|

市场调查报告书

商品编码

1940575

林业设备:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Forestry Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

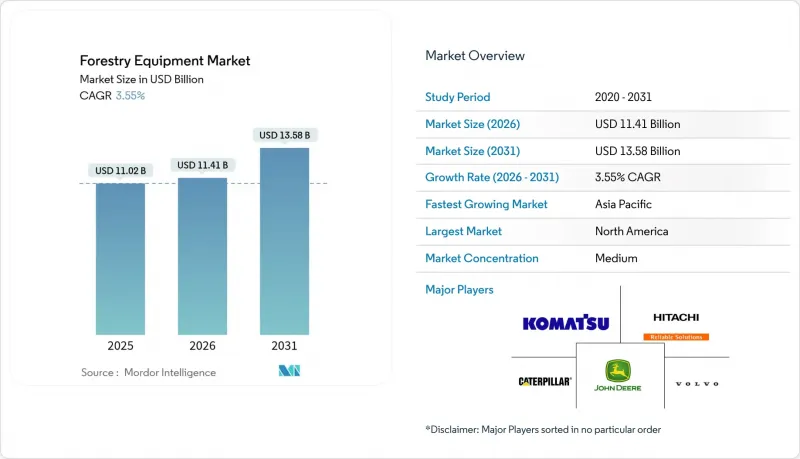

2025年林业设备市场价值为110.2亿美元,预计到2031年将达到135.8亿美元,高于2026年的114.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.55%。

市场需求集中在机械化选择性采伐机、精准林业平台和火灾后采伐系统,这些设备在提高生产效率的同时,也符合更严格的永续性要求。北美营运商正透过车队更新计画推动销售,而亚太地区的买家则优先考虑儘早实现机械化,并结合政府对永续林业的奖励。虽然随着电池在寒冷气候环境下的能量密度不断提高,电动和混合动力系统正从试点阶段过渡到早期商业部署,但柴油仍然是深山林业作业的必需品。熟练设备操作员的长期短缺、不断上涨的资金筹措成本以及木材价格的波动,都限制原本稳定的市场前景。

全球林业设备市场趋势与洞察

机械化导致选择性伐木需求增加

2024年美国国家森林管理指南中纳入的选择性采伐标准,目前已涵盖70%的联邦木材销售,这正推动采伐机机头和控制软体规格的快速升级。製造商正积极回应,推出可同时进行采伐和加工的双臂设计,确保承包商获得优质林木,从而实现每英亩收益提高25%至30%。类似的趋势也出现在欧洲,私人林地所有者正透过优质出口合同,从经认证的永续木材中获利。设备製造商支援的培训项目正在缩短学习曲线,并扩大目标承包商群体。区域伐木合作社正在汇集资金,购买先进的伐木集材机,在提高运转率的同时,也降低了资金筹措。

电动和混合动力林业设备的采用率不断提高

在不列颠哥伦比亚省,一辆柴油-电力混合动力林业卡车原型车在不影响有效负载容量的情况下,实现了40%的燃油消耗降低,电池电动平台已从示范阶段迈向2025年的早期商业化阶段。芬兰和瑞典的寒冷天气实地试验表明,锂离子电池系统能够承受低至-20°C的低温,从而消除了推广应用的一大障碍。在欧盟范围内,政府气候基金正在补贴零排放机械购置价格的30%,加速了集材机、收割机和充电拖车的订单。混合动力系统是一种切实可行的过渡方案,对于远离电网充电站的集材机运作,可节省15%至25%的燃油。路边基础设施是下一个瓶颈,这促使公私合营在木材分类厂安装快速充电桩。

先进机械设备初始投资高

现代收割机的零售价在80万至120万美元之间,是传统机器价格的三倍,但对于某些作业而言,它们确实能带来更高的生产效率。从2024年起,利率的上升加剧了资金筹措负担,迫使小型承包商推迟购买甚至退出市场。租赁车队正以灵活的计量型收费系统填补这一市场空白,根据多家原始设备製造商(OEM)财务部门的数据显示,其复合年增长率(CAGR)为4.27%。租赁公司将维护、远端资讯处理和操作员培训打包在一起,降低了总拥有成本,同时也挤压了经销商的利润空间。设备製造商正在推出简化的「经济型」产品线以促进销售,但这些型号也依赖规模经济才能保持竞争力。

细分市场分析

至2025年,伐木设备将占林业设备市场份额的36.12%,凸显其在减少人工链锯作业和降低安全风险方面发挥的核心作用。配备GPS和选择性伐木演算法的高产能伐木机能够以公分级的精度采集树干,从而提高林分品质和原木回收率。虽然链锯在特殊伐木作业和陡坡作业中仍然必不可少,但随着承包商在关键生产过程中转向机械化替代方案,链锯的使用量正在趋于平稳。

透过采用硬质合金锯片和预测性维护分析技术,伐木头的耐用性得到提升,零件寿命最多可延长 15%。前置整合设备套件将伐木和堆迭设备与车载去枝功能相结合,实现了单人操作工作流程,提高了每个班次的生产效率。原始设备製造商 (OEM) 正与软体公司合作,将数位林分地图迭加到驾驶员显示器上,帮助操作员确定哪些树木需要采伐,以确保最佳的剩余生长量。其他林业设备虽然收入基数较小,但预计到 2031 年将以 4.18% 的复合年增长率增长,因为承包商正将业务多元化经营到土地准备、生物质收割和野火预防等领域。配备可互换刀头的碎枝机可清除灌木丛,计划减少燃料消耗,而专用装载机则为高循环运作终端提供支援。模组化附件(例如快速连接树桩粉碎机)的创新正在扩展机器的多功能性并降低拥有成本,从而促进了即使在规模小规模的车队中也得到应用。整合在抓斗中的测量感测器可记录原木直径和含水量,并将数据直接发送到锯木厂的规划系统,以提高下游效率。

截至2025年,柴油动力平台将占据林业设备市场61.78%的份额,主要得益于完善的加油基础设施和在陡坡上卓越的牵引扭力。 Tier 4-F引擎的粒状物排放性能有所提升,但由于供应链以出口为导向,营运商仍需承担更严格的碳排放责任。燃油追踪远端资讯处理技术显示,经过驾驶行为训练后,燃油消耗可节省8-10%,因此无需更换传动系统设备即可有效降低不断上涨的柴油成本。

电动机械将成为成长最快的细分市场,到2031年将以4.32%的复合年增长率成长。电池化学技术的进步提高了能量密度,并降低了低温环境下的性能劣化。在收割季节部署配备太阳能-柴油混合发电机的快速充电拖车,可在计划维护期间进行部分充电,从而最大限度地减少运作。早期应用案例表明,在收集点有市电供应的情况下,营运成本降低了25%。混合动力机械透过在下坡行驶时回收再生能量并为辅助液压系统供电,继续弥补性能上的不足。汽油/柴油动力装置继续应用于手持式设备和偏远地区的防火隔离带作业,在这些作业中,必须尽可能降低机器的整体重量。

区域分析

北美地区预计占2025年总收入的38.40%,主要得益于其大片私有林地和成熟的机械化作业模式。美国营运商加快了车队现代化改造,以符合修订后的选择性伐木标准;而加拿大承包商则指定了低温作业包,以延长在冰点以下条件下的运作週期。生产力分析显示,实施人工智慧驱动的维护计画的车队,其运转率提高了10%至12%。

由于生质能的扩张抵消了锯木厂原木供应的停滞,欧洲需求保持稳定。斯堪地那维亚在主导,将林分级雷射雷达数据整合到机器控制系统中,以提高采伐率。中欧承包商正在投资适用于混合阔叶林的节能型混合动力集材机。欧盟分类体係等法规结构鼓励购买低排放设备,并为符合规定的买家提供资金筹措优惠。受中国永续林业计画和日本持续进行的地震灾后重建工作的推动,亚太地区预计到2031年将以4.07%的复合年增长率成长。中国省级补贴计画涵盖高达40%的配备人工智慧的采伐机,鼓励国内原始设备製造商与全球供应商在控制软体方面合作。澳洲加强了应对森林火灾的措施,推动了对灌木清除粉碎机和残茬回收采伐机的需求。南美洲人工林业的成长推动了高容量伐木集材机的销售,而中东和非洲的重新造林工作也开始从政策阶段过渡到采购阶段,为多用途机械开闢了新的前沿市场。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 机械化导致选择性伐木需求增加

- 扩大电动和混合动力林业设备的使用

- 全球生质能和生质能源计划扩张

- 政府鼓励精准和永续林业发展

- 整合远端资讯处理和人工智慧驱动的车队优化

- 野火过后,对伐木残余物的需求增加

- 市场限制

- 购置精密机械设备需要较高的初始资本支出。

- 农村地区熟练重型设备操作人员短缺

- 偏远林区缺乏充电基础设施

- 全球木材价格波动对资本投资週期的影响

- 产业价值链分析

- 宏观经济因素的影响

- 技术展望

- 监管环境

- 波特五力分析

- 新进入者的威胁

- 买方和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素的影响

- 新冠疫情对林业设备产业的影响

第五章 市场规模与成长预测

- 依产品类型

- 伐木设备

- 电锯

- 收割机

- 费勒‧邦彻

- 卸货设备

- 货运代理

- 集材机

- 其他卸货设备

- 现场加工设备

- 刀锯和研磨机

- 去枝机和修枝机

- 其他现场加工设备

- 选购部件和附件

- 锯、导板、锯片和锯齿

- 收割机和其他切割头

- 其他零件和配件需另行购买。

- 其他林业设备

- 装载机

- 碎枝机

- 其他林业设备

- 伐木设备

- 透过电源

- 柴油动力设备

- 汽油/柴油动力设备

- 电器

- 油电混合装置

- 其他电源

- 透过使用

- 日誌记录

- 土地开垦

- 森林火灾管理

- 森林道路建设

- 生物质收穫

- 其他用途

- 最终用户

- 商业伐木公司

- Timberland投资管理公司

- 政府林业机构

- 独立承包商和小规模企业

- 租赁服务供应商

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Deere & Company

- Caterpillar Inc.

- Komatsu Ltd.

- Volvo Construction Equipment AB

- Hitachi Construction Machinery Co. Ltd.

- Barko Hydraulics LLC

- HD Hyundai Infracore Co. Ltd.

- Kesla Oyj

- Ponsse Oyj

- Rottne Industri AB

- Eco Log Sweden AB

- AGCO Corporation

- Kubota Corporation

- Bell Equipment Limited

- Tigercat Industries Inc.

- CNH Industrial NV

- Husqvarna AB

- Doosan Bobcat Inc.

- SENNEBOGEN Maschinenfabrik GmbH

- Logset Oy

第七章 市场机会与未来展望

The forestry equipment market was valued at USD 11.02 billion in 2025 and estimated to grow from USD 11.41 billion in 2026 to reach USD 13.58 billion by 2031, at a CAGR of 3.55% during the forecast period (2026-2031).

Demand centers on mechanized selective-logging machinery, precision forestry platforms, and post-wildfire salvage systems that raise productivity while adhering to stricter sustainability mandates. North American operators drive unit sales through fleet renewal programs, whereas Asia-Pacific buyers prioritize first-time mechanization coupled with government incentives for sustainable forestry. Electric and hybrid powertrains are moving from pilot tests to early commercial deployment as battery density improves in cold-weather conditions, though diesel remains indispensable for deep-forest tasks. Persistent shortages of skilled equipment operators, elevated financing costs, and timber-price volatility temper an otherwise steady outlook.

Global Forestry Equipment Market Trends and Insights

Rising Demand for Mechanised Selective Logging

Selective harvesting standards embedded in the 2024 U.S. National Forest Management Guidelines now cover 70% of federal timber sales, prompting rapid specification upgrades for harvester heads and control software. Manufacturers have responded with dual-boom designs that enable simultaneous felling and processing, allowing contractors to capture premium-grade stems with 25-30% higher per-acre revenues. Europe mirrors this pattern as private landowners monetize certified sustainable timber for premium export contracts. Training programs sponsored by equipment OEMs shorten learning curves, broadening the addressable contractor base. Regional logging cooperatives pool capital to acquire advanced feller-bunchers, enhancing utilization while easing financing hurdles.

Increasing Adoption of Electric and Hybrid Forestry Machinery

Battery-electric platforms transitioned from demonstration to early commercialization in 2025 after British Columbia's diesel-electric logging truck prototype cut fuel use by 40% without payload penalties. Cold-climate field trials in Finland and Sweden validated lithium-ion systems down to -20 °C, alleviating one of the biggest adoption barriers. Government climate funds offset up to 30% of purchase prices for zero-emission machines across the European Union, accelerating order books for forwarders, harvesters, and charging trailers. Hybrid drivetrains offer a practical bridge solution, delivering 15-25% fuel savings on skidders that work far from grid-tied chargers. Infrastructure build-outs along forest service roads remain the next bottleneck, spurring public-private partnerships to install fast chargers at log-sorting yards.

High Upfront Capital Expenditure for Advanced Machines

Modern harvesters retail between USD 800,000 and USD 1.2 million, triple the cost of conventional machines while offering incremental productivity gains in some operations. Elevated interest rates since 2024 magnify financing burdens, prompting smaller contractors to delay purchases or exit the business. Rental fleets bridge the gap with flexible pay-per-use terms, expanding at 4.27% CAGR as reported by multiple OEM finance arms. Leasing firms bundle maintenance, telematics, and operator training, lowering total cost of ownership but compressing dealer margins. Equipment makers introduce stripped-down "value" lines to broaden the sales funnel, though these models still depend on scale economies to remain competitive.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Global Biomass and Bioenergy Projects

- Government Incentives for Precision and Sustainable Forestry

- Shortage of Skilled Heavy-Equipment Operators in Rural Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Felling equipment generated 36.12% of the forestry equipment market share in 2025, underscoring its central role in reducing manual chain-saw labor and mitigating safety risks. High-capacity harvesters equipped with GPS and selective-cutting algorithms now capture stems with centimeter-level precision, improving stand quality and log recovery rates. Chainsaws remain indispensable for specialty cuts and steep-slope terrain, but their volumes plateau as contractors switch to mechanized alternatives for core production.

Longevity gains in harvester heads, achieved through carbide-tipped saw bars and predictive maintenance analytics, extend component life cycles by up to 15%. Forward-integrated equipment suites combine feller-bunchers with on-board de-limbing, enabling single-operator workflows that increase productivity per shift. OEMs collaborate with software firms to overlay digital stand maps onto cab displays, guiding operators on which trees to remove for optimal residual growth. Other forestry equipment, while commanding a smaller revenue base, is forecast to grow at 4.18% CAGR through 2031 as contractors diversify into land clearing, biomass harvesting, and wildfire mitigation. Mulchers with interchangeable heads process underbrush for fuel-reduction projects, while purpose-built loaders serve biomass terminals that demand high cycle counts. Innovation in modular attachments-such as quick-coupler stump grinders-broadens machine versatility, lowering ownership costs and encouraging adoption even among smaller fleets. Integrated measurement sensors embedded in grapples record log diameter and moisture, feeding data directly into mill planning systems and raising downstream efficiency.

Diesel-powered platforms retained 61.78% of the forestry equipment market size in 2025 due to ubiquitous refueling infrastructure and unmatched torque for steep terrain hauling. Tier-4-F engines improved particulate performance, but operators still face stricter carbon accountability in export-oriented supply chains. Fuel-tracking telematics reveal 8-10% savings after driver-behavior coaching, allowing fleets to temper rising diesel expenses without swapping powertrains.

Electric-powered machinery marks the fastest-growing line at 4.32% CAGR through 2031 as battery chemistries deliver higher energy density with reduced cold-weather degradation. Mid-harvest fast-charging trailers fitted with solar-plus-diesel hybrid gensets enable partial recharging during scheduled maintenance windows, minimizing downtime. Early adopters report 25% lower operating costs where grid power is available at staging yards. Hybrid machines continue to bridge the gap, capturing regenerative energy on downhill skids and powering auxiliary hydraulics electrically. Petrol/oil units persist in handheld categories and remote fire-break operations where overall machine weights must remain minimal.

The Forestry Equipment Market Report is Segmented by Product Type (Felling Equipment, Extracting Equipment, and More), Power Source (Diesel-Powered, Petrol/Oil-Powered, and More), Application (Logging, Land Clearing, Forest Fire Management, and More), End-User (Commercial Logging Companies, Government Forestry Agencies, Rental Service Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.40% of 2025 revenue, anchored by extensive private timber holdings and mature mechanization practices. U.S. operators accelerated fleet modernization to comply with revised Selective Logging Standards, while Canadian contractors specified cold-weather packages that extend duty cycles in sub-zero regimes. Productivity analytics show utilization improvements of 10-12% across fleets that adopted AI-driven maintenance scheduling.

European demand remains steady as biomass expansion offsets plateauing sawlog volumes. Scandinavia leads precision-forestry adoption, integrating stand-level LiDAR data into machine control systems that raise recovery rates. Central European contractors invest in fuel-efficient hybrid skidders suited to mixed hardwood stands. Regulatory frameworks such as EU taxonomy classifications reinforce purchases of low-emission equipment, providing financing advantages to compliant buyers. Asia-Pacific is projected to log a 4.07% CAGR through 2031, driven by China's sustainable forestry program and Japan's ongoing post-disaster reconstruction commitments. Chinese provincial grants cover up to 40% of AI-enabled harvesters, spurring domestic OEMs to partner with global suppliers on control software. Australia's wildfire mitigation measures expand demand for brush-clearing mulchers and salvage harvesters. South America's plantation forestry growth boosts sales of high-throughput feller-bunchers, while reforestation commitments in Middle East and Africa begin moving from policy to procurement, opening new frontier markets for versatile multi-purpose machines.

- Deere & Company

- Caterpillar Inc.

- Komatsu Ltd.

- Volvo Construction Equipment AB

- Hitachi Construction Machinery Co. Ltd.

- Barko Hydraulics LLC

- HD Hyundai Infracore Co. Ltd.

- Kesla Oyj

- Ponsse Oyj

- Rottne Industri AB

- Eco Log Sweden AB

- AGCO Corporation

- Kubota Corporation

- Bell Equipment Limited

- Tigercat Industries Inc.

- CNH Industrial N.V.

- Husqvarna AB

- Doosan Bobcat Inc.

- SENNEBOGEN Maschinenfabrik GmbH

- Logset Oy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Mechanised Selective Logging

- 4.2.2 Increasing Adoption of Electric and Hybrid Forestry Machinery

- 4.2.3 Expansion of global Biomass and Bioenergy Projects

- 4.2.4 Government Incentives for Precision and Sustainable Forestry

- 4.2.5 Integration of Telematics and AI-Enabled Fleet Optimisation

- 4.2.6 Increased Post-Wildfire Salvage Harvesting Needs

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure for Advanced Machines

- 4.3.2 Shortage of Skilled Heavy-Equipment Operators in Rural Areas

- 4.3.3 Limited Charging Infrastructure in Remote Forest Regions

- 4.3.4 Volatility of Global Timber Prices Impacting CAPEX Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Technological Outlook

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers/Consumers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macroeconomic Factors

- 4.10 Impact of COVID-19 on the Forestry Equipment Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Felling Equipment

- 5.1.1.1 Chainsaws

- 5.1.1.2 Harvesters

- 5.1.1.3 Feller Bunchers

- 5.1.2 Extracting Equipment

- 5.1.2.1 Forwarders

- 5.1.2.2 Skidders

- 5.1.2.3 Other Extracting Equipment

- 5.1.3 On-Site Processing Equipment

- 5.1.3.1 Chippers and Grinders

- 5.1.3.2 Delimbers and Slashers

- 5.1.3.3 Other On-Site Processing Equipment

- 5.1.4 Separately Sold Parts and Attachments

- 5.1.4.1 Saw Chain, Guide Bars, Discs, and Teeth

- 5.1.4.2 Harvesting and Other Cutting Heads

- 5.1.4.3 Other Separately Sold Parts and Attachments

- 5.1.5 Other Forestry Equipment

- 5.1.5.1 Loaders

- 5.1.5.2 Mulchers

- 5.1.5.3 Other Forestry Equipment

- 5.1.1 Felling Equipment

- 5.2 By Power Source

- 5.2.1 Diesel-Powered Equipment

- 5.2.2 Petrol / Oil-Powered Equipment

- 5.2.3 Electric-Powered Equipment

- 5.2.4 Hybrid-Powered Equipment

- 5.2.5 Other Power Source

- 5.3 By Application

- 5.3.1 Logging

- 5.3.2 Land Clearing

- 5.3.3 Forest Fire Management

- 5.3.4 Forest Road Construction

- 5.3.5 Biomass Harvesting

- 5.3.6 Other Application

- 5.4 By End-User

- 5.4.1 Commercial Logging Companies

- 5.4.2 Timberland Investment Managers

- 5.4.3 Government Forestry Agencies

- 5.4.4 Individual Contractors and Small Operators

- 5.4.5 Rental Service Providers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 Caterpillar Inc.

- 6.4.3 Komatsu Ltd.

- 6.4.4 Volvo Construction Equipment AB

- 6.4.5 Hitachi Construction Machinery Co. Ltd.

- 6.4.6 Barko Hydraulics LLC

- 6.4.7 HD Hyundai Infracore Co. Ltd.

- 6.4.8 Kesla Oyj

- 6.4.9 Ponsse Oyj

- 6.4.10 Rottne Industri AB

- 6.4.11 Eco Log Sweden AB

- 6.4.12 AGCO Corporation

- 6.4.13 Kubota Corporation

- 6.4.14 Bell Equipment Limited

- 6.4.15 Tigercat Industries Inc.

- 6.4.16 CNH Industrial N.V.

- 6.4.17 Husqvarna AB

- 6.4.18 Doosan Bobcat Inc.

- 6.4.19 SENNEBOGEN Maschinenfabrik GmbH

- 6.4.20 Logset Oy

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

林业机械市场:2026年至2032年全球预测(依设备类型、推进方式、功率输出、应用通路通路划分)

林业机械市场:2026年至2032年全球预测(依设备类型、推进方式、功率输出、应用通路通路划分) 全球林业机械市场规模、份额、趋势和成长分析报告(2026-2034年)

全球林业机械市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球林业机械市场报告

2026年全球林业机械市场报告 伐木机市场 - 全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年

伐木机市场 - 全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年 2026-2030年全球木片製造机市场全球林业机械市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

2026-2030年全球木片製造机市场全球林业机械市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 林业机械市场规模、份额及成长分析(依设备类型、驱动方式、操作模式、最终用户及地区划分)-2026-2033年产业预测

林业机械市场规模、份额及成长分析(依设备类型、驱动方式、操作模式、最终用户及地区划分)-2026-2033年产业预测 林业机械市场依产品类型、动力来源、材料及地区划分

林业机械市场依产品类型、动力来源、材料及地区划分 木材削片机 - 全球市场份额和排名、总销售量和需求预测(2025-2031 年)

木材削片机 - 全球市场份额和排名、总销售量和需求预测(2025-2031 年) 全球林业机械市场

全球林业机械市场