|

市场调查报告书

商品编码

1940621

协作机器人:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Collaborative Robot - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

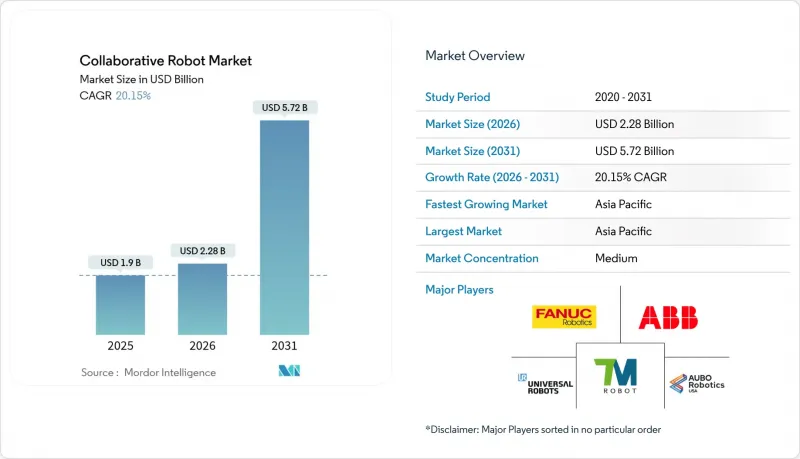

预计到 2025 年,协作机器人市场价值将达到 19 亿美元,到 2031 年将达到 57.2 亿美元,高于 2026 年的 22.8 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 20.15%。

更新后的 ISO/TS 15066 标准明确了安全要求,税收优惠缩短了投资回收期,劳动力短缺也使得弹性自动化迫在眉睫,这些因素共同推动了市场需求。製造商越来越多地采用协作机器人来提高生产效率,而非取代工人,而日益成熟的软体和简化的程式流程正在缩短引进週期。有效载荷能力的提升、仓库自动化需求的成长以及服务业应用场景的不断扩展,都在推动全球价值链中协作机器人的普及应用。

全球协作机器人市场趋势与洞察

针对多品种、小批量生产的经济高效的搬迁方案

在欧洲和北美的工厂里,协作机器人现在在同一班次内轮换使用组装单元,将换线时间从数週缩短到数小时。这种灵活性使汽车供应商能够承接利润率小规模、规模更小的订单,同时也能享受自动化带来的优势。

为中小企业推广即插即用的协作机器人OEM业务

新型控制器、简化的布线和预先载入的任务库使中小製造商无需专业整合商即可采用协作机器人。 Universal Robots 的 UR 系列升级版透过更快的循环时间和直觉的手动引导,降低了整体拥有成本,从而为成千上万的首次用户打开了协作机器人市场的大门。

现有PLC架构中的整合瓶颈

传统 PLC 通常缺乏即时乙太网路或安全操作通道,而将协作机器人添加到使用了几十年的生产线上需要高成本的控制器升级——这些费用导致一些汽车工厂推迟采用协作机器人,直到对整条生产线维修。

细分市场分析

截至2025年,5公斤以下的协作机器人占据了52.40%的市场份额,这主要得益于电子和医疗设备组装等对精度要求极高的行业。同时,10-20公斤级的协作机器人正以22.95%的复合年增长率快速增长,显示其在码垛、机器维护和汽车子组装等领域的应用日益广泛。中等重量级的协作机器人还提供了更广泛的操作范围,使工人无需移动到新的安全区域即可在生产线旁进行作业。虽然重型(20公斤以上)协作机器人目前仍属于小众市场,但在油漆和化学等对防爆认证要求极高的环境中,它们的价值日益凸显。随着机器人製造商不断改进动态扭矩感测技术,预计从2028年起,中等重量级协作机器人市场的成长速度将超过轻型协作机器人市场。

在5-9公斤级的负载中,供应商正在将视觉和人工智慧技术整合到机器人中,以实现亚秒级的取放循环,从而满足半导体后端加工的需求。这种转变反映了买家对兼具灵活性和强大功能,并能降低设备复杂性的机器人的需求。利用协作机器人市场的製造商可以实现不同负载等级的夹爪和控制器标准化,从而简化备件管理和操作员培训。

儘管硬体在2025年仍占总营收的71.35%,但随着用户将智慧化置于机械性能之上,软体领域正以27.15%的复合年增长率快速成长。视觉引导路径规划、车队编配和预测性维护模组正在将一次性硬体销售转化为持续的授权收入,并将供应商的收入来源转向数位服务。协作机器人现在标配ROS相容的API和云端连接器,从而能够快速整合应用程式。

咨询和生命週期服务的成长反映了中小企业对外部专业知识的依赖。供应商正将安全评估、程式设计和操作员技能提升纳入订阅模式,进一步扩大协作机器人市场。未来,软体定义的有效载荷升级将缩短更换週期,使工厂管理人员能够延长机器人框架的运作,并透过韧体增强提升其效能。

协作机器人市场报告按有效载荷(<5 kg、5-9 kg、10-20 kg、>20 kg)、组件(例如硬体)、应用(物料输送、取放)、终端用户行业(例如电子、汽车)、程式设计方法(例如手动引导)和地区进行细分。市场预测以美元以金额为准。

区域分析

到2025年,亚洲将占全球收入的40.55%,这主要得益于中国「十四五」规划中万亿元人民币的机器人产业发展战略以及日本融合人工智慧、物联网和下一代自动化技术的「社会5.0」计画。中国的电子和电池工厂正在部署协作机器人进行精密黏合和电池堆迭,而日本的医院正在进行老年护理服务机器人的现场试验。韩国的「第四个智慧机器人基本规划」为国内中小企业部署协作机器人解决方案提供资金支持,从而强化了其供应链。

北美位居第二。美国的回流政策和创纪录的劳动力短缺正在推动市场发展。获得晶片补贴的半导体工厂正在部署双臂协作机器人进行晶圆搬运,从而降低运输过程中的污染风险。加拿大汽车零件供应商正在安装中型机器人用于压铸件的精加工,而墨西哥的加工出口企业(maquiladoras)则正在采用协作机器人来平衡不断上涨的工资水平和出口竞争力。跨境标准化使得整合商能够重复利用单元设计,从而加速了协作机器人的普及应用。

在欧洲,德国的工业4.0灯塔计划正大力推动将製造执行系统(MES)数据与协作机器人集群连结。欧洲地平线津贴正用于人机介面研究,而开发人工智慧运动规划Start-Ups的新创公司在丹麦和义大利蓬勃发展。一家法国航太工厂选择协作机器人进行碳纤维修整,正是因为它们轻巧且符合人体工学。不断上涨的能源成本促使工厂寻求更有效率的布局,而协作机器人则比起笼式机器人面积较小。此外,环保法规也重视协作机器人相比液压压平机更低的待机电力消耗,这进一步推动了协作机器人市场在永续性永续发展的地区的扩张。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 在多品种、小批量生产中实现经济高效的搬迁(欧洲)

- 中小企业的即插即用型协作机器人OEM推广(北美)

- 快速的电子商务履约推动了仓库中协作机器人的应用(亚洲)

- 更新至 ISO/TS 15066 标准可缓解责任问题(全球)

- 美国为鼓励自动化企业回流而提供的税务优惠

- 市场限制

- 与现有PLC架构整合方面的瓶颈

- 负载容量和速度之间的权衡限制了重型作业。

- 分散式组件生态系统推高了中小企业的整体拥有成本。

- 人机协作工作单元的承保缺口

- 价值/供应链分析

- 监理与技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 定价分析

第五章 市场规模与成长预测

- 按有效载荷

- 5公斤以下

- 5~9kg

- 10~20kg

- 超过20公斤

- 按组件

- 硬体

- 软体

- 服务

- 咨询与整合

- 维护和培训

- 透过使用

- 物料输送

- 拣选和放置

- 组装

- 码垛和卸垛

- 焊接和焊焊

- 品质检验和测试

- 包装

- 其他用途

- 按最终用户行业划分

- 车

- 电子和半导体

- 一般製造业

- 食品/饮料

- 化学品和製药

- 物流与电子商务

- 医疗保健和生命科学

- 金属加工

- 其他行业

- 透过程式方法(仅定性)

- 指南教学/直接教学法

- 引导式教学

- 离线程式设计与仿真

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 北欧国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 南美洲

- 巴西

- 阿根廷

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 非洲

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Universal Robots AS

- FANUC Corp.

- ABB Ltd.

- KUKA AG

- Yaskawa Electric Corp.

- Techman Robot Inc.

- Doosan Robotics Inc.

- AUBO Robotics

- Kawasaki Heavy Industries Ltd.

- Omron Corporation

- Epson Robots

- Precise Automation Inc.

- Staubli International AG

- Hanwha Robotics

- Denso Wave Inc.

- Comau SpA

- Hyundai Robotics

- Festo SE and Co. KG

第七章 市场机会与未来展望

The Collaborative Robot Market was valued at USD 1.9 billion in 2025 and estimated to grow from USD 2.28 billion in 2026 to reach USD 5.72 billion by 2031, at a CAGR of 20.15% during the forecast period (2026-2031).

Demand accelerates as updated ISO/TS 15066 standards clarify safety requirements, tax incentives lower payback periods, and labor shortages raise the urgency of flexible automation. Manufacturers increasingly deploy cobots to lift productivity rather than replace workers, while maturing software and simplified programming shorten deployment cycles. Growing payload capacities, warehouse automation needs, and widening service-sector use cases strengthen adoption momentum across global value chains.

Global Collaborative Robot Market Trends and Insights

Cost-effective Redeployment in High-mix Manufacturing

European and North American factories now rotate cobots across assembly cells within a single shift, cutting changeover from weeks to hours This agility lets automotive suppliers accept smaller, high-margin orders while retaining automation gains.

OEM Push Toward Plug-and-Play Cobots for SMEs

New controllers, capped wiring, and pre-loaded task libraries allow small manufacturers to install cobots without specialist integrators. Universal Robots' UR-series refresh shows how cycle-time gains and intuitive hand-guiding shrink total cost of ownership, opening the collaborative robot market to thousands of first-time users

Integration Bottlenecks with Brownfield PLC Architectures

Legacy PLCs often lack real-time Ethernet or safe-motion channels, forcing costly controller upgrades when cobots are added to decades-old lines . The expense pushes some automotive plants to defer adoption until full line overhauls.

Other drivers and restraints analyzed in the detailed report include:

- Rapid E-commerce Fulfilment Drives Warehouse Cobots

- ISO/TS 15066 Updates Easing Liability Concerns

- Payload-Speed Trade-offs Limiting Heavy-duty Tasks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sub-5 kg models controlled 52.40% of the collaborative robot market in 2025, largely in electronics and medical device assembly where precision is paramount. The 10-20 kg band, however, is pacing a 22.95% CAGR, signaling rising interest in palletizing, machine tending, and automotive sub-assembly. Mid-range units also integrate longer reaches, enabling line-side work without moving humans to new safety zones. Heavy-duty (>20 kg) cobots remain niche but prove valuable in paint and chemical environments where explosion-proof certification is essential. As robot makers refine dynamic torque sensing, the collaborative robot market size for mid-payloads is projected to outgrow light units after 2028.

Within 5-9 kg, vendors package vision and AI for pick-and-place cycles under one second, catering to semiconductor back-end operations. The shift reflects buyers' search for units that bridge dexterity and strength, reducing fleet complexity. Manufacturers leveraging the collaborative robot market gain the option to standardize grippers and controllers across payload classes, simplifying spare-parts management and operator training.

Hardware generated 71.35% of revenue in 2025, yet software is advancing 27.15% annually as users emphasize intelligence over mechanics. Vision-guided path planning, fleet orchestration, and predictive maintenance modules convert one-time hardware sales into recurring licenses, moving vendor profit pools toward digital services. Cobots now ship with ROS-compatible APIs and cloud connectors, allowing quick app integrations.

Growth in consulting and lifecycle services reflects SME reliance on external expertise. Vendors bundle safety assessment, programming, and operator up-skilling into subscription models, further enlarging the collaborative robot market. Over time, software-defined payload upgrades may lower replacement cycles, letting plant managers keep frames in service longer while lifting performance through firmware enhancements.

Collaborative Robots Market Report is Segmented Into by Payload (Less Than 5Kg, 5-9 Kg, 10-20 Kg, More Than 20 KG), Component (Hardware and More), Application (Material Handling, Pick and Place and More), End-User Industry (Electronics, Automotive, and More), Programming Method (Hand-Guiding and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia generated 40.55% of 2025 revenue, propelled by China's 1-trillion-yuan robotics push under the 14th Five-Year Plan and Japan's Society 5.0 roadmap that blends AI, IoT, and next-generation automation . Chinese electronics and battery plants install cobots for precision gluing and cell stacking, while Japanese hospitals test service robots for elder care. South Korea's Fourth Intelligent Robot Basic Plan funds local SMEs to adopt collaborative solutions, reinforcing domestic supply chains.

North America ranks second. U.S. reshoring incentives combined with record labor scarcity elevate the market. Semiconductor fabs subsidized by the CHIPS Act integrate dual-arm cobots for wafer loading, shrinking transport contamination risk. Canadian auto parts suppliers adopt mid-payload units for die-casting part finishing, while Mexican maquiladoras deploy cobots to balance wage inflation with export competitiveness. Cross-border standardization allows integrators to reuse cell designs, accelerating rollout.

Europe shows robust uptake led by Germany's Industrie 4.0 lighthouse projects linking MES data to cobot fleets. Horizon Europe grants finance human-machine interface research, spurring startups in Denmark and Italy that build AI motion-planning stacks. French aerospace plants choose cobots for carbon-fiber trimming, citing weight reduction and ergonomic gains. Rising energy costs push factories toward leaner layouts where cobots save floor space relative to fenced robots. Environmental regulations also favor cobots' lower idle power draw compared with hydraulic presses, aiding the collaborative robot market size in sustainability-conscious regions.

- Universal Robots AS

- FANUC Corp.

- ABB Ltd.

- KUKA AG

- Yaskawa Electric Corp.

- Techman Robot Inc.

- Doosan Robotics Inc.

- AUBO Robotics

- Kawasaki Heavy Industries Ltd.

- Omron Corporation

- Epson Robots

- Precise Automation Inc.

- Staubli International AG

- Hanwha Robotics

- Denso Wave Inc.

- Comau SpA

- Hyundai Robotics

- Festo SE and Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-effective Re-deployment in High-mix Manufacturing (Europe)

- 4.2.2 OEM Push Toward Plug-and-Play Cobots for SMEs (North America)

- 4.2.3 Rapid E-Commerce Fulfilment Drives Warehouse Cobots (Asia)

- 4.2.4 ISO/TS 15066 Updates Easing Liability Concerns (Global)

- 4.2.5 Tax Incentives for Reshoring Automation (United States)

- 4.3 Market Restraints

- 4.3.1 Integration Bottlenecks with Brownfield PLC Architectures

- 4.3.2 Payload-Speed Trade-offs Limiting Heavy-duty Tasks

- 4.3.3 Fragmented Component Ecosystem Inflates TCO for SMEs

- 4.3.4 Insurance Underwriting Gaps for HumanRobot Workcells

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porters Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Intensity of Competitive Rivalry

- 4.6.5 Threat of Substitute Products

- 4.7 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Payload

- 5.1.1 Less than 5 kg

- 5.1.2 5 - 9 kg

- 5.1.3 10 - 20 kg

- 5.1.4 More than 20 kg

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.2.3.1 Consulting and Integration

- 5.2.3.2 Maintenance and Training

- 5.3 By Application

- 5.3.1 Material Handling

- 5.3.2 Pick and Place

- 5.3.3 Assembly

- 5.3.4 Palletizing and De-palletizing

- 5.3.5 Welding and Soldering

- 5.3.6 Quality Testing and Inspection

- 5.3.7 Packaging

- 5.3.8 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Electronics and Semiconductors

- 5.4.3 General Manufacturing

- 5.4.4 Food and Beverage

- 5.4.5 Chemicals and Pharmaceuticals

- 5.4.6 Logistics and E-commerce

- 5.4.7 Healthcare and Life Sciences

- 5.4.8 Metals and Machining

- 5.4.9 Other Industries

- 5.5 By Programming Method (qualitative only)

- 5.5.1 Hand-Guiding / Direct Teaching

- 5.5.2 Lead-through Teaching

- 5.5.3 Offline Programming and Simulation

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Nordics

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Universal Robots AS

- 6.4.2 FANUC Corp.

- 6.4.3 ABB Ltd.

- 6.4.4 KUKA AG

- 6.4.5 Yaskawa Electric Corp.

- 6.4.6 Techman Robot Inc.

- 6.4.7 Doosan Robotics Inc.

- 6.4.8 AUBO Robotics

- 6.4.9 Kawasaki Heavy Industries Ltd.

- 6.4.10 Omron Corporation

- 6.4.11 Epson Robots

- 6.4.12 Precise Automation Inc.

- 6.4.13 Staubli International AG

- 6.4.14 Hanwha Robotics

- 6.4.15 Denso Wave Inc.

- 6.4.16 Comau SpA

- 6.4.17 Hyundai Robotics

- 6.4.18 Festo SE and Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

协作机器人市场预测至2034年:按组件、安装类型、技术、应用、最终用户和地区分類的全球分析

协作机器人市场预测至2034年:按组件、安装类型、技术、应用、最终用户和地区分類的全球分析 协作机器人市场:2026-2032年全球市场预测(按类型、有效载荷能力、安装方式、应用、终端用户产业和销售管道)

协作机器人市场:2026-2032年全球市场预测(按类型、有效载荷能力、安装方式、应用、终端用户产业和销售管道) 2026年全球工业协作机器人市场报告2026年全球行动协作机器人市场报告2026年全球协作机器人关节模组市场报告机器人关节模组市场:按类型、自由度、控制方式、材质、负载能力、机器人类型和最终用户划分-2026-2032年全球预测轻型协作机械臂市场:按负载能力、机器人类型、终端用户产业和应用划分-全球预测,2026-2032年

2026年全球工业协作机器人市场报告2026年全球行动协作机器人市场报告2026年全球协作机器人关节模组市场报告机器人关节模组市场:按类型、自由度、控制方式、材质、负载能力、机器人类型和最终用户划分-2026-2032年全球预测轻型协作机械臂市场:按负载能力、机器人类型、终端用户产业和应用划分-全球预测,2026-2032年 协作机器人市场分析及预测(至2035年):依类型、产品、技术、组件、应用、最终用户、功能、安装类型及部署方式划分协同製造解决方案市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者、部署类型及功能划分行动协作机器人市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分

协作机器人市场分析及预测(至2035年):依类型、产品、技术、组件、应用、最终用户、功能、安装类型及部署方式划分协同製造解决方案市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、流程、最终使用者、部署类型及功能划分行动协作机器人市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分