|

市场调查报告书

商品编码

1940674

亚太地区快递、速递和小包裹(CEP):市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Asia-Pacific Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

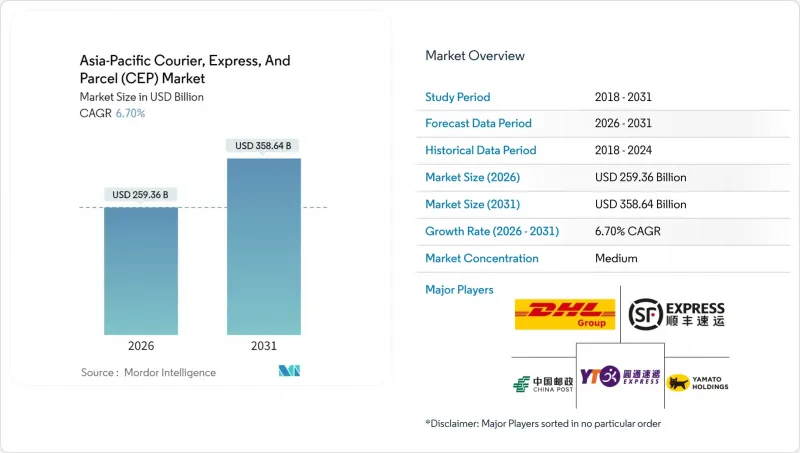

预计到 2026 年,亚太地区快递、速递和小包裹(CEP) 市场规模将达到 2,593.6 亿美元。

这意味着从 2025 年的 2,430.8 亿美元成长到 2031 年的 3,586.4 亿美元,2026 年至 2031 年的复合年增长率为 6.70%。

这一扩张反映了该地区电子商务的持续成长势头、数位支付的日益普及以及RCEP和CPTPP等支持性贸易框架。当日达服务正从一项高端附加服务服务转变为基本服务,促使企业对都市区微型仓配中心进行大规模投资。能够整合即时追踪、预测路线和温控功能的业者可望获得高利润的订单量。同时,劳动力短缺和燃油价格波动正在限制营运利润,并推动自动化进程。

亚太地区快递、速递与小包裹(CEP) 市场趋势与洞察

电子商务和当日配送文化的快速发展

都市区收入的成长和行动网路的普及,使得隔天达和当日达成为亚洲主要城市的新标准。预计到2024年,区域电子商务市场规模将超过2兆美元,而当无法选择快捷邮件服务时,消费者放弃购物车的现像日益普遍。物流公司正透过在城市郊区设立微型仓配中心来应对这项挑战,并利用预测分析技术按邮递区号聚合订单。虽然提高当日达配送密度可以提升配送效率,但也增加了人事费用和房地产成本,从而推动了电动摩托车和自动储物柜的普及。快速生鲜电商模式将配送时间缩短至30分钟以内,迫使传统的中心辐射式网路转型为以接近性为优先的节点式网状结构。这些变化为能够降低单位成本的企业带来了获利机会。

跨境电子商务商业联盟(RCEP、CPTPP)

RCEP成员国已取消90%贸易商品的关税,而CPTPP简化的海关程序已将成员国境内的平均清关时间缩短了三分之一。中型物流公司正利用数位原产地证书实现曼谷和东京之间两日达的门到门配送。菲律宾和越南的小规模经销商正透过与区域一体化服务提供者建立市场合作关係,获得出口管道,这些服务提供者提供货运代理、关税预付和退货管理等服务。随着进口限额的提高,小包裹量正从邮政路线转向特快专递,这有助于在商品价格走软的情况下稳定收费系统。单一视窗平台之间互通性进一步减少了文书工作,并提高了服务的可靠性。

都市区对司机运作时间的限制和劳动力短缺

新加坡实施每週44小时工作制,东京市中心夜间货车交通管制,导致尖峰时段的配送能力受限。日本和韩国人口老化,劳动人口萎缩,而小包裹量却不断增加。在中国的一线城市,物流业的薪资在2024年有所上涨,业者也提供入职奖金以吸引配送员。为了降低风险,货运公司正在拓展替代收货点并测试人行道机器人。然而,自动驾驶技术仍处于测试阶段,劳动力短缺仍是目前限制物流配送的阻碍因素。

细分市场分析

2025年,电子商务将占小包裹需求的34.42%,反映消费者根深蒂固的网路购物习惯。受生物製药、临床试验样本和居家医疗器材的推动,医疗配送将在2026年至2031年间以7.03%的复合年增长率成长。亚太地区的快递、速递和小包裹(CEP)市场以符合规范的低温运输运输路线、被动式包装和即时感测器为特征。

製造业依赖即时原料配送维持稳定的基础,而金融服务业则需要安全可追溯地运输敏感文件。快速生鲜杂货零售需要对高频次、低价值订单进行近乎即时的配送,从而扩大网路容量。

预计2026年至2031年,国际小包裹递送量将以6.86%的复合年增长率成长。同时,截至2025年,国内货物在亚太快递、速递和小包裹(CEP)市场中占据了压倒性的64.02%的份额。区域全面经济伙伴关係协定(RCEP)下的海关数位化缩短了边境停留时间,使得主要城市之间的递送时间缩短至两到三天。与跨境电商密切相关的亚太快递、速递和小包裹(CEP)市场预计将持续成长至2030年。虽然国内市场的密度优势支撑了较低的单价,但大都会圈的当日送达保证却对利润率构成了压力。

跨境需求在寻求供应链多元化的中型出口商中最为强劲。目前,快速电商平台承诺72小时内将韩国小众美妆产品送达东南亚,买家需支付双倍的高级追踪费用。儘管有许多挑战,例如资讯不对称和语言障碍,但随着海关、承运商和电商平台之间共用资料介面的建立,这些挑战正在逐步缓解。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 人口统计数据

- 按经济活动分類的GDP分配

- 按经济活动分類的GDP成长

- 通货膨胀

- 经济表现及概况

- 电子商务产业的趋势

- 製造业趋势

- 运输和仓储业的GDP

- 出口趋势

- 进口趋势

- 燃油价格

- 物流绩效

- 基础设施

- 法律规范

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 巴基斯坦

- 菲律宾

- 泰国

- 越南

- 价值炼和通路分析

- 市场驱动因素

- 电子商务和当日配送文化的快速发展

- 跨境电子商务企业间的合作(RCEP、CPTPP)

- 政府主导的智慧物流走廊(中国、印度、东协)

- 生技药品和生鲜食品低温运输需求快速成长

- 人工智慧驱动的路线优化与自主枢纽

- 微型仓配和暗店的兴起

- 市场限制

- 都市区的行车时间限制与劳力短缺

- 燃油价格波动与航空燃油额外费用

- 消除二、三线城市在医疗服务体系上的差距

- 地缘政治贸易路线中断(海峡、南海)

- 市场创新

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 目的地

- 国内的

- 国际的

- 配送速度

- 快递

- 非快递

- 模型

- B2B

- B2C

- C2C

- 运输重量

- 重型货物

- 轻型货物

- 中等重量货物

- 交通工具

- 航空

- 路

- 其他的

- 终端用户产业

- 电子商务

- 金融服务(BFSI)

- 卫生保健

- 製造业

- 一级产业

- 批发零售(线下)

- 其他的

- 国家

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 巴基斯坦

- 菲律宾

- 泰国

- 越南

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 重大策略倡议

- 市占率分析

- 公司简介

- Blue Dart Express Limited

- China Post

- CJ Logistics Corporation

- DHL Group

- DTDC Express Limited

- FedEx

- Japan Post Holdings Co., Ltd.(including Toll Group)

- JWD Group

- SF Express(KEX-SF)

- SG Holdings Co., Ltd.

- Shanghai YTO Express(Logistics)Co., Ltd.

- United Parcel Service(UPS)

- Yamato Holdings Co., Ltd.

- ZTO Express

第七章 市场机会与未来展望

Asia-Pacific courier, express, and parcel market size in 2026 is estimated at USD 259.36 billion, growing from 2025 value of USD 243.08 billion with 2031 projections showing USD 358.64 billion, growing at 6.70% CAGR over 2026-2031.

This expansion reflects the region's sustained e-commerce momentum, wider digital payments adoption, and supportive trade frameworks such as RCEP and CPTPP. Same-day fulfillment expectations have shifted from premium add-ons to baseline service levels, prompting heavy investment in urban micro-fulfillment assets. Operators that integrate real-time tracking, predictive routing, and temperature-controlled capacity are positioned to secure higher-margin volumes. Meanwhile, labor constraints and fuel price swings temper operating margins and incentivize automation.

Asia-Pacific Courier, Express, And Parcel (CEP) Market Trends and Insights

E-commerce Boom and Same-Day Culture

Rising urban incomes and mobile internet access have entrenched next-day and same-day delivery as the new normal across leading Asian cities. Regional e-commerce value surpassed USD 2 trillion in 2024, and shoppers now abandon carts if express options are unavailable. Logistics firms respond by positioning inventory inside city-edge micro-fulfillment sites and using predictive analytics to consolidate orders by postcode. Same-day density boosts stop efficiency yet raise wages and real estate costs, prompting wider deployment of electric two-wheelers and automated lockers. Rapid-commerce grocery models compress fulfillment windows to under 30 minutes, forcing a redesign of traditional hub-and-spoke networks into nodal mesh layouts that prioritize proximity. These shifts underpin premium yield opportunities for operators able to keep unit costs in check.

Cross-Border E-Tailer Alliances (RCEP, CPTPP)

Tariff elimination on 90% of goods traded under RCEP and streamlined customs protocols under CPTPP have shortened average clearance times by one-third within member states. Mid-sized logistics providers now harness digital certificates of origin to offer two-day door-to-door delivery between Bangkok and Tokyo. Smaller sellers in the Philippines and Vietnam gain export access through marketplace tie-ups with regional integrators that bundle freight, duty pre-payment, and returns management. As import ceilings rise, parcel volumes shift from postal channels to premium express lanes, supporting rate integrity despite softening commodity prices. Enhanced interoperability across single-window platforms further shrinks paperwork and boosts service reliability.

Urban Driver-Hour Caps and Labor Shortages

Singapore's 44-hour weekly limit and Tokyo's downtown truck curfews constrain peak-hour capacity. Aging demographics in Japan and South Korea shrink the available workforce even as parcel counts climb. Chinese tier-one cities saw logistics wages climb during 2024, with operators offering sign-on bonuses to secure riders. To mitigate exposure, carriers extend alternative collection points and test sidewalk robots. Yet autonomous options remain at pilot scale, keeping tight labor supply a near-term constraint.

Other drivers and restraints analyzed in the detailed report include:

- Government Smart-Logistics Corridors

- Cold-Chain Surge for Biologics and Fresh Food

- Volatile Bunker and Jet-Fuel Surcharges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-commerce contributed 34.42% of parcel demand in 2025, reflecting entrenched online shopping behavior. Healthcare deliveries advance at a 7.03% CAGR between 2026-2031, driven by biologics, clinical trial samples, and home-care devices. The Asia-Pacific courier, express, and parcel market supports regulatory-compliant cold-chain lanes featuring passive packaging and real-time sensors.

Manufacturing maintains a stable baseline through just-in-time raw-material flows, while financial services require secure, tracked movement of confidential documents. Grocery quick commerce stretches network capacity with high-frequency, low-ticket orders demanding near-instant dispatch.

International parcel flows expanded at a 6.86% CAGR between 2026-2031, even as domestic consignments retained a commanding 64.02% hold on the Asia-Pacific courier, express, and parcel market in 2025. Customs digitalization under RCEP cuts border dwell time, enabling 2- to 3-day delivery between key metropolitan pairs. The Asia-Pacific courier, express, and parcel market size linked to cross-border e-commerce is forecast to grow steadily through 2030. Domestic density advantages support low unit costs, but same-day guarantees pressure margins in megacities.

Cross-border demand is strongest among mid-market exporters pursuing supply-chain diversification. Quick commerce marketplaces now promise 72-hour delivery for niche Korean beauty products into Southeast Asia, with buyers paying double the standard tariff for premium tracking. Addressing gaps and language barriers persists, yet is gradually mitigated through shared data interfaces between customs, carriers, and marketplaces.

The Asia-Pacific Courier, Express, and Parcel (CEP) Market Report is Segmented by Destination (Domestic and International), Speed of Delivery (Express and Non-Express), Model (Business-To-Business (B2B), and More), Shipment Weight (Heavy Weight, and More), Mode of Transport (Air, Road, and Others), End User Industry (E-Commerce, and More), and Country (China, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Blue Dart Express Limited

- China Post

- CJ Logistics Corporation

- DHL Group

- DTDC Express Limited

- FedEx

- Japan Post Holdings Co., Ltd. (including Toll Group)

- JWD Group

- SF Express (KEX-SF)

- SG Holdings Co., Ltd.

- Shanghai YTO Express (Logistics) Co., Ltd.

- United Parcel Service (UPS)

- Yamato Holdings Co., Ltd.

- ZTO Express

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.13.1 Australia

- 4.13.2 China

- 4.13.3 India

- 4.13.4 Indonesia

- 4.13.5 Japan

- 4.13.6 Malaysia

- 4.13.7 Pakistan

- 4.13.8 Philippines

- 4.13.9 Thailand

- 4.13.10 Vietnam

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 E-Commerce Boom and Same-Day Culture

- 4.15.2 Cross-Border E-Tailer Alliances (RCEP, CPTPP)

- 4.15.3 Government Smart-Logistics Corridors (China, India, ASEAN)

- 4.15.4 Cold-Chain Surge for Biologics and Fresh Food

- 4.15.5 AI-Driven Route-Optimization and Autonomous Hubs

- 4.15.6 Micro-Fulfilment and Dark-Store Proliferation

- 4.16 Market Restraints

- 4.16.1 Urban Driver-Hour Caps and Labor Shortages

- 4.16.2 Volatile Bunker and Jet-Fuel Surcharges

- 4.16.3 Addressing-System Gaps in Tier-2/3 Cities

- 4.16.4 Geopolitical Trade-Lane Disruptions (Straits, SCS)

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

- 5.7 Country

- 5.7.1 Australia

- 5.7.2 China

- 5.7.3 India

- 5.7.4 Indonesia

- 5.7.5 Japan

- 5.7.6 Malaysia

- 5.7.7 Pakistan

- 5.7.8 Philippines

- 5.7.9 Thailand

- 5.7.10 Vietnam

- 5.7.11 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Blue Dart Express Limited

- 6.4.2 China Post

- 6.4.3 CJ Logistics Corporation

- 6.4.4 DHL Group

- 6.4.5 DTDC Express Limited

- 6.4.6 FedEx

- 6.4.7 Japan Post Holdings Co., Ltd. (including Toll Group)

- 6.4.8 JWD Group

- 6.4.9 SF Express (KEX-SF)

- 6.4.10 SG Holdings Co., Ltd.

- 6.4.11 Shanghai YTO Express (Logistics) Co., Ltd.

- 6.4.12 United Parcel Service (UPS)

- 6.4.13 Yamato Holdings Co., Ltd.

- 6.4.14 ZTO Express

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球宅配、包裹及小包裹市场:2026-2032年市场预测(按类型、服务类型、货物类型、目的地、配送速度、货量、运输方式及最终用户划分)

全球宅配、包裹及小包裹市场:2026-2032年市场预测(按类型、服务类型、货物类型、目的地、配送速度、货量、运输方式及最终用户划分) 2026年全球包裹递送服务市场报告2026年全球宅配与小包裹递送市场报告2026年全球宅配服务市场报告2026年全球快递与信差市场报告2026年全球宅配市场报告2026年全球当日配送服务市场报告2026年全球超当地语系化配送应用市场报告

2026年全球包裹递送服务市场报告2026年全球宅配与小包裹递送市场报告2026年全球宅配服务市场报告2026年全球快递与信差市场报告2026年全球宅配市场报告2026年全球当日配送服务市场报告2026年全球超当地语系化配送应用市场报告 2026-2030年全球宅配包裹(CEP)市场

2026-2030年全球宅配包裹(CEP)市场 宅配、包裹及小包裹市场报告:按服务类型、目的地、物品、最终用途行业和地区划分(2026-2034 年)

宅配、包裹及小包裹市场报告:按服务类型、目的地、物品、最终用途行业和地区划分(2026-2034 年)