|

市场调查报告书

商品编码

1940780

亚太地区设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Asia Pacific Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

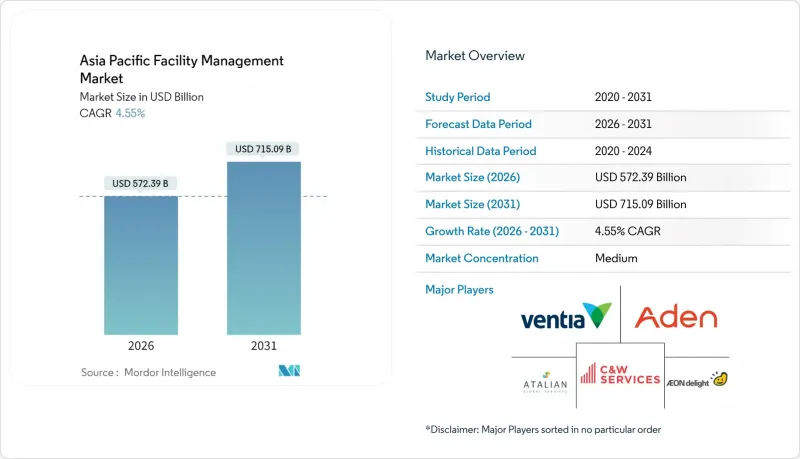

亚太地区设施管理市场在 2025 年的价值为 5,474.8 亿美元,预计到 2031 年将达到 7,150.9 亿美元,而 2026 年为 5,723.9 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.55%。

区域需求受到日益严格的ESG合规要求、资料中心快速部署以及人工智慧驱动的楼宇管理系统日益普及的支撑。儘管硬性服务仍占据支出的大部分,但随着租户对职场体验和安全性的日益重视,软性服务正逐渐获得发展动力。外包业务在营运复杂性不断增加的背景下稳步成长,但供应链成本上涨和监管差异等宏观不利因素限制了其短期成长。

亚太地区设施管理市场趋势与洞察

楼宇管理外包日益增多

企业房地产团队正从分散的内部模式转向整合式外包,从而获得监管、数位化和永续性的专业知识。世邦魏理仕 (CBRE) 报告称,其设施管理业务在 2025 年第一季的收入净额年增 16%,主要得益于科技、医疗保健和生命科学行业的客户成长。整合式服务协议简化了供应商管理,并将绩效与可衡量的结果挂钩。 ISS 与柏克莱续签的五年全球合约显示了跨区域捆绑式服务的吸引力。在劳动力短缺的市场,例如日本和新加坡,外包的采用尤其显着,这些市场老化的劳动力凸显了外部技术专长的价值。拥有合规认证和数位化可追踪服务品质的本地供应商正在获得竞争优势。中期来看,随着数位化平台实现透明的成本基准分析并支援按绩效付费的定价模式,外包的采用率预计将继续成长。

安全保障的需求日益增长

世界各国政府都在收紧职场安全法规,迫使企业升级其监控和培训通讯协定。在新加坡,2025 年《机械和可燃粉尘法规》将提高合规要求,从而推动对具备即时风险分析技能的专业设施合作伙伴的需求。人工智慧设备,例如能够检测溢出物和冷凝水的混合式地面湿度感测器,正从试点阶段走向主流部署,UnaBiz Singapore 的 2024 年部署计画就体现了这一点。拥有多个办公地点的公司需要统一的仪錶板,以实现跨司法管辖区的数据标准化,同时遵守当地的报告法规。拥有成熟的数位安全解决方案的营运商可以实现预测性事故预防,从而帮助降低保险费和停机成本。对员工福祉日益增长的关注,正推动着在人口密集的城市园区内加大对门禁系统、室内空气品质感测器和智慧疏散系统的投资。

高昂的实施成本

对于中型物业而言,智慧建筑硬体、软体许可和合规方面的初始投资可能超过30万美元,这给中小业主带来了采用该技术的障碍。不断上涨的资本和人事费用进一步延长了投资回收期。然而,先导计画始终能够实现两位数的节能效果。即使是整合基于物联网的预测性维护的製造商,也需要两到三年的投资回收期,例如Azbil公司在印尼PT. Aspex Kumbong公司的实施案例。许多租户为了管理现金流而分阶段实施,但部分部署限制了完全整合平台的协同效应。提供按绩效付费或资产即服务模式的营运商可以缓解这一障碍,但该地区中小企业的财务限制使得成本成为市场扩张的最大限制因素。

细分市场分析

随着雇主优先考虑员工体验指标并采用人工智慧辅助的安保、礼宾和清洁解决方案,软性服务预计将以更快的速度成长,到2031年将维持6.05%的复合年增长率。亚太地区设施管理市场的软性服务板块正受益于日常清洁中机器人的应用以及将占用率分析整合到服务台应用程式中。在新加坡、东京和雪梨等地的高端办公空间竞标中,非接触式访客管理系统和基于人工智慧的监控系统已成为必备条件。同时,将食品分析数据与采购系统连结的先进餐饮平台在企业园区中越来越受欢迎,因为它们有助于推广健康计画。

到2025年,硬体服务将维持55.72%的收入份额,这主要得益于关键基础设施维护,例如机电(MEP)、暖通空调(HVAC)和消防系统。预测分析正在创造新的价值:例如,Yamaha Motor Co, Ltd.的机器人自动化(降低了60%的工厂人事费用)等应用案例正在提升亚太地区设施管理领域机电供应商的市场份额。在曼谷瑞吉酒店试点计画中,人工智慧优化的冷却器实现了9%的节能效果并延长了设备使用寿命,吸引了业主和能源服务公司的注意。消防系统供应商正在将物联网感测器与云端仪錶板结合,以从基于巡检的模式转向即时风险缓解。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 目前运转率

- 主要FM业者的盈利能力

- 劳动指标 - 劳动参与率

- 按服务类型分類的设施管理市场占有率(%)

- 按硬体服务分類的设施管理市场占有率(%)

- 以软性服务分類的设施管理市场占有率(%)

- 主要都会区的都市化和人口成长

- 亚太地区基础设施管道投资优先事项(按行业划分)

- 与劳动和安全标准相关的监管因素

- 市场驱动因素

- 楼宇管理外包日益增多

- 日益增长的安全需求

- 设施管理的技术进步

- 推出以ESG主导的绿建筑认证

- 亚太地区资料中心建设扩张

- 生命科学和医疗保健设施的激增需要专业的设施管理服务

- 市场限制

- 高昂的实施成本

- 各国监管标准分散

- 传统设施管理客户的数位化成熟度较低

- 短期设施管理合约条款限制了长期投资回报。

- 价值链分析

- PESTEL 分析

- 新参与企业的监管和法律体制

- 宏观经济指标对FM需求的影响

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资与资金筹措分析

第五章 市场规模与成长预测

- 按服务类型

- 硬服务

- 资产管理

- 机电及暖通空调服务

- 消防系统和安全措施

- 其他硬体维修服务

- 软服务

- 办公室支援与安全

- 清洁服务

- 餐饮服务

- 其他软性调频服务

- 硬服务

- 按规定表格

- 内部

- 外包

- 单频调频

- 捆绑式设施管理

- 综合设施管理

- 按最终用户行业划分

- 商业(IT/通讯、零售/仓储)

- 餐饮服务业(饭店、餐厅、大型餐厅)

- 公共及公共基础设施(政府、教育、交通)

- 医疗保健(公立和私立机构)

- 工业和流程工业(製造业、能源业、采矿业)

- 其他终端用户产业(多用户住宅、娱乐、运动和休閒)

- 按国家/地区

- 中国

- 印度

- 日本

- 韩国

- 印尼

- 泰国

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 策略发展与伙伴关係

- 市占率分析

- 公司简介

- Aden Group

- Aeon Delight Co. Ltd(AEON Co. Ltd)

- ATALIAN Global Services

- Broadspectrum(Ventia)

- CBRE Group Inc.

- C&W Facility Services Inc.

- Commercial Building Maintenance Corp.

- CPG Corporation

- Cushman & Wakefield plc

- DTSS Facility Services

- EMCOR Group Inc.

- G4S Facilities Management

- ISS Facility Services

- Jones Lang LaSalle(JLL)

- OCS Group International Ltd.

- Sodexo SA

- UEMS Solutions

第七章 市场机会与未来展望

The Asia Pacific facility management market was valued at USD 547.48 billion in 2025 and estimated to grow from USD 572.39 billion in 2026 to reach USD 715.09 billion by 2031, at a CAGR of 4.55% during the forecast period (2026-2031).

Regional demand is anchored in stricter ESG compliance, rapid data-center roll-outs, and the uptake of AI-enabled building operating systems. Hard services continue to dominate spend, yet soft services are gaining momentum as occupiers elevate workplace experience and security priorities. Outsourcing grows steadily on the back of rising operational complexity, while macro headwinds such as supply-chain cost inflation and uneven regulation temper near-term expansion.

Asia Pacific Facility Management Market Trends and Insights

Rising Outsourcing in Building Management

Corporate real-estate teams are shifting from fragmented in-house models toward integrated outsourcing to access specialized regulatory, digital, and sustainability expertise. CBRE reported 16% year-on-year net-revenue growth in its facilities-management segment for Q1 2025, with technology, healthcare, and life-science clients as primary contributors. Integrated service contracts simplify vendor management and link performance to measurable outcomes, with the five-year renewal of ISS's global agreement with Barclays illustrating the appeal of bundled, cross-regional delivery. Outsourcing uptake is especially strong in labor-constrained markets such as Japan and Singapore, where aging workforces elevate the value of external technical specialists. Local providers that demonstrate compliance credentials and digitally traceable service quality are gaining competitive advantages. Over the medium term, outsourcing penetration is expected to climb as digital platforms enable transparent cost benchmarking and support pay-for-performance pricing models.

Heightened Safety and Security Needs

Governments are tightening workplace-safety statutes, compelling occupiers to upgrade monitoring and training protocols. Singapore's 2025 regulations on machinery and combustible dust have raised compliance thresholds, driving demand for specialist facility partners versed in real-time risk analytics. AI-enabled devices such as hybrid floor-wetness sensors that detect spills or condensation are moving from pilot to mainstream deployment, as demonstrated by UnaBiz Singapore's 2024 launch.Multisite corporates require unified dashboards that normalize data across jurisdictions while honoring local reporting rules. Providers with mature digital safety suites can deliver predictive incident prevention, lowering insurance premiums and downtime costs. The heightened focus on employee well-being fuels incremental spend on access control, indoor-air quality sensors, and smart-evacuation systems across dense urban campuses.

High Implementation Costs

Up-front capital for smart-building hardware, software licenses, and compliance upgrades can exceed USD 300,000 for a mid-size property, creating adoption hurdles for small and mid-tier owners. Inflation in equipment and labor costs further stretches payback timelines, even though pilot projects regularly demonstrate double-digit energy reductions. Manufacturers integrating IoT-based predictive maintenance still face recovery periods of two to three years, as illustrated by Azbil Corporation's deployment at PT. Aspex Kumbong in Indonesia. Many occupiers sequence implementations in phases to manage cash flow, but partial roll-outs limit the synergy gains of fully integrated platforms. Providers that structure outcome-based pricing or equipment-as-a-service models can mitigate the barrier, yet balance-sheet limitations among regional SMEs keep cost as the most immediate drag on market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Facility Management

- ESG-Driven Green Building Certification Adoption

- Fragmented Regulatory Standards Across Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft services generated faster expansion, recording a 6.05% CAGR through 2031 as employers elevate employee-experience metrics and deploy AI-assisted security, concierge, and cleaning solutions. The Asia Pacific facility management market size for soft services is benefiting from the rollout of robotics for routine cleaning and the integration of occupancy analytics into help-desk applications. Contactless visitor management and AI-based surveillance systems now form mandatory bid requirements in high-grade offices across Singapore, Tokyo, and Sydney. In parallel, advanced catering platforms that link dietary analytics to procurement systems are gaining popularity in corporate campuses looking to meet wellness commitments.

Hard services retained 55.72% revenue share in 2025, supported by critical infrastructure maintenance including MEP, HVAC, and fire-safety systems. Predictive analytics adds new value layers: the Asia Pacific facility management market share for MEP providers is reinforced by use cases such as Yamaha Motor's robotic automation, which has cut factory labor costs by 60%. AI-optimized chillers, exemplified by the St. Regis Bangkok pilot, showcase measurable 9% energy savings and extend equipment life cycles, drawing interest from both owners and energy-service companies. Fire-system vendors are bundling IoT sensors with cloud dashboards to transition from inspection-based models to real-time risk mitigation.

Asia-Pacific Facility Management Market Report is Segmented by Service Type (Hard Services, Soft Services), Offering Type (In-House, Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More), and Geography (China, India, Japan, Korea, Indonesia, Thailand, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Aden Group

- Aeon Delight Co. Ltd (AEON Co. Ltd)

- ATALIAN Global Services

- Broadspectrum (Ventia)

- CBRE Group Inc.

- C&W Facility Services Inc.

- Commercial Building Maintenance Corp.

- CPG Corporation

- Cushman & Wakefield plc

- DTSS Facility Services

- EMCOR Group Inc.

- G4S Facilities Management

- ISS Facility Services

- Jones Lang LaSalle (JLL)

- OCS Group International Ltd.

- Sodexo S.A.

- UEMS Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Current Occupancy Rates

- 4.1.2 Profitability Rates of Major FM Players

- 4.1.3 Workforce Indicators - Labor Participation

- 4.1.4 Facility Management Market Share (%) by Service Type

- 4.1.5 Facility Management Market Share (%) by Hard Services

- 4.1.6 Facility Management Market Share (%) by Soft Services

- 4.1.7 Urbanization and Population Growth in Major Metros

- 4.1.8 Sector Investment Priorities in Asia Pacific Infrastructure Pipeline

- 4.1.9 Regulatory Drivers Specific to Labour and Safety Standards

- 4.2 Market Driver

- 4.2.1 Rising Outsourcing in Building Management

- 4.2.2 Heightened Safety and Security Needs

- 4.2.3 Technological Advancements in Facility Management

- 4.2.4 ESG-Driven Green Building Certification Adoption

- 4.2.5 Expansion of Data Centre Construction Across Asia-Pacific

- 4.2.6 Proliferation of Life-Sciences and Healthcare Facilities Requiring Specialized FM Services

- 4.3 Market Restraint

- 4.3.1 High Implementation Costs

- 4.3.2 Fragmented Regulatory Standards Across Countries

- 4.3.3 Low Digital Maturity Among Traditional FM Clients

- 4.3.4 Short FM Contract Tenures Limiting Long-Term Investment Payback

- 4.4 Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 Korea

- 5.4.5 Indonesia

- 5.4.6 Thailand

- 5.4.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aden Group

- 6.4.2 Aeon Delight Co. Ltd (AEON Co. Ltd)

- 6.4.3 ATALIAN Global Services

- 6.4.4 Broadspectrum (Ventia)

- 6.4.5 CBRE Group Inc.

- 6.4.6 C&W Facility Services Inc.

- 6.4.7 Commercial Building Maintenance Corp.

- 6.4.8 CPG Corporation

- 6.4.9 Cushman & Wakefield plc

- 6.4.10 DTSS Facility Services

- 6.4.11 EMCOR Group Inc.

- 6.4.12 G4S Facilities Management

- 6.4.13 ISS Facility Services

- 6.4.14 Jones Lang LaSalle (JLL)

- 6.4.15 OCS Group International Ltd.

- 6.4.16 Sodexo S.A.

- 6.4.17 UEMS Solutions

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

设施管理市场:2026-2032年全球市场预测(依产品、产品模式、部署类型、公司规模及最终用途划分)

设施管理市场:2026-2032年全球市场预测(依产品、产品模式、部署类型、公司规模及最终用途划分) 设施管理市场规模、份额、趋势和预测:按解决方案、服务、部署类型、组织规模、行业和地区划分,2026-2034 年设施管理服务市场:2026-2032年全球市场预测(依服务类型、合约类型、服务交付方式、最终用户和组织规模划分)

设施管理市场规模、份额、趋势和预测:按解决方案、服务、部署类型、组织规模、行业和地区划分,2026-2034 年设施管理服务市场:2026-2032年全球市场预测(依服务类型、合约类型、服务交付方式、最终用户和组织规模划分) 2026年全球地下设施维护与管理市场报告2026年全球硬性服务设施管理市场报告2026年全球设施支援服务市场报告2026年全球设施管理服务市场报告2026年全球软性服务设施管理市场报告

2026年全球地下设施维护与管理市场报告2026年全球硬性服务设施管理市场报告2026年全球设施支援服务市场报告2026年全球设施管理服务市场报告2026年全球软性服务设施管理市场报告 设施管理市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测硬设施管理市场:依服务类型、合约类型、所有权类型和最终用户产业划分-2026-2032年全球市场预测

设施管理市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测硬设施管理市场:依服务类型、合约类型、所有权类型和最终用户产业划分-2026-2032年全球市场预测