|

市场调查报告书

商品编码

1940620

铝製瓶盖和封盖:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)Aluminum Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

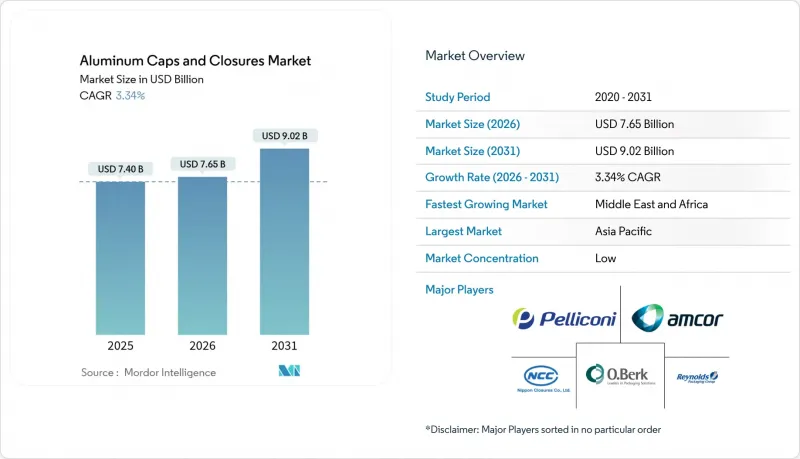

预计铝製瓶盖和瓶塞市场将从 2025 年的 74 亿美元成长到 2026 年的 76.5 亿美元,到 2031 年将达到 90.2 亿美元,2026 年至 2031 年的复合年增长率为 3.34%。

由于主要饮料细分市场的渗透率已趋于成熟,需求成长并非爆发式成长,而是循序渐进。然而,高端烈酒市场需求的成长、生物製药包装需求的增加以及欧盟永续性法规的日益严格,持续开拓着盈利市场。欧洲强制性瓶盖固定法规、中国对再生铝的激励措施以及北美市场向高端即饮产品的转变,都促使品牌所有者重新设计瓶盖,以提升其功能性和美观性。儘管伦敦金属交易所 (LME) 的价格波动给加工商的利润率带来了压力,但对可无限循环利用材料日益增长的需求,仍然使铝材优于软木、钢材和塑胶。区域成本优势,尤其是在亚太地区,以及不断增长的回收能力,有助于抵消原材料价格波动的影响,同时继续使高端市场免受低成本 PET 替代品的衝击。

全球铝製瓶盖及瓶塞市场趋势及洞察

北美高端即饮鸡尾酒铝瓶包装的兴起

2024年,高端即饮鸡尾酒品牌纷纷推出铝瓶,在保持可回收性的同时,将自身定位为高端产品。有些品牌的铝瓶售价比传统易拉罐高出40%至60%,显示消费者非常重视包装的触感耐用性和再封功能。铝的阻隔性能可以保护植物萃取物免受紫外线和氧气的侵害,从而延长以烈酒为基底的配方的保质期。与环保组织的合作进一步强化了永续性的形象,创造了小型钢罐或宝特瓶无法实现的行销优势。这种趋势也正在欧洲旅游零售市场蔓延,那里的烈酒需要既防窜改又美观的包装。

欧盟饮料包装必须使用繫绳式瓶盖(指令 2019/904)

自2024年7月起,欧盟将强制所有饮料瓶使用繫绳式瓶盖,促使碳酸饮料和矿泉水产业重新设计瓶盖。儘管消费者最初对塑胶繫绳式瓶盖有所抵触,但高端矿泉水和果汁品牌已转向使用带有整合式铰链机构的铝製螺旋盖。铝的无限可回收性和在资源回收设施中易于分离的特性,使品牌所有者能够同时满足繫绳式瓶盖法规和即将实现的90%金属回收目标。跨国公司也在非欧盟市场推行包装标准化,以避免生产线变更的复杂性,推动了近期对高价值铝製瓶盖的需求。

伦敦金属交易所(LME)铝价波动对加工商的利润率带来压力。

2025年2月,铝锭价格达到每吨2,662美元,六个月内波动超过15%。签订长期固定合约的加工商面临压力。规模较小的生产商由于缺乏避险机制,利润率不断下降,成为拥有完善风险管理部门的跨国公司的理想收购目标。俄罗斯出口的不确定性、欧洲冶炼电力成本的上涨以及美国新的货柜关税加剧了这种波动。为了稳定供应,大型加工商正在探索提高再生铝含量和使用废钢的合金配方,这些配方符合碳减排承诺,但需要投入资金升级退火炉。

细分市场分析

螺旋盖广泛应用于饮料、调味品和医药产业,预计2025年将维持其主导地位,市占率高达50.74%。这一份额意味着2025年铝製盖和封盖市场规模将达到37.5亿美元,体现了其可靠的密封性能。易开盖虽然体积较小,但预计到2031年将以6.38%的复合年增长率快速增长,这主要得益于消费者对罐装咖啡和蒸馏食品便利性的需求日益增长。连续螺纹ROPP盖在精酿烈酒市场中占据了重要地位,兼具防篡改功能和高端视觉吸引力。皇冠盖在传统啤酒包装中仍占据重要地位,但随着纤细罐装啤酒的普及,其成长速度正在放缓。卡扣盖、按压旋转盖和特殊翻盖设计则针对食品和医药等对篡改敏感的应用领域,标誌着该领域正从「一刀切」的解决方案转向针对特定应用场景的解决方案。

对模切和压痕技术的投资,使得瓶盖拉环更安全、更易于手指抓握,从而开闢了新的大众市场,例如老年人营养饮品市场。瓶盖製造商还在瓶盖上整合雷射雕刻的QR码,在不牺牲装饰空间的前提下实现产品溯源。这些装饰元素提高了单位成本,在原料成本上涨的当下,有效提升了利润率。同时,标准的螺旋盖形式日益趋于同质化,迫使製造商透过改进内衬化学成分来提升产品差异化,从而延长高pH值饮料的保质期。

到2025年,饮料业将占铝製瓶盖和封盖市场(价值34.1亿美元)的46.02%。该领域涵盖矿泉水、碳酸饮料、啤酒、葡萄酒和顶级烈酒,每种产品都有其独特的封盖要求。高檔酒类生产商将铝作为品牌宣传的载体,而碳酸饮料填充商则寻求以最低成本满足欧盟的Tether法规要求。预计製药业的需求将以6.76%的复合年增长率成长,到2031年将创造2.84亿美元的附加价值。这一增长主要得益于生物製药新产品的推出,这些产品指定使用翻盖式易碎密封件以确保无菌性。食品应用领域的需求保持稳定,这主要得益于高檔食用油和酱料采用金属凸耳盖以实现顺畅的倾倒控制。个人护理品牌正在强调铝的可回收性并取代复合材料封盖,例如,采用可回收铝製气雾罐容器的高调推出的除臭剂产品就体现了这一点。

跨行业经验正在推动创新:一家饮料罐供应商正与一家化妆品公司合作,改进其内清漆,使其与乳液相容,从而扩大其目标市场。工业化学品罐盖虽然是一个小众市场,但铝的耐腐蚀性与专用内衬相结合,正使其在市场中占据优势。多种应用情境的通用性有助于建立均衡的产品组合,从而对冲特定产业的週期性低迷风险。

铝製瓶盖及封盖市场按瓶盖类型(螺旋盖、皇冠盖、按压式/旋盖等)、应用领域(饮料、食品、医药、化妆品及个人护理等)、瓶颈直径(20毫米以下、21-30毫米等)、通路(销售管道、间接销售管道)和地区进行细分。市场规模和预测均以美元以金额为准。

区域分析

亚太地区受中国丰富的饮料产量和印度包装产品市场的扩张所推动,预计到2025年将占全球收入的40.20%。中国于2024年11月取消进口再生铝关税,提高了成本竞争力,使冶炼厂能够以低于原铝的价格供应铝捲。日本和韩国正将技术进步引入该地区,出口瓶盖压平机和视觉检测系统。东南亚的需求受到都市化和西方快餐连锁店对防篡改瓶盖的需求的推动,刺激了当地瓶盖加工厂的发展。在印度,食用油包装上强制使用QR码追踪,提高了包装标准,扩大了高端旋盖的价值份额,并鼓励外资合资企业进入市场。

预计中东和非洲地区将成为成长最快的市场,到2031年复合年增长率将达到6.89%。尼日利亚和肯亚的饮料投资以及海湾地区瓶装淡化水产能的提升支撑了市场需求。然而,循环经济基础设施的匮乏限制了铝盖子与封口装置的市场渗透。儘管埃及在建立专门的食品级回收工厂方面取得了进展,但建立经济永续的回收管道是实现广泛应用的先决条件。在南非,完善的铝冶炼基础设施和港口连接为这个内陆国家创造了出口机会。

儘管欧洲市场已趋于成熟,但由于法规主导全球规范,它仍然至关重要。 2024年7月固定瓶盖强制令的最后期限迫使灌装商同时重新设计PET和铝製容器,为瓶盖专家带来了工程咨询收入。一家德国机械工程丛集开发了每分钟可生产600个产品的连续螺纹螺旋盖机,并整合了扭力监控功能,提高了性能标准。一家义大利设计公司为高端烈酒定制了压纹和变色油墨,在从软木塞向铝製瓶盖永续性过渡的过程中,保持了产品的高端质感。

北美市场正在成长,这主要得益于消费者对可重复密封铝瓶装精酿饮料和即饮鸡尾酒的需求增加。美国于2025年4月生效的关税壁垒间接支持了瓶盖卷材製造商,一方面鼓励国内罐体库存生产,另一方面由于供应紧张,促使生产商重返日本市场。墨西哥是主要的啤酒出口国,为了平衡成本和供应风险,该国同时使用铝製和钢製瓶盖材料。然而,铝製瓶盖在欧洲高端瓶装饮料生产线上仍然占据一定地位。在南美洲,尤其是巴西,各公司正在投资建造配备内部瓶盖生产模组的新型饮料罐生产线,以缩短前置作业时间。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 北美高端即饮鸡尾酒铝瓶包装的兴起

- 欧盟饮料包装强制过渡到繫绳式瓶盖(指令 2019/904)

- 中国扩大饮料用再生铝产能

- 製药业向生物製药用翻盖式铝製密封过渡

- 欧洲精酿烈酒包装从软木塞到铝製ROPP的过渡

- 印度电子商务洩漏测试通讯协定推动 RagCap 的普及

- 市场限制

- 伦敦金属交易所(LME)铝价波动对加工商利润带来压力

- 品牌商在碳酸饮料中改用PET材质的瓶盖

- 墨西哥啤酒中无锡钢皇冠瓶塞的替代

- 中东地区对食品级回收途径的限制

- 供应链分析

- 技术展望

- 监理展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

第五章 市场规模与成长预测

- 按帽型

- 螺帽

- 皇冠软木塞

- 凸耳/按压式

- 易打开端

- 滚动式防盗装置(ROPP)

- 其他(竖中指、拆解)

- 透过使用

- 饮料

- 酒精饮料

- 不含酒精的饮料

- 食物

- 製药

- 化妆品和个人护理

- 工业和家用化学品

- 饮料

- 颈部直径

- 20毫米或更小

- 21-30 mm

- 31-40 mm

- 40毫米或以上

- 透过分销管道

- 销售管道

- 间接销售管道

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 义大利

- 英国

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- ASEAN

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 肯亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor plc

- Crown Holdings Inc.

- Silgan Holdings Inc.

- Guala Closures SpA

- Tecnocap Group

- Pelliconi and C. SpA

- Nippon Closures Co. Ltd

- Closure Systems International(CSI)

- Berlin Packaging LLC

- Bericap GmbH

- AptarGroup Inc.

- SKS Bottle and Packaging Inc.

- Hicap Closures Co. Ltd

- Federfin Tech SRL

- Rauh GmbH & Co.

- O.Berk Company

- The Cary Company

- Alutop SAS

- Shandong Lipeng Co. Ltd

- Idea Cap SRL

- Easy Open Lid Industry Corp.(Yiwu)

- RPC Group(PET Power)

第七章 市场机会与未来展望

The aluminium caps and closures market is expected to grow from USD 7.40 billion in 2025 to USD 7.65 billion in 2026 and is forecast to reach USD 9.02 billion by 2031 at 3.34% CAGR over 2026-2031.

Demand growth is paced, not explosive, because penetration in core beverage segments is mature; however, upgrades in premium spirits, biologics packaging, and EU sustainability rules continue to open profitable niches. Mandatory tethered-cap regulations in Europe, recycled-aluminium incentives in China, and a shift toward premium ready-to-drink offerings in North America are prompting brand owners to redesign closures with higher functional and aesthetic value. Volatility in London Metal Exchange (LME) pricing tightens converter margins, yet the push for infinitely recyclable materials still tilts preference toward aluminium over cork, steel, or plastic. Regional cost advantages particularly additional recycled capacity in Asia-Pacific are helping offset raw-material swings while keeping premium segments insulated from low-cost PET alternatives.

Global Aluminum Caps And Closures Market Trends and Insights

Rise of Premium RTD-Cocktail Aluminium Bottling in North America

Premium ready-to-drink cocktail brands introduced aluminium bottles throughout 2024 to signal upscale positioning while retaining recyclability. Several brands recorded 40-60% price premiums versus conventional cans, indicating consumers value tactile rigidity and re-close functionality. The barrier performance of aluminium protects botanical extracts from UV light and oxygen, supporting shelf life for spirit-based formulations. Brand collaborations with environmental non-profits reinforce sustainable credentials, creating a marketing halo that smaller steel or PET formats cannot match. The phenomenon is spilling into European travel-retail channels where single-serve spirits require tamper-evident yet elegant closures.

Mandatory Transition to Tethered Caps in EU Beverage Packaging (Directive 2019/904)

Since July 2024, EU beverage bottles must feature tethered closures, sparking redesign activity across carbonated soft drink and water segments.Early consumer pushback against plastic tethered systems led premium water and juice brands to adopt aluminium screw-top variants with integrated hinge mechanisms. Because aluminium is infinitely recyclable and easily detached in material-recovery facilities, brand owners meet both tethered-cap rules and forthcoming 90% metal-collection targets. Multinationals are harmonizing pack formats across non-EU markets to avoid line-change complexity, magnifying near-term demand for value-added aluminium closures.

Volatile LME Aluminium Prices Compressing Converter Margins

Aluminium ingot reached USD 2,662 per ton in February 2025, swinging more than 15% within six months and squeezing converters that sell on long-term fixed contracts. Smaller closure firms without hedging programs face eroded margins, making them attractive acquisition targets for multinationals with advanced risk-management desks. Russian export uncertainty, elevated European smelting power costs, and new US container duties all amplify volatility. To stabilize supply, leading converters raise recycled content and explore alloy recipes with higher scrap tolerance, an approach aligned with carbon-reduction pledges yet requiring capital spend on upgraded annealing furnaces.

Other drivers and restraints analyzed in the detailed report include:

- Beverage-Grade Recycled Aluminium Capacity Expansions in China

- Pharma Shift to Flip-Off Tear-Down Aluminium Seals for Biologics

- Brand-Owner Switch to PET Tethered Caps in Carbonated Soft Drinks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Screw caps retained dominance with 50.74% share in 2025 as they span beverages, condiments, and pharmaceuticals. That share equals USD 3.75 billion of the aluminium caps and closures market size in 2025, reflecting their proven sealing reliability. Easy-open ends, while smaller, are gaining fastest at a 6.38% CAGR through 2031 as consumers gravitate toward convenience features in canned coffee and ready meals. Continuous-thread ROPP variants secure traction in craft spirits because they reconcile tamper evidence with luxury visual cues. Crown corks hold relevance in traditional beer packaging, yet their growth is modest given the migration toward full-body slim cans. Lug, press-twist, and specialized flip-off designs serve tamper-sensitive food and pharma uses, illustrating the segmentation's shift from generalist to application-specific solutions.

Investment is flowing into die-cutting and scoring technologies that create safer, finger-friendly easy-open tabs, unlocking new mass channels like senior-nutrition beverages. Closure makers are also integrating laser-etched QR codes for trace-and-trace compliance without compromising decoration space. These embellishments carry higher unit economics, cushioning margins when raw-material costs rise. In contrast, standard screw-cap formats face commoditization, pressing manufacturers to differentiate through liner chemistry improvements that extend shelf life in aggressive-pH drinks.

Beverages commanded 46.02% share in 2025, equivalent to USD 3.41 billion of the aluminium caps and closures market. The segment covers still water, carbonated drinks, beer, wine, and premium spirits, each with nuanced closure needs. Premium alcohol producers elevate aluminium as a branding canvas, whereas carbonated soft-drink fillers chase lowest cost compliance to EU tethering. Pharmaceutical demand is expanding at a 6.76% CAGR, adding USD 284 million incremental value by 2031. Growth rests on biologic drug launches that specify flip-off tear-down seals to ensure sterile integrity. Food applications remain steady, propelled by gourmet oils and sauces pursuing metal lug caps for smooth pour control. Personal-care brands leverage aluminium's recyclability story to displace mixed-material lids, evidenced by high-profile deodorant launches in recyclable aluminium aerosols.

Cross-sector learning accelerates innovation: beverage can suppliers partner with personal-care companies to adapt internal varnishes for lotion compatibility, broadening addressable markets. Industrial chemical closures, though niche, benefit from aluminium's corrosion resistance when combined with specialty liners. The versatility across end-uses supports balanced portfolio exposure, hedging against cyclical dips in any one sector.

Aluminum Caps and Closures Market is Segmented by Cap Type (Screw Caps, Crown Cork, Lugs/Press Twist, and More), Application (Beverages, Food, Pharmaceutical, Cosmetics and Personal Care, and More), Neck Finish Diameter ( Less Than and Equal To 20mm, 21-30mm, and More), Distribution Channel (Direct Sales Channels, and Indirect Sales Channels) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 40.20% of global revenue in 2025, driven by China's prolific beverage output and India's packaged-goods expansion. Cost competitiveness improved after November 2024 when China abolished tariffs on imported recycled aluminium, enabling mills to supply coil at discounts versus primary metal. Japan and South Korea added a layer of technological sophistication, exporting closure presses and vision-inspection systems regionally. Southeast Asian demand benefitted from urbanization and Western quick-service restaurant chains insisting on tamper-proof lids, stimulating local cap conversion lines. India's standards upgrade mandating QR traceability for edible-oil packs nudged value share toward premium lug caps, attracting foreign joint ventures.

The Middle East and Africa represent the fastest-growing territory, forecast at 6.89% CAGR through 2031. Beverage investments in Nigeria and Kenya, plus desalinated bottled-water capacity in the Gulf, underpin volume. However, limited circular-economy infrastructure tempers aluminium caps and closures market penetration. Egypt's move to establish a dedicated food-grade recycling mill marks progress, yet widespread adoption awaits proof of economically viable collection streams. South Africa's established aluminium smelter base and port connectivity create export opportunities into landlocked neighbors.

Europe, though mature, remains pivotal because regulation steers global specifications. The July 2024 tethered-cap deadline forced fillers to redesign PET and aluminium containers simultaneously, generating engineering consulting revenue for closure specialists. Germany's mechanical-engineering cluster pioneered continuous-thread screw-top machines capable of 600 cpm with integrated torque monitoring, raising performance benchmarks. Italy's design houses customized embossing and color-shift inks for premium spirits, preserving perceived luxury even as closures migrate from cork to aluminium for sustainability reasons.

North America's market rides consumer migration to craft beverages and ready-to-drink cocktails packaged in resealable aluminium bottles. US tariff barriers imposed in April 2025 boosted domestic can-stock production, indirectly supporting closure coil producers by tightening local supply and encouraging reshoring. Mexico, a major beer exporter, toggles between aluminium and steel closure options to balance cost and supply risk, yet aluminium retains a foothold in premium bottle lines destined for European customers. South America, led by Brazil, invests in new beverage can lines that include in-house closure modules, shortening lead times.

- Amcor plc

- Crown Holdings Inc.

- Silgan Holdings Inc.

- Guala Closures S.p.A

- Tecnocap Group

- Pelliconi and C. SpA

- Nippon Closures Co. Ltd

- Closure Systems International (CSI)

- Berlin Packaging LLC

- Bericap GmbH

- AptarGroup Inc.

- SKS Bottle and Packaging Inc.

- Hicap Closures Co. Ltd

- Federfin Tech SRL

- Rauh GmbH & Co.

- O.Berk Company

- The Cary Company

- Alutop SAS

- Shandong Lipeng Co. Ltd

- Idea Cap SRL

- Easy Open Lid Industry Corp. (Yiwu)

- RPC Group (PET Power)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise of Premium RTD-Cocktail Aluminium Bottling in North America

- 4.2.2 Mandatory Transition to Tethered Caps in EU Beverage Packaging (Directive 2019/904)

- 4.2.3 Beverage-Grade Recycled Aluminium Capacity Expansions in China

- 4.2.4 Pharma Shift to Flip-Off Tear-Down Aluminium Seals for Biologics

- 4.2.5 Craft Spirits Migration from Cork to Aluminium ROPP in Europe

- 4.2.6 E-commerce Leakage-Testing Protocols Driving Lug Cap Adoption in India

- 4.3 Market Restraints

- 4.3.1 Volatile LME Aluminium Prices Compressing Converter Margins

- 4.3.2 Brand-Owner Switch to PET Tethered Caps in Carbonated Soft Drinks

- 4.3.3 Tin-Free Steel Crown Cork Substitution in Mexican Beer

- 4.3.4 Limited Food-Grade Recycling Streams in Middle East

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cap Type

- 5.1.1 Screw Caps

- 5.1.2 Crown Cork

- 5.1.3 Lug / Press-Twist

- 5.1.4 Easy-Open End

- 5.1.5 Roll-On Pilfer Proof (ROPP)

- 5.1.6 Others (Flip-Off, Tear-Down)

- 5.2 By Application

- 5.2.1 Beverages

- 5.2.1.1 Alcoholic Beverages

- 5.2.1.2 Non-Alcoholic Beverages

- 5.2.2 Food

- 5.2.3 Pharmaceutical

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Industrial and Household Chemicals

- 5.2.1 Beverages

- 5.3 By Neck Finish Diameter

- 5.3.1 Less than and Equal to 20 mm

- 5.3.2 21-30 mm

- 5.3.3 31-40 mm

- 5.3.4 More than 40 mm

- 5.4 By Distribution Channels

- 5.4.1 Direct Sales Channels

- 5.4.2 Indirect Sales Channels

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 Italy

- 5.5.2.4 United Kingdom

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Amcor plc

- 6.4.2 Crown Holdings Inc.

- 6.4.3 Silgan Holdings Inc.

- 6.4.4 Guala Closures S.p.A

- 6.4.5 Tecnocap Group

- 6.4.6 Pelliconi and C. SpA

- 6.4.7 Nippon Closures Co. Ltd

- 6.4.8 Closure Systems International (CSI)

- 6.4.9 Berlin Packaging LLC

- 6.4.10 Bericap GmbH

- 6.4.11 AptarGroup Inc.

- 6.4.12 SKS Bottle and Packaging Inc.

- 6.4.13 Hicap Closures Co. Ltd

- 6.4.14 Federfin Tech SRL

- 6.4.15 Rauh GmbH & Co.

- 6.4.16 O.Berk Company

- 6.4.17 The Cary Company

- 6.4.18 Alutop SAS

- 6.4.19 Shandong Lipeng Co. Ltd

- 6.4.20 Idea Cap SRL

- 6.4.21 Easy Open Lid Industry Corp. (Yiwu)

- 6.4.22 RPC Group (PET Power)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

2026-2034年全球铝製盖子与封口装置市场规模、份额、趋势和成长分析报告

2026-2034年全球铝製盖子与封口装置市场规模、份额、趋势和成长分析报告 铝瓶盖和封口市场(按封口类型、最终用途产业、生产技术、瓶盖尺寸和分销管道)—2025-2032 年全球预测

铝瓶盖和封口市场(按封口类型、最终用途产业、生产技术、瓶盖尺寸和分销管道)—2025-2032 年全球预测 铝盖和瓶盖市场、机会、成长动力、产业趋势分析与预测,2024-2032

铝盖和瓶盖市场、机会、成长动力、产业趋势分析与预测,2024-2032