|

市场调查报告书

商品编码

1940596

生物辨识技术:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Biometrics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

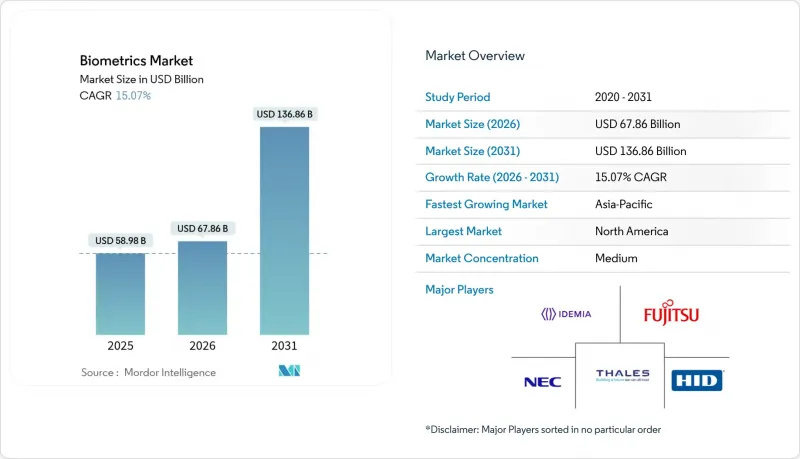

预计生物辨识市场将从 2025 年的 589.8 亿美元成长到 2026 年的 678.6 亿美元,到 2031 年将达到 1,368.6 亿美元,2026 年至 2031 年的复合年增长率为 15.07%。

政府数位身分识别项目、支付代币化技术的进步以及机场现代化建设的加速等因素推动了这一增长,所有这些因素都促使人们对无摩擦身份验证的需求日益增长。儘管硬体在目前部署中仍占据主导地位,但随着企业从点解决方案转向平台模式,云端软体引擎的成长速度最为迅猛。中国和欧盟新的隐私法规在加强合规要求的同时,也促进了兼顾准确性和使用者授权管理的多模态架构的建构。在北美,自2025年5月起实施的REAL ID法案,正推动联邦和州政府对机场和车辆管理局(DMV,即驾驶执照考试中心)的部署产生迫切的采购需求。在亚太地区,生物辨识技术与超级应用、电子钱包和银行电子KYC(电子了解你的客户)框架的融合,预计将使该地区成为长期需求成长的加速器。

全球生物辨识市场趋势与洞察

亚洲各国政府主导的国家电子识别计划

亚洲各国政府正大力推动大规模数位身分转型。例如,韩国基于智慧型手机的居民登记卡以及越南决定在2025年7月前将生物识别身份扩展到外国人,这些都为构建包容性生态系统树立了标竿。印尼斥资2亿美元打造的「INA Digital」平台以及菲律宾8,950万公民的登记计划,将使此前银行帐户享受过银行服务的成年人也能获得金融服务。斯里兰卡结合指纹、脸部和视网膜扫描的多模态计画于2026年完成,显示新兴经济体正在跨越传统基础设施的鸿沟。

EMVCo与ISO标准推动指纹支付卡的普及

EMVCo 和 ISO 的统一规则推动生物辨识卡从试点阶段走向商业发行。英飞凌的 SECORA Pay Bio 晶片和泰雷兹的全球试验正在降低误报率并提高交易限额。万事达卡的身份验证和密码支援功能承诺提供无缝认证,帮助发卡机构减少诈欺和扣回争议帐款。随着银行优先发展无密码、非接触式支付体验,供应商预计到 2028 年,生物辨识卡的出货量将达到 1.133 亿张。

GDPR和BIPA诉讼风险抑制了其应用

这些案例,包括2024年至2025年间总额超过2亿美元的《伊利诺伊州隐私法案》(BIPA)和解金,以及Clearview AI支付的5175万美元,都表明,未经明确同意部署脸部辨识的公司可能面临巨大的法律责任。 GDPR严格的资料最小化和本地处理规则,使得每次在欧洲部署的合规成本高达5万至20万欧元(约合5.65万至22.6万美元),这进一步缩小了小规模计划的可用资金基础。美国联邦贸易委员会(FTC)对Rite Aid的执法行动,为演算法偏见审核树立了美国先例,并隐私纳入设计。

细分市场分析

软体引擎从辅助角色发展成为成长最快的元件,复合年增长率达到 16.35%,而硬体则维持了 41.92% 的收入份额。各组织优先考虑云端协作、基于人工智慧的活体检测以及能够持续适应不断演变的诈骗的去中心化身份钱包。 Entrust 收购 Onfido 正契合了这一趋势,新增了深度造假防护功能,并将其在防止身分造假方面的有效性提高了五倍。

硬体领域依然至关重要,其中专用感测器提供加密模板以保护元件安全。英飞凌经认证的用于汽车应用的指纹识别晶片就是一个很好的例子,它展示了量产级组件如何将生物识别市场拓展到移动出行和门禁控制领域。服务领域虽然规模最小,但随着整合商为受监管产业量身打造多模态部署方案,其需求正稳定成长。

虹膜辨识将以17.85%的复合年增长率成长,这得益于液态透镜光学技术的应用,该技术能够降低组件成本并实现小型化。指纹辨识技术将持续保持强劲势头,到2025年将占据生物辨识市场36.55%的份额,主要得益于智慧型手机、支付卡和考勤管理系统的普及。脸部认证正在机场和体育场馆等场所稳步发展,而语音分析技术则在客服中心身份验证领域占据越来越重要的地位。

行为生物辨识技术,特别是步态模式和按键的动态特征,可以在不增加使用者负担的情况下,提供一层被动的增强安全保障。成熟的指纹和脸部认证解决方案正越来越多地与虹膜辨识、掌纹和语音辨识模组结合,形成多模态辨识套件,从而实现收入来源多元化,并降低单一认证方式的风险。

区域分析

到2025年,北美将占全球收入的30.35%,这得益于联邦政府的资金支持和私营部门的广泛应用。运输安全局)加速扩建通道,以及国土安全部(DHS)为身分国防安全保障拨出的2.508亿美元预算,将支撑未来几年对供应商的需求。加拿大和墨西哥正在对其陆地边境的电子闸门进行现代化改造,以提高贸易效率并加强洲际合作。

亚太地区预计将成为成长最快的地区,到2031年复合年增长率将达到18.10%。韩国在全国范围内推行的行动识别、中国立法实施的脸部认证法规以及印度与Aadhaar(印度居民识别系统)关联的支付服务,正在推动一个超越单一国家项目的一体化生物识别市场。该地区48亿数位钱包用户正促使银行和通讯业者将生物辨识客户身份验证(KYC)要求从可选变为强制执行。

在GDPR的严格监管下,欧洲经济持续稳定成长。欧盟边境控制系统正在申根国家实施生物辨识技术边境管制,而英国新建的信任基础设施正在推动私部门在身分验证技术领域的创新。北欧国家的试点试验表明,设备内处理能够在不牺牲速度的前提下满足隐私监管机构的要求,这有助于塑造欧洲的采购标准。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚洲各国政府主导的国家电子身分证计划

- EMVCo 和 ISO 标准推动北美和欧洲指纹支付卡的普及

- 疫情后欧洲商业不动产对非接触式实体存取的需求

- TSA的生物辨识技术蓝图推动联邦运输安全局激增

- 中国的「智慧机场2025」计画加速了脸部认证和语音辨识技术的应用

- 海湾合作委员会和非洲中央银行的生物辨识KYC强制令

- 市场限制

- GDPR和BIPA诉讼风险抑制脸部辨识技术的应用

- 演算法对深色肤色的偏见导致采购暂停

- CMOS影像感测器供不应求对指纹认证模组供应带来压力

- 南美零售连锁店的整合与投资报酬率问题

- 价值/供应链分析

- 监理展望

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业相关人员分析

- 投资与资金筹措分析

第五章 市场规模与成长预测

- 按组件

- 硬体

- 软体

- 服务

- 透过生物辨识方法

- 生理生物特征学

- 指纹辨识系统(AFIS)

- 指纹(非AFIS(自动指纹辨识系统))

- 脸部认证

- 虹膜辨识

- 其他(掌纹鑑定、手形鑑定)

- 行为生物特征学

- 语音辨识

- 签名验证

- 其他(步态分析、击键动力学)

- 生理生物特征学

- 按联络方式

- 接触式

- 非接触式

- 杂交种

- 按身份验证类型

- 单一因素

- 多种因素

- 透过使用

- 物理和逻辑存取控制

- 考勤管理

- 支付和交易认证

- 电子护照和边境管制

- 病患识别和电子健康记录 (EHR) 安全性

- 客户註册(电子身份验证)

- 公共监督与安全

- 汽车和智慧车辆接口

- 按最终用途行业划分

- 政府和执法机关

- BFSI

- 卫生保健

- 家用电子电器

- 商业和零售

- 旅行和移民

- 军事/国防

- 车

- 教育

- 其他的

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- ASEAN

- 澳洲

- 纽西兰

- 其他亚太地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 以色列

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Thales Group

- NEC Corporation

- IDEMIA France SAS

- Fujitsu Limited

- HID Global Corporation

- Assa Abloy AB

- Aware Inc.

- Suprema Inc.

- Synaptics Incorporated

- Bio-Key International Inc.

- Zwipe AS

- Fingerprint Cards AB

- M2SYS Technology

- Infineon Technologies AG

- Entrust Corporation

- ImageWare Systems Inc.

- Phonexia sro

- BioID AG

- Crossmatch Technologies Inc.

- Hitachi Ltd.

第七章 市场机会与未来展望

The biometrics market is expected to grow from USD 58.98 billion in 2025 to USD 67.86 billion in 2026 and is forecast to reach USD 136.86 billion by 2031 at 15.07% CAGR over 2026-2031.

The expansion is underpinned by government digital-ID programs, rising payments tokenization, and surging airport modernization that collectively elevate the need for frictionless identity proofing. Hardware still dominates current deployments, yet cloud-ready software engines are scaling fastest as enterprises shift from point solutions to platform models. New privacy regulations in China and the European Union are tightening compliance requirements, simultaneously encouraging multi-modal architectures that balance accuracy with consent management. In North America, REAL ID enforcement from May 2025 is driving an urgent wave of federal and state procurements for airport and DMV roll-outs. Asia Pacific's integration of biometrics into super-apps, wallets, and bank e-KYC frameworks positions the region as the long-run demand accelerator.

Global Biometrics Market Trends and Insights

Government-backed National e-ID Programs Across Asia

Asian authorities are orchestrating large-scale digital identity transformations. South Korea's smartphone-based resident registration card and Vietnam's decision to extend biometric IDs to foreign nationals by July 2025 have set benchmarks for inclusive ecosystems. Indonesia's USD 200 million INA Digital platform and the Philippines' registration of 89.5 million citizens unlock financial services for previously unbanked adults. Sri Lanka's multi-modal program combining fingerprints, face, and retina scans targets completion in 2026, illustrating how emerging economies leapfrog legacy infrastructures.

EMVCo and ISO Standards Catalyzing Fingerprint Payment Cards

Harmonized EMVCo and ISO rules have moved biometric cards from pilots to commercial issuance. Infineon's SECORA Pay Bio silicon and Thales' global trials cut false-accept rates and allow higher transaction ceilings . Mastercard's Identity Check and passkey support promise frictionless authentication, helping issuers reduce fraud and chargebacks. Vendors forecast shipments of 113.3 million biometric cards by 2028 as banks prioritize PIN-free contactless experiences.

GDPR and BIPA Litigation Risks Curtailing Roll-outs

More than USD 200 million in BIPA settlements during 2024-2025, including Clearview AI's USD 51.75 million payment, signals material liability for enterprises deploying facial recognition without explicit consent. GDPR's strict data-minimization and local-processing rules add EUR 50,000-200,000 (USD 56,500-226,000) compliance cost per European installation, shrinking the addressable base for small projects. The FTC's enforcement against Rite Aid sets a U.S. precedent for algorithmic-bias audits, compelling vendors to redesign architectures for privacy by design.

Other drivers and restraints analyzed in the detailed report include:

- U.S. TSA Biometrics Road-map Driving Federal Procurement Surge

- China's "Smart Airport 2025" Policy Accelerating Face & Voice Biometrics

- Algorithmic Bias Triggering Procurement Moratoriums

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software engines grew from a supporting role to the highest-growth component at a 16.35% CAGR, even while hardware kept the 41.92 revenue share. Organizations value cloud orchestration, AI-based liveness detection, and decentralized identity wallets that continuously adapt to evolving fraud. Entrust's acquisition of Onfido aligns with this trajectory, adding deep-fake countermeasures that improved forged-ID prevention five-fold.

The hardware segment remains indispensable where specialized sensors deliver cryptographic templates to secure elements. Infineon's automotive-qualified fingerprint ICs illustrate how production-grade components expand the biometrics market into mobility and access domains. Services, while smallest, record consistent uptake as integrators customize multi-modal deployments for regulated industries.

Iris recognition posts an 17.85% CAGR, supported by liquid-lens optics that lower bill-of-material cost and shrink form factors. Fingerprint remains entrenched with 36.55% of biometrics market share in 2025, thanks to smartphones, payment cards, and time-clock systems. Facial recognition steadily penetrates airports and stadiums, while voice analytics gains footing in call-center authentication.

Behavioral biometrics, particularly gait and keystroke dynamics, add passive layers that elevate security without user friction. Mature fingerprint and facial solutions increasingly pair with iris, palm-vein, or voice modules in multi-modal kits, diversifying revenue and diluting single-modality risk.

The Biometrics Market Report is Segmented by Component (Hardware, Software, Services), Biometric Modality (Physiological, Behavioral), Contact Type (Contact-Based, Contactless, Hybrid), Authentication Type (Single-Factor, Multi-Factor), Application (Access Control, Payment Authentication, and More), End-Use Industry (Government, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America produced 30.35% of global revenue in 2025, anchored by federal budgets and widespread private-sector adoption. TSA's accelerating lane expansions and DHS's USD 250.8 million line-item for identity management provide a multi-year demand floor for vendors . Canada and Mexico modernize land-border e-gates to streamline trade, reinforcing continental scale.

Asia Pacific records the steepest trajectory with an 18.10% CAGR forecast to 2031. South Korea's nationwide mobile-ID completion, China's codified face-recognition rules, and India's Aadhaar-linked pay services cultivate a unified biometrics market bigger than any single-country program. The region's 4.8 billion digital-wallet users push biometric KYC from optional to mandatory across banks and telecoms.

Europe's growth remains steady under strict GDPR oversight. The EU Entry/Exit System rolls out border biometrics across Schengen states, while the United Kingdom's new trust framework fosters private-sector credential innovation. Nordic pilots prove that on-device processing can satisfy privacy watchdogs without sacrificing speed, shaping procurement criteria across the continent.

- Thales Group

- NEC Corporation

- IDEMIA France SAS

- Fujitsu Limited

- HID Global Corporation

- Assa Abloy AB

- Aware Inc.

- Suprema Inc.

- Synaptics Incorporated

- Bio-Key International Inc.

- Zwipe AS

- Fingerprint Cards AB

- M2SYS Technology

- Infineon Technologies AG

- Entrust Corporation

- ImageWare Systems Inc.

- Phonexia s.r.o.

- BioID AG

- Crossmatch Technologies Inc.

- Hitachi Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-backed National e-ID Programs Across Asia

- 4.2.2 EMVCo and ISO Standards Catalyzing Fingerprint Payment Cards in North America and Europe

- 4.2.3 Post-pandemic Demand for Touch-free Physical Access in European Commercial Real-estate

- 4.2.4 U.S. TSA Biometrics Road-map Driving Federal Procurement Surge

- 4.2.5 China's "Smart Airport 2025" Policy Accelerating Face and Voice Biometrics

- 4.2.6 Biometric KYC Mandates by GCC and African Central Banks

- 4.3 Market Restraints

- 4.3.1 GDPR and BIPA Litigation Risks Curtailing Facial-Recognition Roll-outs

- 4.3.2 Algorithmic Bias Against Dark-Skin Demographics Triggering Procurement Moratoriums

- 4.3.3 CMOS Image-Sensor Shortages Constricting Fingerprint Module Supply

- 4.3.4 Integration and ROI Concerns in South-American Retail Chains

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Industry Stakeholder Analysis

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Biometric Modality

- 5.2.1 Physiological Biometrics

- 5.2.1.1 Fingerprint AFIS

- 5.2.1.2 Fingerprint Non-AFIS (Automated Fingerprint Identification System)

- 5.2.1.3 Facial Recognition

- 5.2.1.4 Iris Recognition

- 5.2.1.5 Others (Palm Vein, Hand Geometry)

- 5.2.2 Behavioral Biometrics

- 5.2.2.1 Voice Recognition

- 5.2.2.2 Signature Verification

- 5.2.2.3 Others (Gait Analysis, Keystroke Dynamics)

- 5.2.1 Physiological Biometrics

- 5.3 By Contact Type

- 5.3.1 Contact-based

- 5.3.2 Contactless

- 5.3.3 Hybrid

- 5.4 By Authentication Type

- 5.4.1 Single-factor

- 5.4.2 Multi-factor

- 5.5 By Application

- 5.5.1 Physical and Logical Access Control

- 5.5.2 Time and Attendance Management

- 5.5.3 Payment and Transaction Authentication

- 5.5.4 e-Passport and Border Control

- 5.5.5 Patient Identification and EHR Security

- 5.5.6 Customer On-boarding (eKYC)

- 5.5.7 Public Surveillance and Safety

- 5.5.8 Automotive and Smart Vehicle Interfaces

- 5.6 By End-Use Industry

- 5.6.1 Government and Law Enforcement

- 5.6.2 BFSI

- 5.6.3 Healthcare

- 5.6.4 Consumer Electronics

- 5.6.5 Commercial and Retail

- 5.6.6 Travel and Immigration

- 5.6.7 Military and Defense

- 5.6.8 Automotive

- 5.6.9 Education

- 5.6.10 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Nordics

- 5.7.3.7 Russia

- 5.7.3.8 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 ASEAN

- 5.7.4.6 Australia

- 5.7.4.7 New Zealand

- 5.7.4.8 Rest of Asia Paccific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Israel

- 5.7.5.1.5 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Kenya

- 5.7.5.2.4 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes global overview, market overview, core segments, financials, strategic information, market rank/share, products and services, recent developments)

- 6.4.1 Thales Group

- 6.4.2 NEC Corporation

- 6.4.3 IDEMIA France SAS

- 6.4.4 Fujitsu Limited

- 6.4.5 HID Global Corporation

- 6.4.6 Assa Abloy AB

- 6.4.7 Aware Inc.

- 6.4.8 Suprema Inc.

- 6.4.9 Synaptics Incorporated

- 6.4.10 Bio-Key International Inc.

- 6.4.11 Zwipe AS

- 6.4.12 Fingerprint Cards AB

- 6.4.13 M2SYS Technology

- 6.4.14 Infineon Technologies AG

- 6.4.15 Entrust Corporation

- 6.4.16 ImageWare Systems Inc.

- 6.4.17 Phonexia s.r.o.

- 6.4.18 BioID AG

- 6.4.19 Crossmatch Technologies Inc.

- 6.4.20 Hitachi Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球生物辨识市场报告

2026年全球生物辨识市场报告 指静脉认证模组:全球市占率及排名、总收入及需求预测(2026-2032)

指静脉认证模组:全球市占率及排名、总收入及需求预测(2026-2032) 步态生物辨识市场:按组件、技术、部署模式、认证模式、应用和最终用户划分-2026-2032年全球预测2026年政府生物辨识技术全球市场报告

步态生物辨识市场:按组件、技术、部署模式、认证模式、应用和最终用户划分-2026-2032年全球预测2026年政府生物辨识技术全球市场报告 低功耗生物识别晶片市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形状、材质、设备及最终用户划分智慧生物识别门禁系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及安装类型划分生物识别系统市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、部署、最终使用者、功能及安装类型划分

低功耗生物识别晶片市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形状、材质、设备及最终用户划分智慧生物识别门禁系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及安装类型划分生物识别系统市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、部署、最终使用者、功能及安装类型划分 2026-2034年全球生物识别驾驶员识别系统市场规模、份额、趋势与成长分析报告全球语音辨识交易市场规模、份额、趋势和成长分析报告(2026-2034)全球静脉认证生物辨识市场规模、份额、趋势和成长分析报告(2026-2034)

2026-2034年全球生物识别驾驶员识别系统市场规模、份额、趋势与成长分析报告全球语音辨识交易市场规模、份额、趋势和成长分析报告(2026-2034)全球静脉认证生物辨识市场规模、份额、趋势和成长分析报告(2026-2034)