|

市场调查报告书

商品编码

1940773

远端储槽监控系统:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Remote Tank Monitoring System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

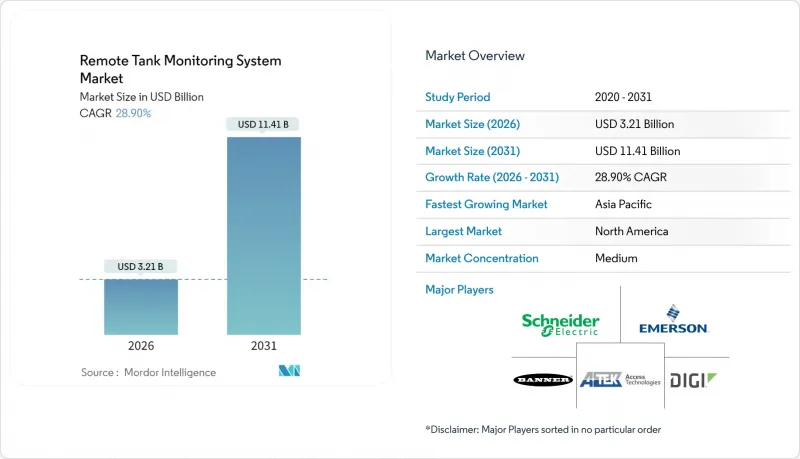

预计远端储槽监控系统市场将从 2025 年的 24.9 亿美元成长到 2026 年的 32.1 亿美元,到 2031 年将达到 114.1 亿美元,2026 年至 2031 年的复合年增长率为 28.9%。

强劲成长反映了工业IoT的日益普及、卫星和低功耗广域网路(LPWAN)连接技术的日益成熟,以及日益严格的环境法规要求对液体储存进行持续监控。产业相关人员正从被动式资产管理转向预测式资产管理,由此带来的效率提升、更少的车辆出勤、更严格的库存管理以及更快的洩漏检测,正吸引着资产所有者和保险公司采用自动化遥测技术。如今,竞争优势主要体现在能够将感测器数据转化为可执行洞察的软体分析技术上,而基于订阅的硬体即服务(HaaS)模式正在降低初始成本门槛,并加速远端储罐监控系统解决方案的普及。

全球远端储罐监控系统市场趋势与洞察

扩大石油、天然气和化学品储存基础设施

根据国际能源总署(IEA)的数据,到2024年,全球油气储存能力预计将成长12%,因为各公司正在为实现能源转型目标而建立策略储备。化学企业也在采取类似措施以应对原材料价格波动,这两种趋势都推动了远端储罐监控系统市场的需求。营运商倾向于扩充性的多站点平台,这些平台能够与现有的SCADA系统集成,并将资料传输到云端进行分析,从而实现全系统最佳化。能够整合卫星通讯链路和蜂窝回程传输的供应商,目前正赢得资本密集型计划的多年期框架合约。

基于云端的物联网平台的普及

预计到 2024 年,微软 Azure IoT 和 AWS IoT Core 在工业应用情境中的年增长率将达到 40%,其中储槽遥测将成为成长最快的新增工作负载之一。云端技术的应用使得基于机器学习的洩漏侦测、自动补给触发和预测性维护等功能成为可能,而这些功能在传统的 SCADA 系统中几乎无法实现。中型企业正在利用订阅定价模式来避免大规模支出 (CAPEX),这进一步加速了远端储罐监控系统解决方案的普及。

高昂的初始硬体和整合成本

从感测器到云端的完整部署,每个储罐的成本可能在 15,000 美元到 45,000 美元之间,而且整合成本通常超过硬体成本。管理储罐数量较少的小型企业很难证明如此高昂的支出是合理的。这种限制正推动远端储罐监控系统市场向模组化套件和硬体即服务 (HaaS) 订阅模式发展,将成本从资本支出 (CAPEX) 转移到营运支出 (OPEX),使用户能够在投资回报率显现时进行扩展。

细分市场分析

2025年,具备低成本和简单二进位警报功能的点位式液位计占据市场主导地位,市占率高达57.92%。同时,连续式液位计平台正赢得许多高价值计划,以29.6%的复合年增长率成长,反映出监管审核和即时物流对持续可视性的要求日益增长。预计2025年至2030年间,连续式液位计安装相关的收入将为远端储槽监控系统市场规模增加40亿美元。

在製药和精细化工行业,高解析度雷达和导波雷达探头的投入正在增加,因为±1毫米的精度有助于提高产品品质。点式液位计系统仍然是丙烷和小型工业储罐的标配,但随着浮球开关逐渐被淘汰,原始设备製造商(OEM)正在将云端控制面板作为标准配置,从而推动了数位式桿式液位计的普及。

到2025年,接触式感测技术将占总收入的61.55%,而非接触式感测技术预计将超越其他类别,这主要得益于超音波和FMCW雷达等避免流体接触的技术。非接触式技术的快速成长将推高平均售价,而先进的讯号处理软体将为供应商提供新的利润成长途径。远端储槽监控系统的安装商也指出,由于没有接触流体的零件,维护成本降低,现场来访频率减少,这些优势进一步提升了物联网在农村资产中的价值。

光学和雷射设备在无菌药品批量处理等高价值应用中占据主导地位,而机械带形水尺仍然用于视觉冗余对于遵守卫生法规至关重要的领域,儘管数位改造套件正朝着将捲尺浮子测量数据传输到 SCADA 的方向发展,从而减少了人工浸入检查。

区域分析

截至2025年,北美仍将维持领先地位,市占率达34.05%,推动要素SPCC法规的实施、广泛的油气基础设施以及工业IoT的早期应用。联邦政府对农村宽频的津贴正在推动低功耗广域网路(LPWAN)的扩展,进一步加速农业省份远端油罐监控系统的普及。加拿大计划扩大战略石油储备,并整合各业者的资产管理平台,这正在形成跨境发展动能。

预计亚太地区将实现最快成长,到2031年复合年增长率将达到33.1%。即时储槽遥测技术对于中国和印度的大规模炼油厂和石化厂扩建计画以及东南亚的采矿计划而言,对于安全措施和环境、社会及治理(ESG)报告都至关重要。区域各国政府也正在实施符合经合组织标准的土壤和水资源保护条例,要求地下储槽所有者实施持续监测。

在欧洲,严格的环境指令和工业脱碳计画正在支撑着经济的稳定成长。一款用于计算散装液体物流中范围3排放的云端仪錶板正受到欧洲大型企业的热烈欢迎,这些企业的目标是在2030年实现碳中和。同时,在中东、非洲和南美洲,液化天然气、海水淡化和采矿等基础设施投资正在推动新计画的开展,从而提升远端储罐监控系统的市场潜力。然而,短期内经济逆风预计将抑制需求成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 扩大石油、天然气和化学品储存基础设施

- 基于云端的物联网平台的兴起

- 加强全球资金外流预防和库存控制

- 卫星物联网技术为偏远地区的油罐提供覆盖

- HaaS订阅模式降低了资本投资门槛

- 范围 3 ESG 报告给散装液体供应链带来压力

- 市场限制

- 高昂的初始硬体和整合成本

- 网路安全和资料所有权问题

- 钢铝关税增加设备物料清单成本

- 负责任的电池废弃物永续性

- 价值链分析

- 监管环境

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 影响市场的宏观经济因素

第五章 市场规模与成长预测

- 透过监测类型

- 点级监测

- 连续液位监测

- 透过技术

- 接触式感应器

- 浮子式和捲尺式压力表

- 磁致伸缩

- 静水压力

- 非接触式感测器

- 超音波

- 雷达/调频连续波

- 光学/雷射

- 接触式感应器

- 连结性别

- 蜂窝通讯(4G LTE、5G、NB-IoT、Cat-M)

- LPWAN(LoRaWAN、Sigfox)

- 卫星(低轨道/地球同步轨道)

- 短距离无线/Wi-Fi/BLE

- 按油箱类型

- 地面固定屋顶

- 地面式浮动顶

- 地下/UST

- 按产能

- 不足10,000公升

- 10,000-50,000 L

- 50,001-200,000 L

- 超过20万公升

- 按最终用户行业划分

- 石油和天然气

- 化学品和石油化工

- 供水/污水处理

- 食品/饮料

- 农业与灌溉

- 发电

- 采矿和金属

- 製药和医疗保健

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 东南亚

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Schneider Electric SE

- Emerson Electric Co.

- Banner Engineering Corp.

- ATEK Access Technologies, LLC(TankScan)

- Anova(DataOnline Corp.)

- Digi International Inc.

- Otodata Wireless Network Inc.

- SkyBitz Inc.

- Powelectrics Ltd.

- Dunraven Systems Limited

- Endress+Hauser Group

- Honeywell International Inc.

- Vega Grieshaber KG

- RemoteTank(Alpha Wireless Automation, Inc.)

- Rugged Telemetry

- Tekelek Group

- Tank Utility, Inc.(Generac Power Systems, Inc.)

- Cavagna Group

- Angus Energy LLC

- Mistras Group, Inc.

第七章 市场机会与未来展望

The Remote Tank Monitoring System market is expected to grow from USD 2.49 billion in 2025 to USD 3.21 billion in 2026 and is forecast to reach USD 11.41 billion by 2031 at 28.9% CAGR over 2026-2031.

Solid growth reflects the widening adoption of industrial IoT, the maturation of satellite and LPWAN connectivity, and tighter environmental regulations that require continuous visibility into liquid storage. Sector participants are shifting from reactive maintenance to predictive asset management, and the resulting efficiency gains, lower truck rolls, tighter inventory control, and faster spill detection continue to draw both asset owners and insurers toward automated telemetry. Competitive differentiation now centers on software analytics that convert sensor data into actionable insights, while subscription-based Hardware-as-a-Service (HaaS) models reduce upfront cost barriers and accelerate the adoption of remote tank monitoring system solutions.

Global Remote Tank Monitoring System Market Trends and Insights

Expansion of Oil and Gas and Chemical Storage Infrastructure

IEA data showed global oil and gas storage capacity increasing by 12% in 2024 as firms built strategic reserves while pursuing energy transition goals . Chemical producers mirrored this pattern to buffer feedstock volatility, and both trends amplified demand for remote tank monitoring system market deployments. Operators favor scalable, multi-site platforms that integrate with existing SCADA systems and feed cloud analytics for portfolio-wide optimization. Vendors able to integrate satellite links and cellular backhaul now win multi-year frame agreements on heavy-capital projects.

Proliferation of Cloud-Based IoT Platforms

Microsoft Azure IoT and AWS IoT Core logged a 40% annual growth in industrial use cases by 2024, with tank telemetry among the fastest-growing add-on workloads. Cloud ingestion unlocks machine-learning leak detection, automated replenishment triggers, and predictive maintenance capabilities that were previously seldom possible in legacy SCADA systems. Mid-market operators tap subscription pricing to sidestep large CAPEX, further accelerating the uptake of remote tank monitoring system market solutions.

High Upfront Hardware and Integration Costs

A full sensor-to-cloud deployment can run USD 15,000-45,000 per tank, with integration often exceeding the hardware bill. SMEs managing a handful of tanks struggle to justify such spend. This restraint steers the remote tank monitoring system market toward modular kits and HaaS subscriptions, which shift costs from CAPEX to OPEX, allowing users to scale as ROI becomes evident.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Global Spill-Prevention and Inventory Regulations

- Satellite-IoT Coverage for Ultra-Remote Tanks

- Cyber-Security and Data-Ownership Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Point-level devices led the 2025 field with a 57.92% share, aided by low cost and simple binary alarms. Continuous-level platforms captured higher-value projects, and their 29.6% CAGR signals a shift toward always-on visibility, as demanded by regulatory audits and just-in-time logistics. Revenue linked to continuous installations is set to add USD 4 billion to the remote tank monitoring system market size between 2025 and 2030.

Spending is tilting toward high-resolution radar and guided-wave radar probes in pharmaceuticals and fine chemicals, where +-1 mm accuracy yields quality dividends. Point-level remains entrenched in propane and small industrial tanks, yet aging float switches increasingly give way to digital stick probes as OEMs bundle cloud dashboards by default.

Contact technologies delivered 61.55% of 2025 sales, but non-contact sensing is expected to outpace all other categories, driven by ultrasonic and FMCW radar that avoid fluid contact. The non-contact boom lifts' average selling prices and advanced signal processing software make it a new margin lever for vendors. Remote tank monitoring system adopters also cite lower maintenance costs, no wetted parts means fewer field visits, which compounds the IoT value in rural assets.

Optical and laser devices occupy premium niches such as sterile pharmaceutical batching. Meanwhile, mechanical tape gauges persist where visual redundancy is mandatory for insurance compliance, although digital retrofit kits now stream tape-float readings into SCADA to reduce manual dip checks.

The Remote Tank Monitoring System Market Report is Segmented by Monitoring Type (Point-Level, Continuous-Level), Technology (Contact Sensors, Non-Contact Sensors), Connectivity (Cellular, LPWAN, and More), Tank Type (Above-Ground Fixed-Roof, and More), Capacity (<10, 000 L, 10, 000 - 50, 000 L, and More), End-User Industry (Oil and Gas, Chemicals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained a 34.05% lead in 2025, driven by SPCC enforcement, extensive oil and gas infrastructure, and early industrial IoT adoption. Federal grants for rural broadband enhance LPWAN coverage, further propelling the deployment of remote tank monitoring systems in agricultural states. Canada's renewed strategic petroleum reserve buildout adds cross-border momentum as operators harmonize asset management platforms.

The Asia-Pacific region is expected to deliver the most rapid growth, with a 33.1% CAGR through 2031. Massive refinery and petrochemical expansions in China and India, alongside Southeast Asian mining projects, require real-time tank telemetry for both safety and ESG reporting purposes. Regional governments also roll out soil-and-water-protection rules mirroring OECD standards, compelling underground tank owners to adopt continuous monitoring.

Stringent environmental directives and industrial decarbonization programs underpin Europe's steady growth. Cloud dashboards that calculate Scope 3 emissions from bulk-liquid logistics are finding eager users among European majors seeking to meet their 2030 carbon-neutral targets. In parallel, the Middle East, Africa, and South America show rising potential for the remote tank monitoring system market as infrastructure investments in LNG, desalination, and mining unlock greenfield projects, although economic headwinds temper near-term volumes.

- Schneider Electric SE

- Emerson Electric Co.

- Banner Engineering Corp.

- ATEK Access Technologies, LLC (TankScan)

- Anova (DataOnline Corp.)

- Digi International Inc.

- Otodata Wireless Network Inc.

- SkyBitz Inc.

- Powelectrics Ltd.

- Dunraven Systems Limited

- Endress+Hauser Group

- Honeywell International Inc.

- Vega Grieshaber KG

- RemoteTank (Alpha Wireless Automation, Inc.)

- Rugged Telemetry

- Tekelek Group

- Tank Utility, Inc. (Generac Power Systems, Inc.)

- Cavagna Group

- Angus Energy LLC

- Mistras Group, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of oil and gas and chemical storage infrastructure

- 4.2.2 Proliferation of cloud-based IoT platforms

- 4.2.3 Stricter global spill-prevention and inventory regulations

- 4.2.4 Satellite-IoT coverage for ultra-remote tanks

- 4.2.5 HaaS subscription models lowering capex barriers

- 4.2.6 Scope-3 ESG reporting pressure on bulk-liquid supply chains

- 4.3 Market Restraints

- 4.3.1 High upfront hardware and integration costs

- 4.3.2 Cyber-security and data-ownership concerns

- 4.3.3 Steel/aluminum tariffs inflating device BOM

- 4.3.4 Battery-waste sustainability liabilities

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Monitoring Type

- 5.1.1 Point-Level Monitoring

- 5.1.2 Continuous-Level Monitoring

- 5.2 By Technology

- 5.2.1 Contact Sensors

- 5.2.1.1 Float and Tape Gauge

- 5.2.1.2 Magnetostrictive

- 5.2.1.3 Hydrostatic Pressure

- 5.2.2 Non-Contact Sensors

- 5.2.2.1 Ultrasonic

- 5.2.2.2 Radar/FMCW

- 5.2.2.3 Optical/Laser

- 5.2.1 Contact Sensors

- 5.3 By Connectivity

- 5.3.1 Cellular (4G LTE, 5G, NB-IoT, Cat-M)

- 5.3.2 LPWAN (LoRaWAN, Sigfox)

- 5.3.3 Satellite (LEO/GEO)

- 5.3.4 Short-Range RF/Wi-Fi/BLE

- 5.4 By Tank Type

- 5.4.1 Above-Ground Fixed-Roof

- 5.4.2 Above-Ground Floating-Roof

- 5.4.3 Underground/UST

- 5.5 By Capacity

- 5.5.1 <10,000 L

- 5.5.2 10,000 - 50,000 L

- 5.5.3 50,001 - 200,000 L

- 5.5.4 >200,000 L

- 5.6 By End-User Industry

- 5.6.1 Oil and Gas

- 5.6.2 Chemicals and Petrochemicals

- 5.6.3 Water and Wastewater

- 5.6.4 Food and Beverage

- 5.6.5 Agriculture and Irrigation

- 5.6.6 Power Generation

- 5.6.7 Mining and Metals

- 5.6.8 Pharmaceuticals and Healthcare

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Australia and New Zealand

- 5.7.4.6 Southeast Asia

- 5.7.4.7 Rest of Asia Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Kenya

- 5.7.6.4 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Emerson Electric Co.

- 6.4.3 Banner Engineering Corp.

- 6.4.4 ATEK Access Technologies, LLC (TankScan)

- 6.4.5 Anova (DataOnline Corp.)

- 6.4.6 Digi International Inc.

- 6.4.7 Otodata Wireless Network Inc.

- 6.4.8 SkyBitz Inc.

- 6.4.9 Powelectrics Ltd.

- 6.4.10 Dunraven Systems Limited

- 6.4.11 Endress+Hauser Group

- 6.4.12 Honeywell International Inc.

- 6.4.13 Vega Grieshaber KG

- 6.4.14 RemoteTank (Alpha Wireless Automation, Inc.)

- 6.4.15 Rugged Telemetry

- 6.4.16 Tekelek Group

- 6.4.17 Tank Utility, Inc. (Generac Power Systems, Inc.)

- 6.4.18 Cavagna Group

- 6.4.19 Angus Energy LLC

- 6.4.20 Mistras Group, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

汽车用液氢市场:2026-2032年全球市场预测(按氢形态、储存技术、加氢基础设施、车辆类型、应用和最终用户划分)

汽车用液氢市场:2026-2032年全球市场预测(按氢形态、储存技术、加氢基础设施、车辆类型、应用和最终用户划分) 全球国防外挂油箱市场:2026-2036LNG驳船加註系统市场按组件、安装类型、推进类型、驳船类型、应用和最终用户划分,全球预测(2026-2032年)

全球国防外挂油箱市场:2026-2036LNG驳船加註系统市场按组件、安装类型、推进类型、驳船类型、应用和最终用户划分,全球预测(2026-2032年) 自供电水质监测系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及功能划分卡车加油系统市场按组件、燃料类型、技术、支付方式、最终用途和车辆类型划分-全球预测(2026-2032 年)

自供电水质监测系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及功能划分卡车加油系统市场按组件、燃料类型、技术、支付方式、最终用途和车辆类型划分-全球预测(2026-2032 年) 液气储槽:全球市占率及排名、总收入及需求预测(2025-2031 年)

液气储槽:全球市占率及排名、总收入及需求预测(2025-2031 年) 全球油轮服务市场远端油罐监控系统的全球市场

全球油轮服务市场远端油罐监控系统的全球市场 二轮车燃料箱市场规模、份额、成长分析(按产能、材料类型、最终用户和地区)- 产业预测,2025 年至 2032 年全球折迭式燃料箱市场

二轮车燃料箱市场规模、份额、成长分析(按产能、材料类型、最终用户和地区)- 产业预测,2025 年至 2032 年全球折迭式燃料箱市场