|

市场调查报告书

商品编码

1940587

汽车温度控管:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Thermal Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

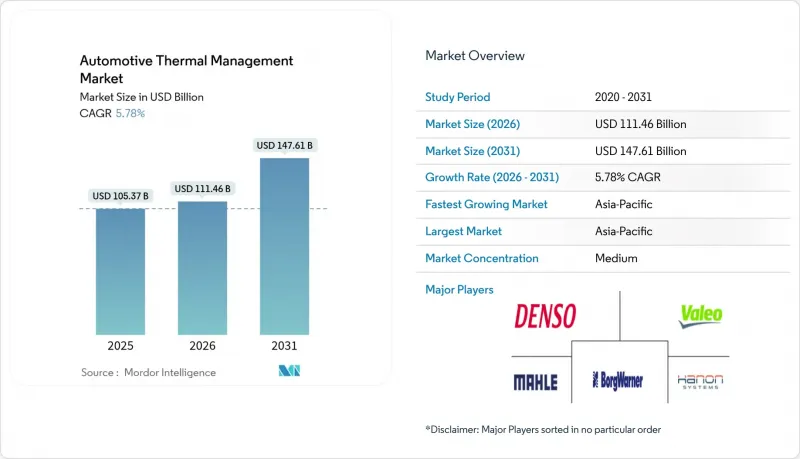

预计到 2026 年,汽车温度控管市场规模将达到 1,114.6 亿美元。

预计该产业规模将从 2025 年的 1,053.7 亿美元成长到 2031 年的 1,476.1 亿美元,2026 年至 2031 年的年复合成长率(CAGR)为 5.78%。

这项成长主要受以下因素驱动:快速的电气化进程、日益严格的全球二氧化碳排放和燃油经济性法规(CAFE),以及对整合式电池冷却系统、暖通空调系统和电力电子设备热迴路日益增长的需求。电池式电动车(BEV)的单位散热能力比内燃机汽车高出五分之二,这迫使供应商重新设计架构,以将电池温度维持在最佳的15-35°C范围内,延长电池组寿命,并支援800V快速充电硬体。竞争压力,尤其是在亚太地区,正在加速浸没式冷却、多迴路模组和不含PFAS的冷媒热泵等技术创新,从而有助于提高车辆的续航里程、舒适性和合规性。

全球汽车温度控管市场趋势与洞察

随着电动车逐渐成为主流,电池温度控管变得越来越重要。

电池组如今占总温度控管预算的五分之一,而传统汽车中这一比例微乎其微。现代摩比斯近期推出了脉衝式热管,其传热效率是标准热板的十倍,厚度仅为0.8毫米,温度均匀性提升20摄氏度,显着降低了失控风险。整合式热泵空调系统可回收废热,略微延长纯电动车的冬季续航里程。将电池、座舱和逆变器冷却功能整合到模组中的供应商也在多个平台上赢得了订单。

内部采用的 800V 架构加速了 SiC 逆变器的冷却。

如今,高阶电动车采用800V碳化硅逆变器,能够承受高达175°C的结温。液冷技术可将热阻降低至0.1°C/W以下,从而实现超过350kW的充电功率和超过15万次的循环可靠性。 NXP和Wolfspeed的最新参考设计都采用了这种液冷迴路,凸显了高功率应用中从风冷到直接液冷的转变。

整合热模组的物料清单成本高

整合模组虽然将多个组件整合到单一机壳中,但与使用分立组件相比,这种方法会显着增加成本。这给散热预算有限的车辆带来了挑战。为了应对这项挑战,供应商正致力于平台标准化、垂直整合和自动化组装流程等策略,以提高成本效益并实现大规模生产的损益平衡点。

细分市场分析

引擎冷却是内燃机汽车的基础,到 2025 年将占汽车温度控管市场的 35.01%。同时,电池系统预计将以 5.83% 的复合年增长率成长最快,这反映出原始设备製造商 (OEM) 将资源重新分配到电池组、模组和电芯级冷却迴路,这些迴路现在几乎占纯电动车 (BEV)温度控管预算的一半。

Stellantis的智慧电池整合系统将冷却板、逆变器和充电器整合在一起,能源效率至少提升10%,功率密度至少提升10%。双源热泵的广泛应用确保了车厢空调的稳定运行,而废热回收和废气再循环(EGR)模组在商业市场中也日益普及。随着800V动力系统的普及,马达和逆变器的冷却技术也正在快速发展,每个零件都需要高达200W/cm²的散热能力。

截至2025年,间接液冷迴路将占据汽车温度控管市场42.77%的份额,这得益于成熟的散热器、储液罐和泵浦技术。浸没式冷却的汽车温度控管市场规模将以5.82%的复合年增长率成长,这反映了其物理优势,使其允许的功率密度提高了10倍。

现代汽车的奈米薄膜空气冷却技术可将车内温度降低12.5°C,显着节省能源,并证明了空气冷却技术在轻量化系统中的独特优势。相变材料可在尖峰负载期间保护电池,混合迴路可将多种介质互连,并透过人工智慧监控实现最佳路径规划。

区域分析

亚太地区预计2025年将占据汽车温度控管市场39.17%的份额,年复合成长率达5.86%,主要成长动力来自比亚迪等中国企业在2024年推出的电动车以及2025年雄心勃勃的目标。韩昂系统公司(Hanon Systems)的大规模压缩机扩建计画将支援北美组装,同时利用亚洲低成本的供应链。日本和韩国的一级供应商正在推动脉衝热管等技术创新,以保持该地区的技术竞争力。

由于严格的燃油经济性标准以及福特、通用和特斯拉等主要汽车製造商对电动车的大规模投资,北美巩固了第二大市场地位。先进平台的快速普及推动了对碳化硅逆变器冷却和预测性热控制技术的需求成长。墨西哥具有成本效益的製造地持续吸引对泵浦、阀门和热交换器的投资,但熟练技术人员的短缺给复杂的电动车服务运作带来了挑战。

欧洲兼具严格的法规结构和雄厚的工程技术传统。排放的减排目标和某些化学品的逐步淘汰正在加速向更环保的冷媒转型。福特近期推出了一个以丙烷为基础的系统,展现了在温度控管的创新能力。德国製造商正优先开发整合模组和废气再循环热回收系统,而法国大力推动电池式电动车的发展也显着提升了对电池冷却解决方案的需求。这种高端市场定位促使每辆车的温度控管投入不断增加,从而确保供应商的可持续盈利。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电动车的普及将推动对电池温度控管的需求。

- 透过扩展豪华和舒适功能,提高每辆车的空调系统价值

- 800V 内部架构加速了 SIC 逆变器的冷却

- 由于内燃机涡轮增压小型化,对引擎和油冷却器的需求增加。

- 日益严格的二氧化碳排放和燃油经济性标准推动了多迴路冷却系统的发展

- PFAS逐步淘汰加速了向天然冷媒热泵的转型

- 市场限制

- 整合热模组的物料清单成本高

- 液体/浸没式系统的可靠性和洩漏路径风险

- 低全球暖化潜势冷媒供应网络短缺

- 维修技师缺乏处理复杂电动车冷却迴路的技能。

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 透过使用

- 引擎冷却

- 客舱/空调温度控管

- 传输温度控管

- 废热回收/废气再循环(EGR)

- 电池温度控管

- 马达和电力电子设备冷却

- 依技术类型

- 空调和暖气

- 液体间接冷却

- 直接冷却/浸没式冷却

- 相变/PCM系统

- 混合与整合迴路

- 按组件

- 热交换器(散热器、中央空调、油冷却器)

- 压缩机和泵浦

- 热感控阀和歧管

- 高压冷却液加热器

- 感测器和控制器

- 依推进类型

- 内燃机车辆

- 油电混合车

- 插电式混合动力汽车

- 电池式电动车

- 燃料电池电动车

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 大型卡车和巴士

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 南非

- 埃及

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Denso Corporation

- Hanon Systems

- Valeo SE

- MAHLE GmbH

- Gentherm Inc.

- Robert Bosch GmbH

- Dana Inc.

- BorgWarner Inc.

- Modine Mfg. Co.

- Schaeffler AG

- ZF Friedrichshafen AG

- Kendrion NV

- Continental AG

- TI Fluid Systems

- Sanden Holdings

- Boyd Corporation

- VOSS Automotive

- Grayson Thermal Systems

第七章 市场机会与未来展望

Automotive Thermal Management Market size in 2026 is estimated at USD 111.46 billion, growing from 2025 value of USD 105.37 billion with 2031 projections showing USD 147.61 billion, growing at 5.78% CAGR over 2026-2031.

Growth stems from rapid electrification, stricter global CO2 and CAFE rules, and rising demand for integrated battery-cooling, cabin HVAC, and power electronics thermal loops. Battery electric vehicles (BEVs) require two-fifths more thermal content per unit than internal-combustion cars, forcing suppliers to redesign architectures that hold battery temperatures in the optimal 15-35 °C band, extend pack life, and support 800 V fast-charge hardware. Competitive pressures, particularly in Asia-Pacific, accelerate innovation in immersion cooling, multi-circuit modules, and PFAS-free refrigerant heat-pumps that improve vehicle range, comfort, and regulatory compliance.

Global Automotive Thermal Management Market Trends and Insights

Mainstream EV Adoption Boosting Battery-Thermal Content

Battery packs now consume one-fifth of total thermal budgets, up from minimal in conventional cars. Hyundai Mobis introduced pulsating heat pipes in recent times that deliver ten-fold higher heat transfer than standard plates, trim thickness to 0.8 mm, and improve temperature uniformity by 20 °C, sharply lowering runaway risk. Integrated heat-pump HVAC recovers waste heat, adding minimal winter range to BEVs, and suppliers bundling battery, cabin, and inverter cooling in unified modules are booking multi-platform awards.

Under-Hood 800 V Architectures Accelerating SiC Inverter Cooling

Premium EVs now rely on 800 V silicon-carbide inverters capable of 175 °C junction temperatures. Immersion dielectric cooling keeps thermal resistance under 0.1 °C/W, enabling charge rates above 350 kW and safeguarding reliability over 150,000 cycles. Reference designs recently released by NXP and Wolfspeed embed these liquid loops, underlining the shift from air to direct liquid cooling in high-power applications.

High BOM Cost of Integrated Thermal Modules

Unified modules integrate multiple components into a single housing, but this approach significantly increases costs compared to using separate pieces. This creates challenges for vehicles operating within a limited thermal content budget. To address this, suppliers are focusing on strategies such as platform-standardization, vertical integration, and automated assembly processes to achieve cost efficiency and reach volume breakeven.

Other drivers and restraints analyzed in the detailed report include:

- Stricter CO2 / CAFE Norms Driving Multi-Circuit Cooling

- PFAS Phase-Out Forcing Switch to Natural-Refrigerant Heat-Pumps

- Reliability & Leak-Path Risks in Liquid/Immersion Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Engine cooling held a 35.01% of the automotive thermal management market share in 2025 as the backbone for ICE fleets. Battery systems, however, are scaling fastest at a 5.83% CAGR, reflecting OEM reallocations toward pack, module, and cell-level loops that now command almost half of BEV thermal budgets.

Stellantis' Intelligent Battery Integrated System bundles cooling plates, inverters, and chargers, boosting energy efficiency by 10% and power density by minimal. Cabin HVAC remains steady, aided by dual-source heat pumps, while waste-heat recovery and EGR modules grow in commercial sectors. Motor and inverter cooling races ahead as 800 V drivetrains proliferate, each demanding up to 200 W/cm2 heat removal.

Liquid indirect loops commanded 42.77% of the automotive thermal management market share in 2025, bolstered by mature radiators, reservoirs, and pumps. The automotive thermal management market size tied to immersion cooling is increasing at a 5.82% CAGR, reflecting physics advantages that elevate allowable power density tenfold.

Hyundai's nano-film air technology cut cabin temperatures by 12.5 °C and saved significant energy, proving air cooling's niche in lightweight systems. Phase-change materials buffer cells during peak load, and hybrid loops interlink multiple media, selecting optimal paths through AI supervision.

The Automotive Thermal Management Market Report is Segmented by Application (Engine Cooling, Cabin/HVAC, and More), Technology (Air, Liquid Indirect, and More), Component (Heat Exchangers, Compressors & Pumps, and More), Propulsion (ICE, HEV, and More), Vehicle Type (Passenger Cars, LCV, and Heavy Trucks & Buses), and Geography (North America, South America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 39.17% of the automotive thermal management market share in 2025 and led growth at a 5.86% CAGR, powered by China's EVs built by BYD in 2024 and a considerable target for 2025 . Hanon Systems' massive compressor expansion supports North American assembly while leveraging low-cost Asian supply lines. Japanese and Korean Tier 1s push breakthroughs such as pulsating heat pipes, keeping the region technologically competitive.

North America secures the second spot, bolstered by stringent fuel efficiency standards and significant EV capital commitments from major automakers such as Ford, GM, and Tesla. The rapid adoption of advanced platforms drives increased demand for silicon carbide inverter cooling and predictive thermal control technologies. While Mexico's cost-effective manufacturing base continues to attract investments in pumps, valves, and exchangers, a shortage of skilled technicians creates challenges for managing complex EV service operations.

Europe combines strict regulatory frameworks with a strong engineering tradition. Ambitious emissions reduction targets and the phase-out of certain chemicals are accelerating the transition to environmentally friendly refrigerants. Ford recently introduced its propane-based system, showcasing innovation in thermal management. German manufacturers are prioritizing integrated modules and exhaust gas recirculation heat recovery systems, while France's aggressive push for battery electric vehicles is significantly increasing the demand for battery cooling solutions. This premium market positioning supports higher thermal management spending per vehicle, ensuring sustained profitability for suppliers.

- Denso Corporation

- Hanon Systems

- Valeo SE

- MAHLE GmbH

- Gentherm Inc.

- Robert Bosch GmbH

- Dana Inc.

- BorgWarner Inc.

- Modine Mfg. Co.

- Schaeffler AG

- ZF Friedrichshafen AG

- Kendrion N.V.

- Continental AG

- TI Fluid Systems

- Sanden Holdings

- Boyd Corporation

- VOSS Automotive

- Grayson Thermal Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream EV Adoption Boosting Battery-Thermal Content

- 4.2.2 Luxury & Comfort Features Expanding HVAC Value Per Car

- 4.2.3 Under-Hood 800 V Architectures Accelerating SIC Inverter Cooling

- 4.2.4 ICE Turbo-Downsizing Raising Engine & Oil-Cooler Demand

- 4.2.5 Stricter Co2 / Cafe Norms Driving Multi-Circuit Cooling

- 4.2.6 PFAS-Phase-Out Forcing Switch To Natural-Refrigerant Heat-Pumps

- 4.3 Market Restraints

- 4.3.1 High BOM Cost Of Integrated Thermal Modules

- 4.3.2 Reliability & Leak-Path Risks In Liquid/Immersion Systems

- 4.3.3 Scarcity Of Low-GWP Refrigerant Supply Chains

- 4.3.4 Limited Service-Technician Capabilities For Complex EV Cooling Loops

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 Engine Cooling

- 5.1.2 Cabin / HVAC Thermal Management

- 5.1.3 Transmission Thermal Management

- 5.1.4 Waste-Heat Recovery / EGR

- 5.1.5 Battery Thermal Management

- 5.1.6 Motor & Power-Electronics Cooling

- 5.2 By Technology Type

- 5.2.1 Air Cooling & Heating

- 5.2.2 Liquid Indirect Cooling

- 5.2.3 Direct / Immersion Liquid Cooling

- 5.2.4 Phase-Change / PCM Systems

- 5.2.5 Hybrid & Integrated Loops

- 5.3 By Component

- 5.3.1 Heat Exchangers (Radiator, CAC, Oil Cooler)

- 5.3.2 Compressors & Pumps

- 5.3.3 Thermal Control Valves & Manifolds

- 5.3.4 High-Voltage Coolant Heaters

- 5.3.5 Sensors & Controllers

- 5.4 By Propulsion Type

- 5.4.1 ICE Vehicles

- 5.4.2 Hybrid Electric Vehicles

- 5.4.3 Plug-in Hybrid Vehicles

- 5.4.4 Battery Electric Vehicles

- 5.4.5 Fuel-Cell Electric Vehicles

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Light Commercial Vehicles

- 5.5.3 Heavy Trucks & Buses

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 UAE

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Nigeria

- 5.6.5.7 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Denso Corporation

- 6.4.2 Hanon Systems

- 6.4.3 Valeo SE

- 6.4.4 MAHLE GmbH

- 6.4.5 Gentherm Inc.

- 6.4.6 Robert Bosch GmbH

- 6.4.7 Dana Inc.

- 6.4.8 BorgWarner Inc.

- 6.4.9 Modine Mfg. Co.

- 6.4.10 Schaeffler AG

- 6.4.11 ZF Friedrichshafen AG

- 6.4.12 Kendrion N.V.

- 6.4.13 Continental AG

- 6.4.14 TI Fluid Systems

- 6.4.15 Sanden Holdings

- 6.4.16 Boyd Corporation

- 6.4.17 VOSS Automotive

- 6.4.18 Grayson Thermal Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026年全球电动汽车温度控管系统市场研究报告

2026年全球电动汽车温度控管系统市场研究报告 电动汽车温度控管系统市场-全球产业规模、份额、趋势、机会、预测:按驱动类型、应用、技术、地区和竞争对手划分,2021-2031年

电动汽车温度控管系统市场-全球产业规模、份额、趋势、机会、预测:按驱动类型、应用、技术、地区和竞争对手划分,2021-2031年 中国新能源汽车热管理系统市场(2025-2026)

中国新能源汽车热管理系统市场(2025-2026) 电动汽车温度控管市场预测至2032年:按动力类型、组件、车辆类型、技术、应用和地区分類的全球分析2032 年汽车温度控管市场预测:按车型、推进类型、零件、应用和地区分類的全球分析2032 年电动车 (EV)热感系统市场预测:按组件、车辆类型、技术、最终用户和地区进行的全球分析

电动汽车温度控管市场预测至2032年:按动力类型、组件、车辆类型、技术、应用和地区分類的全球分析2032 年汽车温度控管市场预测:按车型、推进类型、零件、应用和地区分類的全球分析2032 年电动车 (EV)热感系统市场预测:按组件、车辆类型、技术、最终用户和地区进行的全球分析 电动汽车温度控管系统市场:2034 年市场机会与策略

电动汽车温度控管系统市场:2034 年市场机会与策略 全球汽车温度控管市场

全球汽车温度控管市场 电动车用温度控管系统的全球市场:各技术类型,用途类别,推动类别,各地区,机会,预测,2018年~2032年

电动车用温度控管系统的全球市场:各技术类型,用途类别,推动类别,各地区,机会,预测,2018年~2032年 汽车温度控管市场:按应用、车辆类型和地区划分

汽车温度控管市场:按应用、车辆类型和地区划分