|

市场调查报告书

商品编码

1940681

泰国快递、速递和小包裹(CEP) 市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)Thailand Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

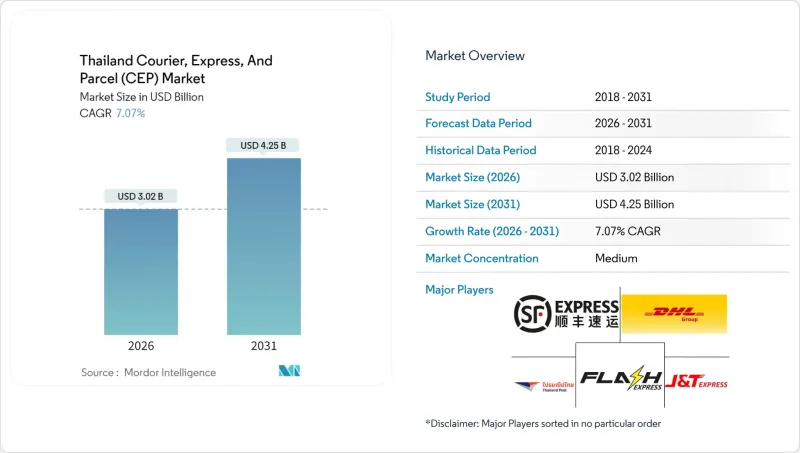

预计泰国快递、速递和小包裹(CEP) 市场将从 2025 年的 28.2 亿美元成长到 2026 年的 30.2 亿美元,到 2031 年将达到 42.5 亿美元,2026 年至 2031 年的复合年增长率为 7.07%。

这一稳健的成长轨迹反映了泰国作为区域物流枢纽的地位,受益于政府的「泰国4.0」策略、电子商务的持续发展大规模基础设施建设。可支配收入的成长促进了国内小包裹流通,而连接寮国-中国走廊的高速铁路则为跨境的快速扩张奠定了基础。低温运输投资正在拓展药品和生鲜食品的物流服务范围,而5G连接和人工智慧投资则实现了路线优化、库存视觉化和即时追踪。平台型物流产业的兴起既推动了竞争,也促使企业不断提升效率,从而维持了高品质的服务和快速的配送速度。

泰国快递、速递与小包裹(CEP) 市场趋势与洞察

电子商务的爆炸性成长

泰国线上零售业持续快速成长,这主要得益于数位支付的普及和行动优先的购物习惯。各大平台承诺当日送达,迫使快递公司在确保网路可靠性的同时,缩短截止时间。持续不断的折扣宣传活动在旺季推高了需求,促使商家采取应对措施,例如建立临时收发货中心、利用人工智慧进行需求预测以及众包司机等。尤其是在曼谷,较高的小包裹密度使得商家即使在价格竞争激烈的情况下也能製定盈利的配送路线。政府对无现金支付的支持进一步扩大了基本客群,而更快的现金处理速度也降低了配送失败率。

中产阶级可支配所得增加

泰国央行预测GDP成长将加快,这将提升家庭购买力,并促使更多消费者为了方便而选择高端快捷邮件服务。财政部推出的数位钱包奖励策略注入了流动性,直接转化为线上购物的成长。随着国内旅游业的復苏,酒店业的需求也随之增加,带动了对床上用品、食品和酒店用品等配送服务的需求,这些服务需要送往全国各地的酒店。为此,快递公司正在将隔天达服务扩展到清迈和普吉岛等区域性城市,併升级其面向客户的应用程序,以提供更精准的送达时间。如今,高端护肤品、电子产品和专门食品咖啡均采用温控包装配送,这显示消费者越来越愿意为更优质的服务付费。

竞争加剧导致利润率下降

平台物流集团过度促销的策略给现有物流公司的小包裹价格带来了压力。折扣券和免运费宣传活动降低了消费者的预期,迫使承运商扩大规模并实现自动化以维持获利能力。规模较小的承运商无力投资机器人分类中心,难以维持服务水平,引发了一波策略联盟浪潮。泰国邮政正透过增值仓储和清关服务来缓解压力,而私人宅配业者则在试点将退货处理和包裹保险相结合的订阅模式。

细分市场分析

电子商务将在交易量方面继续保持领先地位,预计到2025年将占据34.86%的收入份额,这主要得益于社交电商直播和预售活动的蓬勃发展。温控包装和身分验证配送在化妆品和酒类产业正日益普及。医疗小包裹虽然数量不多,但由于严格的监管要求(例如需要符合GDP认证的加工流程),其利润率仍然很高。受人口老化和药品分销改革的推动,预计2026年至2031年间,泰国快递、速递和小包裹(CEP)行业的医疗收入将以7.41%的复合年增长率增长。

随着工厂实施准时制生产模式,对製造业小包裹的需求预计将保持强劲,因为低价值、高紧急性的备件需要透过可靠的宅配运输。金融服务信封的使用量随着银行对帐单的数位化提高而逐渐下降,但对重要文件宅配的需求依然旺盛,这些快递公司负责递送法律文件和公证合约。

儘管国际小包裹目前仅占收入的一小部分,但预计其成长速度将超过国内配送,2026年至2031年的复合年增长率将达到7.31%。这一成长动能主要得益于供应商来源多元化(主要来自中国)、小小包裹免税配额优惠政策以及东协单一窗口提供的简化海关API。受昆明-曼谷铁路走廊建设的推动,泰国快递、速递和小包裹(CEP)市场规模预计到2031年将超过15.3亿美元,该走廊将缩短干线运输时间。泰国邮政已推出海关预付服务以缩短最后一公里配送週期,而私人宅配业者则为面向泰国消费者的海外企业提供集履约和客户服务于一体的增值服务。

国内运输是公司的核心业务,预计到2025年将占总收入的64.35%,主要得益于大都会圈的需求。在曼谷,每位驾驶每天的包裹递送密度超过150件。然而,区域扩张计画以及在农业省份获得无人机试飞许可表明,承运人已做好准备,迎接首都以外地区的下一波成长。服务柔软性——例如站点内的包裹柜、隔夜送达和即时重新派送安排——是该领域竞争优势的关键所在。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 人口统计数据

- 按经济活动分類的GDP分配

- 按经济活动分類的GDP成长

- 通货膨胀

- 经济表现及概况

- 电子商务产业的趋势

- 製造业趋势

- 运输和仓储业GDP

- 出口趋势

- 进口趋势

- 燃油价格

- 物流绩效

- 基础设施

- 法律规范

- 价值炼和通路分析

- 市场驱动因素

- 电子商务的爆炸性成长

- 中产阶级可支配所得不断成长

- 政府主导的「泰国4.0」数位物流推广

- 物流基础建设(东部经济走廊、高速公路)

- 利用寮国-泰国高速铁路进行跨境电子商务

- 扩大低温运输和最后一公里网络

- 市场限制

- 竞争加剧导致利润率下降

- 燃油价格波动

- 零工经济导致外送员离职率

- 曼谷交通瓶颈

- 市场创新

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 目的地

- 国内的

- 国际的

- 配送速度

- 快递

- 非快递

- 模型

- B2B

- B2C

- C2C

- 运输重量

- 重型货物

- 轻型货物

- 中等重量货物

- 交通工具

- 航空

- 陆上

- 其他的

- 终端用户产业

- 电子商务

- 金融服务(BFSI)

- 卫生保健

- 製造业

- 一级产业

- 批发零售(线下)

- 其他的

第六章 竞争情势

- 市场集中度

- 重大策略倡议

- 市占率分析

- 公司简介

- Aqua Corporation(including Thai Parcel Public Company Limited)

- BEST Inc.

- CJ Logistics Corporation

- DHL Group

- FedEx

- Flash Express

- J&T Express

- JWD Group

- Nim Express Company Ltd.

- SF Express(KEX-SF)

- Thailand Post

- United Parcel Service(UPS)

第七章 市场机会与未来展望

The Thailand courier express parcel market is expected to grow from USD 2.82 billion in 2025 to USD 3.02 billion in 2026 and is forecast to reach USD 4.25 billion by 2031 at 7.07% CAGR over 2026-2031.

This healthy trajectory reflects Thailand's role as a regional logistics hub benefiting from the government's Thailand 4.0 strategy, continued e-commerce adoption, and large-scale infrastructure upgrades that knit together road, rail, air, and port assets. Rising disposable income strengthens domestic parcel flows, while the high-speed rail link to the Laos-China corridor positions the country for rapid cross-border expansion. Cold-chain investment widens service breadth toward pharmaceuticals and perishables, and 5G connectivity plus AI investments enable route optimization, inventory visibility, and real-time tracking. Platform-owned logistics arms inject additional competition but also stimulate continuous efficiency improvements that keep service quality high and delivery times low.

Thailand Courier, Express, And Parcel (CEP) Market Trends and Insights

Explosive Growth of E-Commerce

Thailand's online retail sector continues to soar, lifted by digital-payment penetration and mobile-first shopping habits. Major platforms integrate same-day delivery promises, forcing couriers to tighten cutoff times while maintaining network reliability. Continuous discount events create peak-season surges that operators now manage with temporary hubs, AI-based demand forecasting, and crowdsourced driver pools. The resulting parcel density, especially in Bangkok, supports profitable route planning even at competitive price points. Government support for cashless transactions further expands the addressable customer base and lowers failed-delivery rates by shrinking cash-handling time.

Rising Middle-Class Disposable Income

The Bank of Thailand projects accelerating GDP growth that lifts household consumption power, nudging shoppers toward premium express options for convenience. The Ministry of Finance's digital-wallet stimulus injects liquidity that translates directly into online purchases. Domestic travel and tourism rebound adds demand from hospitality suppliers moving linen, food, and amenities to hotels statewide. Couriers expand next-day coverage to regional cities such as Chiang Mai and Phuket in response, while upgrading customer-facing apps to offer precise delivery slots. Luxury skincare, electronics, and specialty coffee now travel via temperature-controlled packs, signaling willingness to pay for service upgrades.

Aggressive Price Competition Eroding Margins

Cut-throat promotional tactics by platform-owned logistics groups compress per-parcel yields for incumbents. Discount vouchers and free-shipping festivals reset consumer expectations downward, forcing carriers to pursue scale and automation to stay profitable. Smaller players without capital for sort-center robotics struggle to match service levels, sparking a wave of strategic alliances. Thailand Post offsets pressure by monetizing value-added warehousing and customs brokerage, while private couriers pilot subscription models that bundle returns handling and parcel insurance.

Other drivers and restraints analyzed in the detailed report include:

- Government Thailand 4.0 Digital-Logistics Push

- Logistics-Infrastructure Upgrades (EEC, Highways)

- Fuel-Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-commerce consistently tops the volume chart with 34.86% revenue share in 2025, underpinned by social-commerce livestreams and payday flash sales. Temperature-controlled packs and secure ID-check delivery are gaining traction within cosmetics and alcohol verticals. Healthcare parcels generate less volume but higher margins, thanks to stringent regulatory compliance mandating GDP-certified handling. The Thailand courier express parcel industry expects healthcare revenue to grow by a 7.41% CAGR between 2026-2031, helped by aging demographics and national pharmaceutical distribution reforms.

Manufacturing parcels stay relevant as factories adopt just-in-time models that need dependable courier links for low-value high-urgency spares. Financial-services envelopes decline gradually as banks digitize statements, though secure-document couriers still serve legal filings and notarized contracts.

International parcels, though contributing a smaller proportion of revenue, are projected to grow faster than domestic flows at a 7.31% CAGR between 2026-2031. That momentum stems from supplier diversification out of China, duty-free thresholds that favor small parcels, and streamlined customs APIs under the ASEAN Single Window. The Thailand courier express parcel market size related to cross-border flows is forecast to surpass USD 1.53 billion by 2031, aided by the Kunming-Bangkok rail corridor that compresses line-haul times. Thailand Post already offers customs pre-payment to shorten last-mile cycles, while private couriers bundle fulfillment and customer-service add-ons for overseas merchants eyeing Thai consumers.

Domestic traffic remains the volume cornerstone with 64.35% revenue share of 2025, anchored by dense metropolitan demand that yields route densities above 150 parcels per driver per day in Bangkok. However, rural expansion programs and drone trial permits in agricultural provinces show carriers are preparing for next-wave growth beyond the capital. Service flexibility-parcel lockers in petrol stations, timed evening delivery, and real-time rescheduling-defines competitive advantage within this segment.

The Thailand Courier, Express, and Parcel (CEP) Market Report is Segmented by End User Industry (E-Commerce and More), Destination (Domestic and More), Speed of Delivery (Express and Non-Express), Shipment Weight (Heavy Weight Shipments and More), Mode of Transport (Air, Road, and Others), and Model (Business-To-Business, Business-To-Consumer, and Consumer-To-Consumer). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Aqua Corporation (including Thai Parcel Public Company Limited)

- BEST Inc.

- CJ Logistics Corporation

- DHL Group

- FedEx

- Flash Express

- J&T Express

- JWD Group

- Nim Express Company Ltd.

- SF Express (KEX-SF)

- Thailand Post

- United Parcel Service (UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 Explosive Growth of E-Commerce

- 4.15.2 Rising Middle-Class Disposable Income

- 4.15.3 Government "Thailand 4.0" Digital-Logistics Push

- 4.15.4 Logistics-Infrastructure Upgrades (EEC, Highways)

- 4.15.5 Cross-Border E-Commerce via Laos-Thailand High-Speed Rail

- 4.15.6 Expansion of Cold-Chain Last-Mile Networks

- 4.16 Market Restraints

- 4.16.1 Aggressive Price Competition Eroding Margins

- 4.16.2 Fuel-Price Volatility

- 4.16.3 Gig-Economy Courier Churn

- 4.16.4 Bangkok Traffic Congestion Bottlenecks

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Aqua Corporation (including Thai Parcel Public Company Limited)

- 6.4.2 BEST Inc.

- 6.4.3 CJ Logistics Corporation

- 6.4.4 DHL Group

- 6.4.5 FedEx

- 6.4.6 Flash Express

- 6.4.7 J&T Express

- 6.4.8 JWD Group

- 6.4.9 Nim Express Company Ltd.

- 6.4.10 SF Express (KEX-SF)

- 6.4.11 Thailand Post

- 6.4.12 United Parcel Service (UPS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球宅配、包裹及小包裹市场:2026-2032年市场预测(按类型、服务类型、货物类型、目的地、配送速度、货量、运输方式及最终用户划分)

全球宅配、包裹及小包裹市场:2026-2032年市场预测(按类型、服务类型、货物类型、目的地、配送速度、货量、运输方式及最终用户划分) 2026年全球包裹递送服务市场报告2026年全球宅配与小包裹递送市场报告2026年全球宅配服务市场报告2026年全球快递与信差市场报告2026年全球宅配市场报告2026年全球当日配送服务市场报告2026年全球超当地语系化配送应用市场报告

2026年全球包裹递送服务市场报告2026年全球宅配与小包裹递送市场报告2026年全球宅配服务市场报告2026年全球快递与信差市场报告2026年全球宅配市场报告2026年全球当日配送服务市场报告2026年全球超当地语系化配送应用市场报告 2026-2030年全球宅配包裹(CEP)市场

2026-2030年全球宅配包裹(CEP)市场 宅配、包裹及小包裹市场报告:按服务类型、目的地、物品、最终用途行业和地区划分(2026-2034 年)

宅配、包裹及小包裹市场报告:按服务类型、目的地、物品、最终用途行业和地区划分(2026-2034 年)