|

市场调查报告书

商品编码

1940781

亚太地区资料中心市场占有率分析、产业趋势与统计、成长预测(2026-2031)Asia-Pacific Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

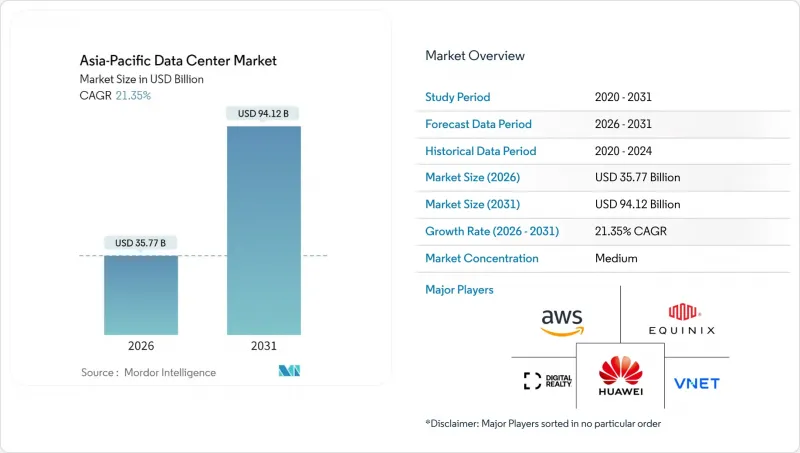

预计到 2026 年,亚太地区资料中心市场规模将达到 357.7 亿美元。

这意味着从 2025 年的 294.7 亿美元成长到 2031 年的 941.2 亿美元,2026 年至 2031 年的复合年增长率为 21.35%。

就装置容量而言,预计市场规模将从2025年的29,310兆瓦成长到2030年的63,110兆瓦,在预测期(2025-2030年)内复合年增长率(CAGR)为16.57%。市场占有率和估计值均以兆瓦(MW)为单位计算和报告。 5G的快速部署、人工智慧/机器学习(AI/ML)工作负载的爆炸性增长以及资料主权法规的推动,使得亚太地区资料中心容量在短短五年内翻了一番,使其成为全球增长最快的数位基础设施领域。为了满足高功率密度工作负载和日益严格的效率要求,营运商正在迅速采用液冷技术、推广可再生能源并发展海底电缆连接。中国目前以34.58%的市占率主导,但印度20.50%的复合年增长率表明,市场需求正在显着向南亚转移。虽然託管仍然是主流服务模式,但以中国云端巨头主导的超大规模建设浪潮正在重塑竞争格局,因为企业正在仔细权衡成本、延迟和合规性之间的利弊。

亚太数据中心市场趋势与洞察

加速部署5G核心网络

5G的扩展正在重塑亚太资料中心市场的工作负载部署格局。到2024年,中国将拥有超过338万个5G基地台,每个基地台的延迟要求低于20毫秒,通讯业者在人口中心附近的基地台边缘设施中部署这些基地台。在日本,通讯业者在2024年投资1.2兆日圆用于5G基础设施建设,以支持製造业和娱乐业的超低延迟应用。这正在加速本地对分散式运算节点的需求。新加坡的5G覆盖率已达到95%,并且强制要求关键服务进行本地处理的政策正在推动新的边缘部署。这种流量分散使得中型设施的成长速度超过了大型资料中心。网路回程传输合作伙伴关係和模组化设计正成为通讯业者租户的关键差异化因素。

中国科技巨头加大对自有超大规模建筑的投资

阿里巴巴、腾讯和位元组跳动正将云端基础设施预算转向建造自有园区,以优化成本并遵守当地法规。阿里巴巴已累计280亿美元用于2027年建造新的区域,其中60%将用于自有设施。位元组跳动已投资72亿美元用于大规模语言模型训练的人工智慧设计,而腾讯则投资58亿美元在东南亚为游戏玩家建造水冷资料中心。这一成长推动了亚太数据中心市场的超大规模细分领域,同时也加剧了零售託管市场的价格竞争。现有企业正透过扩展服务组合(例如云端间互联、託管GPU丛集和合规即服务)来捍卫市场份额。

漫长的併网核准过程

在高速成长的市场中,併网延误会延长计划的投资回收期。在印度,由于各邦委员会需要审查环境影响和电网稳定性,核准平均需要18到24个月。印尼国家电力公司(PLN)对10兆瓦以上的负载也设定了类似的审批时限,而菲律宾的可再生能源认证强制令将使审批流程延长至多一年。开发商被迫承担閒置土地成本和仓储设施折旧免税额,这降低了内部收益率(IRR),并减缓了亚太地区资料中心市场的容量扩张。

细分市场分析

到2031年,中型资料中心将以12.90%的复合年增长率成长,通讯业者和CDN供应商将优先建造5-20MW的节点用于都市区流量聚合。大型园区仍将占据亚太资料中心市场30.62%的份额,全球云端租户因其规模经济优势而选择它们。大型(100MW以上)枢纽将作为区域核心,支援人工智慧训练,而小规模设施将满足特定企业和偏远地区的需求。随着5G网路的不断密集化,即使大型企划主导资本投资,分散式架构也将继续推动对中型资料中心的需求。

亚太地区的资料中心产业正日益采用星型拓朴结构,大型枢纽提供高密度运算能力,中型卫星则确保网路边缘的低延迟。主要城市的电力和土地资源限制促使企业将土地购买策略转向大阪、海德拉巴和新山等二线城市。对投资人而言,分散投资组合,投资不同规模的资料中心,可以降低对单一地点电力瓶颈的依赖。

截至2025年,Tier 3级资料中心将占据亚太地区资料中心市场62.35%的份额,并提供99.982%的运转率,许多公司认为这一水准足以满足需求,无需承担Tier 4级资料中心的额外成本。新加坡金融管理局等监管机构对金融资料居住的要求强制要求使用Tier 3级及以上级别的资料中心,这进一步巩固了市场需求。 Tier 1级和Tier 2级资料中心主要服务于开发和测试工作负载,而Tier 4级资料中心则专用于关键支付系统和某些政府云端平台。

标准化的三级(Tier 3)设计图缩短了审批时间,并允许使用预製构件,从而将工期缩短高达 20%。符合 ISO 27001 标准也进一步简化了认证流程。因此,随着人工智慧推动货架密度的提高,同时营运商仍需专注于成本,三级(Tier 3)有望进一步巩固主导地位。

亚太地区资料中心市场报告按资料中心规模(大型、超大型、中型、巨型、小规模)、等级(Tier 1-2、Tier 3、Tier 4)、资料中心类型(超大规模/自建、企业/边缘、託管)、最终用户(银行、金融服务和保险 (BFSI)、IT 及 ITES、电子商务、政府、製造业、媒体和娱乐等地区进行细分。市场预测以 IT 负载容量(兆瓦)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义 - 研究范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加速部署5G核心网络

- 中国主要科技公司加大对超大规模建设的投资

- 政府为绿色资料中心提供税收奖励

- AI/ML工作负载对本地GPU丛集的需求快速成长

- 快速整合海底电缆登陆站和边缘设施

- 主权财富基金倾向于客製化建造模式

- 市场限制

- 延长併网核准流程

- 中国北方面临严重的水资源短缺风险

- 亚太地区一线城市房地产成本不断上涨

- 认证资料中心技术人员短缺

- 市场展望

- IT负载能力

- 高架地板面积

- 託管收入

- 预装机架

- 机架空间利用率

- 海底电缆

- 主要行业趋势

- 智慧型手机用户

- 每部智慧型手机的资料通讯

- 行动资料通讯速度

- 宽频资料传输速度

- 光纤连接网路

- 法律规范

- 中国

- 日本

- 印度

- 印尼

- 澳洲

- 新加坡

- 纽西兰

- 马来西亚

- 泰国

- 亚太其他地区

- 价值炼和通路分析

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(兆瓦)

- 按资料中心规模

- 大规模

- 巨大的

- 中号

- 百万

- 小规模

- 依层级类型

- 一级和二级

- 三级

- 第四级

- 依资料中心类型

- 超大规模/内部建设

- 企业/边缘运算

- 搭配

- 未使用的

- 使用

- 零售共址

- 批发託管

- 最终用户

- BFSI

- 资讯科技与资讯科技服务

- 电子商务

- 政府

- 製造业

- 媒体与娱乐

- 沟通

- 其他最终用户

- 按国家/地区

- 中国

- 日本

- 印度

- 印尼

- 澳洲

- 新加坡

- 纽西兰

- 马来西亚

- 泰国

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amazon Web Services, Inc

- Equinix, Inc.

- Alibaba Cloud

- Chindata Group Holdings Ltd

- AirTrunk Operating Pty Ltd

- Space DC Pte Ltd

- NTT Ltd

- Huawei Cloud Computing Technologies Co., Ltd

- Global Data Solutions Co., Ltd.(GDS)

- Google Inc

- LG Uplus Corp

- Range Technology Development Co., Ltd

- NEXTDC Limited

- Digital Realty Trust Inc.

- Beijing VNET Broadband Data Center Co., Ltd

第七章 市场机会与未来展望

Asia-Pacific Data Center Market size in 2026 is estimated at USD 35.77 billion, growing from 2025 value of USD 29.47 billion with 2031 projections showing USD 94.12 billion, growing at 21.35% CAGR over 2026-2031.

In terms of installed base, the market is expected to grow from 29.31 thousand megawatt in 2025 to 63.11 thousand megawatt by 2030, at a CAGR of 16.57% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. Rapid 5G roll-outs, AI/ML workload proliferation, and data-sovereignty regulations are doubling capacity in just five years, making the Asia Pacific Data Center market the world's fastest-growing digital-infrastructure arena. Operators are racing to integrate liquid cooling, renewable-energy sourcing, and submarine-cable landing connectivity to satisfy power-dense workloads while meeting increasingly stringent efficiency mandates. China currently dominates with 34.58% share, yet India's 20.50% CAGR signals a seismic rebalancing of demand toward South Asia. Colocation remains the prevailing service model, but the hyperscale self-build wave led by Chinese cloud giants is redrawing the competitive map as enterprises weigh cost, latency, and compliance trade-offs.

Asia-Pacific Data Center Market Trends and Insights

Accelerating Roll-out of 5G Core Networks

Widespread 5G adoption is reshaping workload-placement economics across the Asia Pacific Data Center market. China surpassed 3.38 million 5G base stations in 2024, each requiring sub-20 ms latency, thereby pushing operators to position medium-sized edge facilities nearer to population centers . In Japan, carriers injected JPY 1.2 trillion into 5G infrastructure during 2024 to enable ultra-low-latency applications across manufacturing and entertainment, catalyzing regional demand for distributed compute nodes. Singapore achieved 95% 5G coverage and stipulated local processing for critical services, a policy that accelerates new edge builds . The resulting traffic dispersion explains why medium facilities are growing faster than mega sites. For developers, network-backhaul partnerships and modular designs have emerged as key differentiators when courting telecom tenants.

Rising Hyperscale Self-build Investments by Chinese Tech Majors

Alibaba, Tencent, and ByteDance are redirecting cloud-infrastructure budgets toward in-house campuses to optimize costs and comply with localization rules. Alibaba earmarked USD 28 billion for new regional builds through 2027, allocating 60% to self-operated estates . ByteDance dedicated USD 7.2 billion to AI-ready designs that support large-language-model training, while Tencent invested USD 5.8 billion in liquid-cooled sites targeting Southeast Asian gamers. The surge is boosting the Asia Pacific Data Center market's hyperscale segment yet intensifying pricing pressure on retail colocation. Incumbents are responding with deeper service portfolios-inter-cloud interconnects, managed GPU clusters, and compliance-as-a-service-to defend share.

Prolonged Grid-Connection Approval Cycles

Connection delays extend project payback periods in high-growth markets. Indian approvals average 18-24 months as state boards scrutinize environmental impact and grid stability Indonesia's PLN imposes similar timelines for >10 MW loads, and the Philippines' renewable-certificate mandate lengthens processing by up to a year. Developers shoulder idle-land costs and warehoused equipment depreciation, dampening IRRs and slowing the Asia Pacific Data Center market's capacity ramp.

Other drivers and restraints analyzed in the detailed report include:

- Government Tax-holiday Incentives for Green Data Centers

- Surging AI/ML Workload Demand for On-prem GPU Clusters

- Shortage of Certified Data center Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium-scale sites posted 12.90% CAGR through 2031 as telecom and CDN providers prioritize 5- to 20-MW nodes for metro-edge traffic aggregation. Large campuses still hold 30.62% share of the Asia Pacific Data Center market size, favored by global cloud tenants for economies of scale. Massive (>100 MW) hubs function as regional cores supporting AI training, while small facilities serve niche enterprise or remote-area requirements. As 5G densification continues, decentralized architectures will keep propelling medium-site demand, even as mega-projects dominate capital deployed.

The Asia Pacific Data Center industry increasingly embraces a hub-and-spoke topology: massive hubs supply high-density compute, and medium satellites ensure latency compliance at the network edge. Power and land constraints in primary cities are prompting land-banking strategies in secondary metros such as Osaka, Hyderabad, and Johor Bahru. For investors, portfolio diversification across size classes reduces exposure to single-site utility bottlenecks.

Tier 3 captured 62.35% share of the Asia Pacific Data Center market size in 2025, offering the 99.982% uptime most enterprises deem sufficient without tier 4's cost premium. Mandates from regulators like Singapore's Monetary Authority require tier 3 minimums for financial data residency, cementing demand. Tier 1 and tier 2 attract dev-test workloads, while tier 4 stays confined to critical clearing-house systems and select government clouds.

Standardized tier 3 blueprints shorten permitting cycles and enable prefabricated component use, trimming build schedules by up to 20%. ISO 27001 alignment further streamlines certification. Consequently, tier 3 will likely widen its leadership as AI spurs higher rack densities yet operators remain cost-sensitive.

The Asia Pacific Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, and More), and Geography. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Amazon Web Services, Inc

- Equinix, Inc.

- Alibaba Cloud

- Chindata Group Holdings Ltd

- AirTrunk Operating Pty Ltd

- Space DC Pte Ltd

- NTT Ltd

- Huawei Cloud Computing Technologies Co., Ltd

- Global Data Solutions Co., Ltd. (GDS)

- Google Inc

- LG Uplus Corp

- Range Technology Development Co., Ltd

- NEXTDC Limited

- Digital Realty Trust Inc.

- Beijing VNET Broadband Data Center Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition - Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating roll-out of 5G core networks

- 4.2.2 Rising hyperscale self-build investments by Chinese tech majors

- 4.2.3 Government tax-holiday incentives for green data centers

- 4.2.4 Surging AI/ML workload demand for on-prem GPU clusters

- 4.2.5 Rapid integration of submarine-cable landing stations with edge facilities

- 4.2.6 Build-to-suit models preferred by sovereign wealth funds

- 4.3 Market Restraints

- 4.3.1 Prolonged grid connection approval cycles

- 4.3.2 Pronounced water scarcity risk in Northern China

- 4.3.3 High real-estate cost inflation in tier-one Asia-Pacific cities

- 4.3.4 Shortage of certified data-center engineers

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.5.6.1 China

- 4.5.6.2 Japan

- 4.5.6.3 India

- 4.5.6.4 Indonesia

- 4.5.6.5 Australia

- 4.5.6.6 Singapore

- 4.5.6.7 New Zealand

- 4.5.6.8 Malaysia

- 4.5.6.9 Thailand

- 4.5.6.10 Rest of Asia Pacific

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MW)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale/Self-built

- 5.3.2 Enterprise/Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Indonesia

- 5.5.5 Australia

- 5.5.6 Singapore

- 5.5.7 New Zealand

- 5.5.8 Malaysia

- 5.5.9 Thailand

- 5.5.10 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services, Inc

- 6.4.2 Equinix, Inc.

- 6.4.3 Alibaba Cloud

- 6.4.4 Chindata Group Holdings Ltd

- 6.4.5 AirTrunk Operating Pty Ltd

- 6.4.6 Space DC Pte Ltd

- 6.4.7 NTT Ltd

- 6.4.8 Huawei Cloud Computing Technologies Co., Ltd

- 6.4.9 Global Data Solutions Co., Ltd. (GDS)

- 6.4.10 Google Inc

- 6.4.11 LG Uplus Corp

- 6.4.12 Range Technology Development Co., Ltd

- 6.4.13 NEXTDC Limited

- 6.4.14 Digital Realty Trust Inc.

- 6.4.15 Beijing VNET Broadband Data Center Co., Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

2026年全球智慧客户资料中心市场报告2026年全球网路资料中心(IDC)市场报告2026年全球资料中心房地产市场报告

2026年全球智慧客户资料中心市场报告2026年全球网路资料中心(IDC)市场报告2026年全球资料中心房地产市场报告 资料中心市场:按组件、资料中心类型、层级、冷却方式、电源、最终用户和组织规模划分-2026年至2032年全球市场预测

资料中心市场:按组件、资料中心类型、层级、冷却方式、电源、最终用户和组织规模划分-2026年至2032年全球市场预测 全球在轨资料中心市场预测(至2034年)-按平台、组件、系统、连接类型、应用、最终用户和地区分類的分析

全球在轨资料中心市场预测(至2034年)-按平台、组件、系统、连接类型、应用、最终用户和地区分類的分析 资料中心汇流排市场规模、份额和成长分析:按导体材料、绝缘类型、额定功率、安装/整合方法、资料中心类型和地区划分-2026-2033年产业预测2026年全球客製化资料中心市场报告

资料中心汇流排市场规模、份额和成长分析:按导体材料、绝缘类型、额定功率、安装/整合方法、资料中心类型和地区划分-2026-2033年产业预测2026年全球客製化资料中心市场报告 资料中心能源概况 - Oracle:自 2019 年以来,能源使用量以 24% 的复合年增长率成长,由于可再生能源的使用,排放保持稳定,但 Stargate 专案可能会大幅增加碳足迹。

资料中心能源概况 - Oracle:自 2019 年以来,能源使用量以 24% 的复合年增长率成长,由于可再生能源的使用,排放保持稳定,但 Stargate 专案可能会大幅增加碳足迹。 氢动力资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、功能、安装模式资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、解决方案

氢动力资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、功能、安装模式资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、解决方案