|

市场调查报告书

商品编码

1940663

系统整合商:市场占有率分析、产业趋势与统计资料、成长预测(2026-2031 年)System Integrators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

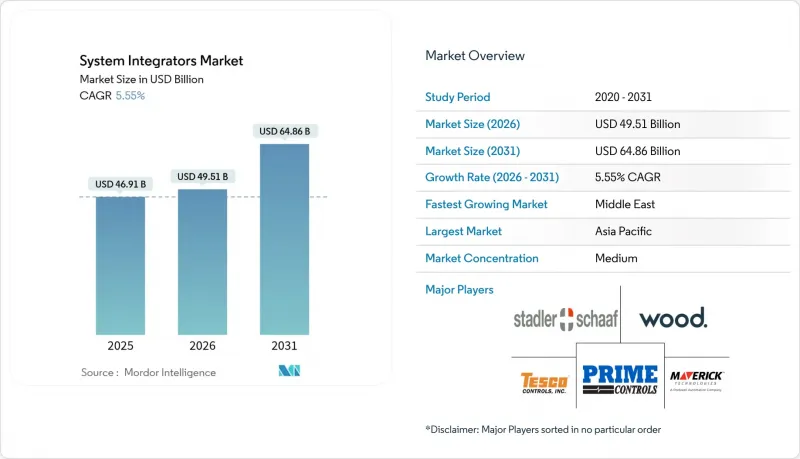

2025年系统整合商市场价值为469.1亿美元,预计到2031年将达到648.6亿美元,高于2026年的495.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.55%。

製造商从独立昇级转向承包OT-IT融合计划,推动了这一增长,此类项目缩短了投资回收期并最大限度地减少了生产停机时间。现有工厂(棕地)正在获得越来越多的新订单,而由私有5G网路支援的多厂商边缘部署正在创造对先进编配技术的新需求。同时,欧洲和亚洲的公共产业正在对其可再生能源资产数位化,以实现雄心勃勃的清洁能源目标。这种转变有利于精通SCADA(监控与资料采集)系统升级和分散式能源(DER)管理的整合商。中东地区针对关键基础设施的严格网路安全法规正在扩大利润丰厚的SCADA维修计划的潜在市场。工厂人才短缺正促使企业将内部开发和采购决策转向外包,这使得中型企业能够从大型自动化供应商手中夺取市场份额。

全球系统整合商市场趋势与洞察

现有製造工厂对承包OT-IT整合计划的需求

随着製造商将投资回报週期缩短至18个月以内,承包OT-IT整合方案正在取代渐进式升级。将使用了数十年的PLC映射到现代云端架构的挑战,使得能够从单一层面管理共存管理、网路安全和分析的整合商的需求持续成长。流程工业感受到的压力最大,因为一小时的非计划性停机可能会造成超过5万美元的生产损失。

加速欧洲和亚洲可再生能源资产的数位化

到2030年,欧洲公用事业公司需要整合约900吉瓦的太阳能发电容量,要实现这一目标,需要预测、储能和併网应用之间密切合作。横河电机的BaxEnergy平台已在40个国家监测120吉瓦的可再生能源,展现了下一代计划的规模和复杂性。

计划范围扩大的风险增加会推高最终用户的总拥有成本。

超过40%的整合专案超出了最初的预算,原因是工程师在计划进行过程中遇到了未记录的介面和过时的韧体。美国政府审核局(GAO)的一项研究发现,第一类技术计划仍然占联邦预算超支的81%,这凸显了即使在严格的管治下,项目范围仍然持续偏离预算。

细分市场分析

截至2025年,软体和数位整合将占系统整合商市场的47.35%,这主要得益于分析、MES和云端边缘整合套件的优势。随着企业在机器层面采用容器化工作负载,工业物联网(IIoT)和边缘运算整合到2031年将以8.75%的复合年增长率成长。虽然棕地硬体维修仍然很重要,但随着製造商寻求数据而非纯粹的处理能力来获利,其份额正在逐渐下降。由于人才短缺迫使企业提升内部员工的技能,咨询和培训需求正在復苏。同时,售后服务支援提供了持续的收入来源,缓解了计划週期性波动的影响。 Litmus Edge与Azure IoT的合作标誌着向OPC UA和MQTT等标准化连接器的转变,这些连接器能够加快部署速度。

第二个结构性变化是专有整合平台的兴起,这些平台整合了中间件、预先建置的API和数数位双胞胎库。这些服务使整合商能够将其智慧财产权货币化,而不仅仅是按小时收取工程费,从而提高了转换成本。随着越来越多的製造商倾向于基于结果的基本契约,到本十年末,软体密集型工作范围将占系统整合商市场份额的55%以上。

到2025年,整合製程控制解决方案(PLC、DCS、SCADA)将占据系统整合商市场份额的34.02%,这显示底层控制层仍是数位转型蓝图的核心。然而,随着勒索软体从IT领域转向OT领域,工业网路安全解决方案将以10.05%的复合年增长率成长,超过所有其他垂直领域。随着经营团队需要整合生产和营运数据以进行利润中心核算,製造执行系统(MES)将继续稳定成长。在人事费用超过资本折旧免税额的地区,机器人和机器视觉计划正在蓬勃发展。

网路安全发展日趋加速,罗克韦尔收购Verve Industrial Protection便是明证。此次收购将资产清单、风险评分和入侵回应整合到一个厂商中立的平台中。西门子也顺应了这一趋势,推出了SIBERprotect解决方案,可在毫秒内实现自动回应,兼顾运作和安全性。随着监管力道的加大,将零信任架构融入製程控制转型中的整合商将获得更高的溢价。

区域分析

亚太地区在系统整合商市场中占据领先地位,预计到2025年将达到31.20%的市场份额,这主要得益于中国对价格高度敏感的自动化市场环境以及印度不断增长的乙醇热电汽电共生规模。像Ditap-V Automation这样的本土竞争对手凭藉着品质与价格的平衡优势赢得竞标,给跨国巨头带来了更大的压力。政府主导的智慧製造计画正在推动市场需求,而地缘政治摩擦和运输瓶颈则威胁交付时间。

中东是成长最快的地区,预计到2031年将维持8.46%的复合年增长率。 「2030愿景」大型企划和不断扩展的营运技术(OT)网路安全法规正在推高计划平均价值。艾默生位于萨勒曼国王能源园区的14万平方英尺製造地,展现了全球供应商如何实现价值链本地化,以满足当地价值标准。同时,一旦运作,印度-中东-欧洲经济走廊可望降低30%的运输成本,这将进一步刺激对熟悉跨境标准的整合商的需求。

北美和欧洲仍然是盈利但趋于成熟的市场。在美国,私有5G和边缘人工智慧试点计画发展迅猛,但长期存在的劳动力短缺推高了人事费用。在欧洲,可再生能源的大力发展迫使电力公司将电网级电池储能、太阳能逆变器和需量反应软体整合到系统中,而这种整合挑战也催生了大量的计划储备。在这两个地区,严格的安全标准导致核准週期较长,凸显了专业整合商的价值。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 承包OT-IT融合计划的需求

- 加速可再生能源资产的数位化

- 5G边缘运算用例

- 监理机关推动SCADA网路安全维修

- 模组化自动化技术的广泛应用

- 工厂自动化人员短缺

- 市场限制

- 计划范围扩张风险较高

- 采购延误

- 分散的供应商生态系统

- 重大法律责任风险

- 价值/供应链分析

- 监理与技术展望

- 波特五力模型

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按服务类型

- 硬体集成

- 软体和数位集成

- 咨询和培训

- 售后服务及维护

- 透过技术

- 整合製程控制(PLC、DCS、SCADA)

- 製造执行系统(MES)

- 机器人与机器视觉

- 工业物联网与边缘平台

- 网路安全解决方案

- 按最终用户行业划分

- 石油和天然气

- 汽车和电动车 (EV) 製造

- 航太/国防

- 医疗保健和生命科学

- 能源与电力

- 化工/石油化工

- 食品/饮料

- 金属和采矿

- 其他(水/污水、纸浆和造纸)

- 按公司规模

- 小型企业

- 大公司

- 按地区

- 北美洲

- 我们

- 加拿大

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 其他拉丁美洲地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 中东和非洲

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 亚太其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ABB Ltd.

- Siemens AG

- Rockwell Automation, Inc.

- Schneider Electric SE

- Honeywell International Inc.

- Emerson Electric Co.

- Yokogawa Electric Corporation

- John Wood Group PLC

- TESCO CONTROLS, Inc.

- STADLER+SCHAAF Mess-und Regeltechnik GmbH

- Prime Controls, LP

- MAVERICK Technologies, LLC

- Adsyst Automation Ltd.

- George T. Hall Company

- Avanceon Ltd.

- Wunderlich-Malec Engineering, Inc.

- Burrow Global, LLC

- ATS Corporation

- HCLTech(Industrial and Digital SI Practice)

- Accenture plc(Industry X)

第七章 市场机会与未来展望

The system integrators market was valued at USD 46.91 billion in 2025 and estimated to grow from USD 49.51 billion in 2026 to reach USD 64.86 billion by 2031, at a CAGR of 5.55% during the forecast period (2026-2031).

Expansion is underpinned by manufacturers shifting from isolated upgrades to turnkey OT-IT convergence projects that shorten payback periods while minimizing production downtime. Brownfield plants account for a rising share of new awards, and multi-vendor edge deployments anchored in private-5G are unlocking fresh demand for advanced orchestration skills. At the same time, utilities in Europe and Asia are digitizing renewable assets to comply with aggressive clean-energy targets, a change that favors integrators fluent in SCADA upgrades and DER management. Regulatory cybersecurity mandates for critical infrastructure, most visibly in the Middle East, are widening the addressable pool of high-margin SCADA retrofit projects. Talent shortages on the plant floor further tilt the build-versus-buy calculus toward outsourcing, enabling mid-tier firms to capture share from large automation vendors.

Global System Integrators Market Trends and Insights

Demand for Turn-Key OT-IT Convergence Projects in Brownfield Manufacturing Plants

Turn-key OT-IT programs are replacing incremental upgrades because manufacturers now target ROI cycles below 18 months. The challenge of mapping decades-old PLCs to modern cloud architectures creates enduring demand for integrators able to manage coexistence, cybersecurity and analytics in one scope. Process industries feel this pressure most acutely, since one hour of unplanned downtime can exceed USD 50,000 in lost output.

Acceleration of Renewable-Energy Asset Digitalization Across Europe and Asia

European utilities must orchestrate nearly 900 GW of solar capacity by 2030, a milestone that compels tighter coupling of forecasting, storage and grid-balancing applications. The BaxEnergy platform, now owned by Yokogawa, already monitors 120 GW of renewables across 40 countries, illustrating the scale and complexity of next-gen projects.

High Project Scope-Creep Risk Elevating Total Cost of Ownership for End-Users

More than 40% of integration programs overshoot original budgets as engineers confront undocumented interfaces and obsolete firmware mid-project. The U.S. Government Accountability Office found that Category 1 technology projects still account for 81% of federal overruns, underscoring how scope drift persists even under strict governance.

Other drivers and restraints analyzed in the detailed report include:

- 5G-Enabled Edge Computing Use-Cases Requiring Complex Multi-Vendor Integration in North America

- Regulatory Push for Cyber-Secure SCADA Retrofits in Critical Infrastructure (Middle East)

- Procurement Delays Caused by Semiconductor Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software and Digital Integration controlled 47.35% of system integrators market size in 2025 on the strength of analytics, MES and cloud-edge orchestration suites. IIoT and Edge-Focused Integration posts a 8.75% CAGR to 2031 as firms deploy containerized workloads at the machine level. Hardware retrofits remain vital for brownfield sites, but their share is gradually receding as manufacturers monetize data rather than pure throughput. Consulting and Training demand is reviving because talent gaps force companies to upskill in-house staff, while After-Sales Support secures recurring revenue that cushions cyclical project flow. The Litmus Edge-Azure IoT tie-up typifies the pivot toward standardized connectors like OPC UA and MQTT that cut roll-out times.

A second structural change is the rise of proprietary integration platforms that bundle middleware, pre-built APIs and digital-twin libraries. These services allow integrators to monetize intellectual property beyond hourly engineering fees, increasing switching costs. As more manufacturers favor outcome-based contracts, software-heavy scopes will likely surpass 55% share of the system integrators market by decade-end.

Integrated Process Control solutions-PLC, DCS and SCADA-accounted for 34.02% of system integrators market share in 2025, evidence that foundational control layers still anchor digital transformation roadmaps. Even so, Industrial Cyber-Security Solutions outpace every other cluster at a 10.05% CAGR as ransomware moves from IT to OT domains. Manufacturing Execution Systems keep growing steadily because executives need unified production and business data to run profit-center accounting. Robotics and Machine Vision projects gain traction where labor costs outstrip capex depreciation curves.

Cybersecurity's acceleration is visible in Rockwell's acquisition of Verve Industrial Protection, which unified asset inventory, risk scoring and breach response in a vendor-neutral stack. Siemens echoed this trend with its SIBERprotect solution that triggers automated responses within milliseconds, balancing uptime and safety. As regulations tighten, integrators that embed zero-trust architectures into process-control migrations are set to capture premium fees.

System Integrators Market Report is Segmented by Service Type (Hardware Integration, Software and Digital Integration, and More), Technology (Integrated Process Control, Manufacturing Execution Systems, and More), End-User Industry (Oil and Gas, Automotive and EV Manufacturing, and More), Enterprise Scale (SMEs, Large Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the system integrators market with 31.20% revenue in 2025, spurred by China's price-intensive automation landscape and India's expanding ethanol and co-gen base. Local competitors such as Ditap-V Automatio win bids by balancing quality and aggressive pricing, raising pressure on multinational incumbents. Government-sponsored smart-manufacturing schemes amplify demand, yet geopolitical frictions and shipping bottlenecks threaten delivery schedules.

The Middle East is the fastest-growing territory, forecast at 8.46% CAGR through 2031. Vision 2030 megaprojects and an expanding regulatory net for OT cybersecurity elevate average project values. Emerson's 140,000 ft2 manufacturing hub at King Salman Energy Park shows how global vendors localize supply chains to satisfy in-country value quotas. Meanwhile, the India-Middle East-Europe Economic Corridor could slash freight costs by 30% once operational, creating further pull for integrators versed in cross-border standards.

North America and Europe remain lucrative but mature. The U.S. sees outsized growth from private-5G and edge-AI pilots, yet chronic labor shortages inflate wage bills. Europe's renewable push forces utilities to blend grid-scale batteries, PV inverters and demand-response software in coherent stacks, an integration puzzle that sustains robust project pipelines. Both regions confront stringent safety codes that lengthen approval cycles, underscoring the value of domain-rich integrators.

- ABB Ltd.

- Siemens AG

- Rockwell Automation, Inc.

- Schneider Electric SE

- Honeywell International Inc.

- Emerson Electric Co.

- Yokogawa Electric Corporation

- John Wood Group PLC

- TESCO CONTROLS, Inc.

- STADLER + SCHAAF Mess- und Regeltechnik GmbH

- Prime Controls, LP

- MAVERICK Technologies, LLC

- Adsyst Automation Ltd.

- George T. Hall Company

- Avanceon Ltd.

- Wunderlich-Malec Engineering, Inc.

- Burrow Global, LLC

- ATS Corporation

- HCLTech (Industrial and Digital SI Practice)

- Accenture plc (Industry X)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Turn-Key OT-IT Convergence Projects

- 4.2.2 Acceleration of Renewable-Energy Asset Digitalization

- 4.2.3 5G-Enabled Edge Computing Use-Cases

- 4.2.4 Regulatory Push for Cyber-Secure SCADA Retrofits

- 4.2.5 Rising Adoption of Modular Automation

- 4.2.6 Shortage of Plant-Floor Automation Talent

- 4.3 Market Restraints

- 4.3.1 High Project Scope-Creep Risk

- 4.3.2 Procurement Delays

- 4.3.3 Fragmented Vendor Ecosystem

- 4.3.4 Critical Liability Exposure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hardware Integration

- 5.1.2 Software and Digital Integration

- 5.1.3 Consulting and Training

- 5.1.4 After-Sales Support and Maintenance

- 5.2 By Technology

- 5.2.1 Integrated Process Control (PLC, DCS, SCADA)

- 5.2.2 Manufacturing Execution Systems (MES)

- 5.2.3 Robotics and Machine Vision

- 5.2.4 IIoT and Edge Platforms

- 5.2.5 Cyber-Security Solutions

- 5.3 By End-User Industry

- 5.3.1 Oil and Gas

- 5.3.2 Automotive and EV Manufacturing

- 5.3.3 Aerospace and Defense

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Energy and Power

- 5.3.6 Chemicals and Petrochemicals

- 5.3.7 Food and Beverage

- 5.3.8 Metals and Mining

- 5.3.9 Others (Water / Waste-Water, Pulp and Paper)

- 5.4 By Enterprise Scale

- 5.4.1 SMEs

- 5.4.2 Large Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Latin America

- 5.5.2.1 Mexico

- 5.5.2.2 Brazil

- 5.5.2.3 Argentina

- 5.5.2.4 Rest of Latin America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Middle East and Africa

- 5.5.5 Asia-Pacific

- 5.5.5.1 China

- 5.5.5.2 Japan

- 5.5.5.3 South Korea

- 5.5.5.4 India

- 5.5.5.5 Australia

- 5.5.5.6 Rest of Asia Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global?level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Siemens AG

- 6.4.3 Rockwell Automation, Inc.

- 6.4.4 Schneider Electric SE

- 6.4.5 Honeywell International Inc.

- 6.4.6 Emerson Electric Co.

- 6.4.7 Yokogawa Electric Corporation

- 6.4.8 John Wood Group PLC

- 6.4.9 TESCO CONTROLS, Inc.

- 6.4.10 STADLER + SCHAAF Mess- und Regeltechnik GmbH

- 6.4.11 Prime Controls, LP

- 6.4.12 MAVERICK Technologies, LLC

- 6.4.13 Adsyst Automation Ltd.

- 6.4.14 George T. Hall Company

- 6.4.15 Avanceon Ltd.

- 6.4.16 Wunderlich-Malec Engineering, Inc.

- 6.4.17 Burrow Global, LLC

- 6.4.18 ATS Corporation

- 6.4.19 HCLTech (Industrial and Digital SI Practice)

- 6.4.20 Accenture plc (Industry X)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

工业自动化系统整合商市场规模、份额和成长分析(按系统整合商类型、服务、专业领域、公司规模、产业和地区划分)-2026年至2033年产业预测

工业自动化系统整合商市场规模、份额和成长分析(按系统整合商类型、服务、专业领域、公司规模、产业和地区划分)-2026年至2033年产业预测 系统整合商市场规模、份额和成长分析(按产品、技术、最终用户产业和地区划分)-2026-2033年产业预测

系统整合商市场规模、份额和成长分析(按产品、技术、最终用户产业和地区划分)-2026-2033年产业预测 2025年全球SAP S4系统整合商服务市场报告

2025年全球SAP S4系统整合商服务市场报告 系统整合商服务市场(按部署模式、服务类型和最终用户产业)- 全球预测,2025 年至 2032 年2025年全球工业自动化系统整合商市场报告

系统整合商服务市场(按部署模式、服务类型和最终用户产业)- 全球预测,2025 年至 2032 年2025年全球工业自动化系统整合商市场报告 2032 年工业自动化系统整合商市场预测:按服务类型、组件、技术、应用、最终用户和地区进行的全球分析

2032 年工业自动化系统整合商市场预测:按服务类型、组件、技术、应用、最终用户和地区进行的全球分析 全球工业自动化系统整合商市场规模(按服务、产业、地区和预测):

全球工业自动化系统整合商市场规模(按服务、产业、地区和预测): 系统整合商市场规模、份额、趋势分析报告:按类型、公司规模、产业、地区和细分市场预测,2024-2030 年

系统整合商市场规模、份额、趋势分析报告:按类型、公司规模、产业、地区和细分市场预测,2024-2030 年 SI/VAR 和合作伙伴计划物联网生态系统:市场资料概述(2024年第3 季)SI/VAR及合作伙伴计划的IoT生态系统

SI/VAR 和合作伙伴计划物联网生态系统:市场资料概述(2024年第3 季)SI/VAR及合作伙伴计划的IoT生态系统