|

市场调查报告书

商品编码

1940725

英国工业自动化系统整合商:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)United Kingdom Industrial Automation System Integrator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

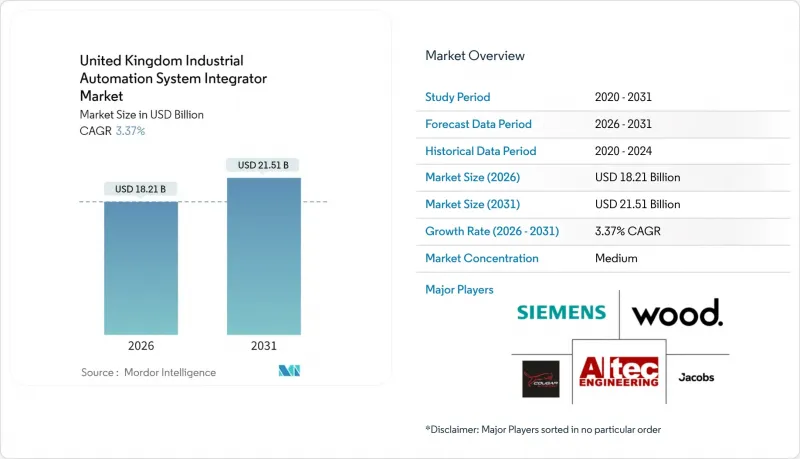

英国工业自动化系统整合商市场规模预计到 2026 年将达到 182.1 亿美元,高于 2025 年的 176.2 亿美元,预计到 2031 年将达到 215.1 亿美元。

预计2026年至2031年年复合成长率(CAGR)为3.37%。

这项扩张的驱动力来自政府支持的数位化专案、因英国脱欧导致的劳动力短缺而更加註重生产力,以及离散产业和流程产业加速向工业4.0平台转型。製造商将全厂互联、云端分析和远端支援视为在依赖出口的经济体中建立韧性的最快途径。中型企业能够获得「智慧製造」(Made Smarter)津贴进行数位化准备评估,因此投资势头最为强劲;而大型企业则正在加快多年维修计划,以在后疫情时代保护其出口份额。政策驱动因素和私人资本的共同作用,即使在宏观经济动盪时期也能保持自动化计划储备的良好状态,并缓解汽车和食品加工市场对传统采购週期的依赖。

英国工业自动化系统整合商市场趋势与洞察

数位转型和工业4.0的采用

製造商正从孤立的自动化系统转向融合营运数据和企业数据的整合式全厂升级。国家「智慧製造」(Made Smarter)计画将在2024年前向1,000家工厂提供1,600万英镑(2,030万美元)的资金,用于诊断、实施蓝图和员工发展支援。企业正在采用通用资料模型和安全云端网关,使现场感测器能够直接连接到ERP系统。中小企业尤其受益,因为计划顾问简化了供应商选择和合规流程。机器製造商现在预先载入符合ISO 23247标准的网路安全模板,从而缩短工程週期并确保不同现有设备站点之间的互通性。随着越来越多的工厂实现数位化成熟,整合商正在赢得多站点合同,这些合约将PLC更换、SCADA现代化和託管分析整合到一个单一的服务包中。

英国劳动力短缺,对提高生产力的需求日益增长

英国数据显示,到2024年,工厂将出现12.4万个空缺职位。近6%的薪资成长正推动工厂快速向自动化检测、机器人堆迭和预测性维护转型,从而降低加班成本。目前的财务模型预测,自动化投资回收期为18至24个月,远低于英国脱欧前通常的五年。物流供应商也支持这一趋势,履约中心的自主移动机器人即使在季节性工人减少的情况下也能维持稳定的生产量。技能委员会正在对现有员工进行再培训,使其能够胜任管理机器人集群而非人工操作的职位。系统整合商正在签订服务合约,以确保达到运转率目标,从而为不堪重负的客户承担人员配备风险。

高昂的初始资本投资与整合成本

由于遗留资产映射发现存在未记录的代码、过时的现场现场汇流排和非标准的电机控制,计划审核平均预算超支高达30%。英国脱欧后的汇率波动推高了进口硬体的价格,而国内供应商难以进行小批量生产,导致单位成本居高不下。整合商提供按里程碑资金筹措的服务包,使现金支出与实现的利润相符。然而,由于许多中小企业推迟全面数位化,转而选择感测器改装而非全面升级,英国工业自动化系统整合商市场的成长势头正在放缓。

细分市场分析

至2025年,PLC将在英国工业自动化系统整合商市场规模中维持32.25%的份额,凸显其作为批量和离散生产线预设控制基础的地位。受电动车动力传动系统组装和生产线末端包装需求成长的推动,机器人单元和机器视觉拣选与检测将以5.45%的复合年增长率推动市场成长。分散式控制系统在化学和炼製产业中仍占据主导地位,这些行业对连续加工和高可用性架构的需求使其高额投入物有所值。 SCADA扩展在数位化驱动的公共产业领域越来越受欢迎,以支援即时资产健康仪錶板。

对互通性的需求促使原始设备製造商 (OEM) 开放 API,使整合商能够将 PLC、机器人、视觉和感测器层整合到单一的数位双胞胎中。客户倾向于选择符合 IEC 61508 和 EMC 指令的硬件,以最大限度地减少重新核准的周期。整合控制堆迭正在推动英国工业自动化系统整合商市场的扩张,因为客户更倾向于捆绑式升级,而不是零散地更换控制面板。

设计和工程服务将占2025年收入的34.15%,因为新计画需要进行模拟、风险分析和概念验证钻机。管理服务结合远端监控将以5.05%的复合年增长率呈现最快的成长轨迹,将计划储备转化为持续的收入来源,并提高客户终身价值。安装和试运行服务仍然很重要,但随着模组化即插即用硬体减少现场工作,其份额正在下降。同时,由于工厂业主透过即插即用的I/O模组和云端韧体更新延长了现有控制系统的使用寿命,升级和维修需求正在上升。

边缘网关将加密的遥测资料传输到服务供应商的分析中心,以便在故障发生前检测轴承磨损或讯号漂移,从而实现基于效能的合约。整合商现在协商的关键绩效指标 (KPI) 与吞吐量和减少废弃物挂钩,而不是与计费工时挂钩,这增强了信任度并为高价定价提供了依据。这种服务转型正在建立一种经常性收入来源,使英国工业自动化系统整合商产业免受週期性资本支出波动的影响。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 数位转型和工业4.0的采用

- 英国劳动力短缺,对提高生产力的需求日益增长

- 加速汽车改造中机器人技术在电动车领域的应用

- 英国铁路网公司的目标:190多个数位讯号系统

- 食品饮料业的「消失的地平线」自动化资金筹措

- 英国政府支持的区域性“智慧机器中心”

- 市场限制

- 高昂的初始资本投资与整合成本

- 熟练自动化工程师短缺

- 铁路号誌系统中的原始设备製造商(OEM)特定智慧财产权壁垒

- 传统OT-IT网路安全标准各自独立

- 产业价值链分析

- 监管环境

- 技术展望

- 宏观经济因素的影响

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 主要应用案例(按行业划分)

第五章 市场规模与成长预测

- 按组件

- 可程式逻辑控制器(PLC)

- 分散式控制系统(DCS)

- 监控与数据采集(SCADA)

- 人机介面(HMI)

- 工业机器人与机器视觉

- 工业感测器和网络

- 按服务类型

- 设计与工程

- 安装和试运行

- 维护和支援

- 升级和改装

- 託管服务和远端监控

- 按最终用户行业划分

- 车

- 食品/饮料

- 药品和医疗设备

- 能源与电力

- 水和污水处理

- 金属和采矿

- 电子装置和半导体

- 石油和天然气

- 其他终端用户产业

- 透过技术

- 工业物联网(IIoT)平台

- 人工智慧与预测分析

- 数位双胞胎与仿真

- 边缘运算和5G连接

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Wood PLC

- Jacobs UK Limited

- Siemens Mobility Limited

- Altec Engineering Limited

- Cougar Automation Limited

- Adsyst Automation Limited

- Au Automation Limited

- Emerson Process Management Limited

- Applied Automation(UK)Limited

- Automated Control Solutions Limited

- Cully Automation Limited

- ABB Limited

- Honeywell Control Systems Limited

- Rockwell Automation UK Limited

- Schneider Electric Systems UK Limited

- Mitsubishi Electric Europe BV(UK Branch)

- Yokogawa United Kingdom Limited

- Hitachi Rail STS UK Limited

- Linbrooke Services Limited

- Adelphi Automation Limited

第七章 市场机会与未来展望

The United Kingdom industrial automation system integrator market size in 2026 is estimated at USD 18.21 billion, growing from 2025 value of USD 17.62 billion with 2031 projections showing USD 21.51 billion, growing at 3.37% CAGR over 2026-2031.

This expansion arises from government-backed digital programs, Brexit-related labor shortages that sharpen the focus on productivity, and a stepped-up shift to Industry 4.0 platforms across discrete and process industries. Manufacturers view full-plant connectivity, cloud analytics, and remote support as the fastest route to resilience in an export-heavy economy. Investment momentum is strongest among mid-sized firms that now access Made Smarter grants for digital readiness assessments, while large enterprises accelerate multi-year retrofit schedules to protect export share in the post-pandemic environment. The policy push combines with private capital to keep automation pipelines healthy even during macroeconomic turbulence, tempering the market's historical dependence on automotive and food processing procurement cycles.

United Kingdom Industrial Automation System Integrator Market Trends and Insights

Digital Transformation and Industry 4.0 Adoption

Manufacturers have shifted from isolated automation islands to integrated plantwide upgrades that blend operational and enterprise data. The Made Smarter national rollout allocated GBP 16 million (USD 20.3 million) in 2024 to support 1,000 factories with diagnostics, implementation roadmaps, and talent coaching. Firms adopt common data models and secure cloud gateways, allowing shop-floor sensors to link directly to enterprise resource planning suites. Small and medium enterprises benefit most because program advisers streamline vendor selection and standards compliance. Machine builders now preload ISO 23247-aligned, cyber-secure templates, reducing engineering cycles and ensuring interoperability within diverse brownfield sites. As more plants reach digital maturity, integrators win multi-site contracts that bundle PLC replacement, SCADA revamps, and managed analytics into a single service envelope.

Rising Demand for Productivity Amid UK Labor Shortages

UK data shows 124,000 factory vacancies in 2024, and pay inflation near 6% drives a rapid pivot to automated inspection, robotic palletizing, and predictive maintenance, which trims overtime costs. Financial modeling places current automation paybacks at 18-24 months, compared with the five-year horizons that were common before Brexit. Logistics operators reinforce the trend; autonomous mobile robots in fulfillment centers maintain stable output even when seasonal worker pools shrink. Skills councils retrain incumbents for supervisory roles that oversee fleets of robots, rather than manual work centers. Integrators seize service contracts that guarantee uptime targets, absorbing staffing risks on behalf of overstretched customers.

High Initial Capex and Integration Costs

Project audits reveal overruns average 30% because legacy asset mapping uncovers undocumented code, obsolete fieldbuses, and nonstandard motor controls. Currency fluctuations since Brexit have increased the prices of imported hardware, while domestic suppliers struggle with small production runs that keep per-unit costs high. Integrators provide service packages financed over milestones, aligning cash outflows with realized gains. Still, many SMEs defer full digitization, opting for sensor retrofits rather than holistic upgrades, which slows the momentum of the total United Kingdom industrial automation system integrator market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Robotics Uptake in Automotive Re-tooling for EVs

- Network Rail Target 190plus Digital Signaling Rollout

- Scarcity of Skilled Automation Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PLCs retained a 32.25% share of the United Kingdom industrial automation system integrator market size in 2025, underscoring their role as the default control backbone in batch and discrete lines. Robot cells and machine-vision pick-checks lead the growth slate at a 5.45% CAGR, propelled by EV power-train assembly and end-of-line packaging. Distributed control systems remain dominant in the chemicals and refining industries, where uninterrupted processing and high-availability architectures justify premium spending. SCADA extensions gain traction in utilities undergoing digitization to support real-time asset health dashboards.

Interoperability pressure nudges OEMs to expose open APIs, enabling integrators to blend PLC, robot, vision, and sensor layers into a single digital twin. Customers favor hardware certified to IEC 61508 and EMC directives, minimizing re-approval cycles. The converged control stack underpins the expansion of the United Kingdom industrial automation system integrator market, because customers award bundled upgrades instead of piecemeal panel changes.

Design and engineering services accounted for 34.15% of 2025 revenue, as greenfield projects require simulation, hazard analysis, and proof-of-concept rigs. Managed services, combined with remote monitoring, exhibit the fastest trajectory at a 5.05% CAGR, converting project pipelines into annuities and increasing lifetime customer value. Installation and commissioning remain essential, but they shrink in proportion as modular plug-and-play hardware reduces on-site effort. Upgrades and retrofits increase because plant owners extend the service life of installed controls through drop-in I/O modules and cloud firmware updates.

Edge-enabled gateways stream encrypted telemetry to service-provider analytics centers that detect bearing wear or signal drift ahead of failure, enabling outcome-based contracts. Integrators now negotiate key performance indicators tied to throughput or scrap reduction, rather than hours billed, reinforcing trust and justifying premium pricing. The service shift anchors recurring revenue streams that stabilize the United Kingdom industrial automation system integrator industry against cyclical capex swings.

The UK Industrial Automation System Integrator Market is Segmented by Component (PLC, DCS, and More), Service Type (Design and Engineering, Installation and Commissioning, and More), End-User Industry (Automotive, Food and Beverage, and More), Technology (Industrial Internet of Things (IIoT) Platforms, Artificial Intelligence and Predictive Analytics, and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Wood PLC

- Jacobs U.K. Limited

- Siemens Mobility Limited

- Altec Engineering Limited

- Cougar Automation Limited

- Adsyst Automation Limited

- Au Automation Limited

- Emerson Process Management Limited

- Applied Automation (U.K.) Limited

- Automated Control Solutions Limited

- Cully Automation Limited

- ABB Limited

- Honeywell Control Systems Limited

- Rockwell Automation U.K. Limited

- Schneider Electric Systems U.K. Limited

- Mitsubishi Electric Europe B.V. (U.K. Branch)

- Yokogawa United Kingdom Limited

- Hitachi Rail STS U.K. Limited

- Linbrooke Services Limited

- Adelphi Automation Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital Transformation and Industry 4.0 Adoption

- 4.2.2 Rising Demand for Productivity Amid UK Labor Shortages

- 4.2.3 Accelerated Robotics Uptake in Automotive Re-Tooling for EVs

- 4.2.4 Network Rail's Target 190plus Digital Signaling Rollout

- 4.2.5 Food and Drink "Vanishing-Horizon" Automation Funding

- 4.2.6 Regional 'Smart Machine Hubs' Backed by UK Government

- 4.3 Market Restraints

- 4.3.1 High Initial Capex and Integration Costs

- 4.3.2 Scarcity of Skilled Automation Engineers

- 4.3.3 OEM-Locked Intellectual-Property Barriers in Rail Signaling

- 4.3.4 Fragmented Legacy OT-IT Cybersecurity Standard

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Key Use-cases Across Different Verticals

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Programmable Logic Controllers (PLC)

- 5.1.2 Distributed Control Systems (DCS)

- 5.1.3 Supervisory Control and Data Acquisition (SCADA)

- 5.1.4 Human-Machine Interface (HMI)

- 5.1.5 Industrial Robots and Machine Vision

- 5.1.6 Industrial Sensors and Networks

- 5.2 By Service Type

- 5.2.1 Design and Engineering

- 5.2.2 Installation and Commissioning

- 5.2.3 Maintenance and Support

- 5.2.4 Upgrades and Retrofits

- 5.2.5 Managed Services and Remote Monitoring

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Food and Beverage

- 5.3.3 Pharmaceuticals and Medical Devices

- 5.3.4 Energy and Power

- 5.3.5 Water and Wastewater

- 5.3.6 Metals and Mining

- 5.3.7 Electronics and Semiconductors

- 5.3.8 Oil and Gas

- 5.3.9 Other End-user Industries

- 5.4 By Technology

- 5.4.1 Industrial Internet of Things (IIoT) Platforms

- 5.4.2 Artificial Intelligence and Predictive Analytics

- 5.4.3 Digital Twin and Simulation

- 5.4.4 Edge Computing and 5G Connectivity

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Wood PLC

- 6.4.2 Jacobs U.K. Limited

- 6.4.3 Siemens Mobility Limited

- 6.4.4 Altec Engineering Limited

- 6.4.5 Cougar Automation Limited

- 6.4.6 Adsyst Automation Limited

- 6.4.7 Au Automation Limited

- 6.4.8 Emerson Process Management Limited

- 6.4.9 Applied Automation (U.K.) Limited

- 6.4.10 Automated Control Solutions Limited

- 6.4.11 Cully Automation Limited

- 6.4.12 ABB Limited

- 6.4.13 Honeywell Control Systems Limited

- 6.4.14 Rockwell Automation U.K. Limited

- 6.4.15 Schneider Electric Systems U.K. Limited

- 6.4.16 Mitsubishi Electric Europe B.V. (U.K. Branch)

- 6.4.17 Yokogawa United Kingdom Limited

- 6.4.18 Hitachi Rail STS U.K. Limited

- 6.4.19 Linbrooke Services Limited

- 6.4.20 Adelphi Automation Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment