|

市场调查报告书

商品编码

1940634

涂层钢:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Coated Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

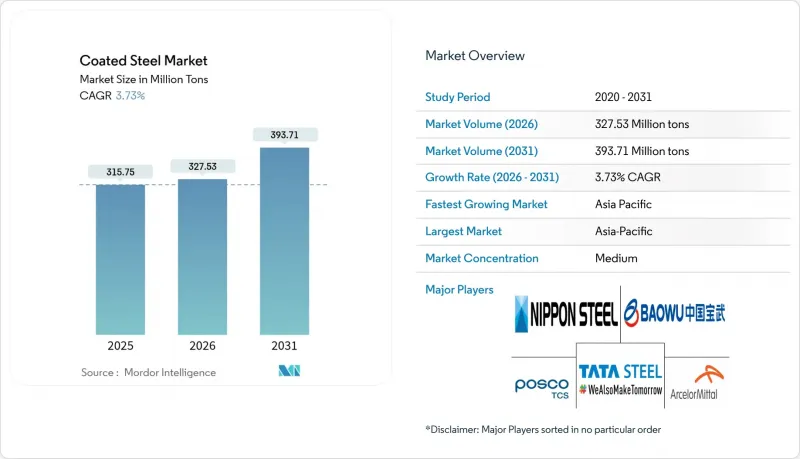

2025年涂层钢市场价值为3.1575亿吨,预计到2031年将达到3.9371亿吨,而2026年为3.2753亿吨。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.73%。

这一增长反映了汽车轻量化项目的强劲需求、节能建筑围护结构的推广以及主要生产基地产能的持续扩张。锌铝镁合金涂层的加速商业化(与传统镀锌产品相比,其使用寿命更长)进一步推动了这种成长动能。生产商也积极推动垂直整合和可再生能源业务,以避免原材料价格波动风险并遵守日益严格的碳排放法规。贸易救济措施,特别是美国对耐腐蚀进口产品征收的反倾销税,正在重塑区域供应链格局,同时鼓励国内投资。同时,欧盟的碳边境调节机制(CBAM)正在加快产品排放的揭露,使得经认证的低碳涂层钢能够获得溢价。

全球涂层钢市场趋势及展望

轻型电动车对高强度钢基涂层钢的需求激增

电动车製造商目前正指定使用高抗拉强度钢结合涂层来保护电池机壳和碰撞结构,同时还要承受复杂的成型过程。安赛乐米塔尔投资12亿美元的阿拉巴马州电钢计划正是顺应这股趋势的策略性资本配置。锌铝镁合金的化学成分赋予了涂层高强度钢(AHSS)雷射焊接电池组所需的边缘耐腐蚀性,使其成为传统汽车用钢与下一代汽车技术之间的桥樑。

预涂漆卷材在节能建筑外墙的应用

冷冻负载法规正在推动采用太阳反射率不低于0.7、热辐射率不低于0.8的涂层盘管屋顶。亚洲开发银行的实地研究表明,在热带地区,冷屋顶可减少15%至20%的冷冻能耗。基于聚偏氟乙烯(PVDF)的涂层,例如Kynar 500,可提供30年质保,从而提高生命週期经济效益,并帮助建筑商达到LEED和欧盟生态设计标准。

锌铝价格波动

2024年底,现货锌价收于每吨人民币25,900元(年增19.8%),但由于矿场作业中断与需求波动,2025年第一季跌至每吨人民币23,370元。铝价也出现类似波动,导致锌铝镁合金和铝电镀生产线的采购更加复杂。成本转嫁和合约滞后交织的领域,利润压力最为严峻。

细分市场分析

截至2025年,热镀锌钢板将占镀锌钢板市场份额的63.10%,相当于约1.99亿吨。到2031年,热浸镀锌钢板市场将以3.89%的复合年增长率成长,这将成为传统建筑、家电和仓储应用领域镀锌钢板市场规模的基础。电镀锌和镀铝产品在高精度、高温应用等细分市场成长更为迅速,但从资本投资效率的角度来看,产能扩张的重点仍是热镀锌线。

涂层钢产业正转向「其他」类别中的锌铝镁合金,其中AM/NS印度公司的Magnelis产品提供的耐腐蚀寿命是热镀锌的三到五倍。製造商正在将雷射焊接涂层应用于汽车车体,这表明热镀锌的产量不会彻底下降,而是逐渐被新一代涂层所取代。

本《涂层钢市场报告》依产品类型(热镀锌、镀锌退火、电镀锌、镀铝及其他)、应用领域(建筑结构构件、汽车零件、家用电器、管道及其他)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲)进行细分。市场预测以吨为单位。

区域分析

预计到2025年,亚太地区将占据全球镀锌钢市场61.10%的份额(超过1.93亿吨),并预计到2031年将以4.47%的复合年增长率增长。中国凭藉其综合性钢铁厂升级下游生产线,主导;而印度、韩国和日本则在出口特种产品。东南亚国协正在扩大其产能,以满足太阳能、物流和住宅计划的需求,这进一步增强了区域镀锌钢市场的韧性。

北美位居第二。美国对来自10个国家的耐腐蚀钢材征收反倾销税,缩小了进口选择范围,促使相关企业进行投资,例如纽柯公司在南卡罗来纳州投资4.25亿美元建设镀锌生产线,以及现代钢铁公司在路易斯安那州投资58亿美元建设综合工厂。墨西哥在2025年至2026年间新增800万吨产能,正在加强近岸外包,并平衡该地区的涂层钢市场。

欧洲正面临能源成本飙升和碳边境调节机制(CBAM)带来的挑战。生产商正在提交环境产品声明(EPD),以确保在建筑业获得溢价并降低碳课税。德国、法国、义大利和英国仍然是主要的消费国,而北欧钢铁厂则专注于可再生能源和海洋领域。有关循环经济和废钢利用的监管确定性将影响欧洲涂层钢市场的竞争力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 轻型电动车对基于高抗拉强度钢(AHSS)的涂层钢的需求激增

- 在节能建筑围护结构中使用预涂漆卷材。

- 亚洲锌铝镁合金涂层生产线的快速引进

- 税收优惠的家电置换计画(欧盟和美国)

- 经认证的低碳(EPD/CBAM相容)涂层钢

- 市场限制

- 锌铝价格波动

- 铝复合材料建筑幕墙的替代方案

- 针对涂层钢的反倾销/反补贴税贸易措施

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 热浸电镀

- 镀锌

- 电镀

- 铝化

- 其他产品类型

- 透过使用

- 建筑构件

- 汽车零件

- 家用电器

- 管道和管材

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AM/NS INDIA

- ArcelorMittal

- China Baowu Steel Group Corp., Ltd

- CUMIC STEEL LIMITED

- JFE Steel Corporation

- Jindal Steel

- JSW

- KOBE STEEL, LTD.

- MMK(PJSC)

- Nippon Steel Coated Sheet Corporation

- NLMK

- NS BlueScope

- Nucor Corporation

- POSCO Coated Steel(Thailand)Co.,Ltd.

- Salzgitter Flachstahl GmbH

- SSAB AB

- Tata Steel

- thyssenkrupp Steel

- United States Steel Corporation

- voestalpine Stahl GmbH

第七章 市场机会与未来展望

The Coated Steel Market was valued at 315.75 Million tons in 2025 and estimated to grow from 327.53 Million tons in 2026 to reach 393.71 Million tons by 2031, at a CAGR of 3.73% during the forecast period (2026-2031).

This growth reflects resilient demand from automotive lightweighting programs, expanding energy-efficient building envelopes, and sustained capacity additions in key production hubs. Momentum is reinforced by quicker commercialization of Zn-Al-Mg alloy coatings that extend service life versus conventional galvanized products. Producers are also pursuing vertical integration and renewable-powered operations to hedge raw-material volatility and meet tightening carbon rules. Trade remedies-most notably the United States' anti-dumping duties on corrosion-resistant imports-reshape regional supply flows while favoring domestic investments. At the same time, EU carbon-border pricing accelerates disclosure of embedded emissions, allowing certified low-carbon coated steel to command premiums.

Global Coated Steel Market Trends and Insights

Surging Demand for AHSS-Based Coated Steels in EV Lightweighting

Electric-vehicle producers now specify advanced high-strength steel grades paired with coatings that survive complex forming while protecting battery enclosures and crash structures. ArcelorMittal's USD 1.2 billion Alabama electrical-steel project illustrates strategic capital alignment with this trend. Zn-Al-Mg chemistries offer edge-corrosion resistance crucial for laser-welded battery packs, positioning coated AHSS as a bridge between legacy auto steel and next-generation mobility.

Energy-Efficient Building Envelope Adoption of Pre-Painted Coil

Cooling-load regulations spur use of pre-painted coil achieving solar reflectance above 0.7 and thermal emittance beyond 0.8. Asian Development Bank field work shows cool roofs can cut cooling energy 15-20% in tropical settings. PVDF-based coatings such as Kynar 500 provide 30-year warranties that improve lifecycle economics while helping builders meet LEED and EU Ecodesign thresholds.

Zinc and Aluminum Price Volatility

Spot zinc closed 2024 at RMB 25,900 per ton, up 19.8% year-on-year, before easing to RMB 23,370 in Q1 2025 amid mine disruptions and demand swings. Aluminum shows similar gyrations, complicating procurement for Zn-Al-Mg and aluminized lines. Margin compression is most severe where passing costs downstream meets contract lags.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Rollout of Zn-Al-Mg Alloy Coating Lines in Asia

- Tax-Driven Appliance Replacement Programs (EU and US)

- Aluminum-Composite Facade Substitution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hot-dipped material held 63.10% of coated steel market share in 2025, equating to roughly 199 million tons. Its 3.89% CAGR through 2031 anchors the coated steel market size for traditional construction, appliance, and storage uses. Electro-galvanized and aluminized alternatives grow faster in high-precision or high-temperature niches, but capacity build-outs center on hot-dip lines due to capital efficiency.

The coated steel industry is pivoting toward Zn-Al-Mg alloys classified in the "Others" bucket, where AM/NS India's Magnelis offers 3-5 times galvanized corrosion life. Producers integrate laser-welding-friendly chemistries for auto body-in-white, suggesting hot-dipped volume will gradually cede mix share to next-generation coatings rather than suffer absolute decline.

The Coated Steel Market Report is Segmented by Product Type (Hot-Dipped, Galvannealed, Electro-Galvanized, Aluminized, and Others), Application (Construction and Building Components, Automotive Components, Appliances, Pipe and Tubular, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific commanded 61.10% of coated steel market share in 2025-just over 193 million tons-and is projected at a 4.47% CAGR to 2031. China leads with integrated mills upgrading downstream lines, while India, South Korea, and Japan export specialty products. ASEAN nations expand capacity for solar, logistics, and housing projects, enhancing regional coated steel market resilience.

North America ranks second. U.S. anti-dumping tariffs covering corrosion-resistant sheet from 10 countries have narrowed import options, encouraging investments such as Nucor's USD 425 million South Carolina galvanizing line and Hyundai Steel's USD 5.8 billion Louisiana integrated plant. Mexico's 8 million-ton capacity additions over 2025-2026 reinforce near-shoring, keeping the coated steel market in the hemisphere balanced.

Europe confronts energy-cost spikes and CBAM compliance. Producers showcase Environmental Product Declarations to secure architectural premiums and mitigate carbon levies. Germany, France, Italy, and the United Kingdom remain anchor consumers, while Nordic mills focus on renewables and marine segments. Regulatory certainty on circularity and scrap use will shape Europe's coated steel market competitiveness.

- AM/NS INDIA

- ArcelorMittal

- China Baowu Steel Group Corp., Ltd

- CUMIC STEEL LIMITED

- JFE Steel Corporation

- Jindal Steel

- JSW

- KOBE STEEL, LTD.

- MMK (PJSC)

- Nippon Steel Coated Sheet Corporation

- NLMK

- NS BlueScope

- Nucor Corporation

- POSCO Coated Steel(Thailand) Co.,Ltd.

- Salzgitter Flachstahl GmbH

- SSAB AB

- Tata Steel

- thyssenkrupp Steel

- United States Steel Corporation

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for AHSS-Based Coated Steels in EV Lightweighting

- 4.2.2 Energy-Efficient Building Envelope Adoption of Pre-Painted Coil

- 4.2.3 Rapid Rollout of Zn-Al-Mg Alloy Coating Lines In Asia

- 4.2.4 Tax-Driven Appliance Replacement Programs (EU And US)

- 4.2.5 Certified Low-Carbon (EPD/CBAM-Ready) Coated Steels

- 4.3 Market Restraints

- 4.3.1 Zinc And Aluminium Price Volatility

- 4.3.2 Aluminium-Composite Facade Substitution

- 4.3.3 AD/CVD Trade Actions on Coated Sheet

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Hot-dipped

- 5.1.2 Galvannealed

- 5.1.3 Electro-galvanized

- 5.1.4 Aluminized

- 5.1.5 Others Product Types

- 5.2 By Application

- 5.2.1 Construction and Building Components

- 5.2.2 Automotive Components

- 5.2.3 Appliances

- 5.2.4 Pipe and Tubular

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AM/NS INDIA

- 6.4.2 ArcelorMittal

- 6.4.3 China Baowu Steel Group Corp., Ltd

- 6.4.4 CUMIC STEEL LIMITED

- 6.4.5 JFE Steel Corporation

- 6.4.6 Jindal Steel

- 6.4.7 JSW

- 6.4.8 KOBE STEEL, LTD.

- 6.4.9 MMK (PJSC)

- 6.4.10 Nippon Steel Coated Sheet Corporation

- 6.4.11 NLMK

- 6.4.12 NS BlueScope

- 6.4.13 Nucor Corporation

- 6.4.14 POSCO Coated Steel(Thailand) Co.,Ltd.

- 6.4.15 Salzgitter Flachstahl GmbH

- 6.4.16 SSAB AB

- 6.4.17 Tata Steel

- 6.4.18 thyssenkrupp Steel

- 6.4.19 United States Steel Corporation

- 6.4.20 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

涂层钢市场:2026-2032年全球市场预测(按涂层类型、涂层技术、基材等级、销售管道、应用和最终用途行业划分)耐候钢市场:依产品类型、技术、应用及通路划分-2026-2032年全球市场预测

涂层钢市场:2026-2032年全球市场预测(按涂层类型、涂层技术、基材等级、销售管道、应用和最终用途行业划分)耐候钢市场:依产品类型、技术、应用及通路划分-2026-2032年全球市场预测 全球涂层钢板市场规模、份额、趋势和成长分析报告(2026-2034)

全球涂层钢板市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球耐候钢市场报告铬碳化物堆焊板市场按产品类型、涂层厚度、终端用户产业、应用和销售管道,全球预测(2026-2032年)

2026年全球耐候钢市场报告铬碳化物堆焊板市场按产品类型、涂层厚度、终端用户产业、应用和销售管道,全球预测(2026-2032年) 耐候钢市场规模、份额及成长分析(按类型、形式、供应、最终用途产业及地区划分)-2026-2033年产业预测

耐候钢市场规模、份额及成长分析(按类型、形式、供应、最终用途产业及地区划分)-2026-2033年产业预测 2025-2029年全球涂层钢市场

2025-2029年全球涂层钢市场 全球耐候钢市场按类型、最终用途产业、材料类型和地区划分

全球耐候钢市场按类型、最终用途产业、材料类型和地区划分 涂层钢市场规模、份额、趋势分析报告:按产品、最终用途、地区、细分市场预测,2025-2030 年美国涂层钢市场规模、份额、趋势分析报告:按产品、应用和细分市场预测,2025-2030 年

涂层钢市场规模、份额、趋势分析报告:按产品、最终用途、地区、细分市场预测,2025-2030 年美国涂层钢市场规模、份额、趋势分析报告:按产品、应用和细分市场预测,2025-2030 年