|

市场调查报告书

商品编码

1940793

钢丝轮胎帘布:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Steel Tire Cord - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

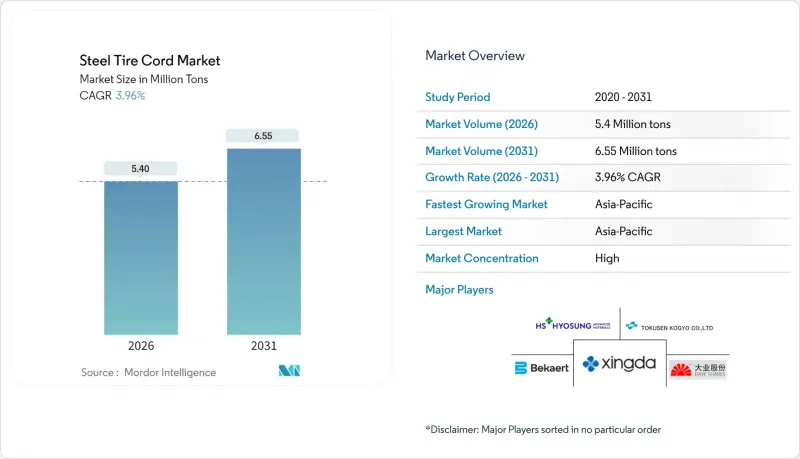

预计钢丝轮胎帘布市场将从 2025 年的 519 万吨增长到 2026 年的 540 万吨,到 2031 年将达到 655 万吨,2026 年至 2031 年的复合年增长率为 3.96%。

推动这一扩张的因素包括强劲的替换需求、新兴市场稳健的汽车生产以及商用轮胎向子午线轮胎的转变。儘管利润率面临压力,但中国2025年上半年的汽车产量达到1,562万辆,凸显了亚洲汽车生产的强劲动能。汽车製造商专注于低滚动阻力设计,并力争2030年达到40%的再生材料含量,迫使帘线供应商改进涂层化学製程并整合再生钢材。子午线结构增加了每条轮胎的钢材用量,从而推高了单位轮胎钢材的需求;而电动车的扭矩特性则推动了对超高模量、抗疲劳帘线的需求。

全球钢丝轮胎轮胎帘布市场趋势与洞察

加速新兴经济体的汽车生产

随着低成本地区汽车产能的扩张,製造业的持续投资支撑了钢丝轮胎帘布市场。中国在2025年上半年的产量激增反映了财政奖励策略的有效性,这些措施保护了整车厂组装免受宏观经济逆风的影响。预计东协地区将在2023年吸引2,300亿美元的外国直接投资(FDI),其中大部分将用于零件供应链,从而巩固泰国、越南和印尼等国对钢丝帘线的新需求。光是在泰国,大陆集团计画投资3.15亿美元进行扩建,每年将新增300万条轮胎的产量,进一步巩固在地采购的钢丝帘线需求。地域多元化降低了对成熟市场的过度依赖,并使供应商能够对冲产能风险。政府为促进电动车组装提供的激励措施,随着电池重量的增加,每条轮胎所需的钢丝帘线数量也随之增加,这将进一步扩大可用产能。

商用车辆加速采用子午线轮胎

美国中型卡车子午线轮胎的出货量预计在2024年成长5.9%,达到2,200万条,扭转先前的下滑趋势。子午线轮胎比斜交轮胎使用更多的高抗拉强度钢丝,因此每条轮胎的帘线数量更多。为了节省8-10%的燃油,车队营运商正在采用子午线轮胎来降低营运成本。日益严格的温室气体排放法规正在收紧总拥有成本(TCO)的计算,使得子午线轮胎的应用至关重要。随着商业货运和建设活动的復苏,帘线供应商将受益于来自原始设备製造商(OEM)和替换需求的成长。北美和欧洲的早期应用已树立了技术标桿,拉丁美洲和东南亚地区也将紧随其后。

高碳钢和黄铜价格波动

预计Becat 2024年的销售额将下降8.6%至40亿欧元,但稳定的利润率证实了有效的避险和成本转嫁机制。世界银行金属指数在2024年4月上涨了9%,预计在2025年之前保持高位,这将对非一体化铜缆厂的盈利构成压力。铜价已上涨至每吨1万美元,推高了包覆层成本,迫使供应商进行合金化或透过生态信用额度进行成本抵销。缺乏避险工具的小规模区域性企业难以获得融资,这为产业整合和策略性退出铺平了道路。

细分市场分析

预计到2025年,黄铜涂层钢丝将维持48.25%的钢丝轮胎帘布市场份额,年复合成长率达4.74%,并在2031年之前巩固其市场主导地位。此涂层中的铜锌相在硫化过程中形成牢固的Cu₂S界面层,从而最大限度地提高橡胶在循环负荷下的黏合力。锌涂层帘线具有优异的耐腐蚀性,但环保法规正在推动锌钴或锌锰混合材料的实验室规模测试。铜涂层钢丝用于需要高导热性的特定应用领域,例如飞机轮胎;而奈米合金镀层则用于电动车原型设计,以在保持相当黏合力的同时减少钢丝直径。加州日益严格的锌径流法规正在推动黄铜配方的最佳化,以在不牺牲性能的前提下减少残留锌,从而促进梯度层涂层技术的研究和开发。

电镀槽控制技术的进步降低了氢脆风险,延长了电动皮卡车严苛使用条件下电线的使用寿命。供应商正在投资建造封闭回路型废水处理系统,以符合欧盟REACH指令,并使生产流程与客户的永续发展标准保持一致。

钢丝轮胎帘布报告按类型(黄铜涂层、锌涂层、铜涂层及其他)、应用(乘用车轮胎、商用车轮胎、两轮车轮胎、飞机轮胎、工业轮胎)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行细分。市场预测以吨为单位。

区域分析

预计到2025年,亚太地区将占全球钢丝轮胎帘布市场的49.12%,并在2031年之前以5.08%的复合年增长率成长。中国2025年上半年汽车产量预计达1,562万辆,加上政府的电动车补贴政策,将确保钢丝帘线的基本负载需求。预计2023年东协地区将吸引2,300亿美元的外国直接投资,为产能扩张奠定基础,例如大陆集团位于泰国的工厂,其目标是每年新增300万条轮胎的产能。

北美正在将轮胎产能迁回本土,以增强供应链的韧性。耐吉森公司投资13亿美元在美国兴建的工厂计画在2029年实现日产3万条轮胎的目标。预计到2025年,美国轮胎出货量将达到3.404亿条,将使替换需求保持在高位。美国环保署(EPA)的排放法规正在推动对闭合迴路镀锌生产线的投资,这些生产线可以收集锌废水。

在欧洲,高端冬季轮胎和永续性认证的细分市场受到优先考虑。儘管销量下降,但大陆集团预计2024年轮胎销售额将达到146亿美元。欧盟于2023年恢復对中国产轮胎征收反倾销税,此举旨在保护本土生产商,并推动欧洲帘线厂的本地需求成长。米其林提出的40%再生材料含量目标正在加速再生钢丝和环保涂层的采购。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴国家汽车生产加速发展

- 商用车向子午线轮胎的转变正在快速推进。

- 永续性推动低滚动阻力「绿色」轮胎的发展

- 电动车对超柔韧、抗疲劳线的需求

- 监管政策转向低铜锌涂层推动合金创新

- 市场限制

- 高碳钢和黄铜价格波动;

- 聚合物/酰胺纤维的替代威胁

- 无气轮胎(NPT)的出现

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型

- 黄铜涂层

- 镀锌

- 铜涂层

- 其他类型

- 透过使用

- 乘用车轮胎

- 商用车辆轮胎

- 摩托车轮胎

- 飞机轮胎

- 工业轮胎

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、合资、资金筹措)

- 市占率(%)/排名分析

- 公司简介

- Bekaert

- Bridgestone Corporation

- Daye Co., Ltd.

- Henan Hengxing Science & Technology Co., Ltd.

- HS HYOSUNG ADVANCED MATERIALS

- Hubei Fuxing Technology Co., Ltd.

- Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- Junma Group

- Kiswire Ltd.

- Qingdao HL Group Ltd.

- Saarstahl AG

- Shandong Xinhao Tire Materials Co., Ltd.

- Shougang Century Holdings Limited

- Sumitomo Electric Industries, Ltd.

- Tokusen Kogyo Co., Ltd.

第七章 市场机会与未来展望

The Steel Tire Cord market is expected to grow from 5.19 Million tons in 2025 to 5.4 Million tons in 2026 and is forecast to reach 6.55 Million tons by 2031 at 3.96% CAGR over 2026-2031.

Strong replacement demand, resilient vehicle output in emerging hubs, and the radialization shift in commercial tires collectively underpin this expansion. China's 15.62 million-unit vehicle output in the first half of 2025 validated Asia's production momentum despite margin pressure. Automakers' pivot toward low-rolling-resistance designs, combined with 40% renewable-content targets for 2030, forces cord suppliers to refine coating chemistries and integrate recycled steel. Radial construction's higher steel content per tire enlarges volume intensity, while electric-vehicle torque profiles accelerate demand for ultra-flex, fatigue-resistant cords.

Global Steel Tire Cord Market Trends and Insights

Accelerating Automotive Production in Emerging Economies

Continuous manufacturing investments sustain the steel tire cord market as low-cost hubs strengthen vehicle output capacity. China's H1 2025 production surge echoed targeted fiscal stimuli that shielded OEM assembly lines from macro headwinds. ASEAN attracted USD 230 billion in 2023 FDI, much of it in component supply chains, anchoring new cord demand in Thailand, Vietnam, and Indonesia. Continental's USD 315 million expansion in Thailand alone adds 3 million tires annually, locking in localized cord call-offs. The geographic diversification reduces over-reliance on mature markets and offers suppliers volume hedging. Government incentives that promote EV assembly further magnify the addressable tonnage because battery weight lifts cord intensity per tire.

Rapid Radialization of Commercial Vehicle Tires

Medium-truck radial shipments in the United States are projected to climb 5.9% to 22 million units in 2024, reversing the prior dip. Radial designs embed more high-tensile steel than bias constructions, raising tonnage per unit. Fleet operators seeking 8-10% fuel savings adopt radials to cut operating costs. Regulatory pressure on greenhouse-gas emissions tightens total-cost-of-ownership calculus, making radialization pivotal. As commercial freight rebounds alongside construction activity, cord suppliers gain both OEM and replacement pull-through. Early adoption in North America and Europe sets technical benchmarks later mirrored in Latin America and Southeast Asia.

Volatile High-Carbon Steel and Brass Prices

Bekaert's 2024 sales slipped 8.6% to EUR 4.0 billion yet margin stability revealed effective hedging and cost pass-through mechanisms. The World Bank metals index rose 9% in April 2024 and is forecast to remain elevated through 2025, compressing profitability for non-integrated cord mills. Copper's rally to USD 10,000 per ton adds coating-layer inflation, forcing suppliers to rethink alloying or present eco-credit offsets. Small regional players lacking hedging tools face cash-flow strain, paving the way for consolidation or strategic exits.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Push for Low-Rolling-Resistance "Green" Tires

- Regulatory Shift to Low-Copper/Zinc Coatings Boosts Alloy Innovation

- Polymer/Aramid Fiber Substitution Threat

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brass-coated wire retained 48.25% steel tire cord market share in 2025 and should climb at a 4.74% CAGR, cementing its dominance through 2031. The coating's Cu-Zn phase enables robust Cu2S interfacial layers during vulcanization, maximizing rubber adhesion under cyclic loading. Zinc-coated cords provide higher corrosion resistance but face environmental scrutiny, driving lab-scale trials of zinc-cobalt or zinc-manganese hybrids. Copper-coated wire occupies niche high-thermal-conductivity applications such as aircraft tires, while nano-alloy platings appear in prototype EV designs seeking thinner gauge with equal adhesion. California's impending zinc runoff limits encourage brass formulation optimization to lower residual zinc without eroding performance, nudging research and development toward gradient-layer coatings.

Technological advances in plating-bath control reduce hydrogen embrittlement risk, extending wire service life even in the harsher duty cycles of electric pickups. Suppliers invest in closed-loop effluent treatment to comply with Europe's REACH directives, aligning production with customer sustainability scorecards.

The Steel Tire Cord Report is Segmented by Type (Brass Coated, Zinc Coated, Copper Coated, and Other Types), Application (Passenger Vehicle Tires, Commercial Vehicle Tires, Two-Wheeler Tires, Aircraft Tires, and Industrial Tire), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific held 49.12% steel tire cord market share in 2025 and is projected to grow at 5.08% CAGR through 2031. China's H1 2025 vehicle output of 15.62 million units, coupled with government EV subsidies, guarantees base-load cord demand. ASEAN's USD 230 billion inbound FDI in 2023 underpins capacity expansions, such as Continental's Thailand plant aimed at 3 million additional tires annually.

North America is reshoring tire capacity to fortify supply resilience, with Nexen's USD 1.3 billion U.S. facility targeting 30,000 units daily by 2029. U.S. tire shipments are forecast to hit 340.4 million units in 2025, sustaining high replacement pull-through. EPA emission rules propel investment in closed-loop galvanizing lines that capture zinc run-off.

Europe prioritizes premium winter and sustainability-certified segments, with Continental reporting USD 14.6 billion tire sales in 2024 despite volume softness. EU anti-dumping duties on Chinese tires, re-imposed in 2023, protect regional producers and channel more local demand to European cord mills. Michelin's 40% renewable-content ambition intensifies the sourcing of recycled wire and eco-coatings.

- Bekaert

- Bridgestone Corporation

- Daye Co., Ltd.

- Henan Hengxing Science & Technology Co., Ltd.

- HS HYOSUNG ADVANCED MATERIALS

- Hubei Fuxing Technology Co., Ltd.

- Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- Junma Group

- Kiswire Ltd.

- Qingdao HL Group Ltd.

- Saarstahl AG

- Shandong Xinhao Tire Materials Co., Ltd.

- Shougang Century Holdings Limited

- Sumitomo Electric Industries, Ltd.

- Tokusen Kogyo Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating automotive production in emerging economies

- 4.2.2 Rapid radialization of commercial vehicle tires

- 4.2.3 Sustainability push for low-rolling-resistance "green" tires

- 4.2.4 EV-specific ultra-flex fatigue-resistant cord demand

- 4.2.5 Regulatory shift to low-copper/zinc coatings boosts alloy innovation

- 4.3 Market Restraints

- 4.3.1 Volatile high-carbon steel and brass prices

- 4.3.2 Polymer/aramid fiber substitution threat

- 4.3.3 Emergence of air-less NPTs (non-pneumatic tires)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Brass Coated

- 5.1.2 Zinc Coated

- 5.1.3 Copper Coated

- 5.1.4 Other types

- 5.2 By Application

- 5.2.1 Passenger Vehicle Tires

- 5.2.2 Commercial Vehicle Tires

- 5.2.3 Two-Wheeler Tires

- 5.2.4 Aircraft Tires

- 5.2.5 Industrial Tire

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, JVs, Funding)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bekaert

- 6.4.2 Bridgestone Corporation

- 6.4.3 Daye Co., Ltd.

- 6.4.4 Henan Hengxing Science & Technology Co., Ltd.

- 6.4.5 HS HYOSUNG ADVANCED MATERIALS

- 6.4.6 Hubei Fuxing Technology Co., Ltd.

- 6.4.7 Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- 6.4.8 Junma Group

- 6.4.9 Kiswire Ltd.

- 6.4.10 Qingdao HL Group Ltd.

- 6.4.11 Saarstahl AG

- 6.4.12 Shandong Xinhao Tire Materials Co., Ltd.

- 6.4.13 Shougang Century Holdings Limited

- 6.4.14 Sumitomo Electric Industries, Ltd.

- 6.4.15 Tokusen Kogyo Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 Whitespace and unmet-need assessment

轮胎帘布帘子布-2026-2032年全球市占率及排名、总收入及需求预测

轮胎帘布帘子布-2026-2032年全球市占率及排名、总收入及需求预测 全球轮胎帘布和轮胎织物市场规模、份额、趋势和成长分析报告(2026-2034年)

全球轮胎帘布和轮胎织物市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球轮胎帘布纤维市场报告

2026年全球轮胎帘布纤维市场报告 增强型绿色轮胎帘布市场-全球产业规模、份额、趋势、机会及预测(依材料类型、应用、通路、地区及竞争格局划分,2021-2031年)

增强型绿色轮胎帘布市场-全球产业规模、份额、趋势、机会及预测(依材料类型、应用、通路、地区及竞争格局划分,2021-2031年) 全球帘线轮胎市场报告、绩效及预测(2020-2031年)

全球帘线轮胎市场报告、绩效及预测(2020-2031年) 轮胎帘布和轮胎织物市场规模、份额和成长分析(按材料、类型、车辆类型、应用和地区划分)-2026-2033年产业预测

轮胎帘布和轮胎织物市场规模、份额和成长分析(按材料、类型、车辆类型、应用和地区划分)-2026-2033年产业预测 全球钢製轮胎帘子线市场:产业分析、规模、份额、成长、趋势与预测(2025-2032)轮胎帘子布市场-全球产业规模、份额、趋势、机会及预测,依材料、轮胎类型、车辆类型、应用、地区及竞争细分,2020-2030 年预测

全球钢製轮胎帘子线市场:产业分析、规模、份额、成长、趋势与预测(2025-2032)轮胎帘子布市场-全球产业规模、份额、趋势、机会及预测,依材料、轮胎类型、车辆类型、应用、地区及竞争细分,2020-2030 年预测 轮胎帘布帘子布市场规模、份额、成长分析(按材料、轮胎类型、应用、车辆类型、地区)-2025-2032 年产业预测

轮胎帘布帘子布市场规模、份额、成长分析(按材料、轮胎类型、应用、车辆类型、地区)-2025-2032 年产业预测 轮胎帘布帘子布市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

轮胎帘布帘子布市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)