|

市场调查报告书

商品编码

1940683

证书颁发机构:市场占有率分析、产业趋势与统计资料、成长预测(2026-2031 年)Certificate Authority - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

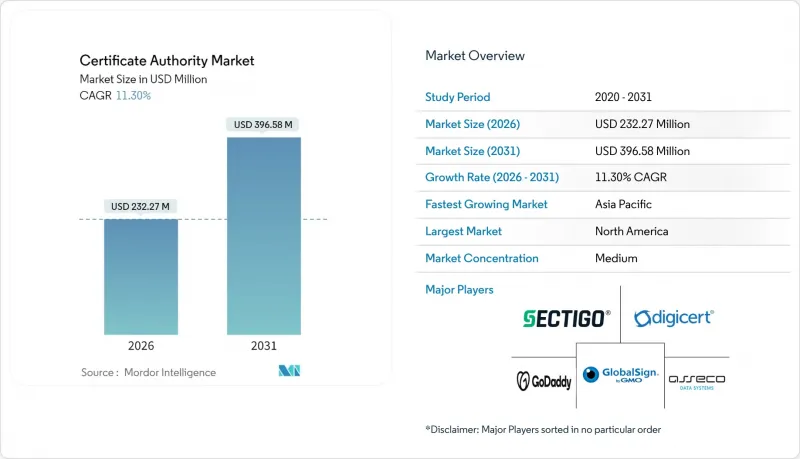

预计到 2026 年,凭证授权单位 (CA) 市场规模将达到 2.3227 亿美元,高于 2025 年的 2.0868 亿美元。

预计到 2031 年将达到 3.9658 亿美元,2026 年至 2031 年的复合年增长率为 11.3%。

随着企业从基于边界的防御转向以身分为中心的模式(该模式依赖于对每次数位互动的加密检验),PKI 的采用速度加快。证书生命週期的缩短、向后量子加密技术的早期过渡以及零信任的快速普及,都增加了证书续订量,并将自动化提升到了董事会层面的优先事项。浏览器厂商扮演着事实上的监管机构的角色,尤其是谷歌 Chrome 严格的根证书计划执行,使得供应商的选择不再仅仅基于价格,而是基于合规历史。同时,云端管理的 PKI 服务表明,外包专业知识能够提供手动流程无法实现的速度和一致性。亚太地区电子商务的快速成长,加上政府对 PKI 的强制性要求,使得该地区的成长速度远超更成熟的北美和欧洲市场。

全球证书颁发机构市场趋势与洞察

严格的法规和合规义务

浏览器根凭证储存区拥有者正在加强合规性,最显着的例子是Chrome宣布将不再信任2024年10月之后颁发的Entrust凭证。因此,企业买家越来越重视证书颁发机构(CA)的纪律记录以及其技术实力,这一趋势正在持续重塑证书颁发机构市场。新的CA/浏览器论坛规则将TLS凭证的最大有效期缩短至47天(到2029年3月),这将增加续约量,并有利于具备即时自动化功能的供应商。託管PKI供应商已经开始强调独立审核结果,以证明其合规性。同时,金融和医疗保健等受监管行业正在加快与一级CA的续订,以避免未来失去信任带来的声誉风险。

扩展基于云端的 PKI 服务

对于那些不想维护自有硬体安全模组 (HSM)、凭证撤销清单 (CRL) 分发点和审核控制措施的组织而言,云端服务已成为预设的起点。 DigiCert 于 2024 年 12 月将其旗舰平台上架 Microsoft Azure Marketplace,实现了点击购买和付费使用制的扩展模式。例如,Paddy Power Betfair 在迁移到 HashiCorp Vault 即服务后,证书颁发前置作业时间从一周缩短至一小时。随着市场朝向近乎持续续期模式发展(例如苹果公司推广 47 天有效期),这些效率优势显得格外重要。那些提供自动密钥轮换、策略执行和即时吊销功能的供应商,相比传统的按数量计费的 SSL经销商,已经获得了明显的定价优势。

自签名证书的普遍性

预算有限且拥有旧有应用程式的团队仍然继续部署自签名证书,因为他们认为内部网路是可信的。然而,像戴尔的 eDellRoot 事件这样备受瞩目的事故凸显了这些证书可能被利用进行中间人攻击的风险。自签章部署对小规模的IT 部门,尤其是在新兴市场,仍然具有吸引力,因为它们可以避免使用凭证授权单位 (CA) 的费用。因此,商业 CA 提供捆绑式的发现和迁移工具包,帮助用户了解隐藏的自签名资产,并量化风险降低带来的收益。

细分市场分析

到2025年,凭证类型将占总收入的67.80%,这主要得益于浏览器在所有面向公众的Web端点强制使用SSL/TLS协定所带来的需求成长。然而,服务板块将成为成长的真正驱动力,其复合年增长率将达到20.35%,因为企业越来越重视营运效率而非单一文件的购买。随着苹果47天证书有效期的临近,手动续订流程已难以为继,促使企业转向整合发现、策略执行和机器优先颁发引擎的託管式PKI订阅服务。

服务供应商已证明其能够将平均续约时间从几天缩短至几分钟,同时也为监管机构提供审核追踪。自动化还实现了大规模撤销和关键证书洩露后的即时重新颁发。因此,分析师预测,到2030年,服务业的市场规模将超过证书类型产业,这标誌着证书颁发机构(CA)市场结构性转变的开始。这一发展趋势凸显了CA产业如今为何在平台稳健性而非单张证书价格方面展开竞争。

到2025年,大型企业将占总支出的63.70%,反映出复杂的多重云端环境需要多层信任模式。随着零信任计画的扩展,预算持续成长,进一步扩大了凭证授权单位市场的绝对规模。然而,中小企业市场的成长速度更快,复合年增长率达到18.10%。云端原生PKI解决方案透过订阅模式提供企业级功能,无需硬体安全模组和公钥专家。

预先整合的 ACME 连接器与 SaaS 计费系统结合,使Start-Ups能够在註册网域后几分钟内部署可信任证书。例如,在印尼,QRIS 数位支付框架利用标准化的 PKI 基础架构,帮助小规模企业安全地开展线上业务。这些用例表明,即使在网路安全专业知识和预算有限的地区,经济实惠且自动化的 PKI 也具有释放数位商务潜力的巨大潜力。

凭证授权单位市场报告按以下因素细分:按元件(SSL/TLS 凭证、程式码签署凭证等)、组织规模(大型企业、中小企业)、最终用户垂直行业(银行、金融服务和保险、IT 和电信、零售和电子商务等)、凭证检验等级(网域检验、组织检验等)、部署模式(本地 PKI、云端/託管 PKI)和地区。

区域分析

到2025年,北美将占全球收入的35.20%,这主要得益于成熟的网路安全预算、积极的零信任部署计画以及向3072位元RSA金钥的早期过渡。诸如白宫第14028号行政命令等联邦指令促使政府机构采用持续证书监控,从而扩大了合规工具证书颁发机构的市场规模。该地区的成长目前依赖于生命週期营运的自动化和后量子演算法先导计画,DigiCert于2025年4月宣布推出Dilithium试点证书便印证了这一点。

亚太地区以16.55%的复合年增长率成为成长最快的地区,这主要得益于无现金支付的普及、数据本地化法律的实施以及印度、越南和印尼等国政府主导的公钥基础设施(PKI)部署。印度储备银行关于数位支付信任锚的指导方针鼓励当地银行对其证书工作流程进行现代化改造。国内云端服务供应商与全球证书颁发机构(CA)合作,将承包颁发功能嵌入其电子商务平台,使数百万中小企业无需内部专业知识即可实现合规。中国大力推动自主演算法研发,帮助区域供应商扩展了相容性范围,从而实现了供应商多元化。

在欧洲,GDPR隐私法规的实施持续稳定地推进,要求资料处理者记录其加密和金钥管理实务。 eIDAS修正案进一步推动了对合格网站验证证书(QVC)的需求,在更广泛的证书颁发机构(CA)市场中开闢了一个高端细分领域。同时,中东和非洲市场随着智慧城市和开放银行计划的推进,对TLS的采用率也在不断提高,儘管基础设施的差异在某些情况下延缓了大规模自动化证书颁发。南美洲的进展缓慢但稳健,政府入口网站现在要求使用TLS,而巴西的金融科技沙盒正在利用与ACME相容的证书颁发机构快速推出新服务。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 人们对安全网路存取的意识日益增强

- 严格的监管和合规要求

- 电子商务和线上交易的激增

- 基于云端的PKI服务的成长

- DevSecOps主导的凭证自动化

- 零信任网路中对机器身分的需求

- 市场限制

- 新兴中小企业缺乏安全证书意识

- 自签名证书的普遍性

- 超大规模环境下的证书生命週期复杂性

- 关于后量子标准的监管不确定性

- 重要法规结构评估

- 价值链分析

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 关键相关人员影响评估

- 主要用例和案例研究

- 宏观经济因素对市场的影响

- 投资分析

第五章 市场区隔

- 按组件

- 证书类型

- SSL/TLS凭证

- 代码签署证书

- 安全电子邮件证书

- 身份验证/客户端凭证

- 服务

- 证书类型

- 按组织规模

- 大公司

- 中小企业

- 按最终用户行业划分

- BFSI

- 资讯科技和电信

- 零售与电子商务

- 医疗保健和生命科学

- 政府和公共部门

- 按证书检验级别

- 领域验证(DV)

- 组织验证(OV)

- 扩展检验(EV)

- 按部署模式

- 本地部署的PKI

- 云端/託管 PKI

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- ASEAN

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- DigiCert Inc.

- Sectigo Ltd.

- GoDaddy Group(Starfield Tech.)

- GlobalSign(KGZ)

- Entrust Corp.

- IdenTrust Services LLC

- Let's Encrypt/ISRG

- Actalis SpA

- SSL.com LLC

- Trustwave SecureTrust

- Network Solutions LLC

- WISeKey Intl. Holdings Ltd.

- SwissSign AG

- OneSpan Inc.

- Camerfirma SA

- Buypass AS

- QuoVadis Trustlink(Bermuda)Ltd.

- Certum(Asseco Data Systems SA)

- Amazon Trust Services

- Google Trust Services LLC

- Microsoft Azure TLS

- Oracle Cloud CA

- Cloudflare Inc.

- DigiSigner LLC

- HARICA(Hellenic Academic CA)

第七章 市场机会与未来展望

Certificate Authority market size in 2026 is estimated at USD 232.27 million, growing from 2025 value of USD 208.68 million with 2031 projections showing USD 396.58 million, growing at 11.3% CAGR over 2026-2031.

Adoption accelerated as organizations shifted from perimeter-based defenses to identity-centric models that rely on cryptographic validation for every digital interaction. Shorter certificate lifecycles, early moves toward post-quantum cryptography, and rapid zero-trust rollouts increased renewal volumes and elevated automation to a board-level priority. Browser vendors acting as de facto regulators, notably through Google Chrome's stricter root-program enforcement, reshaped supplier selection around compliance history rather than price. At the same time, cloud-managed PKI services demonstrated that outsourced expertise can deliver speed and consistency impossible to match with manual processes. Asia-Pacific's e-commerce boom, combined with government PKI mandates, placed the region on a markedly steeper growth curve than mature North American and European markets..

Global Certificate Authority Market Trends and Insights

Stringent Regulations and Compliance Mandates

Browser root-store owners enforced stricter compliance, best illustrated when Chrome announced distrust of Entrust certificates issued after October 2024. Enterprise buyers consequently evaluated CAs on their disciplinary record as much as on technical merit, a trend that continues to reshape the Certificate Authority Market. The forthcoming CA/Browser Forum rule that cuts TLS maximum validity to 47 days by March 2029 will magnify renewal volumes and favor providers equipped with real-time automation. Managed PKI vendors already highlight independent audit results to demonstrate readiness for this compliance wave. Meanwhile, regulated industries such as finance and healthcare accelerated contract renewals with Tier-1 CAs to avoid the reputational risk tied to potential future distrust events.

Expansion of Cloud-Based PKI Services

Cloud delivery became the default starting point for organizations unwilling to maintain hardware security modules, CRL distribution points, and audit controls in-house. DigiCert placed its flagship platform on Microsoft Azure Marketplace in December 2024, enabling click-through procurement and pay-as-you-go scaling. Case studies such as Paddy Power Betfair cut certificate issuance lead times from one week to one hour after migrating to HashiCorp Vault-as-a-Service. These gains matter even more as Apple's push for 47-day validity moves the market toward almost continuous renewal. Vendors differentiating on automated key-rotation, policy enforcement, and instant revocation earned clear pricing power over legacy, unit-based SSL sellers.

Prevalence of Self-Signed Certificates

Legacy applications and budget-constrained teams continued to deploy self-signed certificates, believing that interior networks remained trustworthy. High-profile failures, such as Dell's eDellRoot incident, illustrated how these certificates can be exploited for man-in-the-middle attacks. Because self-signed deployments avoid CA fees, they still appeal to small IT departments, especially in emerging markets. Commercial CAs, therefore, bundled discovery and migration toolkits to expose hidden self-signed assets and calculate risk savings in monetary terms.

Other drivers and restraints analyzed in the detailed report include:

- DevSecOps-Led Certificate Automation

- Machine-Identity Demand in Zero-Trust Networks

- Regulatory Uncertainty on Post-Quantum Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Certificate Types retained 67.80% of 2025 revenue, anchored by SSL/TLS demand that browsers enforce for every public web endpoint. However, Services generated the momentum, expanding at 20.35% CAGR as customers realized that operational excellence matters more than purchasing individual files. With Apple's 47-day validity on the horizon, manual renewal processes became untenable, pushing enterprises toward managed PKI subscriptions that bundle discovery, policy enforcement, and machine-first issuance engines.

Services providers showed they could shrink mean-time-to-renewal from days to minutes while supplying audit trails for regulators. Automation also enabled bulk revocation and immediate re-issuance during key-compromise events. As a result, analysts projected Services to surpass Certificate Types by value before 2030, marking a structural shift in the certificate authority market. This evolution underscores why the certificate authority industry now competes on platform robustness rather than on certificate unit price.

Large Enterprises generated 63.70% of total spending in 2025, reflecting complex multi-cloud estates that require layered trust models. Their budgets continued to climb as zero-trust initiatives expanded, reinforcing the certificate authority market size in absolute terms. Yet the SME segment exhibited the steeper trajectory at an 18.10% CAGR. Cloud-native PKI offerings delivered enterprise-grade functionality via subscription, removing the need for hardware security modules or public-key specialists.

SaaS invoicing and pre-integrated ACME connectors allowed start-ups to deploy trusted certificates within minutes of domain registration. In Indonesia, for example, QRIS digital payment frameworks used standardized PKI rails to bring micro-merchants online securely. These use cases validated the idea that affordable, automated PKI can unlock digital commerce in regions where cybersecurity expertise and budgets remain limited.

The Certificate Authority Market Report is Segmented by Component (SSL/TLS Certificates, Code-Signing Certificates, and More), Organization Size (Large Enterprises, and SMEs), End-User Vertical (BFSI, IT and Telecom, Retail and E-Commerce, and More), Certificate Validation Level (Domain Validation, Organization Validation, and More), Deployment Model (On-Premise PKI, and Cloud/Managed PKI), and Geography.

Geography Analysis

North America retained 35.20% of global revenue in 2025 on the back of mature cybersecurity budgets, aggressive zero-trust roadmaps, and early migration to 3072-bit RSA keys. Federal directives such as the White House Executive Order 14028 prompted agencies to adopt continuous certificate monitoring, reinforcing the certificate authority market size for compliance tooling. The region's growth now hinges on automating lifecycle tasks and pilot projects for post-quantum algorithms, evidenced by DigiCert's Dilithium test-certificates released in April 2025.

Asia-Pacific posted the swiftest CAGR at 16.55%, sparked by cashless-payment expansion, data-localization statutes, and government PKI rollouts in India, Vietnam, and Indonesia. The Reserve Bank of India's guidelines for digital-payment trust anchors spurred local banks to modernize certificate workflows. Domestic cloud providers partnered with global CAs to embed turnkey issuance into e-commerce platforms, allowing millions of SMEs to comply without in-house expertise. China's push for indigenous algorithms also encouraged regional vendors to expand compatibility matrices, broadening supplier variety.

Europe maintained steady momentum under GDPR's privacy regime, where data processors must document encryption and key-management practices. The eIDAS revision additionally drives demand for qualified website authentication certificates, creating a premium niche within the broader certificate authority market. Meanwhile, Middle East and Africa markets showed rising adoption tied to smart-city and open-banking projects, though uneven infrastructure sometimes slowed large-scale automated issuance. South America's trajectory remained moderate but positive; governments there increasingly required TLS on public-sector portals, while fintech sandboxes in Brazil leveraged ACME-compatible issuers to launch new services rapidly.

- DigiCert Inc.

- Sectigo Ltd.

- GoDaddy Group (Starfield Tech.)

- GlobalSign (KGZ)

- Entrust Corp.

- IdenTrust Services LLC

- Let's Encrypt / ISRG

- Actalis S.p.A

- SSL.com LLC

- Trustwave SecureTrust

- Network Solutions LLC

- WISeKey Intl. Holdings Ltd.

- SwissSign AG

- OneSpan Inc.

- Camerfirma SA

- Buypass AS

- QuoVadis Trustlink (Bermuda) Ltd.

- Certum (Asseco Data Systems SA)

- Amazon Trust Services

- Google Trust Services LLC

- Microsoft Azure TLS

- Oracle Cloud CA

- Cloudflare Inc.

- DigiSigner LLC

- HARICA (Hellenic Academic CA)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing awareness of secure web access

- 4.2.2 Stringent regulations and compliance mandates

- 4.2.3 Surge in e-commerce and online transactions

- 4.2.4 Expansion of cloud-based PKI services

- 4.2.5 DevSecOps-led certificate automation

- 4.2.6 Machine-identity demand in zero-trust networks

- 4.3 Market Restraints

- 4.3.1 Low security-certificate awareness in emerging SMBs

- 4.3.2 Prevalence of self-signed certificates

- 4.3.3 Certificate lifecycle complexity at hyperscale

- 4.3.4 Regulatory uncertainty on post-quantum standards

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Certificate Types

- 5.1.1.1 SSL/TLS Certificates

- 5.1.1.2 Code-Signing Certificates

- 5.1.1.3 Secure Email Certificates

- 5.1.1.4 Authentication/Client Certificates

- 5.1.2 Services

- 5.1.1 Certificate Types

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises (SMEs)

- 5.3 By End-user Vertical

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Retail and E-commerce

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Government and Public Sector

- 5.4 By Certificate Validation Level

- 5.4.1 Domain Validation (DV)

- 5.4.2 Organization Validation (OV)

- 5.4.3 Extended Validation (EV)

- 5.5 By Deployment Model

- 5.5.1 On-premise PKI

- 5.5.2 Cloud/Managed PKI

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 DigiCert Inc.

- 6.4.2 Sectigo Ltd.

- 6.4.3 GoDaddy Group (Starfield Tech.)

- 6.4.4 GlobalSign (KGZ)

- 6.4.5 Entrust Corp.

- 6.4.6 IdenTrust Services LLC

- 6.4.7 Let's Encrypt / ISRG

- 6.4.8 Actalis S.p.A

- 6.4.9 SSL.com LLC

- 6.4.10 Trustwave SecureTrust

- 6.4.11 Network Solutions LLC

- 6.4.12 WISeKey Intl. Holdings Ltd.

- 6.4.13 SwissSign AG

- 6.4.14 OneSpan Inc.

- 6.4.15 Camerfirma SA

- 6.4.16 Buypass AS

- 6.4.17 QuoVadis Trustlink (Bermuda) Ltd.

- 6.4.18 Certum (Asseco Data Systems SA)

- 6.4.19 Amazon Trust Services

- 6.4.20 Google Trust Services LLC

- 6.4.21 Microsoft Azure TLS

- 6.4.22 Oracle Cloud CA

- 6.4.23 Cloudflare Inc.

- 6.4.24 DigiSigner LLC

- 6.4.25 HARICA (Hellenic Academic CA)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment