|

市场调查报告书

商品编码

1940669

轮胎翻新:市占率分析、产业趋势与统计、成长预测(2026-2031)Tire Retreading - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

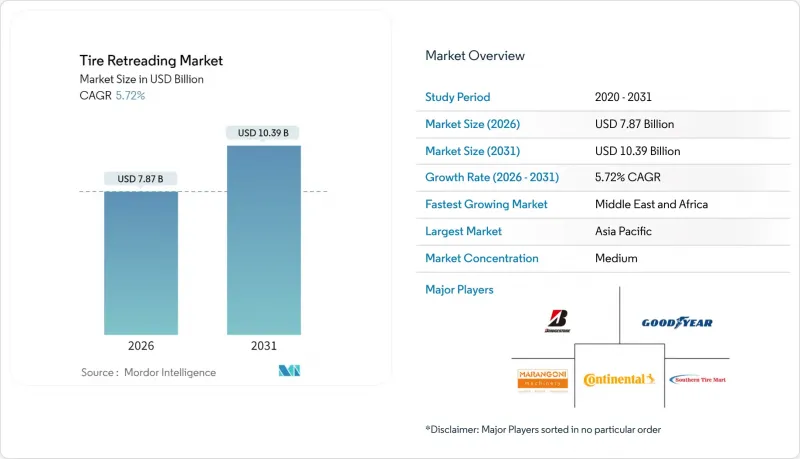

2025年轮胎翻新市场价值为74.4亿美元,预计到2031年将达到103.9亿美元,高于2026年的78.7亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.72%。

受原物料价格上涨、持续推进的碳减排目标以及提高卡车运转率需求的推动,翻新轮胎产业持续蓬勃发展。翻新轮胎不仅能显着降低成本,还能大幅减少碳排放和能源消耗,展现经济和环境的双重优势。亚太地区占最大的市场份额,这主要得益于中国庞大的重型车辆保有量和印度快速扩张的物流网络。同时,中东和非洲地区正崛起为成长最强劲的地区,这主要得益于蓬勃发展的采矿业和基础设施计划带动了非公路轮胎使用量的增加。此外,RFID追踪、自动化侦测线和预测性维护分析等技术创新正从单纯的成本节约措施发展成为以资料为中心的综合车队管理服务。

全球轮胎翻新市场趋势与洞察

与新轮胎相比,可节省成本

商业业者现在已将轮胎翻新纳入年度预算计划,因为与同等规格的新轮胎相比,每次翻新可节省五分之二的购买成本。随着合成橡胶和石油价格的波动,这一差异将进一步扩大,从而增强轮胎翻新在高运转率车队(例如长途货运和宅配运输)的成本效益。中国重型车辆产业就是这种成本会计的典型例子,预计2025年上半年中国重型卡车销售将达到约30万辆。航空公司也是如此,它们透过延长航空轮胎的使用寿命来维持微薄的营运利润。

循环经济和更严格的二氧化碳排放法规

欧盟循环经济行动计画的规定要求运输业者优先考虑轮胎再利用而非废弃,这使得轮胎翻新从一项可选措施转变为一项监管合规工具。欧盟7排放标准透过对提前更换轮胎进行处罚来强化这项义务,北美和亚太地区的主要经济体也正在引入类似的法规。环境效益显而易见:每翻新一条轮胎可减少30%的碳排放和70%的能源消耗,这些指标有助于运输公司达到其范围3报告目标。

外壳和橡胶价格波动

天然橡胶基准价格和与石油价格挂钩的合成橡胶成本的快速波动会侵蚀翻新轮胎厂的利润率,并使定价结构复杂化。小规模的独立工厂通常缺乏远期采购能力,容易受到现货市场价格剧烈波动的影响,从而挤压毛利率或迫使其提高价格,缩小翻新轮胎相对于新进口轮胎的成本优势。当原物料价格下跌时,新轮胎的折扣可能会暂时抑制对翻新轮胎的需求,直到市场恢復平衡。

细分市场分析

到2025年,中型和重型卡车将占轮胎翻新收入的45.02%,证实了高里程数使得轮胎翻新对于公路和区域运输业者至关重要。随着货运需求的持续强劲,预计到2031年,这一细分市场将继续支撑轮胎翻新市场的发展。受非洲和南美洲矿产开采活动不断扩大的推动,非公路和矿用轮胎预计将以5.96%的复合年增长率增长,这些地区的专用胎体成本是公路轮胎的数倍。航空领域的细分市场,其轮胎经批准可进行4到10次翻新,显示严格的安全监控可以与积极的成本管理相结合。这将带来强劲的复合年增长率,超过大多数地面交通领域的成长率。

由于安全方面的顾虑,乘用车翻新在欧洲和北美市场规模仍然小规模,但在监管门槛较低的拉丁美洲和亚洲市场则保持一定的份额。作为电子商务物流支柱的轻型商用车,为了适应都市区频繁的停靠,正在采用更短的翻新週期。在日本,双铰接式拖车的兴起需要能够承受更高轴荷的翻新轮胎设计,而目前只有少数技术先进的独立翻新企业能够提供这种技术。

截至2025年,预固化製程将占全球收入的60.95%,并将继续作为卡车轮胎大量生产的主流製程。其竞争优势源自于单位成本低、生产速度快。同时,模塑固化製程的市占率正以5.88%的复合年增长率快速成长,这得益于精密加热技术的进步和自动化压机的改进,这些技术缩短了生产週期,并实现了客製化胎面花纹。从基于人工智慧的表面检测到协作机器人操作,自动化技术透过标准化品质和减少人工投入,为这两种流程提供了支援。然而,不断增长的资本需求可能会加速产业整合,因为中小型工厂难以资金筹措设备升级资金。

随着车队对客製化花纹轮胎的需求不断增长,模塑硫化轮胎翻新的市场规模预计将会扩大。然而,预硫化製程的简单性和低能耗仍然是注重成本的车队的首选方法。 OEM整合式翻新工厂透过营运混合型设备来分散风险,这些设备会根据订单配置和胎体供应情况在不同製程之间切换。

区域分析

到2025年,亚太地区将占全球收入的38.51%,这主要得益于中国庞大的卡车保有量以及印度基础建设带来的高速公路吨公里数增长。各国政府推行的循环经济转型政策,例如中国的大规模更新换代行动计划,正在推动翻新轮胎的使用,因为车队正在向新能源汽车转型。日本对总拥有成本(TLC)模型的重视,也带动了对与预测性维护仪錶板直接相关的先进再製造服务的需求。

中东和非洲地区以6.06%的复合年增长率快速成长,这主要得益于能源和矿产计划的发展,这些项目推动了沙漠和露天矿场对越野轮胎的需求成长。沙乌地阿拉伯禁止进口翻新轮胎,并推出激励措施鼓励国内生产,从而保护了当地工厂免受海外价格波动的影响。南非和波札那的矿业走廊支撑着稳定的需求,但物流方面的限制使得移动侦测单元和现场抛光设备必不可少,以减少设备停机时间。

北美市场虽然成熟,但正经历快速的技术创新,RFID计画和政府激励措施正在推动工厂现代化。加拿大拥有多家专门的回收设施,主要用于卡车车壳的回收。如果美国提案的税额扣抵得以实施,预计将促进国内生产。在欧洲,诸如欧7排放标准和《废弃物框架指令》等监管利多因素,加上来自低成本进口产品的竞争,正促使回收企业投资于自动立体成像技术和机器人技术,以获得成本和品质优势。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 购买新轮胎可节省成本

- 循环经济和更严格的二氧化碳排放法规

- 电子商务物流推动车队行驶里程增加

- 政府对国产翻新轮胎的税额扣抵

- 基于RFID的生命週期追踪与保固分析

- 主要货运公司的绿色采购政策

- 市场限制

- 外壳和橡胶价格波动

- 大量超低价进口轮胎涌入

- 乘用车安全意识差距

- 仅限电动车相容的翻新胎设计

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和大型卡车

- 公车和长途客车

- 越野和采矿

- 农业/特种作物

- 透过生产方法

- 光之美少女

- 模具硬化

- 按轮胎类型

- 径向

- 偏见

- 固态/发泡材填充

- 按销售管道

- 独立翻新轮胎製造商

- OEM/自有车队设施

- 按最终用户行业划分

- 运输和物流车辆管理

- 建筑和采矿

- 农业

- 航空

- 军事/国防

- 废弃物管理及其他

- 透过使用

- 公路

- 越野

- 地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Bridgestone Corporation

- Michelin

- Goodyear

- Marangoni

- Continental AG

- Vipal Rubber

- Kal Tire

- Best-One Tire Group

- Southern Tire Mart

- Yokohama Rubber

- Hankook Tire

- Pirelli

- Sumitomo Rubber

- MRF

- Oliver Rubber

- TreadWright

- Qingdao Doublestar

- Rethread(Pty)Ltd

- Parrish Tire

- Redburn Tire

第七章 市场机会与未来展望

The Tire Retreading Market was valued at USD 7.44 billion in 2025 and estimated to grow from USD 7.87 billion in 2026 to reach USD 10.39 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031).

Driven by rising raw-material prices, ongoing carbon-reduction targets, and the imperative to maximize truck uptime, the momentum in the retreading industry continues. Retreaded casings offer significant cost savings and achieve notable reductions in carbon emissions and energy consumption, underscoring their dual economic and environmental advantages. The Asia-Pacific region commands the largest share of the market, thanks to China's expansive heavy-duty fleet and India's rapidly expanding logistics networks. In contrast, the Middle East & Africa emerge as the region with the most robust growth, driven by heightened off-road tire usage spurred by booming mining and infrastructure projects. Furthermore, advancements like RFID tracking, automated inspection lines, and predictive maintenance analytics are evolving from a mere cost-saving measure to a pivotal, data-centric service integral to comprehensive fleet contracts.

Global Tire Retreading Market Trends and Insights

Cost-savings Over New Tires

Commercial operators now embed retreading in annual budget planning because a single retread delivers two-fifths purchase-price relief versus a comparable new tire. That differential widens as synthetic rubber and petroleum costs trend upward, reinforcing retreading's payback in high-utilization fleets such as long-haul trucking and express-parcel delivery. China's heavy-duty sector, which logged almost 300,000 truck sales in the first half of 2025, epitomizes this cost calculus, while airlines stretch aviation-tire service life across multiple cycles to preserve thin operating margins .

Stricter Circular-Economy & CO2 Regulations

EU Circular Economy Action Plan rules oblige transport operators to prioritize reuse over disposal, turning tire retreading into a compliance tool rather than a discretionary measure. Euro 7 emission thresholds reinforce the mandate by penalizing premature tire replacement, and similar stimuli surface in North America and key Asia-Pacific economies. Environmental math is straightforward: every retread slashes carbon output by 30% and energy inputs by 70%, metrics that help carriers meet Scope 3 reporting targets .

Volatile Casing & Rubber Prices

Sudden swings in natural-rubber benchmarks and petroleum-linked synthetic rubber costs erode profit margins and complicate pricing grids for retread shops. Smaller independents often lack forward-buying capacity, exposing them to spot-market shocks that compress gross margin or force price hikes that narrow retread's cost edge against new imports. When raw material prices pull back, new-tire discounts can temporarily curb retread demand until equilibrium reasserts.

Other drivers and restraints analyzed in the detailed report include:

- Fleet-Mileage Growth From E-Commerce Logistics

- Government Tax-Credit Schemes For Domestic Retreads

- Influx Of Ultra-Low-Cost Import Tires

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium and heavy-duty trucks generated 45.02% of 2025 revenue, confirming that high-mileage cycles make retreading indispensable for line-haul and regional-haul carriers. This segment will continue anchoring the tire retreading market through 2031 as freight demand remains resilient. Off-the-road and mining tires are charted for a 5.96% CAGR, riding on mineral extraction activity in Africa and South America, where specialized casings cost multiples of on-road equivalents. With its 4-10 approved retread cycles, the aviation niche reveals how rigorous safety oversight can coexist with aggressive cost management, forecasting a robust CAGR that outpaces most ground-based segments.

Passenger car retreading remains marginal in Europe and North America amid safety perceptions but maintains footholds in Latin America and Asia, where regulatory barriers are lower. Light commercial vans, pivotal in e-commerce logistics, now adopt shorter retread cycles adjusted to urban stop frequency. Emerging double-articulated rigs in Japan require retread designs capable of handling higher axle loads, a technical capability that only the most advanced independent retreaders currently offer.

The pre-cure process held 60.95% of global revenue in 2025 and remains the go-to for high-volume truck casings. Its competitive advantage stems from lower per-unit cost and faster throughput. Mold-cure is gaining a 5.88% CAGR owing to improved precision heating and automated presses that shorten cycle times while allowing bespoke tread patterns. Automation, from AI-based surface inspection to collaborative robotic handlers, props up both methods by standardizing quality and trimming labor input. However, capitalization requirements could accelerate industry consolidation as smaller shops struggle to fund upgrades.

The tire retreading market size attributed to mold-cure lines is projected to increase as fleet demand for custom patterns grows. Yet, pre-cure's simplicity and lower energy load keep it the preferred method for cost-sensitive fleets. OEM-integrated retread plants hedge their bets by running hybrid facilities that switch methods based on order mix and casing availability.

The Tire Retreading Market Report is Segmented by Vehicle Type (Passenger Car, Light Commercial Vehicle, and More), Production Method (Pre-Cure and Mold-Cure), Tire Type (Radial, Bias, and Solid/Foam-filled), Sales Channel (Independent Retreaders and More), End-User Industry (Transport & Logistics Fleets and More), Application (On-Road, Off-Road), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 38.51% revenue in 2025, due to China's gigantic truck fleet and India's infrastructure push that multiplies highway ton-kilometers. Government policies emphasizing circular-economy compliance, such as China's Large-scale Equipment Renewal Action Plan, channel fleets toward retreading while they phase into new-energy vehicles. Japan's emphasis on total-life cost modeling translates into sophisticated demand for retread services that plug directly into predictive maintenance dashboards.

Middle East & Africa, the fastest-advancing region at 6.06% CAGR, gains from energy and mineral projects that lift off-road tire usage in deserts and open-pit mines. Saudi Arabia's ban on retread imports, combined with incentives for domestic production, shields local plants from foreign price shocks. South Africa and Botswana mining corridors underpin steady demand, although logistical constraints require mobile inspection units and on-site buffing rigs to curtail equipment downtime.

North America remains a mature yet tech-progressive territory where RFID programs and government incentives foster plant modernization. Canada hosts multiple dedicated retread facilities focused mainly on truck casings, and proposed U.S. credits would boost domestic volumes if passed into law. Europe blends regulatory tailwinds, Euro 7 and waste-framework directives, with competitive headwinds from low-priced imports, prompting retreaters to invest in automated stereography and robotics to achieve cost and quality leadership.

- Bridgestone Corporation

- Michelin

- Goodyear

- Marangoni

- Continental AG

- Vipal Rubber

- Kal Tire

- Best-One Tire Group

- Southern Tire Mart

- Yokohama Rubber

- Hankook Tire

- Pirelli

- Sumitomo Rubber

- MRF

- Oliver Rubber

- TreadWright

- Qingdao Doublestar

- Rethread (Pty) Ltd

- Parrish Tire

- Redburn Tire

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-Savings Over New Tires

- 4.2.2 Stricter Circular-Economy & Co2 Regulations

- 4.2.3 Fleet-Mileage Growth From E-Commerce Logistics

- 4.2.4 Government Tax-Credit Schemes for Domestic Retreads

- 4.2.5 RFID-Enabled Lifecycle Tracking & Warranty Analytics

- 4.2.6 Green Procurement Policies by Freight Majors

- 4.3 Market Restraints

- 4.3.1 Volatile Casing & Rubber Prices

- 4.3.2 Influx of Ultra-Low-Cost Import Tires

- 4.3.3 Passenger-Car Safety Perception Gaps

- 4.3.4 Limited EV-Ready Retread Designs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Light Commercial Vehicle

- 5.1.3 Medium & Heavy-Duty Truck

- 5.1.4 Bus & Coach

- 5.1.5 Off-the-Road & Mining

- 5.1.6 Agriculture & Specialty

- 5.2 By Production Method

- 5.2.1 Pre-cure

- 5.2.2 Mold-cure

- 5.3 By Tire Type

- 5.3.1 Radial

- 5.3.2 Bias

- 5.3.3 Solid / Foam-filled

- 5.4 By Sales Channel

- 5.4.1 Independent Retreaders

- 5.4.2 OEM / Captive Fleet Facilities

- 5.5 By End-user Industry

- 5.5.1 Transport & Logistics Fleets

- 5.5.2 Construction & Mining

- 5.5.3 Agriculture

- 5.5.4 Aviation

- 5.5.5 Military & Defense

- 5.5.6 Waste Management & Others

- 5.6 By Application

- 5.6.1 On-road

- 5.6.2 Off-road

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.1.4 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Russia

- 5.7.3.6 Spain

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Egypt

- 5.7.5.5 South Africa

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Bridgestone Corporation

- 6.4.2 Michelin

- 6.4.3 Goodyear

- 6.4.4 Marangoni

- 6.4.5 Continental AG

- 6.4.6 Vipal Rubber

- 6.4.7 Kal Tire

- 6.4.8 Best-One Tire Group

- 6.4.9 Southern Tire Mart

- 6.4.10 Yokohama Rubber

- 6.4.11 Hankook Tire

- 6.4.12 Pirelli

- 6.4.13 Sumitomo Rubber

- 6.4.14 MRF

- 6.4.15 Oliver Rubber

- 6.4.16 TreadWright

- 6.4.17 Qingdao Doublestar

- 6.4.18 Rethread (Pty) Ltd

- 6.4.19 Parrish Tire

- 6.4.20 Redburn Tire

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2035年再生轮胎市场分析及预测:按类型、产品类型、服务、技术、组件、应用、材质、製造流程和最终用户划分

2035年再生轮胎市场分析及预测:按类型、产品类型、服务、技术、组件、应用、材质、製造流程和最终用户划分 2026年全球轮胎翻新市场报告

2026年全球轮胎翻新市场报告 2025-2029年全球汽车轮胎翻新服务市场

2025-2029年全球汽车轮胎翻新服务市场 全球翻新轮胎市场-按车辆类型、翻新製程、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年)

全球翻新轮胎市场-按车辆类型、翻新製程、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年) 汽车轮胎胎面感测器:全球市场份额和排名、总收入和需求预测(2025-2031年)

汽车轮胎胎面感测器:全球市场份额和排名、总收入和需求预测(2025-2031年) 轮胎翻新市场,按轮胎类型、按工艺、按车辆类型、按最终用户、按销售管道、按国家/地区划分 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测

轮胎翻新市场,按轮胎类型、按工艺、按车辆类型、按最终用户、按销售管道、按国家/地区划分 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测 2025-2029年全球汽车翻新轮胎市场汽车翻新轮胎市场报告:2030 年趋势、预测与竞争分析

2025-2029年全球汽车翻新轮胎市场汽车翻新轮胎市场报告:2030 年趋势、预测与竞争分析 全球汽车翻新轮胎市场:按製程类型、销售通路、车型和地区进行预测(截至2030年)

全球汽车翻新轮胎市场:按製程类型、销售通路、车型和地区进行预测(截至2030年)