|

市场调查报告书

商品编码

1940709

超音波流量计:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Ultrasonic Flow Meters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

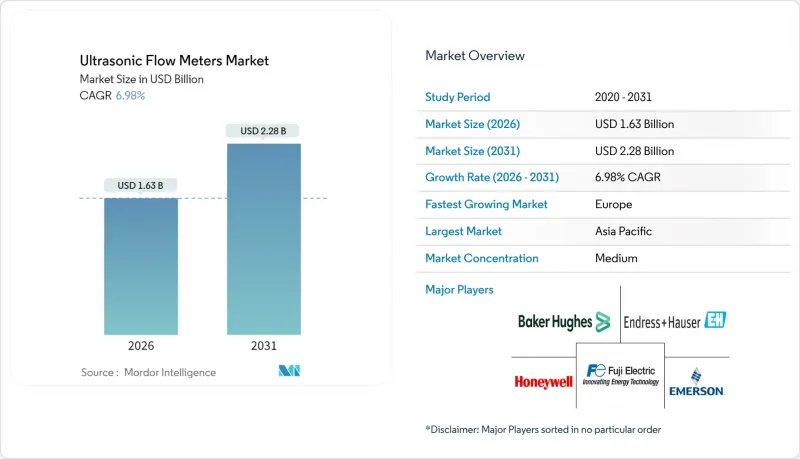

预计到 2026 年,超音波流量计市场规模将达到 16.3 亿美元,高于 2025 年的 15.2 亿美元。

预计到 2031 年将达到 22.8 亿美元,2026 年至 2031 年的复合年增长率为 6.98%。

大口径天然气管道中计量式流量计的广泛应用、老旧水网对夹装式流量计的维修需求,以及氢能基础设施的早期投资,共同推动了整个製程工业近两位数的成长。与差压式和涡轮式流量计相比,零压降、可进行预测性维护且整合工业物联网 (IIoT) 的超音波流量计更受营运商青睐,因为它们能够降低生命週期内的运行成本。在环境法规要求严格控制流量的领域,例如化学工业的零液体排放要求和市政供水系统的洩漏控制计划,超音波流量计的应用正在加速推进。竞争优势日益凸显,企业越来越注重边缘人工智慧诊断和多路径冗余等技术,这些技术即使在严苛的贸易计量条件下也能维持 ±0.15% 的重复性。

全球超音波流量计市场趋势及洞察

加速大直径天然气管道计量级超音波流量计的过渡

由于超音波流量计能够消除压降损失,降低压缩机能耗高达15%,且使用寿命长达20年,维护量极低,管道运营商正逐步淘汰涡轮流量计。多通道设计可满足API标准的精度要求,并支援使用小体积探针进行现场检验,从而最大限度地减少校准停机时间。这种应用在北美页岩气运输路线和中东出口管道中尤其明显,因为这些地区输送量的波动需要更宽的雷诺数容差范围。

水资源紧张地区对非侵入式夹装流量计的快速维修需求

非侵入式夹装式计量装置使公共产业无需切割预力混凝土圆柱形管道即可安装计量设备,从而降低灾难性破裂的风险并精确定位洩漏点。在新兴经济体中,洩漏造成的处理水损失占20%至30%。市政计划可在数週内安装数百个计量表,并提供特定区域的计量分析,以优化压力并减少无收益水。

与传统差压/涡轮流量计相比,初始资本投资较高。

超音波的安装成本(包括试运行和培训)是差压式检测方法的3到5倍,儘管其在整个生命週期内具有潜在的运营成本优势,但对于预算小规模的市政机构而言,这仍然是一个挑战。资金筹措限制减缓了发展中地区先进诊断技术的应用,因为在这些地区,功能性往往比先进的诊断技术更为重要。

细分市场分析

预计到2025年,在线连续超音波流量计将占据65.60%的市场。同时,夹装式流量计预计将以8.18%的复合年增长率成长,反映出亚太地区公共产业维修专案的不断扩大。夹装式流量计受惠于WaveInjector感测器外壳,可承受-200°C至+630°C的製程温度。非侵入式设备正在加速工业工厂对紧急洩漏检测和临时审核的需求,以避免生产停机。

第二代耦合垫和自动化安装钻机将安装时间缩短了一半,在停水成本高于水錶价格的环境中,显着提升了经济优势。试点智慧水务计画的公共产业在安装夹式流量计后的几个月内,洩漏率就有所降低,这加快了投资回报,并进一步拓展了超音波流量计在资金受限环境下的市场。

预计到2025年,时差式流量计将占据82.10%的市场份额,并在2031年之前以8.36%的复合年增长率成长。其测量声速的功能支持成分监测,这对于氢气混合至关重要,并且随着脱碳进程的推进,其价值提案也在不断提升。即使在温度波动的环境下,利用机器学习进行剖面校正也能维持±0.5%的精确度。

另一方面,多普勒装置的精度有限,不适用于含污流体环境。对于多相管道,单一技术的限制显而易见,因此,结合多普勒和飞行时间测量的混合平台正在兴起。采用可切换原理的模组化电子设备使操作人员能够标准化使用单一发送器系列,从而减少各种应用场景下的库存。

区域分析

到2025年,亚太地区将占全球营收的41.25%,这主要得益于中国「一带一路」沿线计划和印度「智慧城市计画」对高精度测量的迫切需求。日本和韩国的本土製造商正透过物联网赋能的变送器和温度补偿感测器来增强自身竞争力,从而提升该地区的供应安全。各国政府正将基础设施奖励策略放在污水再利用上,这推动了市政计划中超音波流量计的应用。

预计欧洲将以10.11%的复合年增长率成长,这主要得益于欧盟政策推动的氢气管道维修和对计量指令更严格的遵守。德国一家化工企业正在其製程强化项目中应用超音波流量计,以降低每吨产品的能耗。荷兰正在加速推进其氢气注入试点项目,该项目需要专有的品质调整技术。区域供应商正利用垂直整合,将测量设备与云端分析结合,以满足严格的永续性审核。

北美地区持续保持个位数温和成长,这主要得益于页岩气交易计量升级以及西部供水事业地区各州的洩漏预防计划。联邦基础设施立法正在津贴采用智慧水系统,该系统使用夹装式水錶安装在老旧的球墨铸铁管道上。南美和中东/非洲是新兴的需求区域,但DN1000以上规格管道的认证校准实验室数量有限,导致新管道的审批流程延误。为此,供应商正在透过部署行动服务供应商和远端支援中心来降低服务门槛。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 宏观经济因素的影响

- 市场驱动因素

- 加速向大口径天然气管道交易型超音波流量计过渡

- 缺水地区对维修非侵入式夹式水錶的需求迅速成长

- 与氢气相容的超音波设计在能源转型中带来先发优势

- 边缘人工智慧自诊断技术有助于公共产业降低营运成本并促进预测性维护

- 推动化学工业精准流量控制的因素:强制性零液体排放(ZLD)政策

- 整合到智慧泵中的超音波发送器扩大了可触及的OEM市场

- 市场限制

- 与传统差压式流量计和涡轮流量计相比,初始资本投资成本较高。

- 在不使用高阶讯号处理技术的情况下,多相流和浆料环境中的精度漂移问题

- 新兴地区缺乏经认证的DN1000以上等级校准实验室

- 关键基础设施中工业物联网连接电錶的网路安全隐患

- 产业供应链分析

- 监管环境

- 科技展望(物联网相容性、氢能相容性、人工智慧)

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过安装方法

- 夹式

- 在线连续

- 透过测量技术

- 交通时刻表

- 多普勒

- 混合/多路径

- 按最终用户行业划分

- 石油和天然气

- 供水和污水处理

- 化工和石油化工

- 工业领域(食品饮料、航太、汽车)

- 其他产业(生命科学、采矿和金属)

- 按路线数量

- 单一途径

- 多轮传球(3轮、4轮、5轮以上)

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Baker Hughes Company

- Endress+Hauser Group Services AG

- Fuji Electric Co., Ltd.

- Honeywell International Inc.

- Emerson Electric Co.

- ABB Ltd.

- Aichi Tokei Denki Co., Ltd.

- Apator SA

- Arad Group

- Badger Meter Inc.

- Bronkhorst High-Tech BV

- Diehl Metering GmbH

- FLEXIM Instruments GmbH

- Itron Inc.

- Kamstrup A/S

- KOBOLD Messring GmbH

- KROHNE Group

- Landis+Gyr AG

- Mueller Systems LLC

- Neptune Technology Group Inc.

- Omega Engineering Inc.

- SICK AG

- Siemens AG

- Sensus USA Inc.

- WEIHAI Ploumeter Co., Ltd.

第七章 市场机会与未来展望

Ultrasonic flow meters market size in 2026 is estimated at USD 1.63 billion, growing from 2025 value of USD 1.52 billion with 2031 projections showing USD 2.28 billion, growing at 6.98% CAGR over 2026-2031.

The growing deployment of custody-transfer-grade meters in large-diameter gas pipelines, retrofit demand for clamp-on devices in aging water networks, and early-stage investments in hydrogen infrastructure sustain near-double-digit demand across the process industries. Operators favor ultrasonic designs for zero pressure loss, predictive maintenance, and IIoT integration, which reduce lifetime operating expenditure compared with differential-pressure or turbine meters. Adoption accelerates where environmental compliance drives high-accuracy flow control, such as zero-liquid-discharge mandates in chemical processing and leakage-reduction programs in municipal water systems. Competitive differentiation is increasingly centered on edge-AI diagnostics and multi-path redundancy, which maintain +-0.15% repeatability in demanding custody-transfer conditions.

Global Ultrasonic Flow Meters Market Trends and Insights

Accelerated shift to custody-transfer-grade ultrasonic meters in large-diameter gas pipelines

Pipeline operators have begun phasing out turbine meters because ultrasonic units eliminate pressure-drop penalties, reducing compressor energy consumption by up to 15% while offering 20-year lifetimes with minimal maintenance. Multi-path designs now deliver API-compliant accuracy and enable field verification through small-volume provers, limiting downtime for calibration. Adoption is most visible in North American shale gas corridors and Middle Eastern export pipelines, where throughput variability requires wide Reynolds-number tolerance.

Rapid retrofit demand for non-invasive clamp-on meters in water-stress hotspots

Non-invasive clamp-on devices enable utilities to instrument prestressed concrete cylinder pipelines without cutting, thereby mitigating the risk of catastrophic failure while identifying leaks responsible for 20-30% of treated-water losses in emerging economies. Municipal projects can deploy hundreds of meters in weeks, enabling district-metered-area analytics that optimize pressure and drive down non-revenue water.

High initial CAPEX vs. legacy DP/turbine meters

Ultrasonic installations cost three to five times more than differential-pressure alternatives once commissioning and training are included, challenging smaller municipal budgets despite lifecycle OPEX savings. Financing constraints slow the adoption of advanced diagnostics in developing regions, where functionality often takes precedence over advanced diagnostics.

Other drivers and restraints analyzed in the detailed report include:

- Hydrogen-ready ultrasonic designs enable early-mover advantage in energy transition

- Edge-AI self-diagnostics cut OPEX for utilities and boost predictive maintenance adoption

- Accuracy drift in multiphase/slurry service without advanced signal conditioning

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In-line designs accounted for 65.60% of the ultrasonic flow meters market share in 2025. Clamp-on units, however, are projected to register an 8.18% CAGR, reflecting expanding retrofit programs across APAC utilities. The clamp-on segment benefits from WaveInjector transducer housings that can tolerate process ranges of -200 °C to +630 °C. As non-invasive devices avoid production outages, demand accelerates for emergency leak surveys and temporary audits in industrial plants.

Second-generation coupling pads and automated mounting rigs halve installation time, reinforcing economic advantages where shutdown costs exceed instrument price. Utilities piloting smart-water programs confirm leak-rate reductions within months of clamp-on deployments, supporting rapid investment payback and further penetration of the ultrasonic flow meters market in constrained capital environments.

Transit-time units held an 82.10% share in 2025 and are set to grow at an 8.36% CAGR through 2031. Their capability to capture sonic velocity supports composition monitoring needed for hydrogen-gas blends, elevating their value proposition as decarbonization momentum builds. Machine-learning-driven profile correction now sustains +-0.5% accuracy even under variable temperature regimes.

Doppler devices remain confined to dirty-fluid contexts due to their lower precision, while hybrid platforms combining Doppler and transit-time measurements are emerging for multiphase pipelines where shortfalls of single-method approaches are apparent. Modular electronics that switch between principles enable operators to standardize on one transmitter family, reducing inventory even as application diversity expands.

The Ultrasonic Flow Meters Market Report is Segmented by Mounting Method (Clamp-On, In-Line), Measurement Technology (Transit-Time, Doppler, Hybrid/Multipath), End-User Industry (Oil and Gas, Water and Wastewater, Chemical and Petrochemical, Industrial, Other Industries), Number of Paths (Single-Path, Multi-Path), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 41.25% of global revenue in 2025, fueled by China's Belt and Road pipeline projects and India's Smart Cities Mission that mandates high-accuracy metering. Local producers in Japan and South Korea enhance competitiveness through IoT-ready transmitters and temperature-compensating transducers, reinforcing regional supply security. Governments channel infrastructure stimulus toward wastewater reuse, thereby elevating the adoption of ultrasonic flow meters in municipal projects.

Europe is projected to expand at a 10.11% CAGR as EU policy drives hydrogen-ready pipeline retrofits and rigorous conformance to the Measuring Instruments Directive. Germany's chemical heartland embeds ultrasonic meters within process intensification programs to reduce energy consumption per ton of output, while the Netherlands accelerates hydrogen injection pilots that require custody-grade mass reconciliation. Regional suppliers leverage vertical integration, combining instruments with cloud analytics to satisfy stringent sustainability audits.

North America sustains mid-single-digit growth, anchored by shale gas custody-transfer upgrades and water utility leakage projects in drought-prone western states. Federal infrastructure bills subsidize smart-water deployments that favor clamp-on meters for aging ductile-iron mains. South America and the Middle East-Africa represent emerging demand pockets, though limited accredited calibration facilities above DN 1000 slow some greenfield pipeline approvals. Suppliers counter by deploying mobile providers and remote support hubs, easing service barriers.

- Baker Hughes Company

- Endress+Hauser Group Services AG

- Fuji Electric Co., Ltd.

- Honeywell International Inc.

- Emerson Electric Co.

- ABB Ltd.

- Aichi Tokei Denki Co., Ltd.

- Apator SA

- Arad Group

- Badger Meter Inc.

- Bronkhorst High-Tech BV

- Diehl Metering GmbH

- FLEXIM Instruments GmbH

- Itron Inc.

- Kamstrup A/S

- KOBOLD Messring GmbH

- KROHNE Group

- Landis+Gyr AG

- Mueller Systems LLC

- Neptune Technology Group Inc.

- Omega Engineering Inc.

- SICK AG

- Siemens AG

- Sensus USA Inc.

- WEIHAI Ploumeter Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Accelerated shift to custody-transfer-grade ultrasonic meters in large-diameter gas pipelines

- 4.3.2 Rapid retrofit demand for non-invasive clamp-on meters in water-stress hotspots

- 4.3.3 Hydrogen-ready ultrasonic designs enable early-mover advantage in energy transition

- 4.3.4 Edge-AI self-diagnostics cut OPEX for utilities and boost predictive maintenance adoption

- 4.3.5 Mandatory zero-liquid-discharge policies push high-accuracy flow control in chemicals

- 4.3.6 OEM-embedded ultrasonic transmitters in smart pumps expand addressable OEM market

- 4.4 Market Restraints

- 4.4.1 High initial CAPEX vs. legacy DP/turbine meters

- 4.4.2 Accuracy drift in multiphase / slurry service without advanced signal conditioning

- 4.4.3 Scarcity of accredited calibration labs above DN 1000 in emerging regions

- 4.4.4 Cyber-security concerns over IIoT-connected meters in critical infrastructure

- 4.5 Industry Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook (IoT-enabled, hydrogen-ready, AI)

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mounting Method

- 5.1.1 Clamp-on

- 5.1.2 In-line

- 5.2 By Measurement Technology

- 5.2.1 Transit-time

- 5.2.2 Doppler

- 5.2.3 Hybrid / Multipath

- 5.3 By End-User Industry

- 5.3.1 Oil and Gas

- 5.3.2 Water and Wastewater

- 5.3.3 Chemical and Petrochemical

- 5.3.4 Industrial (F&B, Aerospace, Automotive)

- 5.3.5 Other Industries (Life Sciences, Mining and Metals)

- 5.4 By Number of Paths

- 5.4.1 Single-path

- 5.4.2 Multi-path (3-Path, 4-Path, 5+-Path)

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Baker Hughes Company

- 6.4.2 Endress+Hauser Group Services AG

- 6.4.3 Fuji Electric Co., Ltd.

- 6.4.4 Honeywell International Inc.

- 6.4.5 Emerson Electric Co.

- 6.4.6 ABB Ltd.

- 6.4.7 Aichi Tokei Denki Co., Ltd.

- 6.4.8 Apator SA

- 6.4.9 Arad Group

- 6.4.10 Badger Meter Inc.

- 6.4.11 Bronkhorst High-Tech BV

- 6.4.12 Diehl Metering GmbH

- 6.4.13 FLEXIM Instruments GmbH

- 6.4.14 Itron Inc.

- 6.4.15 Kamstrup A/S

- 6.4.16 KOBOLD Messring GmbH

- 6.4.17 KROHNE Group

- 6.4.18 Landis+Gyr AG

- 6.4.19 Mueller Systems LLC

- 6.4.20 Neptune Technology Group Inc.

- 6.4.21 Omega Engineering Inc.

- 6.4.22 SICK AG

- 6.4.23 Siemens AG

- 6.4.24 Sensus USA Inc.

- 6.4.25 WEIHAI Ploumeter Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

超音波流量计市场:按安装方式、测量技术、最终用户和应用划分-全球市场预测(2026-2032 年)超音波油罐检测器市场按安装类型、产品和最终用户划分,全球预测(2026-2032年)

超音波流量计市场:按安装方式、测量技术、最终用户和应用划分-全球市场预测(2026-2032 年)超音波油罐检测器市场按安装类型、产品和最终用户划分,全球预测(2026-2032年) 超音波流量计市场 - 全球产业规模、份额、趋势、机会及预测(按感测器类型、技术、终端用户产业、地区和竞争格局划分,2021-2031年)

超音波流量计市场 - 全球产业规模、份额、趋势、机会及预测(按感测器类型、技术、终端用户产业、地区和竞争格局划分,2021-2031年) 超音波流量计市场规模、份额和成长分析(按部署类型、测量技术、测量路径数量、最终用户和地区划分)—2026-2033年产业预测全球废水及污水处理超音波流量计市场-依技术、区域及竞争格局分類的产业规模、份额、趋势、机会及预测(2021-2031年预测)

超音波流量计市场规模、份额和成长分析(按部署类型、测量技术、测量路径数量、最终用户和地区划分)—2026-2033年产业预测全球废水及污水处理超音波流量计市场-依技术、区域及竞争格局分類的产业规模、份额、趋势、机会及预测(2021-2031年预测) 全球超音波流量计市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析、未来预测(2026-2034)油气超音波流量计市场-全球产业规模、份额、趋势、机会及预测(依感测器类型、技术、地区及竞争格局划分,2021-2031年预测)

全球超音波流量计市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析、未来预测(2026-2034)油气超音波流量计市场-全球产业规模、份额、趋势、机会及预测(依感测器类型、技术、地区及竞争格局划分,2021-2031年预测) 夹装式超音波流量计市场:按产品类型、技术、产业垂直领域、国家及地区划分 - 全球产业分析、市场规模、市场份额及2025-2032年预测

夹装式超音波流量计市场:按产品类型、技术、产业垂直领域、国家及地区划分 - 全球产业分析、市场规模、市场份额及2025-2032年预测 超音波流量计市场按安装方式、技术、最终用户和地区划分超音波流量计市场:2025-2030 年预测

超音波流量计市场按安装方式、技术、最终用户和地区划分超音波流量计市场:2025-2030 年预测