|

市场调查报告书

商品编码

1940794

水泥:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

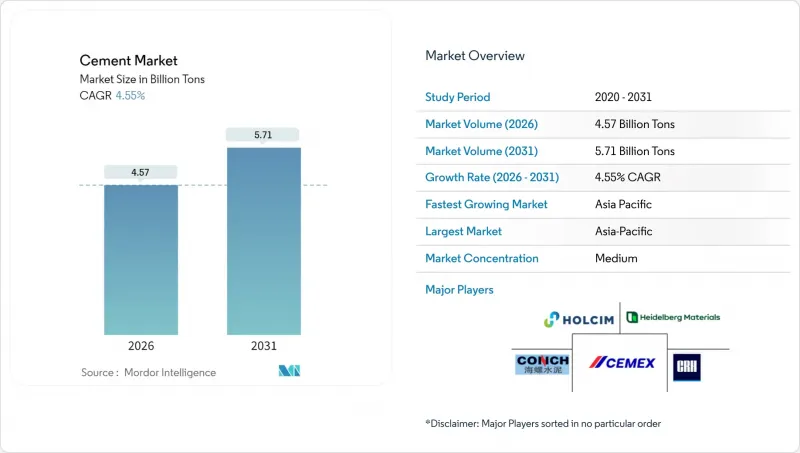

预计到 2026 年,水泥市场规模将达到 45.7 亿吨,高于 2025 年的 43.7 亿吨。

预计到 2031 年产量将达到 57.1 亿吨,2026 年至 2031 年的复合年增长率为 4.55%。

建设业的復苏、基础设施建设的推进以及向低碳接合材料的加速转型构成了需求的核心。随着采购部门将环境、社会和管治)要求纳入考量,混合料正逐渐被接受,而资料中心和物流设施的建置也将推动需求的成长。生产商正透过窑炉数位化和燃料转换来应对能源价格波动,从而稳定成本。日益严格的二氧化碳排放法规正在加速水泥熟料替代,而辅助胶凝材料在主要水泥市场中被视为策略性投入品。

全球水泥市场趋势与洞察

亚洲和非洲新兴地区与都市化相关的基础建设热潮

特大城市计画、区域铁路走廊和大型住宅建设计画将持续推动亚太地区所有主要水泥市场的需求。中国的「一带一路」倡议正在扩大对伙伴国家的需求,而印度每年的基础设施支出接近GDP的5%,支撑着国内消费。住宅短缺(例如,预计到2028年,菲律宾的住房供不应求将达到1,000万套)将进一步刺激住宅需求。非洲的城市化与亚洲领先的周期类似,加纳的价格法规结构正在平衡住房的可负担性和供应量。每位农村人口涌入都市区,都会使交通、住宅、公共产业和商业设施等水泥密集型资产增加三到四倍。

政府对低碳公共基础设施的奖励策略(新冠疫情后)

疫情后的经济復苏计画将把排放上限纳入计划规范,并在先进水泥市场优先发展低碳替代方案。美国两党共同提出的基础设施法案拨款5,500亿美元用于新业务,波特兰水泥协会预计这些项目将在五年内增产4,600万吨。联邦政府的支持也延伸至製程创新,能源部资助了CEMEX公司位于诺克斯维尔工厂的碳捕获试点计画。每投资1美元,将产生超过3.5美元的乘数效应,从而建立可持续的合约管道,并确保对混合水泥和替代燃料产品的稳定需求。

严格的二氧化碳排放上限和水泥熟料与水泥比例

欧盟排放交易体系和加州净零排放指令等合规计画需要对窑炉进行高成本的维修。燃煤发电厂的退役导致飞灰短缺日益严重,迫使生产商寻找替代补充资料。美国国家水泥公司与Carbon TerraVolt公司合作建造加州首个净零排放工厂,凸显了合规监管带来的巨大资金负担。 ISO 14001等认证标准逐渐演变为进入要求,提高了资金匮乏企业的进入门槛。

细分市场分析

到2025年,混合水泥将占水泥出货量的68.45%,成为该细分市场中水泥市场规模最大的组成部分。石灰石基混合水泥将推动需求成长,因为它兼具商业性性能和低碳排放。普通硅酸盐水泥是道路和预铸面板的重要材料,这些材料需要较高的早期强度,但由于法规限制水泥熟料含量,其市场份额正在下降。白水泥已在装饰应用领域开闢了一个利基市场,尤其是建筑幕墙墙板方面,土耳其是北美的主要出口国。纤维水泥板因其耐用性和防火性能,已成功打入住宅墙板市场。

投资趋势也印证了这个转变。豪瑞集团(Holcim)在瑞士工厂投资2.78亿美元,旨在将替代燃料的使用率从57%提高到85%以上,这表明提升环境绩效需要巨额投资。海德堡材料公司(Heidelberg Materials)正在加纳扩建全球最大的煅烧黏土生产线之一,因此能够向该地区供应低碳接合材料。这些倡议强化了支撑混合水泥产业4.88%复合年增长率预测的结构调整,巩固了主导地位。

此水泥报告按产品类型(混合水泥、纤维水泥、普通硅酸盐水泥、白水泥及其他)、最终用途领域(住宅、商业、基础设施、工业及公共)和地区(亚太、北美、欧洲、南美、中东和非洲)进行细分。市场预测以吨为单位。

区域分析

亚太地区预计到2025年将占全球水泥产量的74.60%,巩固其作为水泥市场核心的地位。受房地产市场调整的影响,中国2024年的水泥产量下降了10%,但大型国有企业透过将剩余产能出口到东南亚和非洲,抵消了国内市场的疲软。印度继续保持成长势头,这得益于有利的人口结构和联邦政府资本支出计划带来的订单增长。越南、印尼和泰国也实现了两位数的工厂使用率,主要得益于电子製造业和城市交通计划的涌入。

预计到2031年,中东和非洲地区的复合年增长率将达到4.92%,成为全球水泥市场成长最快的区域。海湾地区的经济多元化计划,例如沙乌地阿拉伯的“2030愿景”,催生了大规模基础设施建设联盟,但出口配额的周期性收紧也导致了当地供应受限。非洲各市场的扩张情况不尽相同。加纳实施了价格上限以保护消费者权益,而肯亚则经历了与公共工程资金流动相关的周期性波动。海德堡材料公司正利用其一体化网路克服物流挑战,并挖掘尚未充分满足的需求。北美和欧洲的水泥消费正趋于成熟,但由于资产维修计画的推进,市场趋于稳定。碳定价和窑炉电气化计划正在主导欧洲的资本投资,而跨国公司则将研发重点放在製程优化上。 Holcim 计划于 2025 年分拆 Amrise,估值超过 300 亿美元,这标誌着该公司更加重视在北美实现盈利和高效的资本配置。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚洲和非洲新兴地区都市化带来的基础建设热潮

- 政府对低碳公共基础设施的奖励策略(后疫情时代)

- 为满足企业ESG目标,对混合水泥/环保水泥的需求不断成长

- 在二、三线城市扩大预拌混凝土供应网络

- 3D混凝土列印技术创造了对特殊黏合剂的利基需求。

- 市场限制

- 严格的二氧化碳排放法规和水泥熟料与水泥比例

- 煤炭和石油焦价格的波动正在推高生产成本。

- 由于燃煤发电厂关闭,飞灰供应量减少

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 混合水泥

- 纤维水泥

- 普通硅酸盐水泥

- 白色水泥

- 其他类型

- 按最终用途

- 住宅

- 商业的

- 基础设施

- 按行业/机构

- 按地区

- 亚太地区

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 韩国

- 泰国

- 越南

- 澳洲

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 法国

- 德国

- 义大利

- 俄罗斯

- 西班牙

- 英国

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Adani Group

- Anhui Conch Cement Co., Ltd.

- BBMG Corporation

- Buzzi SpA

- CEMEX SAB de CV

- Cemros

- China National Building Material Group Corporation(CNBM)

- China Resources Building Materials Technology Holdings

- Concreat

- CRH

- Dangote Cement Plc

- Heidelberg Materials

- HOLCIM

- InterCement

- JSW Cement

- OYAK Cement

- SCG

- TCC GROUP HOLDINGS

- UltraTech Cement Ltd

- Vicat

- Votorantim Cimentos

第七章 市场机会与未来展望

Cement market size in 2026 is estimated at 4.57 Billion Tons, growing from 2025 value of 4.37 Billion Tons with 2031 projections showing 5.71 Billion Tons, growing at 4.55% CAGR over 2026-2031.

Construction recovery, infrastructure upgrades, and accelerated shifts toward low-carbon binders form the core demand engine. Blended formulations gain acceptance as procurement teams embed environmental, social, and governance requirements, while data-center and logistics construction spur incremental volumes. Producers respond with kiln digitalization and fuel switching to stabilize costs in a volatile energy landscape. Regulatory tightening on CO2 emissions accelerates clinker substitution, positioning supplementary cementitious materials as strategic inputs across every major cement market.

Global Cement Market Trends and Insights

Urbanization-Linked Infrastructure Boom in Emerging Asia and Africa

Mega-city projects, regional rail corridors, and mass-housing plans push sustained volumes into every major cement market across Asia-Pacific. China's Belt and Road Initiative extends demand into partner nations, while India sustains annual infrastructure spending near 5% of GDP, underpinning domestic consumption. Housing shortfalls, such as the Philippines' projected 10 million-unit backlog by 2028, amplify residential requirements. African urban growth mirrors earlier Asian cycles, with Ghana's price-regulation framework balancing affordability and supply. Each rural-to-urban migrant drives a three-to-four-fold increase in cement-intensive assets spanning transit, housing, utilities, and commercial space.

Government Stimulus for Low-Carbon Public Infrastructure (Post-COVID)

Post-pandemic recovery packages embed emissions ceilings into project specifications, favoring lower-carbon alternatives across developed cement markets. The U.S. Bipartisan Infrastructure Law earmarks USD 550 billion for new works, a program the Portland Cement Association links to a 46 million-ton five-year volume uplift. Federal support extends to process innovation, with the Department of Energy backing carbon-capture pilots at Cemex's Knoxville plant. Multiplier effects above USD 3.5 per dollar invested trigger sustained contractor pipelines, ensuring steady pull-through of blended cement and alternative-fuel output.

Stringent CO2-Emission Caps and Clinker-to-Cement Ratios

Compliance programs such as the EU Emissions Trading System and California's net-zero mandate obligate costly kiln upgrades. Fly-ash scarcity worsens as coal utilities retire, pressing producers to seek alternative supplementary materials. National Cement's partnership with Carbon TerraVault to construct California's first net-zero facility highlights the capital burden attached to regulatory alignment. Certification standards like ISO 14001 evolve into entry requirements, raising barriers for under-capitalized firms.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Blended/Green Cement to Meet Corporate ESG Targets

- Expansion of Ready-Mix Concrete Networks in Tier-2/3 Cities

- Volatile Coal and Pet-Coke Prices Inflating Production Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blended cement captured 68.45% of 2025 shipments, underpinning the largest portion of the cement market size at the segment level. Limestone-based formulations drive the uptick, aligning commercial performance with reduced embodied carbon. Ordinary Portland Cement remains vital for early-strength highways and precast panels, yet its share declines as regulations push for lower clinker content. White cement fills decorative niches, particularly for facade panels, with Turkey acting as the primary exporter into North America. Fiber cement boards penetrate residential siding thanks to their durability and fire resistance benefits.

Investment patterns confirm the pivot. Holcim's USD 278 million package across Swiss plants seeks to boost alternative-fuel usage from 57% to above 85%, illustrating the required spend to fortify environmental credentials. Heidelberg Materials is scaling the world's largest calcined clay line in Ghana, providing a regional supply of low-carbon binder. These moves reinforce a structural realignment that supports the blended segment's 4.88% forecast CAGR and consolidates leadership within the global cement market.

The Cement Report is Segmented by Product Type (Blended Cement, Fiber Cement, Ordinary Portland Cement, White Cement, and Other Types), End-Use Sector (Residential, Commercial, Infrastructural, and Industrial and Institutional), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific accounted for 74.60% of 2025 volume, confirming the region's centrality to the cement market. China's 2024 output fell 10% amid property corrections, yet state-owned majors offset domestic softness by exporting surplus to Southeast Asia and Africa. India remains the growth engine as favorable demographics and federal capital-expenditure commitments strengthen order books. Vietnam, Indonesia, and Thailand also report double-digit factory utilization rates, supported by electronics manufacturing inflows and urban transport projects.

The Middle East and Africa advance at a 4.92% CAGR through 2031, the fastest regional trajectory in the global cement market. Gulf diversification plans, typified by Saudi Arabia's Vision 2030, generate large infrastructure consortia, albeit with periodic export quotas tightening local supply. African expansion varies by market; Ghana adopts price caps to protect consumers, while Kenya experiences cyclical volatility linked to public works funding streams. Heidelberg Materials leverages an integrated network to navigate logistic hurdles and capture underserved demand pockets. North American and European consumption is mature yet steadied by asset-refurbishment agendas. In Europe, carbon pricing and kiln electrification projects dominate capex, with multinationals clustering research and development around process optimization. Holcim's 2025 spin-off of Amrize, valued above USD 30 billion, signals a sharpened focus on North American profitability and efficient capital deployment

- Adani Group

- Anhui Conch Cement Co., Ltd.

- BBMG Corporation

- Buzzi S.p.A.

- CEMEX S.A.B. de C.V.

- Cemros

- China National Building Material Group Corporation (CNBM)

- China Resources Building Materials Technology Holdings

- Concreat

- CRH

- Dangote Cement Plc

- Heidelberg Materials

- HOLCIM

- InterCement

- JSW Cement

- OYAK Cement

- SCG

- TCC GROUP HOLDINGS

- UltraTech Cement Ltd

- Vicat

- Votorantim Cimentos

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanisation-linked infrastructure boom in emerging Asia and Africa

- 4.2.2 Government stimulus for low-carbon public infrastructure (post-COVID)

- 4.2.3 Rising demand for blended/green cement to meet corporate ESG targets

- 4.2.4 Expansion of ready-mix concrete networks in Tier-2/3 cities

- 4.2.5 3-D concrete-printing creating niche demand for specialised binders

- 4.3 Market Restraints

- 4.3.1 Stringent CO2-emission caps and clinker-to-cement ratios

- 4.3.2 Volatile coal and pet-coke prices inflating production costs

- 4.3.3 Shrinking fly-ash supply as coal plants retire

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Blended Cement

- 5.1.2 Fiber Cement

- 5.1.3 Ordinary Portland Cement

- 5.1.4 White Cement

- 5.1.5 Other Types

- 5.2 By End-Use Sector

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Infrastructural

- 5.2.4 Industrial and Institutional

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Indonesia

- 5.3.1.4 Japan

- 5.3.1.5 Malaysia

- 5.3.1.6 South Korea

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Australia

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 France

- 5.3.3.2 Germany

- 5.3.3.3 Italy

- 5.3.3.4 Russia

- 5.3.3.5 Spain

- 5.3.3.6 United Kingdom

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adani Group

- 6.4.2 Anhui Conch Cement Co., Ltd.

- 6.4.3 BBMG Corporation

- 6.4.4 Buzzi S.p.A.

- 6.4.5 CEMEX S.A.B. de C.V.

- 6.4.6 Cemros

- 6.4.7 China National Building Material Group Corporation (CNBM)

- 6.4.8 China Resources Building Materials Technology Holdings

- 6.4.9 Concreat

- 6.4.10 CRH

- 6.4.11 Dangote Cement Plc

- 6.4.12 Heidelberg Materials

- 6.4.13 HOLCIM

- 6.4.14 InterCement

- 6.4.15 JSW Cement

- 6.4.16 OYAK Cement

- 6.4.17 SCG

- 6.4.18 TCC GROUP HOLDINGS

- 6.4.19 UltraTech Cement Ltd

- 6.4.20 Vicat

- 6.4.21 Votorantim Cimentos

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Emerging Sustainable Cement Technologies

- 7.3 Digitalisation and Automation Opportunities

水泥市场:依产品类型、建筑风格、材料成分、黏结强度、纹理和表面处理、建筑构件、终端用户产业和通路划分-2026-2032年全球预测餐俱生产线市场:依产品类型、材料、价格范围、通路和最终用户划分,全球预测,2026-2032年

水泥市场:依产品类型、建筑风格、材料成分、黏结强度、纹理和表面处理、建筑构件、终端用户产业和通路划分-2026-2032年全球预测餐俱生产线市场:依产品类型、材料、价格范围、通路和最终用户划分,全球预测,2026-2032年 2026年全球注射式水泥市场报告2026年全球磷酸钙水泥市场报告

2026年全球注射式水泥市场报告2026年全球磷酸钙水泥市场报告 日本水泥水泥熟料市场规模、份额、趋势及预测(按类型、通路、应用、最终用途产业及地区划分),2026-2034年水泥市场规模、份额、趋势及预测(按类型、最终用途及地区划分),2026-2034年2026年全球水泥及混凝土製品市场报告2026年全球矿渣水泥市场报告

日本水泥水泥熟料市场规模、份额、趋势及预测(按类型、通路、应用、最终用途产业及地区划分),2026-2034年水泥市场规模、份额、趋势及预测(按类型、最终用途及地区划分),2026-2034年2026年全球水泥及混凝土製品市场报告2026年全球矿渣水泥市场报告 低碳水泥和混凝土产业的成长机会

低碳水泥和混凝土产业的成长机会 水泥及混凝土製品市场-全球产业规模、份额、趋势、机会及预测(按类型、产品、应用、地区及竞争格局划分,2021-2031年)

水泥及混凝土製品市场-全球产业规模、份额、趋势、机会及预测(按类型、产品、应用、地区及竞争格局划分,2021-2031年)