|

市场调查报告书

商品编码

1940738

大幅面印表机(LFP):市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)Large Format Printers (LFP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

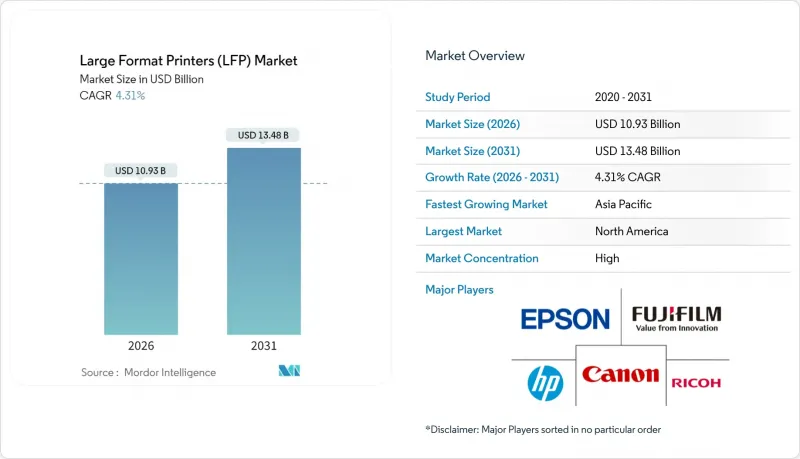

预计到 2026 年,大幅面印表机市场价值将达到 109.3 亿美元,高于 2025 年的 104.8 亿美元。

预计到 2031 年,该产业规模将达到 134.8 亿美元,2026 年至 2031 年的复合年增长率为 4.31%。

这一成长轨迹反映出,印刷业经历了快速扩张期,但随着数位化包装、纺织品个人化和高衝击力标牌需求的融合,该行业正持续巩固自身地位。高速紫外线固化系统、永续水性油墨的创新以及人工智慧驱动的工作流程自动化,在延长印表机使用寿命的同时,有效控制了营运成本。儘管北美地区仍保持主导地位,但亚太地区加速的资本投资和不断壮大的製造业基地预示着未来五年产业格局将会转变。竞争优势将取决于整合硬体、软体和经认证的环保油墨的端到端解决方案,使印刷服务供应商能够在不牺牲品质的前提下,快速回应小批量、可变资料印刷作业。

全球大幅面印表机(LFP)市场趋势与洞察

包装、广告和纺织品产业快速成长

预计印刷包装市场将从2024年的5,120亿美元成长到2029年的6,950亿美元,复合年增长率(CAGR)为6.3%,成为大尺寸印表机市场最具影响力的需求驱动因素。同时,随着时尚品牌越来越多地采用小批量定制,预计数位纺织品生产将从2024年的31亿美元增长到2030年的79亿美元,复合年增长率(CAGR)为14.9%。户外媒体预算的復苏也推动了对耐用承印物的需求。这些趋势共同促使供应商开发模组化印表机,使其能够在单班制生产中处理瓦楞纸板、柔性薄膜和聚酯织物。Canon配备白色墨水的Colorado M系列印表机展现了混合列印功能的价值,实现了从原型製作到批量生产的无缝过渡。

采用紫外线固化和高速喷墨列印技术

由于其即时固化、广泛的承印物相容性和低排放优点,UV固化设备在北美和欧洲正得到越来越广泛的应用。Canon的UVgel系统和FUJIFILM的AQUAFUZE系统透过缩短印后加工时间和避免使用挥发性溶剂,提高了工厂的生产效率。Ricoh报告称,受标牌和图形需求激增的推动,其2024年第一季工业印刷硬体业务成长了32%。高速喷墨技术兼具接近胶印的列印速度和数位印刷的柔软性,对于需要快速切换作业的大量商业印刷而言,尤其具有吸引力。因此,传统的溶剂型设备正稳定地转向具有自动化色彩管理功能的UV固化和水性技术。

数位电子看板的替代方案

预计2018年至2023年,印刷指示牌市场将以-2.2%的复合年增长率萎缩,规模将达到409亿美元。同时,欧洲数字显示市场正以每年约11%的速度成长。数位户外广告(DOOH)已占户外广告(OOH)总收入的37%,在澳洲的渗透率高达76%。广告商优先考虑即时内容更新和受众分析,而印刷品无法提供这些功能。因此,在高流量交通枢纽,印刷广告的投放量正在下降,而纸张和乙烯基材料仍然是成本敏感型或一次性宣传活动的首选。这种限制正在影响大尺寸印表机市场,但也推动了混合宣传活动的创新,将静态背景与动态LED迭加层结合。

细分市场分析

到2025年,印表机将贡献76.92%的收入,巩固大幅面印表机市场的基础。 UV固化引擎、混合式平板/捲筒系统以及能够一次列印多种承印物的乳胶平台,正推动稳定的硬体需求。Canon、Epson和惠普正在扩展其白色墨水和萤光颜料的选择范围,使印表机能够承接利润更高的装饰和包装业务。持续的更新换代週期,使得大尺寸印表机市场始终处于资本预算的核心地位。

软体收入虽然规模较小,但正以 5.63% 的复合年增长率成长,这主要得益于人工智慧驱动的作业分组、自动拼版和远端设备健康监控等技术的普及。惠普 PrintOS、CanonPRISMA 和RicohTotalFlow 套件将独立印表机转变为云端连接的生产节点。这项转变表明,大尺寸印表机市场与工业 4.0 的理念高度契合,其价值不仅体现在机械输出上,更体现在数据驱动的效率上。

预计到2025年,喷墨列印仍将占据大幅面印表机市场47.74%的份额,这主要得益于其按需列印技术的多功能性和广色域。喷墨列印可使用多种水性、乳胶、溶剂型和UV墨水,使用者可根据应用需求选择最合适的墨水,使其成为标誌和装饰应用领域的首选技术。

儘管目前规模较小,但随着新一代静电照相印刷机尺寸达到B2XL,预计到2031年,碳粉和雷射平台将以5.52%的复合年增长率成长。RicohPro C9500系列在复杂作业中可达到额定速度的97%,使其成为高印量商业印刷的理想选择,因为在这些领域,运作的稳定性优于卷轴式介质的灵活性。喷墨和碳粉的共存表明,大尺寸印表机市场正在满足多种作业需求,而非单一的主导技术。

区域分析

预计到2025年,北美将占全球收入的40.86%,这主要得益于人工智慧工作流程的早期应用以及NESHAP(40 CFR Part 63)下严格的环境标准,该标准有利于低排放印表机的发展。对预测性维护的投资已将营运成本降低了10%至35%,从而在列印量下降的情况下保持了稳定的利润率。华盛顿州等州的PFAS法规正在加速向相容的水性系统的升级,巩固了支撑大幅面印表机市场的高端细分市场。亚太地区是成长最快的地区,预计到2031年将以5.48%的复合年增长率成长。根据FAPGA的报告,商业印刷市场预计将从2022年的1,846亿美元成长到2031年的2,826亿美元。

欧洲在永续性趋势方面持续引领潮流。 2024/825 号指令禁止模糊的环境声明,并强制规定可回收性阈值,引导买家使用不含 PFAS 的油墨和经 FSC 认证的基材。需要 ESG 报告审核追踪的品牌所有者正在采用配备在线连续光强度和封闭回路型色彩引擎的印刷机。虽然成熟的需求放缓了整体成长速度,但早期合规投资正在支持服务合约和改造套件的销售,从而扩大潜在市场规模。

南美洲和中东及非洲地区的贡献较小,但为能够提供可承受电压波动和高温的坚固耐用设备的供应商提供了机会。沿岸地区的体育场馆和旅游综合体等大型企划青睐高阶UV混合印表机,而巴西的加工业者则在寻找经济实惠的溶剂型印表机。随着资金筹措通路的拓展,这些地区将推动大幅面印表机市场产量的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 包装、广告和纺织领域的需求不断增长

- 采用紫外线固化和高速喷墨列印技术

- ESG主导的向水性油墨转型

- 中小型印刷厂的AI自动化工作流程

- 社区型「微型工厂」印刷中心的兴起

- 用于乳製品替代品的无菌冷填充技术

- 市场限制

- 数位电子看板的替代方案

- 工业磷酸铁锂电池的高昂资本与营运成本

- PFAS-free油墨监理方面即将出现的空白

- 轻质玻璃技术降低了重量优势

- 产业供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 报价

- 印表机

- 软体

- 服务

- 透过印刷技术

- 喷墨

- 墨粉/雷射

- 按墨水类型

- 水溶液

- 溶剂型及环保溶剂型

- 紫外线固化型

- 乳胶

- 染料昇华

- 按最终用户行业划分

- 标誌和户外广告

- 服装和纺织品

- 装饰和室内图形

- 电脑辅助设计/技术

- 包装和标籤

- 其他终端用户产业

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 马来西亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- HP Inc.

- Canon Inc.

- Seiko Epson Corporation

- Roland DG Corporation

- Mimaki Engineering Co., Ltd.

- Ricoh Company, Ltd.

- Agfa-Gevaert NV

- Durst Group AG

- Electronics For Imaging, Inc.(EFI)

- Konica Minolta, Inc.

- Kyocera Corporation

- Mutoh Holdings Co., Ltd.

- Fujifilm Holdings Corporation

- ColorJet Group

- SwissQprint AG

- JHF Group

- DGI Co., Ltd.

第七章 市场机会与未来展望

Large-format printers market size in 2026 is estimated at USD 10.93 billion, growing from 2025 value of USD 10.48 billion with 2031 projections showing USD 13.48 billion, growing at 4.31% CAGR over 2026-2031.

The growth path reflects a sector that has moved beyond rapid expansion yet continues to gain ground as packaging digitization, textile personalization, and high-impact signage demand converge. Faster UV-curable systems, sustainable water-based ink innovations, and AI-enabled workflow automation are extending printer lifecycles while keeping operating costs in check. Regional leadership remains with North America, but Asia Pacific's accelerating capital investment and expanding manufacturing base signal a shift in power over the next five years. Competitive differentiation hinges on end-to-end solutions that integrate hardware, software, and certified eco-inks, enabling print service providers to respond promptly to short-run, variable-data jobs without compromising quality.

Global Large Format Printers (LFP) Market Trends and Insights

Packaging, advertising and textile boom

Printed packaging is projected to expand from USD 512 billion in 2024 to USD 695 billion by 2029, at a 6.3% CAGR, making packaging the most influential demand driver for the large-format printers market. Simultaneously, digital textile output is projected to rise from USD 3.1 billion in 2024 to USD 7.9 billion in 2030, at a 14.9% CAGR, as fashion brands increasingly adopt short-run customization. Outdoor media budgets are rebounding, which elevates the need for high-durability substrates. Together, these trends push vendors to develop modular printers capable of handling corrugated board, flexible films, and polyester fabric in a single shift. Canon's Colorado M-series with white ink showcases the value of hybrid capability that seamlessly transitions between prototyping and production.

UV-curable and high-speed inkjet adoption

Immediate curing, broad substrate support, and low emissions drive the adoption of UV-curable installations in North America and Europe. Canon UVgel and Fujifilm AQUAFUZE systems reduce finishing times and eliminate volatile solvents, enhancing shop throughput. Ricoh reports that its industrial printing hardware grew 32% in Q1 2024, driven by surging sign-graphics demand. Print speeds that approach offset quality while retaining digital flexibility make high-speed inkjet technology attractive for high-volume commercial work, especially where quick job changeovers are crucial. The outcome is a steady migration away from legacy solvent machines toward UV-curable and aqueous technologies with automated color control.

Digital signage substitution

Printed signage contracted at a -2.2% CAGR between 2018 and 2023 to USD 40.9 billion, while digital displays gained roughly 11% annually in Europe. Digital out-of-home already secures 37% of total OOH revenue and holds 76% penetration in Australia. Advertisers value real-time content updates and audience analytics that print cannot match. As a result, print volumes fall in high-traffic transit hubs, although cost-sensitive or temporary campaigns still favor paper or vinyl. The restraint pulls on the large-format printers market yet sparks innovation in hybrid campaigns that pair static backdrops with active LED overlays.

Other drivers and restraints analyzed in the detailed report include:

- ESG-driven shift to water-based inks

- AI-automated workflow for SMB print shops

- High cap-ex and opex of industrial LFPs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Printers generated 76.92% of revenue in 2025, anchoring the large format printers market. Hardware demand remains stable, thanks to UV-curable engines, hybrid flatbed-roll systems, and latex platforms that handle diverse substrates in a single pass. Canon, Epson, and HP expand their white-ink and neon pigment options, allowing print shops to pursue higher-margin decor and packaging work. Ongoing replacement cycles sustain the large-format printers market size at the core of capital budgets.

Software revenue, though smaller, is rising at a 5.63% CAGR as AI-driven job ganging, automatic imposition, and remote device health monitoring gain traction. HP PrintOS, Canon PRISMA, and Ricoh TotalFlow suites convert stand-alone printers into cloud-linked production nodes. The shift illustrates how the large-format printers market aligns with Industry 4.0, where value resides in data-enabled efficiency as much as in mechanical output.

Inkjet maintained a 47.74% market share of the large-format printers market in 2025, driven by the versatility of drop-on-demand technology and its wide color gamut. Water-based, latex, solvent, and UV variations enable users to tailor fluids to meet end-use requirements, making inkjet the default technology for signage and decor.

Toner and laser platforms, although smaller, are projected to show a 5.52% CAGR through 2031 as next-generation electrophotographic presses reach B2XL sizes. Ricoh's Pro C9500 series achieves a 97% rated speed on complex jobs, making it an attractive option for high-volume commercial runs where uptime consistency outweighs the benefits of roll-to-roll media freedom. The coexistence of inkjet and toner confirms that the large-format printers market serves multiple job profiles rather than a single dominant method.

The Large Format Printers Market Report is Segmented by Offering (Printers, Software, and Services), Printing Technology (Inkjet, and Toner/Laser), Ink Type (Aqueous, Solvent and Eco-Solvent, UV-Curable, Latex, and Dye-Sublimation), End-User Industry (Signage and Outdoor Advertising, Apparel and Textiles, Decor and Interior Graphics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 40.86% of revenue in 2025, driven by the early adoption of AI-enabled workflows and stringent environmental standards under NESHAP 40 CFR Part 63, which rewards low-emission printers. Investments in predictive maintenance deliver 10-35% operating cost reductions, keeping profit margins resilient even as print runs shrink. PFAS limits in states such as Washington accelerate upgrades to compliant water-based systems, solidifying a premium segment that underpins the large-format printers market. The Asia Pacific is the fastest-growing region, with a 5.48% CAGR projected to 2031. FAPGA reports that commercial printing is expected to expand from USD 184.6 billion in 2022 to USD 282.6 billion in 2031.

Europe remains a sustainability trendsetter. Directive 2024/825 bans vague green claims and enforces recyclability thresholds, steering buyers toward PFAS-free inks and FSC-certified substrates. Printers equipped with inline spectrophotometers and closed-loop color engines gain acceptance among brand owners who require audit trails for ESG reporting. While mature demand keeps overall growth modest, early compliance spend supports service contracts and retrofit kits, enriching the total addressable opportunity.

South America, the Middle East, and Africa contribute smaller shares, yet present opportunities for suppliers that can deliver rugged devices tolerant of voltage swings and heat. Mega-projects in the Gulf, such as stadiums and tourism complexes, favor high-end UV hybrids, whereas Brazilian converters seek cost-effective solvent units. As financing options widen, these territories will add incremental tonnage to the large-format printers market.

- HP Inc.

- Canon Inc.

- Seiko Epson Corporation

- Roland DG Corporation

- Mimaki Engineering Co., Ltd.

- Ricoh Company, Ltd.

- Agfa-Gevaert NV

- Durst Group AG

- Electronics For Imaging, Inc. (EFI)

- Konica Minolta, Inc.

- Kyocera Corporation

- Mutoh Holdings Co., Ltd.

- Fujifilm Holdings Corporation

- ColorJet Group

- SwissQprint AG

- JHF Group

- DGI Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Packaging, Advertising and Textile Boom

- 4.2.2 UV-curable and High-speed Inkjet Adoption

- 4.2.3 ESG-Driven Shift to Water-based Inks

- 4.2.4 AI-Automated Workflow for SMB Print Shops

- 4.2.5 Rise of Localised "Micro-Factory" Print Hubs

- 4.2.6 Aseptic cold-fill for dairy-alternatives

- 4.3 Market Restraints

- 4.3.1 Digital Signage Substitution

- 4.3.2 High Cap-Ex and Opex of Industrial LFPs

- 4.3.3 Looming PFAS-Free Ink Compliance Gap

- 4.3.4 Lightweight glass tech eroding weight edge

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Printers

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Printing Technology

- 5.2.1 Inkjet

- 5.2.2 Toner / Laser

- 5.3 By Ink Type

- 5.3.1 Aqueous

- 5.3.2 Solvent and Eco-Solvent

- 5.3.3 UV-curable

- 5.3.4 Latex

- 5.3.5 Dye-Sublimation

- 5.4 By End-user Industry

- 5.4.1 Signage and Outdoor Advertising

- 5.4.2 Apparel and Textiles

- 5.4.3 Decor and Interior Graphics

- 5.4.4 CAD and Technical

- 5.4.5 Packaging and Labels

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Malaysia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 HP Inc.

- 6.4.2 Canon Inc.

- 6.4.3 Seiko Epson Corporation

- 6.4.4 Roland DG Corporation

- 6.4.5 Mimaki Engineering Co., Ltd.

- 6.4.6 Ricoh Company, Ltd.

- 6.4.7 Agfa-Gevaert NV

- 6.4.8 Durst Group AG

- 6.4.9 Electronics For Imaging, Inc. (EFI)

- 6.4.10 Konica Minolta, Inc.

- 6.4.11 Kyocera Corporation

- 6.4.12 Mutoh Holdings Co., Ltd.

- 6.4.13 Fujifilm Holdings Corporation

- 6.4.14 ColorJet Group

- 6.4.15 SwissQprint AG

- 6.4.16 JHF Group

- 6.4.17 DGI Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

瓶子印刷机市场规模、份额和成长分析:按印刷技术、自动化程度、适用瓶材、终端用户产业和地区划分-2026-2033年产业预测

瓶子印刷机市场规模、份额和成长分析:按印刷技术、自动化程度、适用瓶材、终端用户产业和地区划分-2026-2033年产业预测 3D热压压平机市场:依产品类型、操作模式、材料类型、压制能力、应用和终端用户产业划分,全球预测,2026-2032年轮转印刷机市场:材料类型、印刷机类型、速度范围、应用和最终用途产业划分-全球预测,2026-2032年

3D热压压平机市场:依产品类型、操作模式、材料类型、压制能力、应用和终端用户产业划分,全球预测,2026-2032年轮转印刷机市场:材料类型、印刷机类型、速度范围、应用和最终用途产业划分-全球预测,2026-2032年 2026年全球印刷检测设备市场报告PCB SMT设备市场按设备类型、基板类型、吞吐量、产量和最终用途行业划分 - 全球预测(2026-2032年)按类型、连接方式、列印解析度、最终用户和分销管道分類的收据印表机市场—2026-2032年全球预测翻新印表机市场:依产品类型、组件、连接方式、功能、最终用户和通路划分,全球预测,2026-2032年

2026年全球印刷检测设备市场报告PCB SMT设备市场按设备类型、基板类型、吞吐量、产量和最终用途行业划分 - 全球预测(2026-2032年)按类型、连接方式、列印解析度、最终用户和分销管道分類的收据印表机市场—2026-2032年全球预测翻新印表机市场:依产品类型、组件、连接方式、功能、最终用户和通路划分,全球预测,2026-2032年 印刷设备市场规模、份额和成长分析(按产品类型、业务类型、承印物类型、应用、最终用途和地区划分)-2026-2033年产业预测

印刷设备市场规模、份额和成长分析(按产品类型、业务类型、承印物类型、应用、最终用途和地区划分)-2026-2033年产业预测 印刷机市场展望(至2030年)

印刷机市场展望(至2030年) 在线连续印刷机:全球市占率及排名、总收入及需求预测(2025-2031年)

在线连续印刷机:全球市占率及排名、总收入及需求预测(2025-2031年)