|

市场调查报告书

商品编码

1940612

沼气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Biogas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

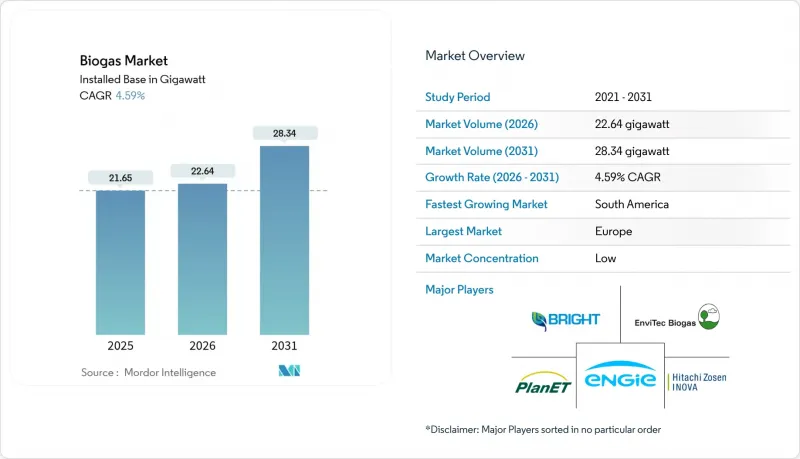

2025 年沼气市场价值为 21.65 吉瓦,预计到 2031 年将达到 28.34 吉瓦,高于 2026 年的 22.64 吉瓦。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.59%。

成熟的政策奖励、从专用电厂向可再生天然气 (RNG) 升级改造的转变,以及企业不断增加脱碳力度,正在重塑投资标准。交通燃料法规认可酪农和食品废弃物废弃物的负碳特性,公用事业公司正在整合可客製化的沼气,以稳定以太阳能和风能为主的电网。欧洲凭藉上网电价补贴 (FIT) 和併网生物甲烷基础设施保持着先发优势,但南美洲预计到 2030 年将实现 10% 的复合年增长率,这意味着新的政策框架可能会加速欠发达地区的发展。虽然 0.5 至 2 兆瓦的中型设施仍占据新增装置容量的大部分,但在分散式发电激励措施能够缩短併网等待时间的地区,0.5 兆瓦以下的区域性电站正在迅速扩张。竞争仍然激烈,像 EnviTec Biogas 这样的现有整合商透过自筹资金进行扩张来捍卫市场份额,而新参与企业则专注于模组化升级和碳捕获附加元件,以提高产量并获得优质的上网电价合约。

全球沼气市场趋势与洞察

政府支持措施和可再生能源强制规定

基于产量的税额扣抵正在取代传统的上网电价补贴,从而延长开发商的收入期限。 2025 年美国沼气税收抵免计画专注于可再生天然气 (RNG) 升级改造计划,而非电力销售。印度的压缩沼气计画透过上网电价补贴支持 5,000 座沼气厂,而波兰的 FEnIKS 计画已拨款 9,300 万美元欧盟资金以吸引更多资本。这些不断发展的措施支持分散式沼气厂,这些沼气厂能够创造农村收入、闭合营养循环并稳定电网。

公共产业和企业脱碳目标

公用事业公司目前正在评估沼气作为一种稳定能源,以填补太阳能发电量下降时出现的晚间用电需求缺口。各公司正在采购可再生天然气 (RNG),以减少范围 3 的排放并获得检验的排碳权。加州的负碳排放强度评分使得酪农衍生的 RNG 的交易价格比化石天然气高出三到四倍,从而提高了计划的内部收益率。第三方检验框架正在推动对具有透明甲烷捕集核算系统的工厂的需求。

与太阳能和风能计划相比,资本投资更高

安装成本远高于大型太阳能发电厂,高达每千瓦3000至5000美元,使得融资条款更加复杂。 EnviTec Biogas透过自筹1亿欧元新增300吉瓦时的装置容量,克服了这个挑战,实现了小规模开发商难以企及的规模经济。由于原料价格波动和营运复杂性,贷款方通常要求15%至20%的股权。

细分市场分析

至2025年,畜禽粪便将占原料供应的37.25%,并构成与农场签订长期供应合约的基础。然而,都市区掩埋禁令政策的实施将使有机废弃物转向厌氧消化,食物废弃物的复合年增长率将达到7.12%。这将为能源收入增加废弃物处理费收入。农业残余物和污水污泥可作为灵活的共消化原料,缓解季节性供需波动。

由于碳氮比平衡,将牲畜粪便和食物废弃物混合处理的厌氧消化厂通常能实现高达 827 公升/公斤的挥发性固态产量。在地方政府政策的支持下,市政废弃物收集商正积极寻求与厌氧消化厂建立合作关係,透过签订多年期入厂费合约来增强自身的财务状况。

到2025年,湿式厌氧消化器将占总装置容量的59.10%,这反映了其数十年来成熟的供应商系统和较低的资本投入。干式厌氧消化器到2031年将以7.55%的复合年增长率增长,因为其能够处理25-35%的固态,且用水量低,使其成为干旱地区和高固态废弃物处理的理想选择。

技术选择与原料特性密切相关:干式双级消化器越来越受青睐,尤其适用于处理家禽粪便、园林废弃物和预包装食品废弃物,因为它可以减少预处理步骤并降低水费。两级高温系统可实现高达 43% 的更高能源回收,但只有经验丰富的操作人员才能承担先进控制系统带来的额外成本。因此,沼气市场正在围绕各种适用的设计方案竞争,而非单一的主导製程。

沼气市场报告按原料(农业残余物、牲畜粪便、食品和饮料废弃物等)、製程技术(湿式厌氧消化、干式厌氧消化、垃圾掩埋沼气回收)、工厂容量(小于 0.5 MW、0.5-2 MW、大于 2 MW)、应用(发电、供热、车用燃料/可再生

区域分析

2025年,欧洲将占据全球65.10%的沼气市场份额,传统的上网电价补贴政策(FIT)和标准化的生物甲烷注入规范有助于降低贷款方的计划风险。光是德国就拥有400多座沼气厂,而欧盟再生能源计画(REPowerEU)设定的到2030年生物甲烷产量达到350亿立方公尺的目标,进一步推动了对管线输送级天然气的需求。丹麦是多角化发展的典范:六座沼气船用燃料厂向航运航线供应液化生物液化天然气(bio-LNG),在实现废弃物资源化利用的同时,也符合国际海事组织(IMO)的碳排放法规。

南美洲将迎来最快的成长,到2031年复合年增长率将达到9.45%。巴西国营石油公司Petrobras已发布生物甲烷采购竞标,阿根廷的农业废弃物奖励政策也促成了2024年82兆瓦生物甲烷计画的兴建。然而,管道连接和信贷风险仍然是规模化发展的障碍,开发商越来越多地聚集在甘蔗加工厂和肉类加工中心附近,因为这些地方废弃物丰富且即时收集。

北美正处于一个关键的转折点。到2024年,美国将有超过2500座设施生产每分钟140万标准立方英尺(scfm)的沼气,农业沼气计划的产量将首次超过垃圾掩埋沼气。加拿大效仿加州低碳燃料标准(LCFS)的无污染燃料法规,正在扩大对优质可再生天然气的需求。在亚太地区,印度计划在2030年建成5,000座压缩沼气厂,并为此设立了需求保障计画。同时,中国正将沼气纳入农村发展规划,将沼气池与併网微电网结合,以促进乡村电气化。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府支持和可再生能源强制规定

- 公共产业和企业脱碳目标

- 避免掩埋和循环经济废弃物指令

- 交通运输领域对可再生天然气(RNG)的需求不断增长

- 将沼渣货币化为认证生物肥料

- 联合消化与污水处理厂的综效

- 市场限制

- 与太阳能和发电工程相比,资本投资更高

- 农村地区原材料物流不完善

- 传统天然气价格的波动正在影响可再生天然气(RNG)的消费。

- 新兴市场缺乏电网连接基础设施

- 供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按原料

- 农业残余物

- 牲畜粪便

- 污水污泥

- 食物和饮料废弃物

- 能源作物

- 透过工艺技术

- 湿式厌氧消化

- 干式厌氧消化

- 掩埋气回收

- 按工厂产能

- 小于0.5兆瓦

- 0.5~2 MW

- 2兆瓦或以上

- 透过使用

- 发电

- 火力发电

- 汽车燃料/可再生天然气(RNG)

- 热电联产(CHP)

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 捷克共和国

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 泰国

- 韩国

- 马来西亚

- 印尼

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 中东和非洲

- 以色列

- 伊朗

- 南非

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、伙伴关係、购电协议)

- 市场占有率分析(主要企业的市场排名和份额)

- 公司简介

- Engie SA

- DMT International

- IES Biogas

- EnviTec Biogas AG

- Weltec Biopower GmbH

- Hitachi Zosen Inova AG

- AEV Energy GmbH

- AAT Abwasser-und Abfalltechnik GmbH

- BEKON GmbH

- Nijhuis Saur Industries

- Xebec Adsorption Inc.

- Bright Renewables BV

- Scandinavian Biogas Fuels International AB

- Naskeo Environnement

- PlanET Biogas Group

- BTS Biogas SRL

- BioConstruct GmbH

- Wartsila Corporation

- Greenlane Renewables Inc.

- Clarke Energy

第七章 市场机会与未来展望

The Biogas Market was valued at 21.65 gigawatt in 2025 and estimated to grow from 22.64 gigawatt in 2026 to reach 28.34 gigawatt by 2031, at a CAGR of 4.59% during the forecast period (2026-2031).

Maturing policy incentives, a pivot from power-only plants to renewable natural gas (RNG) upgrading, and rising corporate decarbonization commitments are re-shaping investment criteria. Transport fuel mandates reward the negative-carbon attributes of dairy and food-waste gas, while utilities integrate dispatchable biogas to stabilize solar- and wind-heavy grids. Europe retains first-mover advantage because of feed-in tariffs and grid-ready biomethane infrastructure, but South America's 10% CAGR through 2030 underlines how fresh policy frameworks can accelerate late-entry regions. Mid-scale 0.5-2 MW facilities still dominate capacity additions, yet sub-0.5 MW community plants are scaling quickly where distributed-generation incentives cut connection queues. Competitive intensity remains high: established integrators such as EnviTec Biogas defend their share by self-funding capacity, whereas new entrants focus on modular upgrading and carbon capture add-ons to lift yields and secure premium offtake contracts.

Global Biogas Market Trends and Insights

Supportive Government Incentives & Renewable Energy Mandates

Production-based tax credits are replacing legacy feed-in tariffs, lengthening revenue visibility for developers. The 2025 U.S. biogas credit pivots projects toward RNG upgrading rather than electricity sales. India's Compressed Bio-Gas scheme backs 5,000 plants with fixed offtake, and Poland's FEnIKS program allocates USD 93 million, leveraging European Union funds to crowd-in further capital. These evolving instruments favor distributed plants that unlock rural income, close nutrient loops, and stabilize the grid.

Decarbonization Targets of Utilities & Corporates

Utilities now value biogas as a firming resource that fills evening demand gaps when solar output fades. Corporates procure RNG to cut Scope 3 emissions and lock in verifiable carbon credits. Negative-carbon intensity scores in California let dairy RNG trade at premiums 3-4 times fossil gas, raising project internal rates of return. Third-party verification frameworks elevate demand for plants with transparent methane-capture accounting.

High Capex Relative to Solar & Wind Projects

Installed costs of USD 3,000-5,000/kW outstrip utility-scale solar, complicating debt terms. EnviTec Biogas offsets this by self-funding EUR 100 million to add 300 GWh capacity, capturing economies of scale that smaller developers cannot. Because of feedstock volatility and operational complexity, lenders typically demand 15-20% equity.

Other drivers and restraints analyzed in the detailed report include:

- Landfill Diversion & Circular-Economy Waste Directives

- Rising Demand for Renewable Natural Gas in Transport

- Sub-optimal Feedstock Logistics in Rural Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Livestock manure delivered 37.25% of feedstock input in 2025 and anchors long-term supply agreements with farms. Yet food-waste volumes expand 7.12% CAGR as cities adopt landfill bans that shift organics toward digesters, adding tipping-fee revenue to energy income. Agricultural residues and sewage sludge are flexible co-digestion recipes that smooth seasonal imbalances.

Digesters blending manure with food scraps regularly hit 827 L/kg volatile solids yields, thanks to balanced C:N ratios. Municipal policy support means urban waste haulers actively seek digester partners, letting operators lock multi-year gate-fee contracts that strengthen balance sheets.

Wet digestion systems owned 59.10% of 2025 installations, reflecting decades-long supplier ecosystems and lower capex. Dry digestion grows 7.55% CAGR to 2031 because it tolerates 25-35% solids and uses less water, ideal for arid locations or high-solids waste.

Technology selection correlates with feedstock profile: poultry litter, yard trimmings, or packaged food waste increasingly favors dry twin-digester lines that cut preprocessing steps and water bills. Two-stage thermophilic setups achieve up to 43% higher energy recovery, yet only sophisticated operators absorb the extra control-system costs. The biogas market, therefore, segments around fit-for-purpose designs rather than a single dominant process.

The Biogas Market Report is Segmented by Feedstock (Agri Residues, Livestock Manure, Food and Beverage Waste, and More), Process Technology (Wet Anaerobic, Dry Anaerobic Digestion, and Landfill Gas Recovery), Plant Capacity (Below 0. 5 MW, 0. 5 To 2 MW, Above 2 MW), Application (Electricity Generation, Heat Generation, Vehicle Fuel/RNG, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More).

Geography Analysis

Europe held 65.10% of the biogas market share 2025 as legacy feed-in tariffs and standardized biomethane injection codes derisk projects for lenders. Germany alone hosts more than 400 plants, and the REPowerEU goal of 35 bcm of biomethane by 2030 further lifts pipeline-quality gas demand. Denmark illustrates diversification: six biogas-to-marine-fuel plants supply liquefied bio-LNG to shipping lanes, marrying waste valorization with IMO carbon rules.

South America records the fastest expansion at 9.45% CAGR through 2031 as Brazil's Petrobras issues biomethane tenders and Argentina adds 82 MW in 2024 under agricultural-waste incentives. However, pipeline access and credit risk still hamper scale-up, so developers often cluster near sugarcane mills or meat-packing hubs where waste is abundant and offtake immediate.

North America stands at an inflection point: over 2,500 U.S. sites generated 1.4 million scfm in 2024, and agricultural projects exceeded landfill gas for the first time. Canada's Clean Fuel Regulations mimic California's LCFS, widening premium RNG catchment. In Asia-Pacific, India targets 5,000 compressed biogas plants by 2030, supported by guaranteed offtake, while China embeds biogas within rural revitalization plans, pairing digesters with grid-connected micro-grids for village electrification.

- Engie SA

- DMT International

- IES Biogas

- EnviTec Biogas AG

- Weltec Biopower GmbH

- Hitachi Zosen Inova AG

- AEV Energy GmbH

- AAT Abwasser- und Abfalltechnik GmbH

- BEKON GmbH

- Nijhuis Saur Industries

- Xebec Adsorption Inc.

- Bright Renewables BV

- Scandinavian Biogas Fuels International AB

- Naskeo Environnement

- PlanET Biogas Group

- BTS Biogas SRL

- BioConstruct GmbH

- Wartsila Corporation

- Greenlane Renewables Inc.

- Clarke Energy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Supportive government incentives & renewable energy mandates

- 4.2.2 Decarbonisation targets of utilities & corporates

- 4.2.3 Landfill diversion & circular-economy waste directives

- 4.2.4 Rising demand for renewable natural gas (RNG) in transport

- 4.2.5 Monetisation of digestate as certified bio-fertiliser

- 4.2.6 Co-digestion synergies with wastewater treatment plants

- 4.3 Market Restraints

- 4.3.1 High capex relative to solar & wind projects

- 4.3.2 Sub-optimal feedstock logistics in rural areas

- 4.3.3 Price volatility of conventional natural gas affecting RNG offtake

- 4.3.4 Limited grid-injection infrastructure in emerging markets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Feedstock

- 5.1.1 Agricultural Residues

- 5.1.2 Livestock Manure

- 5.1.3 Sewage Sludge

- 5.1.4 Food and Beverage Waste

- 5.1.5 Energy Crops

- 5.2 By Process Technology

- 5.2.1 Wet Anaerobic Digestion

- 5.2.2 Dry Anaerobic Digestion

- 5.2.3 Landfill Gas Recovery

- 5.3 By Plant Capacity

- 5.3.1 Below 0.5 MW

- 5.3.2 0.5 to 2 MW

- 5.3.3 Above 2 MW

- 5.4 By Application

- 5.4.1 Electricity Generation

- 5.4.2 Heat Generation

- 5.4.3 Vehicle Fuel/RNG

- 5.4.4 Combined Heat and Power (CHP)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Czech Republic

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 Thailand

- 5.5.3.4 South Korea

- 5.5.3.5 Malaysia

- 5.5.3.6 Indonesia

- 5.5.3.7 Australia

- 5.5.3.8 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Israel

- 5.5.5.2 Iran

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Engie SA

- 6.4.2 DMT International

- 6.4.3 IES Biogas

- 6.4.4 EnviTec Biogas AG

- 6.4.5 Weltec Biopower GmbH

- 6.4.6 Hitachi Zosen Inova AG

- 6.4.7 AEV Energy GmbH

- 6.4.8 AAT Abwasser- und Abfalltechnik GmbH

- 6.4.9 BEKON GmbH

- 6.4.10 Nijhuis Saur Industries

- 6.4.11 Xebec Adsorption Inc.

- 6.4.12 Bright Renewables BV

- 6.4.13 Scandinavian Biogas Fuels International AB

- 6.4.14 Naskeo Environnement

- 6.4.15 PlanET Biogas Group

- 6.4.16 BTS Biogas SRL

- 6.4.17 BioConstruct GmbH

- 6.4.18 Wartsila Corporation

- 6.4.19 Greenlane Renewables Inc.

- 6.4.20 Clarke Energy

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球废弃物衍生沼气市场报告2026年全球沼气市场报告

2026年全球废弃物衍生沼气市场报告2026年全球沼气市场报告 生质气化发电系统市场:按原料类型、技术、工厂容量、压力和最终用户分類的全球预测,2026-2032年

生质气化发电系统市场:按原料类型、技术、工厂容量、压力和最终用户分類的全球预测,2026-2032年 2026-2030年全球沼气市场

2026-2030年全球沼气市场 沼气市场规模、份额和成长分析(按原料、来源、技术、应用、最终用途和地区划分)-2026-2033年产业预测2026年全球沼气重整设备市场报告

沼气市场规模、份额和成长分析(按原料、来源、技术、应用、最终用途和地区划分)-2026-2033年产业预测2026年全球沼气重整设备市场报告 沼气市场-全球产业规模、份额、趋势、机会、预测:按来源、应用、区域和竞争格局划分,2021-2031年沼气储存市场按储存类型、储存材料、容量、压力和应用划分,全球预测(2026-2032年)沼气膜技术市场(按膜类型、容量、压力、组件、运作模式、应用和最终用户划分)—全球预测,2026-2032年沼气过滤器市场按过滤器类型、应用、滤材类型、最终用户和分销管道划分-全球预测(2026-2032 年)

沼气市场-全球产业规模、份额、趋势、机会、预测:按来源、应用、区域和竞争格局划分,2021-2031年沼气储存市场按储存类型、储存材料、容量、压力和应用划分,全球预测(2026-2032年)沼气膜技术市场(按膜类型、容量、压力、组件、运作模式、应用和最终用户划分)—全球预测,2026-2032年沼气过滤器市场按过滤器类型、应用、滤材类型、最终用户和分销管道划分-全球预测(2026-2032 年)