|

市场调查报告书

商品编码

1940784

交流电机(AC马达):市场份额分析、行业趋势和统计数据、成长预测(2026-2031年)Alternating Current (AC) Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

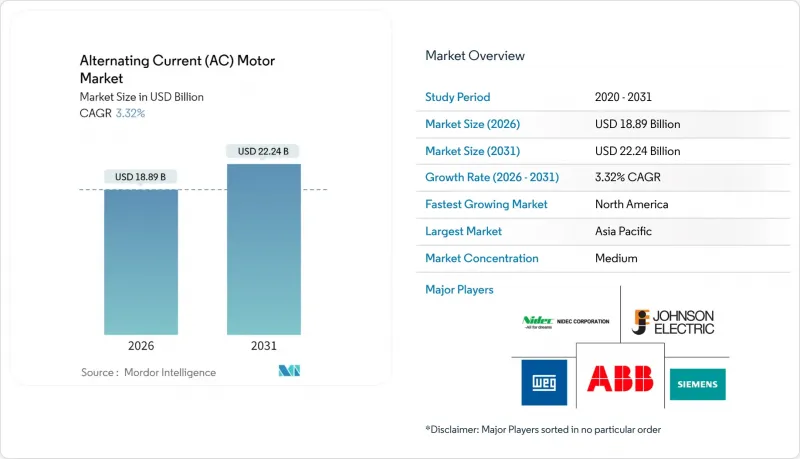

预计到 2026 年,AC马达马达市场价值将达到 188.9 亿美元,从 2025 年的 182.9 亿美元成长到 2031 年的 222.4 亿美元。

预计2026年至2031年年复合成长率(CAGR)为3.32%。

这一成长轨迹更受到IE3和IE4法规驱动的能源效率提升驱动型设备更新换代週期的影响,而非新增产能。在离散製造、可再生能源和暖通空调(HVAC)领域,高效节能设计的应用日益普及,亚洲的自动化项目和北美地区的回流生产也支撑了基准需求。为因应原物料价格波动和半导体短缺,供应商的策略围绕着铜绕组、电工钢和电力电子领域的垂直整合。虽然石油和天然气等成熟的终端用户领域仍然是收入的主要来源,但成长速度更快的领域正转向水处理、资料中心和风力发电机辅助设备,这些领域全生命週期的节能效益足以支撑其溢价。

全球交流电机市场趋势与洞察

强制性节能法规推动了高端引擎的普及

IE3 已成为全球最低标准,而 IE4 在欧洲和美国的普及速度正在加快,这有效地将老旧、效率较低的型号从采购清单中剔除。为了满足更严格的损耗限制,製造商正在升级工厂,配备自动化迭片压机生产线和精密磁铁组装。这种转变给缺乏资金投资新模具的小型区域性公司带来了压力,同时也加剧了市场集中度,使其集中在成熟的全球企业手中。采购团队现在会在 75% 和 50% 的负载点评估马达的满载效率,这增强了永磁同步马达设计的价值提案。符合公用事业公司高额电机补贴条件的终端用户可以将投资回收期缩短至两年以内,这进一步推动了监管改革的进程。

工业自动化推动了对中功率马达的需求

汽车、电子和物流企业正在扩大协作机器人规模,这需要功率在 1-100kW 之间的精密马达。配备编码器的伺服同步马达能够提供机器人焊接、取放和自动导引运输车(AGV) 所需的亚毫米级精度。整合式驱动器和马达安装感测器的扭矩向量控制技术可最大限度地减少停机时间。中国、日本和韩国针对智慧工厂的区域性奖励正在加速升级计划,而北美工厂也将类似的架构纳入其回流计画。能够提供驱动器、控制器和分析软体捆绑销售的供应商正在获得更高的利润率。

原物料价格波动对製造业经济带来压力。

铜绕组占电机材料成本的四分之一之多,因此,伦敦金属交易所铜价在2024年之前18%的波动幅度给原始设备製造商(OEM)的季度利润率带来了压力。由于中国出口政策的不确定性,钕镝永磁体的价格也大幅上涨。製造商们采取了替代策略,包括优化槽填充、采用铝製转子笼和高铁氧体磁铁材料。大型製造商则透过签订多年期供应合约和建立自身的磁体回收计画来规避风险。

细分市场分析

由于其结构稳固且初始成本低,预计即使到2025年,感应电动机仍将维持69.12%的AC马达马达市场份额。然而,随着永久磁铁磁通密度的提高和控制设备的下降,同步马达的替代需求预计将以5.53%的复合年增长率成长。因此,同步马达型AC马达马达的市场规模预计将比现有感应电动机的替代需求成长更快。

高效率对于高能耗工厂来说极具吸引力,而内建的位置回馈功能则有助于机器人和输送机的定位控制。原始设备製造商(OEM)正在将同步马达与磁场定向驱动装置捆绑销售,以简化试运行。虽然单相感应马达在住宅空调仍然占据主导地位,但多相同步马达正在汽车喷漆车间和SMT生产线上逐步普及。预计未来十年,这两种技术在交流马达市场份额上的差距将逐渐缩小。

预计到2025年,低压(低于1千伏特)马达将占通用製造业和暖通空调(HVAC)领域总收入的60.88%。然而,由于风力发电厂和海水淡化厂对兆瓦级辅助设备的需求,高压(高于11千伏特)马达将呈现最高的复合年增长率(CAGR),达到5.14%。因此,高压交流电机市场规模预计将以高于中压马达市场的速度成长。

为了应对高压下的局部放电,原始设备製造商 (OEM) 正在将紧凑型定子槽设计为标准;环氧树脂云母绝缘系统则可延长马达在潮湿的海上机舱环境中的使用寿命。电网规范的实施也推动了具有卓越功率因数性能的同步马达的应用。巴西和越南的工程总承包商 (EPC) 越来越多地采用高压电机,以最大限度地减少长距离电缆传输过程中的电流和电缆损耗,从而扩大了此类交流电机的市场份额。

区域分析

到2025年,亚太地区将占全球收入的44.10%。在中国,高科技製造业的復苏推动了精密马达的进口;而印度可再生能源的普及应用则带动了风能和太阳能等大型设施对驱动装置的需求。越南和泰国等东南亚国家正逐步实现伺服生产线的在地化,从而缩短进口前置作业时间。在韩国和日本,政府对高效率马达成本高达20%的补贴正在加速升级改造。

南美洲是成长最快的地区,预计到2031年年均复合成长率将达到4.02%。在巴西,国家开发银行的资金正用于工业现代化,带动了石化产业丛集对IE3+马达的订单成长。阿根廷的RenovAr竞标系统刺激了风电场投资,并提振了对500kW以上同步马达的需求。汇率波动正在缩小资本投资窗口,但墨西哥和巴西设有组装厂的原始设备製造商(OEM)正在对冲外汇风险并锁定大额订单。

北美和欧洲仍然是以替换为主导的市场。美国《CHIPS法案》和《IRA法案》下的回流生产激励措施鼓励新建工厂,这些工厂需要中型伺服阵列。加拿大偏远地区的矿场偏好坚固耐用、高功率、配备防冰轴承的马达。欧盟生态设计指令正在推动现有工厂升级至IE4标准。斯堪地那维亚国家正在为区域供热泵制定IE5标准,而德国汽车产业则越来越多地整合智慧马达和驱动组件,同时保持较高的价格。在这两个地区,平均售价的上涨抵消了销售成长放缓的影响,稳定了老牌交流马达的市占率。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 强制性能效法规(IE3/IE4)

- 工业自动化和机器人技术的快速普及

- 扩大可再生能源资产(风能、太阳能)

- 商业地产中暖通空调/冷冻设备的扩建

- 轴向磁通AC马达在电动车领域的兴起

- 人工智慧驱动的预测性维护生态系统

- 市场限制

- 铜和稀土元素价格波动

- 高效率马达的初始成本高

- 电力电子(IGBT)供应链中的瓶颈

- 遵守废旧产品回收及收集义务

- 产业生态系分析

- 监管现状和标准

- 技术展望(边缘运算和人工智慧分析)

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依马达类型

- AC马达

- 单相

- 多相

- 同步AC马达

- 直流励磁转子

- 永久磁铁

- 滞后现象

- 磁阻

- AC马达

- 按电压等级

- 低电压(1千伏特或以下)

- 中压(1-11kV)

- 高压(超过11千伏特)

- 按额定输出

- 小于1千瓦

- 1~100kW

- 100~500 kW

- 超过500千瓦

- 按效率等级

- IE1(标准)

- IE2(高效率)

- IE3(高级版)

- IE4(超级高级版)

- IE5(超高级版)

- 按最终用户行业划分

- 石油和天然气

- 化学品/石油化工

- 发电

- 用水和污水

- 金属和采矿

- 食品/饮料

- 个人作品

- 其他终端用户产业

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 供应商排名分析

- 公司简介

- ABB Ltd.

- Siemens AG

- WEG Equipamentos Eletricos SA

- Nidec Corporation

- Johnson Electric Holdings Limited

- Yaskawa Electric Corporation

- Regal Rexnord Corporation

- Rockwell Automation, Inc.

- Franklin Electric Co., Inc.

- Bosch Rexroth AG

- Kirloskar Electric Company Ltd.

- SEVA-tec GmbH

- Toshiba Corporation

- Mitsubishi Electric Corporation

- TECO Electric & Machinery Co., Ltd.

- Leroy-Somer Holding(Nidec)

- ATB Austria Antriebstechnik AG

- Getriebebau NORD GmbH & Co. KG

- Oriental Motor Co., Ltd.

- Brook Crompton UK Ltd.

第七章 市场机会与未来展望

The alternating current motor market size in 2026 is estimated at USD 18.89 billion, growing from 2025 value of USD 18.29 billion with 2031 projections showing USD 22.24 billion, growing at 3.32% CAGR over 2026-2031.

This growth trajectory is shaped less by green-field capacity additions and more by efficiency-driven replacement cycles mandated by IE3 and IE4 regulations. Premium-efficiency design adoption is expanding across discrete manufacturing, renewable-energy, and HVAC segments, while automation programs in Asia and reshoring efforts in North America sustain baseline demand. Vendor strategies revolve around vertical integration in copper winding, electrical steel, and power electronics to buffer raw-material volatility and semiconductor shortages. Mature end-user sectors such as oil and gas continue to anchor revenues, yet faster growth is migrating toward water treatment, data centers, and wind-turbine auxiliaries, where lifetime energy savings justify premium pricing.

Global Alternating Current (AC) Motor Market Trends and Insights

Mandatory Energy-Efficiency Regulations Drive Premium Motor Adoption

IE3 has become the global compliance floor, and IE4 adoption is accelerating across Europe and the United States, effectively eliminating low-efficiency legacy models from procurement lists. Manufacturers are therefore retooling plants with automated lamination stamping and precision magnet-assembly lines to meet stricter loss limits. The shift burdens smaller regional firms that lack capital for new tooling, consolidating share with global incumbents. Procurement teams now evaluate motors on full-load efficiency at 75% and 50% duty points, which strengthens the value proposition of synchronous permanent-magnet designs. End-users capturing utility rebates for premium motors shorten payback periods to under two years, further reinforcing the regulatory push.

Industrial Automation Accelerates Mid-Range Motor Demand

Automotive, electronics, and logistics facilities are scaling collaborative robot fleets that rely on precision-controlled 1-100 kW motors. Servo-grade synchronous machines equipped with encoders deliver the sub-millimeter accuracy required in robotic welding, pick-and-place, and automated guided vehicles. Integrated drives and on-motor sensors enable torque-vector control, minimizing downtime. Regional incentives for smart factories in China, Japan, and Korea are pulling forward upgrade projects, while North American plants adopt similar architectures under reshoring schemes. Suppliers able to bundle drives, controllers, and analytics software capture premium margins.

Raw-Material Price Volatility Pressures Manufacturing Economics

Copper winding accounts for up to one-quarter of motor material cost, so London Metal Exchange price swings of 18% in 2024 drove quarterly margin compression among OEMs. Permanent-magnet grades of neodymium and dysprosium likewise spiked amid Chinese export policy uncertainty. Manufacturers adopted substitution tactics such as optimized slot fills, aluminum rotor cages, and ferrite-rich magnet compositions. Larger players hedge with multiyear supply contracts and proprietary magnet recycling programs.

Other drivers and restraints analyzed in the detailed report include:

- Renewable-Energy Infrastructure Expands High-Power Motor Applications

- Commercial HVAC Modernization

- Premium Motor Cost Barriers in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Induction motors retained 69.12% share of the alternating current motor market in 2025 due to their rugged construction and low initial cost. Yet synchronous alternatives are projected at a 5.53% CAGR as permanent-magnet flux densities climb and controller prices fall. The alternating current motor market size for synchronous variants is therefore set to outpace replacements in the installed induction base.

Their premium efficiency appeals to energy-intensive plants, while built-in position feedback supports robotics and conveyor indexing. OEMs bundle synchronous machines with field-oriented drives that simplify commissioning. Although single-phase induction units remain dominant in residential air conditioners, multi-phase synchronous motors now permeate automotive paint shops and SMT lines. The alternating current motor market share gap between the two technologies is expected to narrow over the decade.

Low-voltage (<1 kV) machines delivered 60.88% revenue in 2025 across general manufacturing and HVAC. High-voltage (>11 kV) models, however, show the strongest 5.14% CAGR as wind farms and desalination plants demand multi-megawatt auxiliaries. The alternating current motor market size in high-voltage will therefore rise faster than the mid-voltage segment.

OEMs standardize compact stator slot designs to manage partial-discharge at high voltages, while epoxy-mica insulation systems extend lifetimes in damp offshore nacelles. Grid-code compliance further drives synchronous options with leading power-factor capability. EPC contractors in Brazil and Vietnam increasingly specify high-voltage motors to minimize current and cable losses across long cable runs, enlarging the alternating current motor market share for this class.

The Alternating Current (AC) Motor Market Report is Segmented by Motor Type (Induction AC Motors, and Synchronous AC Motors), Voltage Class (Low, Medium, and High Voltage), Power Rating (less Than 1 KW, 1-100 KW, 100-500 KW, and More), Efficiency Class (IE1-IE5), End-User Industry (Oil and Gas, Chemicals, Power Generation, Water Treatment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 44.10% of global revenue in 2025. China's high-tech manufacturing rebound spurred precision-motor imports, whereas India's renewable-energy rollout necessitated utility-scale drives for wind and solar assets. Southeast Asian countries such as Vietnam and Thailand are now localizing servo production lines, shrinking import lead times. Government subsidies covering up to 20% of premium-efficiency motor cost accelerate replacements in Korea and Japan.

South America is the fastest-growing region at 4.02% CAGR through 2031. Brazil channels National Development Bank funding toward industrial modernization, lifting orders for IE3-plus motors in petrochemical clusters. Argentina's RenovAr auctions foster wind-farm investment, triggering demand for >500 kW synchronous units. Currency volatility narrows capex windows, but OEMs with Mexican or Brazilian assembly plants hedge exchange-rate risks and secure volume contracts.

North America and Europe remain replacement-driven markets. U.S. reshoring incentives under the CHIPS and IRA acts stimulate greenfield factories requiring mid-range servo arrays. Canada's remote mining operations favor rugged high-power motors with ice-rated bearings. Europe's Ecodesign mandates drive IE4 upgrades across legacy plants. Scandinavian countries specify IE5 for district-heating pumps, while Germany's automotive sector integrates smart-motor plus drive packages, sustaining premium price points. Both regions compensate for slower unit growth with higher average selling prices, stabilizing alternating current motor market share among established brands.

- ABB Ltd.

- Siemens AG

- WEG Equipamentos Eletricos S.A.

- Nidec Corporation

- Johnson Electric Holdings Limited

- Yaskawa Electric Corporation

- Regal Rexnord Corporation

- Rockwell Automation, Inc.

- Franklin Electric Co., Inc.

- Bosch Rexroth AG

- Kirloskar Electric Company Ltd.

- SEVA-tec GmbH

- Toshiba Corporation

- Mitsubishi Electric Corporation

- TECO Electric & Machinery Co., Ltd.

- Leroy-Somer Holding (Nidec)

- ATB Austria Antriebstechnik AG

- Getriebebau NORD GmbH & Co. KG

- Oriental Motor Co., Ltd.

- Brook Crompton UK Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory energy-efficiency regulations (IE3/IE4)

- 4.2.2 Rapid industrial automation and robotics uptake

- 4.2.3 Expansion of renewable-energy assets (wind, solar)

- 4.2.4 HVAC/R build-out in commercial real estate

- 4.2.5 Rise of axial-flux PM AC motors in e-mobility

- 4.2.6 AI-enabled predictive-maintenance ecosystems

- 4.3 Market Restraints

- 4.3.1 Volatile copper and rare-earth metal prices

- 4.3.2 High upfront cost of premium-efficiency motors

- 4.3.3 Power-electronics (IGBT) supply-chain bottlenecks

- 4.3.4 End-of-life recycling and take-back compliance

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape and Standards

- 4.6 Technological Outlook (Edge and AI analytics)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Induction AC Motors

- 5.1.1.1 Single-phase

- 5.1.1.2 Poly-phase

- 5.1.2 Synchronous AC Motors

- 5.1.2.1 DC-excited Rotor

- 5.1.2.2 Permanent-Magnet

- 5.1.2.3 Hysteresis

- 5.1.2.4 Reluctance

- 5.1.1 Induction AC Motors

- 5.2 By Voltage Class

- 5.2.1 Low Voltage (<=1 kV)

- 5.2.2 Medium Voltage (>1-11 kV)

- 5.2.3 High Voltage (>11 kV)

- 5.3 By Power Rating

- 5.3.1 Less than 1 kW

- 5.3.2 1-100 kW

- 5.3.3 100-500 kW

- 5.3.4 Greater than 500 kW

- 5.4 By Efficiency Class

- 5.4.1 IE1 (Standard)

- 5.4.2 IE2 (High)

- 5.4.3 IE3 (Premium)

- 5.4.4 IE4 (Super-Premium)

- 5.4.5 IE5 (Ultra-Premium)

- 5.5 By End-user Industry

- 5.5.1 Oil and Gas

- 5.5.2 Chemicals and Petrochemicals

- 5.5.3 Power Generation

- 5.5.4 Water and Wastewater

- 5.5.5 Metals and Mining

- 5.5.6 Food and Beverage

- 5.5.7 Discrete Manufacturing

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Ranking Analysis

- 6.5 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.5.1 ABB Ltd.

- 6.5.2 Siemens AG

- 6.5.3 WEG Equipamentos Eletricos S.A.

- 6.5.4 Nidec Corporation

- 6.5.5 Johnson Electric Holdings Limited

- 6.5.6 Yaskawa Electric Corporation

- 6.5.7 Regal Rexnord Corporation

- 6.5.8 Rockwell Automation, Inc.

- 6.5.9 Franklin Electric Co., Inc.

- 6.5.10 Bosch Rexroth AG

- 6.5.11 Kirloskar Electric Company Ltd.

- 6.5.12 SEVA-tec GmbH

- 6.5.13 Toshiba Corporation

- 6.5.14 Mitsubishi Electric Corporation

- 6.5.15 TECO Electric & Machinery Co., Ltd.

- 6.5.16 Leroy-Somer Holding (Nidec)

- 6.5.17 ATB Austria Antriebstechnik AG

- 6.5.18 Getriebebau NORD GmbH & Co. KG

- 6.5.19 Oriental Motor Co., Ltd.

- 6.5.20 Brook Crompton UK Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

马达保护装置市场:依产品类型、保护机制、电压等级、应用、最终用户产业划分,全球预测(2026-2032年)石油燃烧器马达市场:依马达类型、额定功率、转速、绝缘等级、最终用户、应用领域划分,全球预测(2026-2032年)开关磁阻马达调速系统市场:按应用、驱动类型、控制技术和速度范围划分,全球预测(2026-2032年)防爆电机市场按推进类型、车辆类型、价格范围、最终用户和销售管道,全球预测(2026-2032年)

马达保护装置市场:依产品类型、保护机制、电压等级、应用、最终用户产业划分,全球预测(2026-2032年)石油燃烧器马达市场:依马达类型、额定功率、转速、绝缘等级、最终用户、应用领域划分,全球预测(2026-2032年)开关磁阻马达调速系统市场:按应用、驱动类型、控制技术和速度范围划分,全球预测(2026-2032年)防爆电机市场按推进类型、车辆类型、价格范围、最终用户和销售管道,全球预测(2026-2032年) 能源与电能品质计量市场分析及至2035年预测:类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型、解决方案

能源与电能品质计量市场分析及至2035年预测:类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型、解决方案 全球开关式磁阻电动机市场规模、份额、趋势及成长分析报告(2026-2034)全球轧延电机市场规模、份额、趋势和成长分析报告(2026-2034年)

全球开关式磁阻电动机市场规模、份额、趋势及成长分析报告(2026-2034)全球轧延电机市场规模、份额、趋势和成长分析报告(2026-2034年) 同步磁阻马达(SynRM)-全球市场份额和排名、总收入和需求预测(2026-2032)

同步磁阻马达(SynRM)-全球市场份额和排名、总收入和需求预测(2026-2032) 2026年全球中高功率马达市场报告2026年全球交流电机市场报告

2026年全球中高功率马达市场报告2026年全球交流电机市场报告