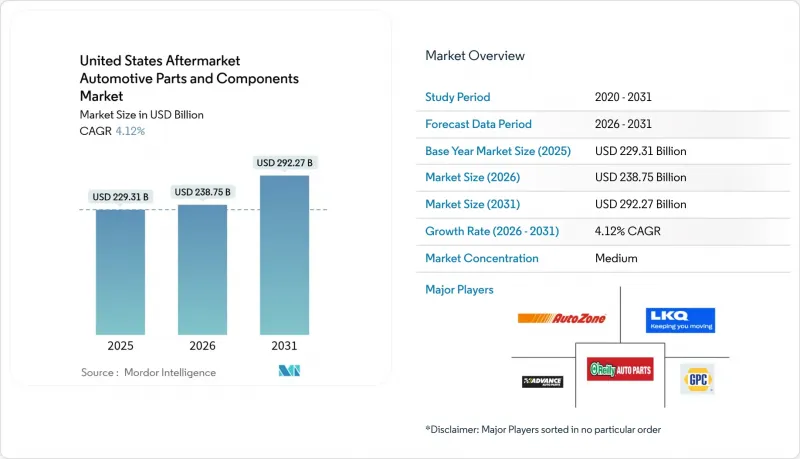

美国汽车售后零件市场预计将从 2025 年的 2,293.1 亿美元成长到 2026 年的 2,387.5 亿美元,到 2031 年达到 2,922.7 亿美元,2026 年至 2031 年的复合年增长率为 4.12%。

推动这一扩张的因素包括车辆平均车龄延长、轻型卡车销售强劲以及电子商务的快速发展。新车价格上涨、维修权法律的扩大以及疫情后驾驶量的復苏刺激了替换需求,而新兴的电动改装套件则开闢了一个高端专业细分市场。儘管不同零件类别的竞争情况各不相同,但那些将全通路分销与电子技术专长相结合的供应商正在为持续成长奠定基础。从美国环保署(EPA)的排放气体标准到各州的电动车强制令,管理方案既是推动因素也是推动因素,它们透过不断变化的合规要求重塑着汽车售后零件市场。

美国汽车售后市场零件及组件市场趋势与洞察

大型SUV和皮卡车的普及带动了易耗零件收入的成长。

轻型卡车在汽车市场占据主导地位,预计到2027年将占据新车销售的相当大份额。与传统乘用车相比,这些重型车辆的售后市场支出更高,这反映了它们独特的性能和需求。由于需要牵引和承载重物,构成这些卡车的部件——悬吊、煞车系统和传动系统部件——必须承受更大的负荷。

越野旅行、拖车和户外探险等生活方式趋势正在推动车辆性能升级的需求。爱好者们正在寻找升高套件、重型减震器和更大尺寸的轮胎,以改善驾驶体验并应对崎岖地形。皮卡车专用配件市场规模已高达每年160亿美元,製造商也为这些多功能车辆提供专门的产品线。

轻型卡车车主往往热衷于改装,升级改造的平均交易金额通常超过标准零件更换的费用。这种趋势不仅提升了卡车的美观性和功能性,也提高了汽车售后市场零件产业的利润率,展现出一个蓬勃发展、潜力无限的市场。

电子商务的渗透加速了长尾SKU的供应。

如今,绝大多数汽车售后市场交易都发生在充满活力的数位管道中,其速度远远超过美国整体零售电商的渗透率。这一显着转变使得网路商店商店能够展示专业化的SKU,而无需承担传统实体批发商的库存成本。因此,全国各地都能轻鬆找到老式车款的稀有零件,满足了爱好者和收藏家的需求。直接发货和即时库存数据缩短了DIY爱好者和小规模维修厂的前置作业时间,并将市场力量重新分配给了精通数位技术的供应商。然而,仿冒品仍然是一个严重的风险,联邦执法行动凸显了品牌保护计画的重要性。那些将强大的认证技术与用户友好介面相结合的公司正在不断扩大其在数位售后市场的份额。

ADAS降低了对碰撞部件的需求

自动紧急煞车和车道维持系统正在降低事故率,从而减少了对保险桿、挡泥板和车灯的需求。事故频率的下降在新型豪华车中最为显着,这些车辆的ADAS普及率最高,进一步压缩了对外部零件的需求。然而,由于需要进行感测器校准和更长的工时,配备ADAS的车辆维修费用更高,抵消了部分需求下降的影响。损坏的摄影机和雷达模组的更换推动了专用电子产品细分市场的成长。碰撞维修中心正在提升技能并投资先进的扫描工具,这使得提供原厂级感测器和校准夹具的零件供应商受益。

细分市场分析

截至2025年,乘用车将占美国汽车售后市场零件总收入的52.74%,这主要得益于其庞大的保有量。然而,商用轻型卡车预计将以7.05%的复合年增长率成长,随着小包裹递送和服务车队行驶里程的不断增加,其对汽车售后市场零件规模的贡献也将更大。严苛的使用週期以及对运转率的严格要求,导致煞车系统总成、传动系统接头和冷却零件的更换频率不断提高。车队营运商优先选择能够保证快速交付和高效保固流程的供应商,这迫使零件製造商转向仓库级库存和预测性供应系统。

中型和重型卡车由于销量低、零件成本高且运作损失巨大,因此创造了相对较大的经济价值。美国环保署 (EPA) 2027 年排放气体法规正在推动购车前的活动以及售后市场对选择性催化还原 (SCR) 和颗粒过滤器 (DPF) 的改装,从而暂时提振了对重型车辆的需求。预测中新分類的巴士和长途客车市场为大批量温度控管和悬吊产品的专业供应商提供了更多机会。虽然乘用车市场仍然很重要,但随着家庭在混合办公时代质疑是否需要多辆车,其销售成长已趋于平稳。同时,车队车辆的成长似乎与物流业的扩张密切相关。

到2025年,引擎零件将占美国汽车售后市场零件市场的31.45%,这反映出内燃机(ICE)的持续主导地位。同时,高级驾驶辅助系统(ADAS)感测器预计将以7.52%的复合年增长率成长,标誌着价值正从机械转向电子。相机模组、雷达单元和控制ECU经常在轻微碰撞中发生故障,或受到环境污染物的影响,从而形成利润丰厚的更换週期。大陆集团计划在2024年推出700个新的引擎管理SKU,这反映了该供应商在扩展其电子产品组合的同时,保护其机械基础的双管齐下的策略。

在悬吊、煞车和轮胎领域,大型SUV和皮卡的流行趋势持续推动需求成长。随着驾驶员对更高连接性和空中升级功能的需求不断增长,电气和资讯娱乐细分市场也在扩张,售后硬体和软体服务之间的界线也变得模糊。车身和外观零件的市场格局更为复杂:ADAS(高级驾驶辅助系统)降低了事故发生率,而个人化客製化文化和区域气候变迁造成的损害则支撑着潜在的需求。随着独立维修店越来越有能力维修复杂的软体驱动型车辆系统,工具、诊断设备和车间耗材的需求也不断增长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 现役老旧轻型车辆数量众多,推动了车辆更换需求。

- 大型SUV和皮卡车的普及推动了易损件收入的成长。

- 电子商务的普及加速了长尾SKU的上市。

- 电动改装套件开闢了高利润的专业领域。

- 《维修权法案》扩大了独立售后市场的进入范围

- 疫情里程恢復推动服务频率提升

- 市场限制

- 电动车的活动部件比一般汽车少30-40%。

- ADAS的引入降低了对碰撞部件的需求。

- OE服务即软体订阅模式将蚕食硬体销售。

- 跨境电商涌入的仿冒品侵蚀品牌份额

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按车辆类型

- 搭乘用车

- 轻型商用车(1-3 类)

- 中型和大型卡车(4-8级)

- 巴士和长途客车(新)

- 依组件类型

- 引擎零件(滤清器、垫片、活塞)

- 变速箱/传动系统

- 电气和电子设备(感测器、交流发电机、ADAS)

- 悬吊和煞车

- 车身及外观(保险桿、照明)

- 胎

- 室内用品和配件

- 润滑剂和润滑剂

- 其他(座椅、椅套等)

- 按销售管道

- 在线的

- 离线

- 依推进类型

- 内燃机车辆

- 混合动力电动车(HEV)

- 电池电动车(BEV)

- 插电式混合动力电动车(PHEV)

- 燃料电池电动车(FCEV)

- 透过服务管道

- DIY

- DIFM独立维修店

- 车队/商业服务供应商

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Magna International Inc.

- Continental AG

- ZF Friedrichshafen AG

- DENSO Corporation

- Robert Bosch GmbH

- Lear Corporation

- Flex-N-Gate Corporation

- Panasonic Automotive Systems Co. of America

- Aisin World Corp. of America

- American Axle & Manufacturing

- Yazaki North America

- Adient PLC

- Faurecia SE

- Aptiv PLC

- LKQ Corporation

- Advance Auto Parts Inc.

- O'Reilly Automotive Inc.

- AutoZone Inc.

- Genuine Parts Co.(NAPA)

- Tenneco Inc.

- Dana Incorporated

- BorgWarner Inc.

- Goodyear Tire & Rubber Co.

第七章 市场机会与未来展望

The United States aftermarket automotive parts and components market is expected to grow from USD 229.31 billion in 2025 to USD 238.75 billion in 2026 and is forecast to reach USD 292.27 billion by 2031 at 4.12% CAGR over 2026-2031.

A longer average vehicle age, strong light-truck sales, and rapid e-commerce uptake underpin this expansion. Elevated new-vehicle prices, wider right-to-repair statutes, and post-pandemic driving recovery stimulate replacement demand, while emerging electrified retrofit kits carve out premium specialty niches. Competitive intensity varies by component category, yet suppliers that pair omnichannel distribution with electronics expertise are positioning for durable growth. Regulatory initiatives, from EPA emissions rules to state EV mandates, act as simultaneous headwinds and tailwinds, reshaping the aftermarket automotive parts market through shifting compliance requirements.

United States Aftermarket Automotive Parts And Components Market Trends and Insights

Shift to Larger SUVs and Pickups Raises Wear-Part Revenues

Light trucks are poised to take the automotive market by storm, likely capturing a substantial share of new-vehicle sales by 2027. Each of these robust vehicles commands a higher aftermarket expenditure compared to traditional passenger cars, reflecting their unique demands and capabilities. The components that comprise these trucks, suspension, braking, and drivetrain parts, must endure considerably greater stress due to the hefty loads they tow and carry.

As lifestyle trends like overlanding, trailering, and outdoor adventures gain popularity, the appetite for performance-enhancing upgrades swells. Enthusiasts are seeking out lift kits, heavy-duty shocks, and oversized tires to elevate their driving experiences and tackle rugged terrains. The market for specialty equipment tailored to pickups has already surpassed an impressive USD 16 billion annually, prompting manufacturers to roll out dedicated product lines for these versatile vehicles.

Light-truck owners are often passionate about customization, leading to an average transaction value for upgrades that frequently eclipses that of standard replacements. This trend not only enhances the aesthetics and functionality of their trucks but also elevates profit margins across the aftermarket automotive parts sector, signaling a thriving market with boundless potential.

E-Commerce Penetration Accelerates Long-Tail SKU Availability

The vast majority of aftermarket transactions now traverse the dynamic landscape of digital channels, far surpassing the overall adoption of retail e-commerce across the United States. This remarkable shift allows online storefronts to showcase specialized SKUs without the burdensome costs of inventory that traditional brick-and-mortar wholesalers encounter. As a result, they can effortlessly provide nationwide access to hard-to-find parts for vintage models, catering to enthusiasts and collectors alike. Drop-shipment logistics and real-time inventory data reduce lead times for DIYers and small garages, redistributing market power toward digitally savvy suppliers. Yet counterfeit inflow remains an acute risk; federal enforcement actions underscore the importance of brand-protection programs . Firms that combine robust authentication technology with user-friendly interfaces are capturing a disproportionate share of the expanding digital aftermarket.

ADAS Lowers Collision-Part Volumes

Automatic emergency braking and lane-keeping systems are cutting crash rates, trimming demand for bumpers, fenders, and lamps. Collision frequency declines most among late-model premium vehicles, where ADAS penetration is highest, compressing volumes for cosmetic body parts. Offsetting this decline, repairs on ADAS-equipped vehicles command higher invoice values due to mandatory sensor calibration and longer labor hours. Replacement of damaged cameras or radar modules fosters growth in specialized electronics sub-segments. Collision-repair centers are upskilling and investing in advanced scan tools, benefiting parts suppliers that offer OE-grade sensors and calibration fixtures.

Other drivers and restraints analyzed in the detailed report include:

- Electrified Retrofit Kits Open High-Margin Specialty Niches

- Post-Pandemic Rebound in Vehicle Miles Traveled Lifts Service Frequency

- OEM "Service-as-Software" Subscriptions Cannibalize Hardware Sales

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars accounted for 52.74% of the United States Aftermarket Automotive Parts and Components Market overall revenue in 2025, anchored through an expansive installed base. Nevertheless, commercial light trucks are projected to post a 7.05% CAGR, elevating their contribution to the aftermarket automotive parts market size as parcel delivery and service fleets log higher daily mileage. Combining intensive duty cycles and stringent uptime requirements lifts replacement frequency for brake assemblies, driveline joints, and cooling components. Fleet operators' procurement practices favor suppliers that guarantee rapid availability and streamlined warranty processes, nudging parts makers toward depot-level inventory and predictive fulfillment systems.

Medium and heavy trucks yield outsized monetary value, while smaller in volume, because individual components carry higher price tags and downtime penalties. EPA 2027 emissions rules motivate prebuy activity and aftermarket retrofits of selective catalytic reduction and particulate filters, temporarily boosting heavy-duty demand. Buses and coaches, newly segmented in the forecast, open ancillary potential for specialist providers of high-capacity thermal-management and suspension products. Passenger-car segments remain relevant but confront a plateauing unit base as households question the need for multiple vehicles in the era of hybrid work, whereas fleet vehicles appear locked into growth trajectories tied to logistics expansion.

Engine components retained 31.45% of the United States Aftermarket Automotive Parts and Components Market in 2025, mirroring the still-dominant ICE parc. Yet ADAS sensors are forecast for a 7.52% CAGR, signaling the pivot from mechanical to electronic value. Camera modules, radar units, and control ECUs often fail in minor collisions or succumb to environmental contaminants, creating high-margin replacement cycles. Continental's 2024 launch of 700 new engine-management SKUs illustrates suppliers' dual strategy of defending mechanical strongholds while scaling electronics portfolios.

Suspension, brake, and tire categories see ongoing lift from the trend toward heavier SUVs and pickups. Electrical and infotainment sub-segments increase as drivers seek connectivity upgrades and over-the-air functionality, blurring the line between aftermarket hardware and software services. Body and exterior parts face mixed fortunes: ADAS reduces collision frequency, yet personalization culture and regional climate damage sustain baseline demand. Tools, diagnostics, and shop consumables are expanding as independent garages gear up to service complex, software-driven vehicle systems.

The United States Aftermarket Automotive Parts and Components Market is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component Type (Engine Components, Transmission and Driveline, and More), Sales Channel (Online and Offline), Propulsion Type (ICE Vehicles, and More), and by Service Channel (DIY, DIFM Independent Garages, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Magna International Inc.

- Continental AG

- ZF Friedrichshafen AG

- DENSO Corporation

- Robert Bosch GmbH

- Lear Corporation

- Flex-N-Gate Corporation

- Panasonic Automotive Systems Co. of America

- Aisin World Corp. of America

- American Axle & Manufacturing

- Yazaki North America

- Adient PLC

- Faurecia SE

- Aptiv PLC

- LKQ Corporation

- Advance Auto Parts Inc.

- O'Reilly Automotive Inc.

- AutoZone Inc.

- Genuine Parts Co. (NAPA)

- Tenneco Inc.

- Dana Incorporated

- BorgWarner Inc.

- Goodyear Tire & Rubber Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Light-Vehicle Parc Drives Replacement Demand.

- 4.2.2 Shift To Larger SUVs and Pickups Raises Wear-Part Revenues.

- 4.2.3 E-Commerce Penetration Accelerates Long-Tail SKU Availability.

- 4.2.4 Electrified Retrofit Kits Open High-Margin Specialty Niches.

- 4.2.5 Right-To-Repair Statutes Widen Independent Aftermarket Access.

- 4.2.6 Post-Pandemic Rebound In Vehicle-Miles-Traveled Lifts Service Frequency

- 4.3 Market Restraints

- 4.3.1 EVs Contain 30-40 % Fewer Moving Parts.

- 4.3.2 ADAS Lowers Collision-Part Volumes

- 4.3.3 OE Service-As-Software Subscriptions Cannibalize Hardware Sales.

- 4.3.4 Counterfeit Inflow Via Cross-Border E-Commerce Erodes Brand Share.

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles (Class 1-3)

- 5.1.3 Medium & Heavy Trucks (Class 4-8)

- 5.1.4 Buses & Coaches (NEW)

- 5.2 By Component Type

- 5.2.1 Engine Components (filters, gaskets, pistons)

- 5.2.2 Transmission & Driveline

- 5.2.3 Electrical & Electronics (sensors, alternators, ADAS)

- 5.2.4 Suspension & Brakes

- 5.2.5 Body & Exterior (bumpers, lighting)

- 5.2.6 Tires

- 5.2.7 Interior & Accessories

- 5.2.8 Fluids & Lubricants

- 5.2.9 Others (Seat and Covers, etc.)

- 5.3 By Sales Channel

- 5.3.1 Online

- 5.3.2 Offline

- 5.4 By Propulsion Type

- 5.4.1 Internal-Combustion Engine (ICE) Vehicles

- 5.4.2 Hybrid Electric Vehicles (HEV)

- 5.4.3 Battery Electric Vehicles (BEV)

- 5.4.4 Plug-in Hybrid Electric Vehicles (PHEV)

- 5.4.5 Fuel-Cell Electric Vehicles (FCEV)

- 5.5 By Service Channel

- 5.5.1 DIY (Do-It-Yourself)

- 5.5.2 DIFM Independent Garages

- 5.5.3 Fleet / Commercial Service Providers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Magna International Inc.

- 6.4.2 Continental AG

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 DENSO Corporation

- 6.4.5 Robert Bosch GmbH

- 6.4.6 Lear Corporation

- 6.4.7 Flex-N-Gate Corporation

- 6.4.8 Panasonic Automotive Systems Co. of America

- 6.4.9 Aisin World Corp. of America

- 6.4.10 American Axle & Manufacturing

- 6.4.11 Yazaki North America

- 6.4.12 Adient PLC

- 6.4.13 Faurecia SE

- 6.4.14 Aptiv PLC

- 6.4.15 LKQ Corporation

- 6.4.16 Advance Auto Parts Inc.

- 6.4.17 O'Reilly Automotive Inc.

- 6.4.18 AutoZone Inc.

- 6.4.19 Genuine Parts Co. (NAPA)

- 6.4.20 Tenneco Inc.

- 6.4.21 Dana Incorporated

- 6.4.22 BorgWarner Inc.

- 6.4.23 Goodyear Tire & Rubber Co.