|

市场调查报告书

商品编码

1940699

英国快递、速递和小包裹(CEP) 市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)United Kingdom Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

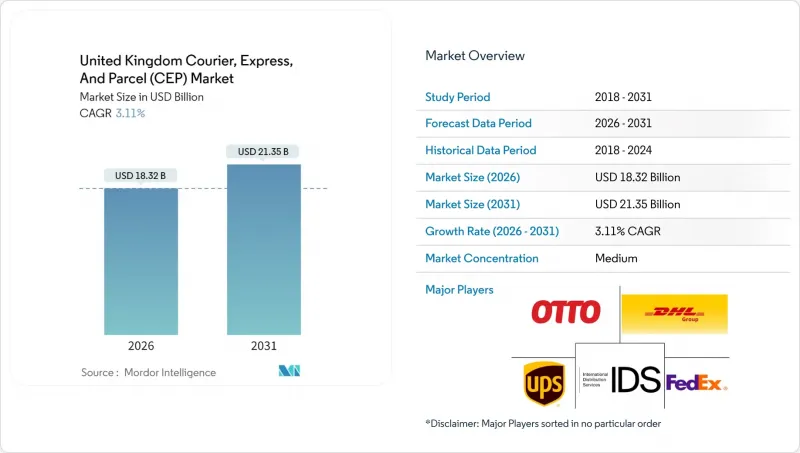

2025年英国快递小包裹(CEP)市值为177.7亿美元,预计2031年将达到213.5亿美元,高于2026年的183.2亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.11%。

这种温和的扩张显示市场环境竞争日益成熟,技术主导的效率提升、自动化和网路优化已发展到足以影响盈利的阶段,而不仅仅是表面上的销售成长。国内配送仍占据主导地位,但随着英国脱欧后贸易协定的稳定,跨境配送量正在復苏。同时,以消费者为中心的电子商务正在重新定义服务组合和配送速度预期。竞争策略强调数据驱动的路线规划、轻资产伙伴关係以及旨在提高最后一公里配送密度的定向收购。 2024 年《数位市场、竞争和消费者法案》加强了法律规范,增加了合规成本,但也创建了一个清晰的营运框架,强调透明度和消费者保护。

英国快递小包裹(CEP) 市场趋势与洞察

电子商务渗透率快速成长

线上零售小包裹量持续成长,消费者对更快、可追踪、更灵活的配送服务提出了更高的期望。能够保证准时时限的业者获得了丰厚的利润,而依赖标准服务的业者则面临利润压力。专门处理易碎品或高价值物品的物流网络正利用差异化服务赢得顾客忠诚度。同时,点对点转售平台正在扩大绕过传统实体店供应链的货运量,从而扩大了大型承运商提供的储物柜网路和无标籤配送服务的基本客群。这些因素共同推动了对路线规划软体和自动化分类系统的投资,以支持盈利、高速的最后一公里配送业务。

跨境电子商务的扩张

可预测的海关规则的重建重振了国际小包裹流通,尤其是欧盟境内的包裹流通。拥有海关专业知识和多语言支援的货运代理公司正在缩短清关週期,并透过人工智慧驱动的分类引擎等数据丰富的预申报工具来扩大市场份额。根据温莎框架,北爱尔兰享有独特的双市场结构,允许其在英国和欧盟范围内提案服务,而无需重复提交文件。消费者对从欧洲大陆企业订购商品信心的恢復,提高了货运价值密度,并增加了对限时送达的需求。

司机短缺和工资上涨

该行业持续面临人才短缺的挑战,这推高了人事费用并威胁到准点率。薪资调整空间有限的独立营运商正面临盈利压力,而大型运输网路则透过实施留任奖金、车载安全技术和职业发展路径来稳定离职率。一些运输公司已开始试验众包车辆和自动驾驶配送,以减少对传统大型货车牌照的依赖。人事费用的上涨也推高了保险和培训费用,加剧了季节性需求高峰期的成本压力。

细分市场分析

製造业在可预测的生产计画和零件采购流程的驱动下,将在2025年维持33.27%的市场占有率。然而,随着全通路零售商将履约和最后一公里配送外包,电子商务将成为最突出的成长领域,2026年至2031年的复合年增长率将达到3.41%。医疗保健物流也呈现强劲成长势头,这主要得益于居家临床试验和直接送药给患者的模式,这些都需要严格的温度控制和监管链通讯协定。

金融服务业对安全文件运输的需求依然旺盛,但由于数位化,实体运输量正在逐步下降。工业用品和原料的配送仰赖能够处理危险物品和受管制货物的承运商,这提升了英国国内快递、速递和小包裹(CEP) 市场中专业认证的价值。

从2026年到2031年,国际物流将以3.24%的复合年增长率成长,显示稳定的海关框架正在重振英国与欧洲大陆之间的贸易往来。将数位化海关预清关功能整合到预订平台的快递业者,正在打造无缝的跨境购物体验,并满足消费者对限时送达服务的需求。在电子商务和优先考虑区域供应链韧性的回流措施的推动下,到2025年,国内运输仍将占英国快递、速递和小包裹(CEP)市场份额的64.62%。

英国快递、速递和小包裹(CEP) 市场的规模正受惠于业务量的多元化成长,平台业者不断拓展国际消费群,英国消费者也扩大了采购选择。拥有多语种客服支援、透明的关税计算工具和便捷的退货流程的营运商正将这种多元化转化为盈利的重复业务。北爱尔兰凭藉其更便捷的欧盟通道,正崛起为物流桥头堡,使承运商能够将其枢纽迁至此处,从而高效覆盖英国当地和欧洲市场。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 人口统计数据

- 按经济活动分類的GDP分配

- 按经济活动分類的GDP成长

- 通货膨胀

- 经济表现及概况

- 电子商务产业的趋势

- 製造业趋势

- 运输和仓储业GDP

- 出口趋势

- 进口趋势

- 燃油价格

- 物流绩效

- 基础设施

- 法律规范

- 价值炼和通路分析

- 市场驱动因素

- 电子商务渗透率快速成长

- 跨境电子商务的扩张

- 引入自动化和即时追踪系统

- 车队电气化奖励

- 微型仓配快速电商的兴起

- 室内/室外储物柜生态系统

- 市场限制

- 司机短缺和工资上涨

- 燃料和能源价格波动

- 都市区拥挤/超低排放区(ULEZ)收费区

- 由于土地短缺导致枢纽容量受限

- 市场创新

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 目的地

- 国内的

- 国际的

- 配送速度

- 快递

- 非快递

- 模型

- B2B

- B2C

- C2C

- 运输重量

- 重型货物

- 轻型货物

- 中等重量货物

- 交通工具

- 航空

- 陆上

- 其他的

- 终端用户产业

- 电子商务

- 金融服务(BFSI)

- 卫生保健

- 製造业

- 一级产业

- 批发零售(线下)

- 其他的

第六章 竞争情势

- 市场集中度

- 重大策略倡议

- 市占率分析

- 公司简介

- APC Overnight

- DHL Group

- FedEx

- GEODIS

- International Distributions Services(including Royal Mail)

- La Poste Group

- Otto Group(including The Hermes Group)

- Rapid Parcel

- United Parcel Service(UPS)

- Yodel

第七章 市场机会与未来展望

The United Kingdom courier, express, and parcel market was valued at USD 17.77 billion in 2025 and estimated to grow from USD 18.32 billion in 2026 to reach USD 21.35 billion by 2031, at a CAGR of 3.11% during the forecast period (2026-2031).

This measured expansion indicates a mature competitive arena in which technology-led efficiency, automation, and network optimization now influence profitability more than headline volume growth. Domestic deliveries still dominate activity, but cross-border volumes are rebounding as post-Brexit trade protocols stabilize, while consumer-centric e-commerce is redefining service mix and delivery speed expectations. Competitive strategies emphasize data-driven routing, asset-light partnerships, and targeted acquisitions that deepen last-mile density. Regulatory oversight has intensified under the Digital Markets, Competition and Consumers Act 2024, sharpening compliance costs but also creating a clearer operating framework that rewards transparency and consumer protection.

United Kingdom Courier, Express, And Parcel (CEP) Market Trends and Insights

E-commerce Penetration Surge

Online retail continues to lift parcel volumes, reshaping service expectations toward faster, traceable, and flexible deliveries. Operators able to guarantee narrow time windows capture premium yields, while those relying on standard services face margin pressure. Specialist networks that handle fragile or high-value items leverage their service differentiation to win customer loyalty. At the same time, peer-to-peer resale platforms are scaling shipments that bypass traditional store-based supply chains, broadening the customer base for locker networks and label-free shipping options offered by major carriers. These forces collectively push investment into routing software and automated sortation systems that underpin profitable high-velocity last-mile operations.

Cross-Border E-commerce Expansion

The re-establishment of predictable customs rules has reignited international parcel flows, especially toward EU destinations. Carriers with customs brokerage depth and multilingual support are now widening market share by shortening clearance cycles through data-rich pre-declaration tools exemplified by AI-enabled classification engines. Northern Ireland enjoys a unique dual-market profile under the Windsor Framework, encouraging service propositions that span Great Britain and the EU without duplicative paperwork. As shoppers regain confidence in ordering from continental merchants, shipment value density rises, favoring time-definite express products.

Driver Shortages and Wage Inflation

The industry confronts persistent recruitment gaps that elevate labor costs and threaten on-time performance. Independent operators with limited wage flexibility see profitability squeezed, whereas larger networks deploy retention bonuses, in-cab safety tech, and career pathways to stabilize turnover. Some carriers are piloting crowd-sourced fleets and autonomous delivery pilots to reduce reliance on traditional HGV licenses. Rising payroll also inflates insurance premiums and training overheads, compounding cost pressure during seasonal surges.

Other drivers and restraints analyzed in the detailed report include:

- Automation and Real-Time Tracking Roll-Out

- Rise of Micro-Fulfillment Q-commerce

- Urban Congestion and ULEZ Charging Zones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing maintains a 33.27% share in 2025, leveraging predictable production schedules and inbound component flows. However, e-commerce is the brightest growth spot at 3.41% CAGR between 2026-2031 as omnichannel retailers outsource fulfillment and last-mile delivery. Healthcare logistics registers brisk momentum, supported by home-based clinical trials and direct-to-patient pharmaceutical deliveries that demand strict temperature and chain-of-custody protocols.

Financial services continue to require secure documentation transport, but digitalization is gradually trimming physical shipment volumes. Industrial and raw-material flows depend on carriers equipped to handle hazardous or regulated goods, reinforcing the value of specialized certifications inside the United Kingdom courier, express, and parcel market.

International values, expanding at a 3.24% CAGR between 2026-2031, illustrate how stabilized customs frameworks are reinvigorating trade flows between the United Kingdom and continental Europe. Express carriers that integrate digital customs pre-clearance into booking platforms facilitate seamless cross-border shopping experiences, thereby capturing demand for time-definite delivery. Domestic traffic still anchors 64.62% of the United Kingdom courier, express, and parcel market share in 2025, buoyed by e-commerce and reshoring initiatives that prioritize local supply chain resilience.

The United Kingdom courier, express, and parcel market size benefits from volume diversification as platform-based merchants tap foreign consumer bases and U.K. shoppers broaden sourcing choices. Operators with multilingual support desks, transparent duty calculators, and consumer-friendly returns processes convert these flows into profitable repeat business. Northern Ireland, enjoying streamlined EU access, is emerging as a logistics bridgehead, enabling carriers to reposition hubs that serve both Great Britain and Europe efficiently.

The United Kingdom Courier, Express, and Parcel (CEP) Market Report is Segmented by End User Industry (E-Commerce, Manufacturing, and More), Destination (Domestic and International), Speed of Delivery (Express and Non-Express), Shipment Weight (Heavy Weight Shipments, and More), Mode of Transport (Air, Road, and Others), and Model (Business-To-Business, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- APC Overnight

- DHL Group

- FedEx

- GEODIS

- International Distributions Services (including Royal Mail)

- La Poste Group

- Otto Group (including The Hermes Group)

- Rapid Parcel

- United Parcel Service (UPS)

- Yodel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 E-Commerce Penetration Surge

- 4.15.2 Cross-Border E-Commerce Expansion

- 4.15.3 Automation and Real-Time Tracking Roll-Out

- 4.15.4 Fleet Electrification Incentives

- 4.15.5 Rise of Micro-Fulfilment Q-Commerce

- 4.15.6 Indoor/Out-of-Home Locker Ecosystems

- 4.16 Market Restraints

- 4.16.1 Driver Shortages and Wage Inflation

- 4.16.2 Volatile Fuel and Energy Prices

- 4.16.3 Urban Congestion/ULEZ Charging Zones

- 4.16.4 Land-Scarce Hub Capacity Constraints

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 APC Overnight

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 GEODIS

- 6.4.5 International Distributions Services (including Royal Mail)

- 6.4.6 La Poste Group

- 6.4.7 Otto Group (including The Hermes Group)

- 6.4.8 Rapid Parcel

- 6.4.9 United Parcel Service (UPS)

- 6.4.10 Yodel

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球宅配、包裹及小包裹市场:2026-2032年市场预测(按类型、服务类型、货物类型、目的地、配送速度、货量、运输方式及最终用户划分)

全球宅配、包裹及小包裹市场:2026-2032年市场预测(按类型、服务类型、货物类型、目的地、配送速度、货量、运输方式及最终用户划分) 2026年全球包裹递送服务市场报告2026年全球宅配与小包裹递送市场报告2026年全球宅配服务市场报告2026年全球快递与信差市场报告2026年全球宅配市场报告2026年全球当日配送服务市场报告2026年全球超当地语系化配送应用市场报告

2026年全球包裹递送服务市场报告2026年全球宅配与小包裹递送市场报告2026年全球宅配服务市场报告2026年全球快递与信差市场报告2026年全球宅配市场报告2026年全球当日配送服务市场报告2026年全球超当地语系化配送应用市场报告 2026-2030年全球宅配包裹(CEP)市场

2026-2030年全球宅配包裹(CEP)市场 宅配、包裹及小包裹市场报告:按服务类型、目的地、物品、最终用途行业和地区划分(2026-2034 年)

宅配、包裹及小包裹市场报告:按服务类型、目的地、物品、最终用途行业和地区划分(2026-2034 年)