|

市场调查报告书

商品编码

1940718

欧洲设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

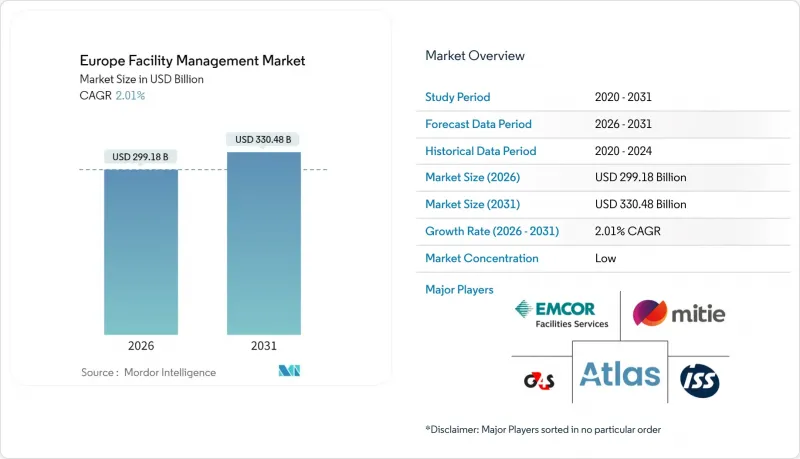

预计到 2026 年,欧洲设施管理市场规模将达到 2,991.8 亿美元,高于 2025 年的 2,932.8 亿美元。

预计到 2031 年将达到 3,304.8 亿美元,2026 年至 2031 年的复合年增长率为 2.01%。

稳定成长反映了维护模式从成本主导转变为资料驱动型绩效服务的转变、日益严格的能源效率法规以及公共部门外包业务的成长。硬性服务仍然是该行业的基础,因为老化的建筑基础设施需要密集的机械、电气和管道维护。同时,在以健康、福祉和体验为导向的职场的推动下,软性服务正在加速发展。俄乌衝突后能源价格上涨,促使客户越来越倾向选择优化合约而非工时和材料合约。随着ESG报告法规和日益复杂的数位技术对专业知识的需求不断增长,外包业务也在不断扩张。私募股权投资,例如Techem公司72亿美元的收购案,凸显了对该领域经常性收入的信心。

欧洲设施管理市场趋势与洞察

老旧建筑存量:维修主导的设施管理支出

欧洲四分之三的建筑存量超过50年,因此对结合技术维护和能源效率的综合维修项目有持续的需求。绩效合约模式,例如Centrica与圣乔治大学医院签订的15年合约(该合约每年减少二氧化碳排放6000吨,节省110万美元),证明了以维修为重点的设施服务在财务上的可行性。随着净零能耗建筑标准的日益严格,德国和法国的建筑组合在维修中迫切需要整合物联网感测器、预测性维护和能源效能分析。欧洲投资银行估计,能源效率领域的年度资金缺口高达1,850亿欧元,这使得设施服务供应商成为筹集资金的关键中介。

后紧缩时代公共部门外包势头强劲

为了达到效率目标和履行环境、社会及治理(ESG)资讯揭露义务,政府机构正在将复杂的服务外包。英国就业与退休金部已授予ISS一份为期七年、每年价值1.75亿美元的合同,用于集中管理清洁、餐饮服务和设施维护。北欧和德国的市政当局也纷纷效仿,剪切机议会与VINCI Facilities签订了为期十年的框架合同,优先考虑协同能源管理。医疗机构尤其重视协同能源管理,因为全天候运作、感染控制和高能耗空调都需要专门的支援。

经济压力(通货膨胀、成本最佳化)

人事费用、材料和能源成本的上涨正迫使客户重新谈判合约并削减非必要的设施管理支出。世邦魏理仕 (CBRE) 的研究发现,儘管 35% 的企业增加了 2023 年的设施管理预算,但仍有 29% 的企业认为供应链中断是其面临的最大威胁。由于医疗保健客户推迟了竞标,索迪斯 (Sodexo) 的欧洲业务在 2025 财年上半年的内部成长率仅为 2.1%。利润率压力在南欧和东欧尤为严峻,这些地区对价格的高度敏感导致商品化趋势加剧。

细分市场分析

到2025年,硬性服务将占欧洲设施管理市场的61.05%,凸显了对老旧建筑基础设施的机电装置(MEP)、暖通空调(HVAC)和消防安全进行维护的必要性。儘管由于持续的维修活动,整个行业的成长速度放缓,但欧洲硬性服务领域的设施管理市场规模仍在不断扩大。由于客户希望延长资产使用寿命并遵守能源使用法规,预测性资产管理正变得越来越普遍。

儘管规模较小,但随着员工体验策略优先考虑高级清洁、礼宾和保全服务,软性服务预计将实现 4.61% 的复合年增长率。混合办公模式的兴起推动了对空间预订、灵活餐饮和非接触式门禁的需求,并将技术融入传统的前台营运中。客流量分析等软性服务数据回馈到能源演算法中,创造了整合机会,使服务提供者能够更深入地参与客户的营运规划。

欧洲设施管理市场按服务类型(硬性服务与软性服务)、交付模式(内部营运与外包)、最终用户行业(商业、酒店、公共基础设施及机构、医疗保健、工业及流程、其他最终用户行业)和国家/地区进行细分。市场预测以以金额为准。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 欧洲商业地产目前运转率

- 领先设施管理服务提供者的盈利基准

- 劳动指标-技术纯熟劳工和非技术技术纯熟劳工参与率

- 按服务类型分類的设施管理市场占有率(%)

- 按硬体服务分類的设施管理市场占有率(%)

- 以软性服务分類的设施管理市场占有率(%)

- 主要都会区的都市化和人口成长

- 欧洲部门投资优先事项基础设施发展计划

- 与劳动和安全标准相关的监管驱动因素

- 欧盟绿色交易中能源效率目标对FM需求的影响

- 科技整合:物联网与人工智慧变革服务交付

- 不断变化的职场:混合办公模式重塑设施管理优先事项

- 市场驱动因素

- 老旧建筑存量:维修主导的设施管理支出

- 财政紧缩后公共部门外包趋势

- 能源价格波动加速了能源优化型设施管理服务的发展

- 强制性ESG报告需要数据驱动的设施管理解决方案。

- 疫情后对健康与安全认证的需求

- 私募股权整合推动了综合设施管理的普及。

- 市场限制

- 经济压力(通货膨胀、成本最佳化)

- 欧盟内部分散的管理体制阻碍了标准化供应。

- 房地产科技互通性有限会增加整合成本

- 互联建筑系统面临的网路安全风险

- 价值链分析

- PESTEL 分析

- 新参与企业的监管和法律体制

- 宏观经济指标对FM需求的影响

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资与资金筹措分析

第五章 市场规模与成长预测

- 按服务类型

- 硬服务

- 资产管理

- 机电及暖通空调服务

- 消防系统和安全措施

- 其他硬体维修服务

- 软服务

- 办公室支援与安全

- 清洁服务

- 餐饮服务

- 其他软性调频服务

- 硬服务

- 以规定形式

- 内部

- 外包

- 单频调频

- 综合设施管理服务

- 综合设施管理(综合FM)

- 按最终用户行业划分

- 商业(IT/通讯、零售/仓储)

- 餐饮服务业(饭店、餐厅、大型餐厅)

- 公共及公共基础设施(政府、教育、交通)

- 医疗保健(公立和私立机构)

- 工业和流程工业(製造业、能源业、采矿业)

- 其他终端用户产业(多用户住宅、娱乐、运动和休閒)

- 按国家/地区

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 斯洛维尼亚

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Mitie Group PLC

- Emcor Facilities Services WLL

- Atlas FM Ltd.

- G4S Facilities Management UK Ltd.

- ISS Global

- Engie FM Ltd.(Cofely AG)

- Andron Facilities Management

- Apleona GmbH

- Dussmann Group

- Vinci Facilities Ltd.

- Okin Group

- Aramark Corporation

- CBRE Group Inc.

- Assured Europe

- Jones Lang LaSalle Inc.

- Sodexo SA

- Johnson Controls International plc

- Bouygues Energies and Services

第七章 市场机会与未来趋势

- 评估差距和未满足的需求

- 技术主导整合设施管理(物联网、楼宇管理系统、基于人工智慧的预测性维护)

- 对符合ESG标准的设施管理解决方案的需求

- 服务模式的未来变化(基于绩效的合约)

European Facility Management Market size in 2026 is estimated at USD 299.18 billion, growing from 2025 value of USD 293.28 billion with 2031 projections showing USD 330.48 billion, growing at 2.01% CAGR over 2026-2031.

A steady expansion reflects the sector's shift from cost-driven maintenance toward data-enabled performance services, tighter energy-efficiency mandates, and widening public-sector outsourcing. Hard services remain the industry's anchor as ageing building systems require intensive mechanical, electrical, and plumbing care, while soft services accelerate on the back of health, wellness, and experience-oriented workplaces. Rising energy prices since the Russia-Ukraine conflict have pushed clients to favor optimization contracts over time-and-materials tasks. Outsourcing gains scale as ESG reporting rules and digital-technology complexity demand specialized know-how. Private-equity interest, typified by Techem's USD 7.2 billion transaction, underlines confidence in the segment's recurring-revenue profile.

Europe Facility Management Market Trends and Insights

Aging Building Stock: Retrofit-Driven FM Spending

Three-quarters of the European building stock is more than 50 years old, creating sustained demand for comprehensive retrofit programmes that bundle technical maintenance with energy upgrades. Performance-contract models such as Centrica's 15-year deal at St George's University Hospitals, which cuts 6,000 tonnes of carbon and saves USD 1.1 million annually, illustrate the financial viability of retrofit-oriented facility services. German and French portfolios face the greatest urgency as Nearly-Zero-Energy Building standards tighten, pushing facility managers to integrate IoT sensors, predictive maintenance, and energy-performance analytics during refurbishments. The European Investment Bank estimates a EUR 185 billion yearly funding gap for energy efficiency, positioning facility service providers as key intermediaries for capital access.

Public-Sector Outsourcing Momentum Post-Fiscal Austerity

Government departments are transferring multi-service bundles to external providers to meet efficiency targets and ESG disclosure obligations. The UK Department for Work and Pensions awarded ISS a seven-year contract worth USD 175 million per year, consolidating cleaning, catering, and technical maintenance under one roof. Nordic and German municipalities follow suit, evidenced by VINCI Facilities' decade-long framework with Lincolnshire County Council that prioritises collaborative energy management. Health-care estates are prominent adopters as 24/7 operations, infection control, and high-energy HVAC loads demand specialist support.

Economic Pressures (Inflation, Cost Optimisation)

Rising labour, material, and energy inputs prompt clients to renegotiate contracts, curbing discretionary FM spend. CBRE notes that while 35% of organisations raised FM budgets in 2023, 29% still listed supply-chain disruption as the top threat. Sodexo's European business recorded only 2.1% organic growth for the first half of fiscal 2025 as healthcare clients delayed tenders. Margin pressure is acute in Southern and Eastern Europe, where price sensitivity drives commoditisation.

Other drivers and restraints analyzed in the detailed report include:

- Energy Price Volatility Accelerating Energy-Optimisation Services

- ESG Reporting Mandates Requiring Data-Driven Solutions

- Fragmented EU Regulatory Regimes Hindering Standardised Delivery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services hold 61.05% of the European facility management market in 2025, underlining the necessity of MEP, HVAC, and fire-safety upkeep across an ageing building base. Persistent retrofit activity keeps the European facility management market size for hard services expanding despite moderate industry growth. Predictive asset management gains traction as clients look to extend equipment life cycles and comply with energy-use regulations.

Soft services, though smaller, deliver a 4.61% forecast CAGR as employee-experience strategies prioritise advanced cleaning, concierge, and security packages. Hybrid work drives demand for space booking, flexible catering, and touchless access control, threading technology through traditional frontline functions. Integration opportunities arise where soft-service data, such as footfall analytics, feed back into energy algorithms, further embedding providers in client operational planning.

Europe Facility Management Market is Segmented by Service Type (Hard Services and Soft Services), Offering Type (In-House and Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, and Other End-User Industries), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mitie Group PLC

- Emcor Facilities Services WLL

- Atlas FM Ltd.

- G4S Facilities Management UK Ltd.

- ISS Global

- Engie FM Ltd. (Cofely AG)

- Andron Facilities Management

- Apleona GmbH

- Dussmann Group

- Vinci Facilities Ltd.

- Okin Group

- Aramark Corporation

- CBRE Group Inc.

- Assured Europe

- Jones Lang LaSalle Inc.

- Sodexo SA

- Johnson Controls International plc

- Bouygues Energies and Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Current Occupancy Rates in Europe Commercial Real Estate

- 4.1.2 Profitability Benchmarks of Major FM Providers

- 4.1.3 Workforce Indicators - Skilled and Unskilled Labor Participation

- 4.1.4 Facility Management Market Share (%) by Service Type

- 4.1.5 Facility Management Market Share (%) by Hard Services

- 4.1.6 Facility Management Market Share (%) by Soft Services

- 4.1.7 Urbanization and Population Growth in Top Metro Areas

- 4.1.8 Sector Investment Priorities in Europe Infrastructure Pipeline

- 4.1.9 Regulatory Drivers Specific to Labour and Safety Standards

- 4.1.10 EU Green Deal Energy-Efficiency Targets Impact on FM Demand

- 4.1.11 Technology Integration: IoT and AI Transforming Service Delivery

- 4.1.12 Changing Workplace Dynamics: Hybrid Work Reshaping FM Priorities

- 4.2 Market Drivers

- 4.2.1 Aging Building Stock: Retrofit-Driven FM Spending

- 4.2.2 Public Sector Outsourcing Momentum Post-Fiscal Austerity

- 4.2.3 Energy Price Volatility Accelerating Energy-Optimization FM Services

- 4.2.4 ESG Reporting Mandates Requiring Data-Driven FM Solutions

- 4.2.5 Post-Pandemic Health and Safety Certification Demand

- 4.2.6 Private Equity Consolidation Driving Integrated FM Adoption

- 4.3 Market Restraint

- 4.3.1 Economic Pressures (Inflation, Cost Optimisation)

- 4.3.2 Fragmented EU Regulatory Regimes Hindering Standardised Delivery

- 4.3.3 Limited PropTech Interoperability Increasing Integration Costs

- 4.3.4 Cybersecurity Risks to Connected Building Systems

- 4.4 Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Slovenia

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mitie Group PLC

- 6.4.2 Emcor Facilities Services WLL

- 6.4.3 Atlas FM Ltd.

- 6.4.4 G4S Facilities Management UK Ltd.

- 6.4.5 ISS Global

- 6.4.6 Engie FM Ltd. (Cofely AG)

- 6.4.7 Andron Facilities Management

- 6.4.8 Apleona GmbH

- 6.4.9 Dussmann Group

- 6.4.10 Vinci Facilities Ltd.

- 6.4.11 Okin Group

- 6.4.12 Aramark Corporation

- 6.4.13 CBRE Group Inc.

- 6.4.14 Assured Europe

- 6.4.15 Jones Lang LaSalle Inc.

- 6.4.16 Sodexo SA

- 6.4.17 Johnson Controls International plc

- 6.4.18 Bouygues Energies and Services

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-based Contracts)

设施管理市场:2026-2032年全球市场预测(依产品、产品模式、部署类型、公司规模及最终用途划分)

设施管理市场:2026-2032年全球市场预测(依产品、产品模式、部署类型、公司规模及最终用途划分) 设施管理市场规模、份额、趋势和预测:按解决方案、服务、部署类型、组织规模、行业和地区划分,2026-2034 年设施管理服务市场:2026-2032年全球市场预测(依服务类型、合约类型、服务交付方式、最终用户和组织规模划分)

设施管理市场规模、份额、趋势和预测:按解决方案、服务、部署类型、组织规模、行业和地区划分,2026-2034 年设施管理服务市场:2026-2032年全球市场预测(依服务类型、合约类型、服务交付方式、最终用户和组织规模划分) 2026年全球地下设施维护与管理市场报告2026年全球硬性服务设施管理市场报告2026年全球设施支援服务市场报告2026年全球设施管理服务市场报告2026年全球软性服务设施管理市场报告

2026年全球地下设施维护与管理市场报告2026年全球硬性服务设施管理市场报告2026年全球设施支援服务市场报告2026年全球设施管理服务市场报告2026年全球软性服务设施管理市场报告 设施管理市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测硬设施管理市场:依服务类型、合约类型、所有权类型和最终用户产业划分-2026-2032年全球市场预测

设施管理市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测硬设施管理市场:依服务类型、合约类型、所有权类型和最终用户产业划分-2026-2032年全球市场预测